|

시장보고서

상품코드

1782094

간질환 치료제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Liver Disease Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

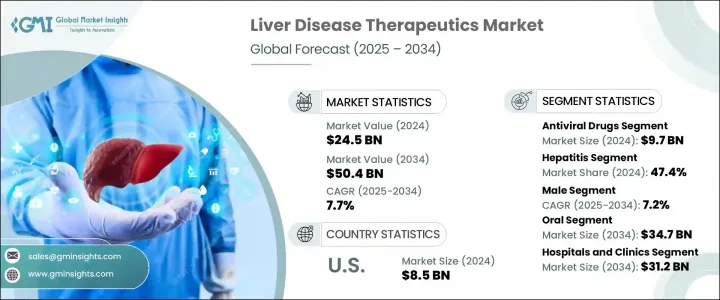

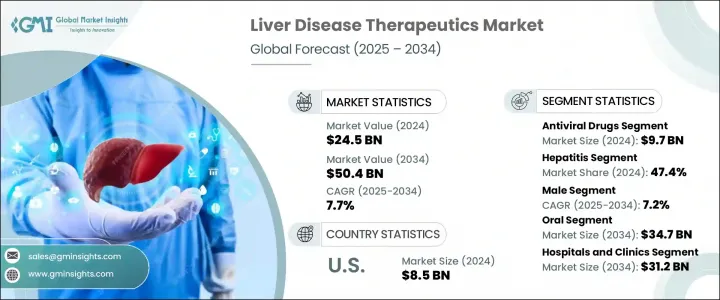

세계의 간 질환 치료제 시장은 2024년에는 245억 달러로 평가되었고 2034년에는 504억 달러에 이를 것으로 예측되며, CAGR 7.7%로 성장할 전망입니다.

세계적으로 간 관련 건강 질환의 유병률이 계속 증가함에 따라 이 시장은 강력한 성장을 보이고 있습니다. 이러한 성장을 주도하는 주요 요인 중 하나는 모든 연령대에서 전 세계적으로 간 질환의 발병률이 증가하고 있다는 점입니다. 만성 및 급성 간 질환은 유전적, 환경적, 생활 습관적 요인의 복합적인 영향으로 점점 더 널리 퍼지고 있습니다.

인구 고령화는 간 질환 치료에 대한 수요 확대에 기여하는 또 다른 중요한 요인입니다. 수명이 연장됨에 따라 간 기능 장애를 비롯한 노화 관련 건강 문제가 점점 더 흔해지고 있습니다. 노인은 알코올 섭취, 처방약 사용, 대사 장애 등 요인에 장기간 노출되어 만성 간 질환에 걸릴 위험이 더 높습니다. 결과적으로 의료 산업은 노인 환자의 간 질환을 특정적으로 치료하는 치료 옵션에 대한 수요가 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 245억 달러 |

| 예측 금액 | 504억 달러 |

| CAGR | 7.7% |

의료 기술의 혁신도 시장 성장에 중요한 역할을 했습니다. 진단 도구의 발전으로 환자 치료 결과에 중요한 조기 발견 및 적시 개입이 가능해졌습니다. 간 질환을 조기에 발견할 수 있는 기술이 점점 더 접근하기 쉽고 신뢰할 수 있게 되어 효과적인 치료에 대한 수요가 촉진되고 있습니다. 또한, 의약품 개발에 대한 지속적인 연구로 복잡한 간 질환을 보다 효과적으로 치료하기 위해 고안된 첨단 치료 제제가 개발되고 있습니다. 이러한 개선은 치료의 폭을 넓히고 시장 규모를 확대하는 데 기여하고 있습니다.

제품별로는 항바이러스제가 2024년에 97억 달러를 차지하며 최고 실적을 기록한 부문으로 부상했습니다. 이 부문이 우위를 차지한 이유는 만성 간 손상 및 관련 합병증의 주요 원인인 바이러스성 간염, 특히 B형 및 C형 간염이 널리 퍼져 있기 때문입니다.

