|

시장보고서

상품코드

1773431

카테터 안정화 기기 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Catheter Stabilization Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

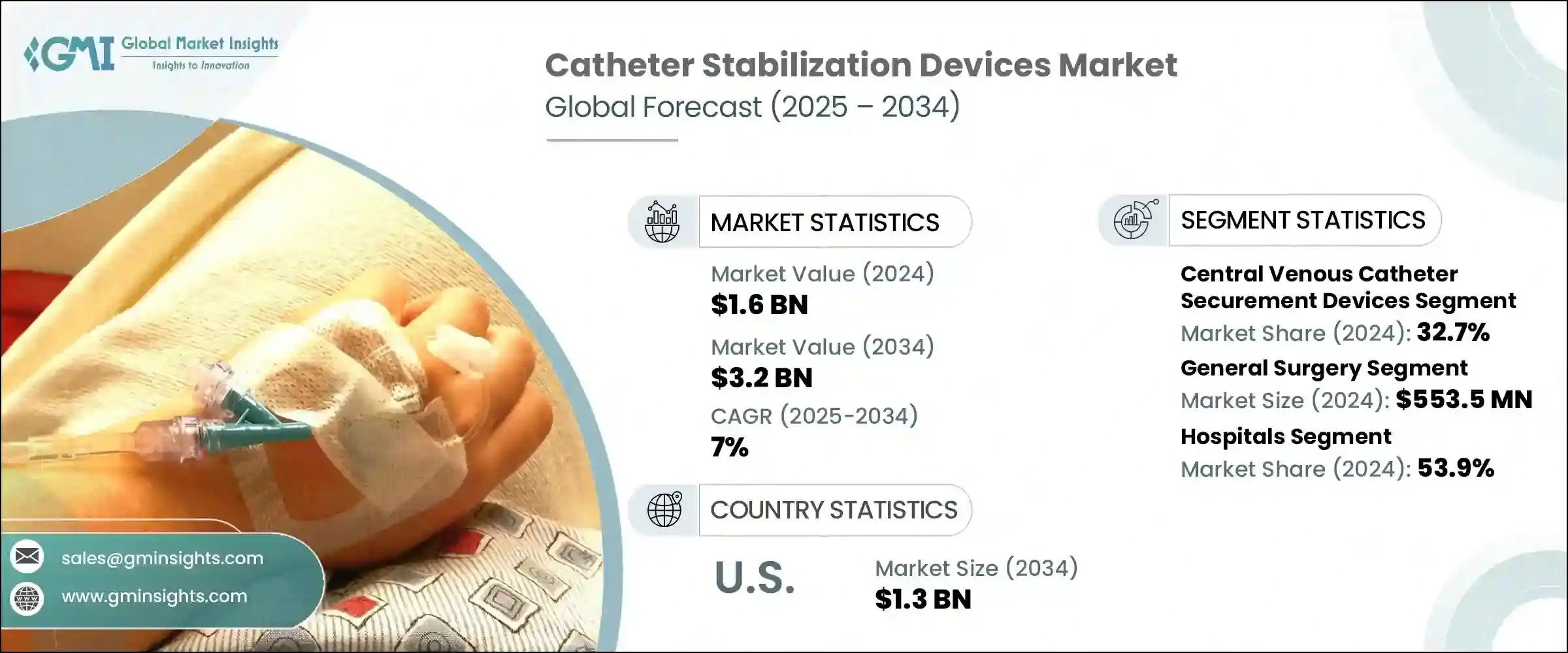

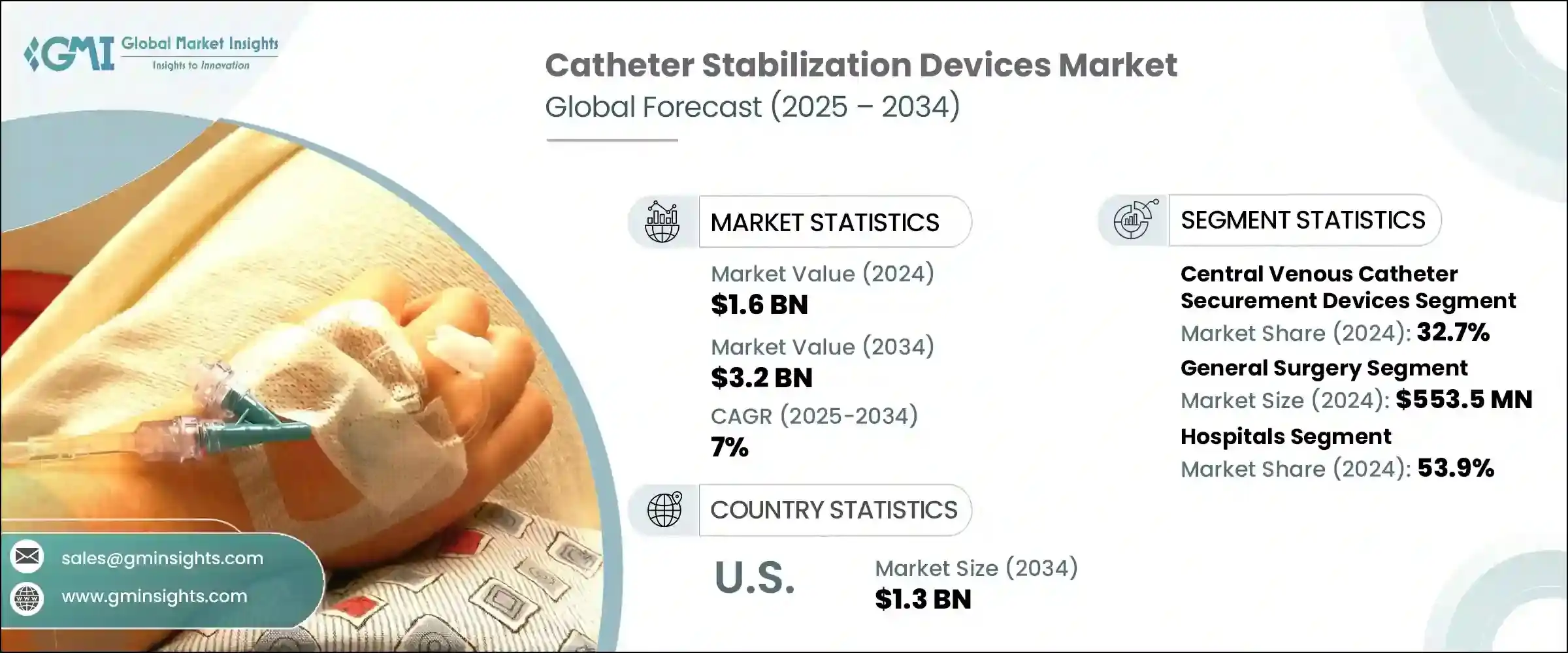

카테터 안정화 기기 세계 시장 규모는 2024년에 16억 달러로 평가되었고, CAGR 7%로 성장하여 2034년에는 32억 달러에 이를 것으로 예측됩니다.

카테터 안정화 기기는 임상 치료에 필수적인 도구로, 다양한 유형의 카테터를 신체에 단단히 고정하고 움직임을 억제하여 이탈을 방지하고 이동의 위험을 줄 이도록 설계되었습니다. 이러한 안정성은 환자를 보호할 뿐만 아니라 정확하고 중단 없는 치료를 가능하게 합니다. 암, 신부전, 당뇨병, 심혈관 질환과 같은 만성 질환이 전 세계적으로 확산됨에 따라 임상 현장에서 카테터의 장기적인 사용의 필요성이 증가하고 있습니다.

