|

시장보고서

상품코드

1773473

프로바이오틱스 기반 영양보조식품 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Probiotics Based Dietary Supplement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

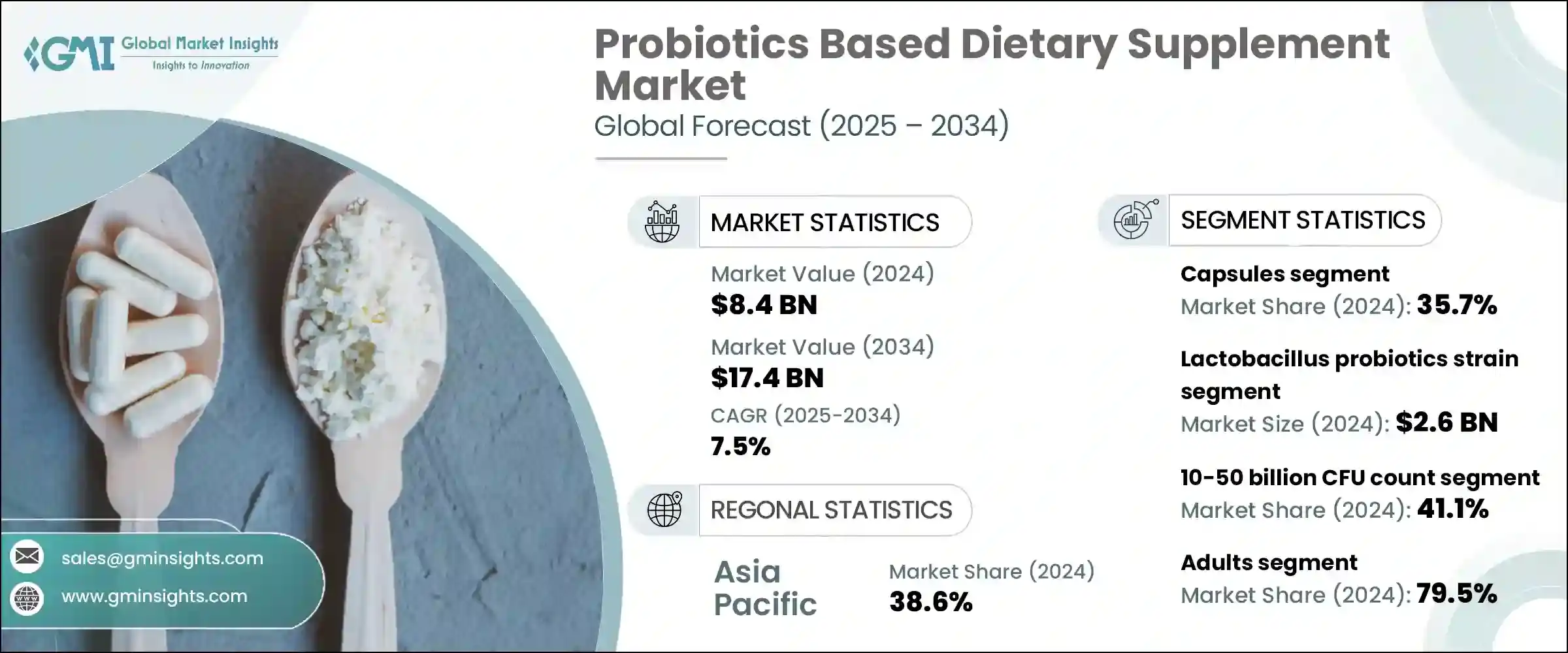

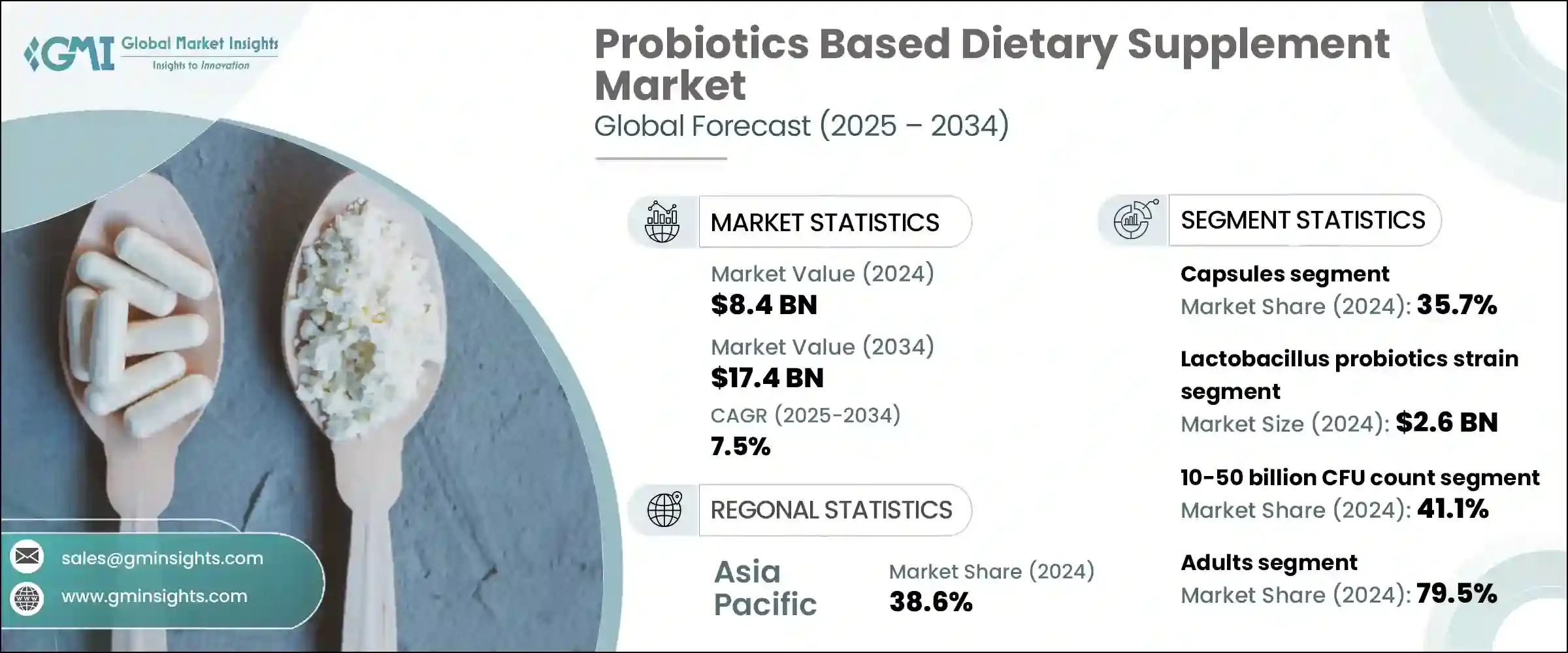

세계의 프로바이오틱스 기반 영양보조식품 시장은 2024년에는 84억 달러로 평가되었으며 CAGR 7.5%를 나타내 2034년에는 174억 달러에 이를 것으로 추정됩니다.

유산균, 비피더스균, 사카로미세스 등의 살아있는 균주로 만들어진 이러한 보충제는 소화의 균형을 지원하고 면역력을 높이고 장과 뇌의 건강을 강화합니다. 소비자는 높은 CFU, 멀티 스트레인 제제, 구미나 파우치등의 편리한 형태를 선택하고 있습니다. 유아, 노인, 건강 지향의 성인, 특히 북미와 아시아태평양을 중심으로 이용이 퍼지고 있기 때문에 임상 검증, 전달 시스템, 클린 라벨 제품에 혁신의 여지가 태어났습니다.