직접 작용 항바이러스제(DAA)는 높은 치료율과 적은 부작용으로 치료의 미래를 크게 변화시켰습니다. 이러한 최근의 치료법은 치료 기간이 짧아 효과적일 뿐만 아니라 환자가 치료를 완료하기 쉽습니다. 효능과 안전성이 더 뛰어난 차세대 항바이러스제가 출시되면서 전 세계적으로, 특히 감염 부담이 높은 지역에서 사용이 가속화되고 있습니다. 임상 결과를 개선하는 능력이 입증된 이 부문은 전체 시장 매출에 주요 기여 요인으로 계속 자리매김하고 있습니다.

질병 유형에 따라 간 질환 치료제 시장은 간염, 자가 면역 질환, 비알코올성 지방간 질환(NAFLD), 암, 유전적 질환 및 기타 범주로 분류됩니다. 간염 부문은 2024년에 47.4%의 상당한 점유율로 시장을 지배했습니다. 이는 주로 효과적인 의료 솔루션에 대한 수요가 계속되고 있는 B형 및 C형 간염의 지속적인 전 세계적 부담에 기인합니다.

지속적인 의약품 혁신으로 치료가 더 쉬워지고 효율성이 높아졌으며, 제형이 개선되어 치료 기간이 단축되고 안전성이 높아졌습니다. 최근의 간염 치료제는 투여 일정이 단순화되고 치료 성공률이 높아져 환자의 치료 순응도가 향상되었습니다. 또한, 기능성 치료제 개발을 위한 지속적인 연구로 간염 부문은 광범위한 치료제 시장에서 선두 위치를 유지하고 있습니다.

성별에 따라 시장은 남성 그룹과 여성 그룹으로 나뉩니다. 2024년에는 남성 인구가 주요 점유율을 차지할 것으로 예상되며, 연평균 7.2%의 성장률을 보일 것으로 전망됩니다. 이러한 동향은 여성에 비해 남성의 간 질환 발병률이 높기 때문에 촉진되고 있습니다. 연구 결과에 따르면 남성은 알코올성 간 질환, NAFLD, 간염 등 만성 간 질환으로 진단받는 비율이 더 높습니다.

이 성별 격차는 생물학적 및 호르몬적 차이와도 연관되어 있습니다. 에스트로겐은 간 조직에 보호 효과를 발휘해 폐경 전 여성은 심각한 간 손상 위험이 낮습니다. 반면 남성은 지방간에서 지방간염, 간경변과 같은 심각한 질환으로 진행될 가능성이 높아 이 인구 집단에서 의료 개입 수요가 증가합니다.

지역별로는 미국이 전 세계 매출에서 가장 큰 비중을 차지하고 있습니다. 미국 시장은 2021년에 75억 달러, 2022년에 78억 달러, 2023년에 81억 달러로 평가되었으며, 2024년에는 85억 달러에 도달할 것으로 예상됩니다. 이러한 지속적인 성장은 간 관련 건강 문제, 특히 비알코올성 지방간 질환(NAFLD)과 그 더 심각한 형태인 비알코올성 지방간염(NASH)의 증가를 반영합니다. 비만의 급증, 앉아있는 생활 방식 및 관련 대사 장애가 요인으로 작용하고 있습니다.

미국의 의료 시스템은 공공 및 민간 보험 프로그램을 통해 조기 진단과 고비용 전문 치료에 대한 접근성을 지원하며, 이는 시장 확대를 촉진하는 요인으로 작용합니다. 인식 향상, 광범위한 검진 노력, 의료 인프라 개선은 모두 해당 국가의 선도적 위치를 강화하는 요인입니다.