또한, 병원에서는 감염 대책이 점점 더 우선순위가 되고 있으며, 고정 방법의 개선을 통해 카테터 관련 감염을 예방하는 데 점점 더 많은 초점을 맞추었습니다. 카테터를 이용한 시술과 재택 간호 지원이 자주 필요한 고령화도 이 시장 확대에 더욱 기여하고 있습니다. 노인은 피부가 약하고 감염에 취약하기 때문에 안전하고 편안한 카테터 고정에 대한 필요성이 증가하고 있습니다. 따라서, 특히 장기 및 재택치료 서비스를 제공하는 시설에서 고품질, 간편한 착용이 가능한 안정화 장치에 대한 수요가 빠르게 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 16억 달러 |

| 예측 금액 | 32억 달러 |

| CAGR | 7% |

2024년에는 장치 부문이 32.7%의 점유율을 차지했습니다. 이러한 카테터는 집중치료, 종양학, 응급의료에서 약물 투여 및 영양 공급과 같은 중요한 치료에 광범위하게 적용되고 있습니다. 이러한 임상 영역에서 고급 치료에 대한 수요가 증가함에 따라 카테터 이동 및 오염으로 인한 혈류 감염, 심내막염, 패혈증과 같은 합병증을 최소화하기 위해 고정기구가 필수적입니다. 이러한 위험을 줄이기 위해 의료 기관 및 관리 단체는 보다 엄격한 감염 관리 프로토콜을 시행하고 있으며, 대부분 카테터 고정 도구의 사용을 의무화하고 있습니다. 이러한 규제 변화로 인해 여러 의료 현장에서 고정기구의 채택이 증가하고 있습니다.