유제품 사용, 투명성에 중점을 둔 제품, 지속 가능한 조달로의 전환은 건강 지향과 환경 지향 영양의 광범위한 동향을 반영하며, 프로바이오틱스를 예방적 건강의 중심 기둥으로 자리 매김하고 있습니다. 성분표를 음미하게 되어, 윤리적 가치관이나 식사 제한에 따른 클린 라벨의 처방을 요구하게 되어 있습니다. 가속시켜 각 브랜드에 비유제품 담체, 천연 향료, 생분해성 포장 등의 혁신을 촉진하고 있습니다. 이 진화는 추적성, 환경에 대한 책임, 현대의 라이프 스타일에 맞춘 개별화된 건강 성과 등, 제조업체가 제품 개발에 임하는 방법을 바꾸고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 84억 달러 |

| 예측 금액 | 174억 달러 |

| CAGR | 7.5% |

캡슐은 35.7%의 점유율을 차지하며, 2024년에는 30억 달러에 달했습니다. 프로바이오틱스가 위산에 견디고 장까지 닿는 것을 보증합니다.

유산균 균주는 30.4%의 점유율을 차지하며, 2024년 시장 규모는 26억 달러였습니다. 위산에 강하고, 단일균주와 복수균주의의 블렌드 양쪽에 적응할 수 있는 것으로부터, 유제품 미사용이나 비건의 프로바이오틱스 제품에 인기가 있어, 특히 북미와 아시아 시장에서 보급되고 있습니다.

아시아태평양 프로바이오틱스 기반 영양보조식품 시장은 2024년에 38.6%의 점유율을 차지했습니다. 소비자의 요구를 충족시키기 위해 소매점의 존재감을 높이고, 연구 개발을 확대하고, 유당을 사용하지 않고 식물 유래의 프로바이오틱스 옵션을 제공합니다.

세계적인 주요 혁신자 및 판매자로는 야쿠르트 본사, BioGaia AB, Nestle SA, Danone SA, Chr. Hansen Holding A/S. 등이 있습니다. 대기업은 계통의 다양화와 투명한 표시로 경쟁력을 강화하고 건강 지향적이고 알레르겐에 민감한 소비자들에게 호소하고 있습니다. 또한 장뇌, 면역, 소화기계의 건강강조표시를 검증하기 위한 임상시험에도 투자하고 있습니다. 채식주의 캡슐, 딜레이드 릴리즈 옵션, 구미, 파우더를 포함한 형식 혁신은 광범위한 레이어에 대한 액세스를 확장합니다. 기업은 전자상거래 채널과 소비자 직접 판매 모델을 확대하는 한편, 헬스케어 전문가나 식품 브랜드와 파트너십을 맺어 신뢰성을 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 제품 형식별(2021-2034년)

- 주요 동향

- 캡슐

- 채식 캡슐

- 젤라틴 캡슐

- 서방형 캡슐

- 기타

- 정제

- 씹을 수 있는 정제

- 장용 코팅 정제

- 기타

- 분말

- 일회용 봉지

- 벌크 용기

- 기타

- 액체

- 샷

- 방울

- 기타

- 구미

- 젤라틴 기반

- 펙틴 기반

- 기타

- 기타

제6장 시장 추계·예측 : 프로바이오틱스 균주별(2021-2034년)

- 주요 동향

- 락토바실러스

- L. 애시도필루스

- L. 람노서스

- L. 플랜타룸

- L. 카세이

- L. 루 테리

- 기타

- 비피도 박테리움

- B. 비피 둠

- B. 롱검

- B. 락티스

- B. 브레브

- 기타

- 스트렙토 코커스

- S. 써모 필 루스

- 기타

- 바실러스

- B. 코아굴란스

- B. 서브틸리스

- 기타

- 사카로미세스

- S. 불라디

- 기타

- 다중 균주 제형

- 기타

제7장 시장 추계·예측 : CFU수별(2021-2034년)

- 주요 동향

- 10억 CFU 미만

- 10억-100억 CFU

- 100억-500억 CFU

- 500억 CFU 이상

제8장 시장 추계·예측 : 소비자 층별(2021-2034년)

- 주요 동향

- 성인

- 18-34세

- 35-54세

- 55세 이상

- 어린이

- 유아(0-2세)

- 어린이(3-12세)