전 세계적으로 경쟁 환경은 대규모 다국적 기업, 지역 기업 및 신흥 업체들이 혼재되어 있습니다. 시장 점유율의 약 45-50%는 협력, 인수 및 혁신적인 치료법 출시를 통해 시장 입지 확대에 적극적으로 나서고 있는 4개의 선도 기업이 차지하고 있습니다. 이 기업들은 미충족 임상 요구를 해결하고 환자 치료 결과를 개선하기 위해 연구 개발에 막대한 투자를 하고 있으며, 빠르게 성장하는 업계에서 전략적 우위를 차지하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 간 질환의 유병률 증가

- 진단 기술의 진보

- 앉아있는 생활 방식, 잘못된 식습관, 알코올 섭취의 증가

- 업계의 잠재적 위험 및 과제

- 특히 생물학적 제제의 높은 치료 비용

- 특정 의약품의 부작용 및 제한된 효능

- 시장 기회

- 비알코올성 지방간염(NASH) 및 간암에 대한 강력한 R&D 파이프라인

- 신흥 시장으로 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 파이프라인 분석

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품별(2011-2034년)

- 주요 동향

- 항바이러스제

- 백신

- 화학요법

- 표적요법

- 면역 억제제

- 면역글로불린

- 코르티코스테로이드

- 기타 제품

제6장 시장 추계 및 예측 : 질병 유형별(2011-2034년)

- 주요 동향

- 간염

- 자가면역질환

- 비알코올성 지방성 간질환(NAFLD)

- 암

- 유전성 질환

- 기타 질병의 유형

제7장 시장 추계 및 예측 : 성별별(2011-2034년)

- 주요 동향

- 남성

- 여성

제8장 시장 추계 및 예측 : 투여 경로별(2011-2034년)

- 주요 동향

- 경구

- 비경구

제9장 시장 추계 및 예측 : 최종 용도별(2011-2034년)

- 주요 동향

- 병원 및 진료소

- 외래수술센터(ASC)

- 기타 용도

제10장 시장 추계 및 예측 : 지역별(2011-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Amgen

- AbbVie

- Bristol-Myers Squibb

- Bayer

- GSK plc

- Gilead Sciences

- Hoffmann-La Roche

- Intercept Pharmaceuticals

- Johnson &Johnson Services

- Merck &Co.

- Novartis

- Pfizer

- Sanofi

- Takeda Pharmaceutical Company Limited

- Zydus Lifesciences

The Global Liver Disease Therapeutics Market was valued at USD 24.5 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 50.4 billion by 2034. The market is witnessing robust growth as the prevalence of liver-related health conditions continues to rise worldwide. One of the primary forces fueling this growth is the increasing global incidence of liver diseases across all age groups. Liver conditions, both chronic and acute, are becoming more widespread due to a combination of genetic, environmental, and lifestyle-related factors.

An aging population is another important factor contributing to the expanding demand for liver disease treatments. As people live longer, age-related health issues, including liver dysfunction, are becoming more common. Elderly individuals often face a higher risk of chronic liver problems due to prolonged exposure to factors such as alcohol consumption, use of prescription medications, and metabolic disorders. As a result, the healthcare industry is seeing a greater need for therapeutic options that specifically address liver diseases in older patients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.5 Billion |

| Forecast Value | $50.4 Billion |

| CAGR | 7.7% |

Innovations in medical technology have also played a significant role in supporting market growth. Advancements in diagnostic tools have enabled early detection and timely intervention, which are critical for improving patient outcomes. Technologies that allow for early-stage identification of liver disorders are becoming more accessible and reliable, driving the demand for effective treatments. Furthermore, continuous research in pharmaceutical development is leading to the creation of advanced therapeutic formulations designed to treat complex liver conditions more effectively. These improvements are contributing to broader treatment adoption and helping expand the market size.

By product, antiviral drugs emerged as the top-performing segment, accounting for USD 9.7 billion in 2024. The segment dominates due to the widespread occurrence of viral hepatitis, particularly hepatitis B and C, which remain among the leading causes of chronic liver damage and associated complications.

Direct-acting antiviral agents (DAAs) have significantly changed the treatment landscape by offering high cure rates and fewer side effects. These modern therapies are not only more effective but also easier for patients to complete, thanks to their shorter treatment durations. The launch of next-generation antivirals with better efficacy and safety profiles has accelerated global adoption, especially in regions with high infection burdens. Their proven ability to improve clinical outcomes continues to position this segment as a major contributor to overall market revenues.