일반 수술 부문은 2024년 5억 5,350만 달러의 수익을 창출했습니다. 카테터는 마취 투여, 체액 모니터링, 활력 징후 추적 등 외과 수술에 광범위하게 사용됩니다. 안정화 장치는 수술 중 및 수술 후 관리, 특히 수술실에서 회복실로 이동하는 동안 카테터의 위치를 안정적으로 유지하기 위해 필수적입니다. 병원은 수술 중 자주 발생하는 중심정맥관 관련 혈류 감염 및 수술 부위 감염의 발생률을 낮춰야 합니다. 따라서 병원의 안전 조치에 부합하고 수술 결과를 개선할 수 있는 안정화 솔루션에 대한 수요가 증가하고 있습니다.

미국 카테터 안정화 기기 2024년 시장 규모는 6억 6,750만 달러였으며, 2034년에는 13억 달러에 달할 것으로 예측됩니다. 미국 전역에 만성질환 환자가 증가함에 따라 카테터를 이용한 치료의 필요성이 증가하고 있으며, 이에 따라 안정화 장치의 채택이 증가하고 있습니다. 미국 병원은 다양한 의료 단체가 정한 엄격한 안전 규정을 따르고 있으며, 시설은 표준화된 감염 관리 방법을 사용하도록 의무화되어 있습니다. 이러한 안전 기준을 준수하지 않을 경우, 의료 기관은 진료비 삭감 및 금전적 처벌을 받을 수 있기 때문에 의료 기관은 고정식 기기에 대한 투자를 장려하고 있습니다. 이러한 추세는 미국을 전 세계 카테터 안정화 분야의 주요 성장 지역으로 자리매김하고 있습니다.

현재 BD, 3M, Cardinal Health, ConvaTec, B. Braun 등의 기업이 시장을 지배하고 있으며, 총 65% 시장 점유율을 차지하고 있습니다. 카테터 안정화 기기 시장의 주요 기업들은 다양한 전략을 통해 존재감을 높이고 장기적인 성장을 보장하고 있습니다. 주요 초점은 감염 위험을 줄이고, 적용을 용이하게 하며, 환자 친화적인 첨단 제품 개발에 초점을 맞추었습니다.

각 회사는 특정 의료 수요에 대응하고 노인과 같은 취약한 환자 그룹을 위한 혁신적인 디자인을 제공하기 위해 연구개발 노력을 강화하고 있습니다. 파트너십, 현지 제조 및 전략적 유통 계약을 통한 지리적 확장은 제품 라인에 대한 접근성을 확대하는 데 도움이 되고 있습니다. 규제 준수 또한 주요 초점이며, 회사는 진화하는 임상 표준을 준수하여 의료기관의 신뢰도를 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술 및 혁신 상황

- 현재 기술 동향

- 신기술

- 상환 시나리오

- 상환 정책이 시장 성장에 미치는 영향

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 소비자 행동 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 제품별, 2021년-2034년

- 주요 동향

- 동맥 고정 기기

- 중심 정맥 카테터 고정기구

- 주변 고정 기기

- 요도 카테터 고정 기기

- 흉부 배액관 고정 기기

- 기타 제품

제6장 시장 추산·예측 : 용도별, 2021년-2034년

- 주요 동향

- 심장혈관 수술

- 일반외과

- 비뇨기 시술

- 종양학 시술

- 기타 용도

제7장 시장 추산·예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 홈케어 환경

- 기타 용도

제8장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 일본

- 중국

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 개요

- B. Braun

- Baxter International

- Becton, Dickinson and Company

- Cardinal Health

- Centurion Medical Products

- ConvaTec

- Dale Medical Products

- DeRoyal Industries

- Merit Medical Systems

- Pepper Medical

- Smiths Medical

- TIDI Products

- VYGON

- Zibo Qichuang Medical Products

- 3M

The Global Catheter Stabilization Devices Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 3.2 billion by 2034. Catheter stabilization devices are essential tools in clinical care, designed to securely anchor various types of catheters to the body, reducing movement, preventing dislodgement, and lowering the risk of migration. This stability not only safeguards the patient but also ensures accurate and uninterrupted delivery of medical treatments. The increasing global prevalence of chronic illnesses such as cancer, kidney failure, diabetes, and cardiovascular conditions is driving the need for long-term catheter use in clinical settings.