- 청소년(13-17세)

제9장 시장 추계·예측 : 건강 앱별(2021-2034년)

- 주요 동향

- 소화기 건강

- 과민성 대장 증후군(IBS)

- 염증성 장 질환(IBD)

- 항생제 관련 설사

- 기타

- 면역 건강

- 여성 건강

- 체중 관리

- 뇌 건강

- 구강 건강

- 기타

제10장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 소매 약국

- 건강 및 웰빙 스토어

- 슈퍼마켓 및 하이퍼마켓

- 온라인 소매

- 전자상거래 플랫폼

- 브랜드 웹사이트

- 온라인 약국

- 직접 판매

- 기타

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Chr. Hansen Holding A/S

- Danone SA(Activia, Actimel)

- Yakult Honsha Co. Ltd.

- Nestle SA(Garden of Life)

- Probi AB

- BioGaia AB

- Probiotics International Ltd(Protexin)

- Lallemand Inc.

- DuPont(IFF)

- Lifeway Foods, Inc.

- Morinaga Milk Industry Co. Ltd.

- Bifodan A/S

- Culturelle(i-Health, Inc.)

- Jarrow Formulas, Inc.

- NOW Foods

The Global Probiotics Based Dietary Supplement Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 17.4 billion by 2034. These supplements, crafted with live strains like Lactobacillus, Bifidobacterium, and Saccharomyces, support digestive balance, bolster immunity, and enhance gut-brain health. Rising awareness around digestive wellness, preventive health, and allergen-free options is spurring demand. Today's consumers are opting for high-CFU, multi-strain formulations, as well as convenient formats like gummies and sachets. Broadening use among infants, seniors, and health-conscious adults-especially across North America and Asia-Pacific-is creating space for innovations in clinical validation, delivery systems, and clean-label offerings.

The shift toward dairy-free, transparency-focused products and sustainable sourcing reflects a wider trend in health-conscious and eco-minded nutrition, positioning probiotics as a central pillar of preventive wellness. Consumers are increasingly scrutinizing ingredient lists, demanding clean-label formulations that align with ethical values and dietary restrictions. This behavioral shift is accelerating the demand for plant-based and allergen-free probiotic supplements, pushing brands to innovate with non-dairy carriers, natural flavorings, and biodegradable packaging. As awareness grows around the gut's role in immunity, mood, and overall vitality, probiotics are no longer viewed as niche supplements but rather as daily essentials. This evolution is transforming how manufacturers approach product development, with traceability, environmental responsibility, and personalized health outcomes tailored to modern lifestyles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $17.4 Billion |

| CAGR | 7.5% |

The capsule segment dominated the market with a 35.7% share, totaling USD 3 billion in 2024. Their success is due to precise dosage, long shelf-life, and ease of use. Vegetarian, gelatin, and delayed-release versions cater to diverse consumer needs, ensuring probiotics survive stomach acid to reach the gut. High-CFU capsule options tailored for digestion, immunity, and mental health are particularly sought after amid growing interest in personalized gut health regimens.

Lactobacillus strains segment made up 30.4% share, worth USD 2.6 billion in 2024. These clinically backed strains-such as L.acidophilus, L.rhamnosus, and L.plantarum-are known for improving gut flora, strengthening immunity, and aiding lactose intolerance. Their resilience against stomach acid and adaptability in both single- and multi-strain blends make them popular in dairy-free and vegan probiotic products, especially prevalent in North American and Asian markets.

Asia-Pacific Probiotics Based Dietary Supplement Market held a 38.6% share in 2024. Growth in this region is driven by increasing digestive and immune health awareness, higher lactose intolerance rates, urbanization, and rising demand for functional foods. Local and international brands are expanding their retail presence and R&D to meet consumer needs, offering lactose-free, plant-based probiotic options. Government-led wellness campaigns, a growing middle class, and the regional popularity of fermented foods are contributing to mass adoption.