In terms of disease type, the liver disease therapeutics market is classified into hepatitis, autoimmune disorders, non-alcoholic fatty liver disease (NAFLD), cancer, genetic conditions, and other categories. The hepatitis segment dominated the landscape with a substantial 47.4% share in 2024. This is largely due to the persistent global burden of hepatitis B and C infections, which continue to demand effective medical solutions.

Ongoing drug innovations have made treatment more accessible and efficient, with improved formulations offering shorter and safer therapeutic regimens. Modern treatments for hepatitis feature simplified dosing schedules and increased cure rates, resulting in improved patient adherence. In addition, continuous research to develop functional cures ensures that the hepatitis segment maintains its lead within the broader therapeutics market.

By gender, the market is divided into male and female groups. In 2024, the male population represented the dominant share and is expected to grow at a CAGR of 7.2%. This trend is driven by a higher incidence of liver conditions among men compared to women. Studies show that men are more frequently diagnosed with chronic liver diseases, including alcoholic liver disease, NAFLD, and hepatitis.

This gender disparity is also linked to biological and hormonal differences. Estrogen is thought to have a protective effect on liver tissue, making premenopausal women less likely to experience severe liver damage. Men, on the other hand, are more prone to disease progression from fatty liver to more serious conditions such as steatohepatitis and cirrhosis, which increases the demand for medical intervention in this demographic.

Regionally, the United States is the largest contributor to global revenues. The U.S. market was valued at USD 7.5 billion in 2021, USD 7.8 billion in 2022, USD 8.1 billion in 2023, and reached USD 8.5 billion in 2024. This consistent growth reflects a rising number of liver-related health issues, particularly non-alcoholic fatty liver disease (NAFLD) and its more severe form, non-alcoholic steatohepatitis (NASH). Contributing factors include a surge in obesity, sedentary lifestyles, and associated metabolic disorders.

The healthcare system in the U.S. supports early diagnosis and access to high-cost specialty treatments through public and private insurance programs, which helps fuel continued market expansion. Increasing awareness, widespread screening efforts, and improved healthcare infrastructure all contribute to the country's leading position.

Globally, the competitive landscape features a mix of large multinational firms, regional companies, and emerging players. Approximately 45% to 50% of the market share is held by four leading companies that are actively engaged in expanding their market presence through collaborations, acquisitions, and the launch of innovative therapies. These companies are investing heavily in research and development to address unmet clinical needs and improve patient outcomes, giving them a strategic advantage in a rapidly growing industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Disease type

- 2.2.4 Gender

- 2.2.5 Route of administration

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of liver diseases

- 3.2.1.2 Advancements in diagnostic technologies

- 3.2.1.3 Rise in sedentary lifestyles, poor diet, and alcohol use

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment, especially for biologics

- 3.2.2.2 Side effects and limited efficacy of certain drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Strong R&D pipeline for nonalcoholic steatohepatitis (NASH) and liver cancer

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antiviral drugs

- 5.3 Vaccines

- 5.4 Chemotherapy

- 5.5 Targeted therapy

- 5.6 Immunosuppressants

- 5.7 Immunoglobulins

- 5.8 Corticosteroids

- 5.9 Other products

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hepatitis

- 6.3 Autoimmune diseases

- 6.4 Non-alcoholic fatty liver disease (NAFLD)

- 6.5 Cancer

- 6.6 Genetic disorders

- 6.7 Other disease types

Chapter 7 Market Estimates and Forecast, By Gender, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Male

- 7.3 Female

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Parenteral

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgical centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amgen

- 11.2 AbbVie

- 11.3 Bristol-Myers Squibb

- 11.4 Bayer

- 11.5 GSK plc

- 11.6 Gilead Sciences

- 11.7 Hoffmann-La Roche

- 11.8 Intercept Pharmaceuticals

- 11.9 Johnson & Johnson Services

- 11.10 Merck & Co.

- 11.11 Novartis

- 11.12 Pfizer

- 11.13 Sanofi

- 11.14 Takeda Pharmaceutical Company Limited

- 11.15 Zydus Lifesciences