In addition, as infection control becomes a growing priority in hospitals, there is an increasing focus on preventing catheter-related infections through improved securement methods. An aging population that frequently requires catheter-based procedures and home care support further contributes to this market's expansion. Fragile skin and susceptibility to infections in older adults heighten the need for secure and comfortable catheter fixation. The demand for high-quality, easy-to-apply stabilization devices is therefore rising rapidly, especially across facilities providing long-term and in-home healthcare services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 7% |

In 2024, the devices segment held a 32.7% share. These catheters are widely applied in intensive care, oncology, and emergency care for critical treatments such as drug administration and nutritional support. With the rise in demand for advanced therapies in these clinical areas, securement devices have become essential in minimizing complications like bloodstream infections, endocarditis, and septic conditions that stem from catheter movement or contamination. To reduce these risks, healthcare institutions and governing bodies have enforced stricter infection control protocols, many of which mandate the use of catheter securement tools. These regulatory shifts are boosting the adoption of securement devices across multiple care settings.

The general surgery segment generated USD 553.5 million in 2024. Catheters are used extensively in surgical procedures for delivering anesthesia, monitoring fluids, and tracking vital signs. Stabilization devices are indispensable in ensuring catheter placement remains intact during surgeries and post-operative care, especially during transitions from operating theaters to recovery areas. Hospitals are under pressure to lower rates of central line-associated bloodstream infections and surgical site infections, which often occur during surgical interventions. This is intensifying the demand for stabilization solutions that align with hospital safety initiatives and improve procedural outcomes.

U.S. Catheter Stabilization Devices Market was valued at USD 667.5 million in 2024 and is expected to reach USD 1.3 billion by 2034. Rising chronic disease cases across the country are driving the need for catheter-based treatments, and in turn, increasing the adoption of stabilization devices. U.S. hospitals follow stringent safety regulations set by various healthcare bodies, which require institutions to use standardized infection control practices. Failure to comply with these safety benchmarks could lead to reduced reimbursement and financial penalties, prompting providers to invest in securement devices. These trends are firmly positioning the U.S. as a key growth region in the global catheter stabilization space.

Companies such as BD, 3M, Cardinal Health, ConvaTec, and B. Braun currently dominate the industry and collectively hold around 65% of the total market share. Leading players in the catheter stabilization devices market are leveraging multiple strategies to boost their presence and secure long-term growth. A primary focus lies in the development of advanced, patient-friendly products that reduce infection risk and enhance application ease.

Companies are strengthening their R&D efforts to deliver innovative designs that cater to specific medical needs and accommodate fragile patient populations, such as the elderly. Geographic expansion through partnerships, local manufacturing, and strategic distribution agreements helps widen access to their product lines. Regulatory compliance is also a major focus, as firms align with evolving clinical standards to increase institutional trust.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of chronic diseases

- 3.2.1.2 Global aging population

- 3.2.1.3 Continuous innovations in catheter stabilization technology

- 3.2.1.4 Cost-benefits of securement devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative products

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in surgical procedure volume

- 3.2.3.2 Growing demand for preventing hospital acquired infections

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Price trends

- 3.5.1 By region

- 3.5.2 By product

- 3.6 Future market trends

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Arterial securement devices

- 5.3 Central venous catheter securement devices

- 5.4 Peripheral securement devices

- 5.5 Urinary catheters securement devices

- 5.6 Chest drainage tubes securement devices

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiovascular procedures

- 6.3 General surgery

- 6.4 Urological procedures

- 6.5 Oncology procedures

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Home care settings

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B. Braun

- 9.2 Baxter International

- 9.3 Becton, Dickinson and Company

- 9.4 Cardinal Health

- 9.5 Centurion Medical Products

- 9.6 ConvaTec

- 9.7 Dale Medical Products

- 9.8 DeRoyal Industries

- 9.9 Merit Medical Systems

- 9.10 Pepper Medical

- 9.11 Smiths Medical

- 9.12 TIDI Products

- 9.13 VYGON

- 9.14 Zibo Qichuang Medical Products

- 9.15 3M