Key global innovators and distributors include Yakult Honsha Co., Ltd., BioGaia AB, Nestle S.A., Danone S.A., and Chr. Hansen Holding A/S. Leading firms are sharpening their competitive edge through strain diversification and transparent labeling, appealing to health-conscious and allergen-sensitive consumers. They're also investing in clinical trials to validate gut-brain, immune, and digestive health claims. Format innovation-with vegan capsules, delayed-release options, gummies, and powders-is broadening access across demographics. Companies are expanding e-commerce channels and direct-to-consumer models while forming partnerships with healthcare professionals and food brands to boost credibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Format, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Capsules

- 5.2.1 Vegetarian capsules

- 5.2.2 Gelatin capsules

- 5.2.3 Delayed-release capsules

- 5.2.4 Others

- 5.3 Tablets

- 5.3.1 Chewable tablets

- 5.3.2 Enteric-coated tablets

- 5.3.3 Others

- 5.4 Powders

- 5.4.1 Single-serve sachets

- 5.4.2 Bulk containers

- 5.4.3 Others

- 5.5 Liquids

- 5.5.1 Shots

- 5.5.2 Drops

- 5.5.3 Others

- 5.6 Gummies

- 5.6.1 Gelatin-based

- 5.6.2 Pectin-based

- 5.6.3 Others

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Probiotic Strain, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Lactobacillus

- 6.2.1 L. acidophilus

- 6.2.2 L. rhamnosus

- 6.2.3 L. plantarum

- 6.2.4 L. casei

- 6.2.5 L. reuteri

- 6.2.6 Others

- 6.3 Bifidobacterium

- 6.3.1 B. bifidum

- 6.3.2 B. longum

- 6.3.3 B. lactis

- 6.3.4 B. breve

- 6.3.5 Others

- 6.4 Streptococcus

- 6.4.1 S. thermophilus

- 6.4.2 Others

- 6.5 Bacillus

- 6.5.1 B. coagulans

- 6.5.2 B. subtilis

- 6.5.3 Others

- 6.6 Saccharomyces

- 6.6.1 S. boulardii

- 6.6.2 Others

- 6.7 Multi-strain formulations

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By CFU Count, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Below 1 billion CFU

- 7.3 1-10 billion CFU

- 7.4 10-50 billion CFU

- 7.5 Above 50 billion CFU

Chapter 8 Market Estimates and Forecast, By Consumer Demographics, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Adults

- 8.2.1 18-34 Years

- 8.2.2 35-54 Years

- 8.2.3 55+ Years

- 8.3 Children

- 8.3.1 Infants (0-2 Years)

- 8.3.2 Children (3-12 Years)

- 8.3.3 Adolescents (13-17 Years)

Chapter 9 Market Estimates and Forecast, By Health Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Digestive health

- 9.2.1 Irritable bowel syndrome (IBS)

- 9.2.2 Inflammatory bowel disease (IBD)

- 9.2.3 Antibiotic-associated diarrhea

- 9.2.4 Others

- 9.3 Immune health

- 9.4 Women's health

- 9.5 Weight management

- 9.6 Brain health

- 9.7 Oral health

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Retail pharmacies

- 10.3 Health & wellness stores

- 10.4 Supermarkets & hypermarkets

- 10.5 Online retail

- 10.5.1 E-commerce platforms

- 10.5.2 Brand websites

- 10.5.3 Online pharmacies

- 10.6 Direct selling

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Chr. Hansen Holding A/S

- 12.2 Danone S.A. (Activia, Actimel)

- 12.3 Yakult Honsha Co., Ltd.

- 12.4 Nestle S.A. (Garden of Life)

- 12.5 Probi AB

- 12.6 BioGaia AB

- 12.7 Probiotics International Ltd (Protexin)

- 12.8 Lallemand Inc.

- 12.9 DuPont (IFF)

- 12.10 Lifeway Foods, Inc.

- 12.11 Morinaga Milk Industry Co., Ltd.

- 12.12 Bifodan A/S

- 12.13 Culturelle (i-Health, Inc.)

- 12.14 Jarrow Formulas, Inc.

- 12.15 NOW Foods