|

시장보고서

상품코드

1782156

장 질환 검사 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Enteric Disease Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

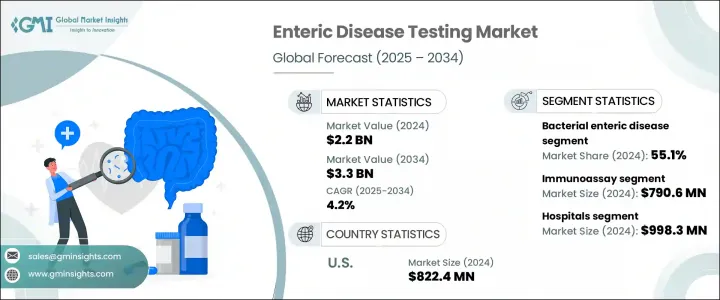

세계의 장 질환 검사 시장은 2024년 22억 달러로 평가되었고, CAGR 4.2%로 성장할 전망이며, 2034년 33억 달러에 이를 것으로 추정됩니다.

이 성장의 원동력은 장내 감염증의 유병률 증가, 인지도 향상, 서베이런스 대처, 진단 검사의 기술적 진보입니다. 장관감염병은 중저소득 국가에서 발생하는 경우가 많으며, 일반적으로 미흡한 위생환경 및 오염된 물과 관련되어 있습니다. 이러한 감염병은 재발을 반복하며 풍토병으로 뿌리 깊게 남아 있기 때문에 시기적절하고 정확한 진단의 필요성이 강조되고 있습니다. 조기 발견은 환자의 전귀를 개선하고 더 나은 질병 관리 노력을 지원하는 효과적인 개입을 촉진하는 데 매우 중요합니다.

또한, 캡슐 내시경, 섭취 가능한 센서, 약물 전달 시스템에 대한 수요 증가는 장내 장치의 정확한 검사의 필요성에 박차를 가하고 있습니다. 여기에는 소화관 구조 내에서의 용출, 통과 시간, 국소 방출 등의 요인 평가가 포함되어 시장 확대를 더욱 촉진하고 있습니다. 장 질환 검사는 소화관에 영향을 미치는 세균, 바이러스, 기생충에 의한 감염증을 특정하기 위해 사용되는 진단법을 말합니다. 검사는 설사, 콜레라, 장티푸스, 이질 등의 상태를 검출하기 위해 사용됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 22억 달러 |

| 예측 금액 | 33억 달러 |

| CAGR | 4.2% |

면역 분석 분야가 시장을 독점하고, 2024년에는 7억 9,060만 달러를 창출했으며, 2034년까지 CAGR 4.3%로 성장할 것으로 예측됩니다. Immunoassays는 장내 병원체의 검출에 널리 사용되고 있으며, 포인트 오브 케어 환경을 포함한 저자원 환경에서 특히 인기가 있습니다. 특히 세균성 독소나 로타바이러스, 노로바이러스 등의 바이러스 감염증의 서베이런스나 아웃브레이크 대응의 주요한 방법이 되고 있습니다.

병원 분야는 2024년에 9억 9,830만 달러의 수익으로 시장을 선도하였고, 2025-2034년 CAGR 4.4%로 성장할 것으로 예측됩니다. 급성기 의료 및 긴급 개입의 주요 센터로서, 병원은 특히 식중독과 관련된 많은 심각한 위장 증례를 다룹니다. 대부분의 긴급 사례는 병원의 실험실에서 처리되지만 이것은 장 질환 검사입니다.

미국 장 질환 검사 시장은 2024년 8억 2,240만 달러로 평가됐습니다. 이 나라에서는 살모넬라, 대장균, 노로바이러스 등의 병원체를 원인으로 하는 식중독이 연간 수백만 건 발생하고 있습니다. 이 공중 보건 문제를 해결하려면 정기적이고 정확한 장 질환 검사가 필요합니다. CDC 및 FDA의 FoodNet 및 PulseNet과 같은 조직 프로그램은 아웃 브레이크 감지 및 고급 진단 검사 개발에 중요한 역할을 합니다. 이 기관들은 진단 속도와 정확성을 향상시키는 데 필요한 기술 혁신을 추진하고 있습니다.

장 질환 검사 시장의 주요 기업은 Abbott Laboratories, Becton, Dickinson and Company, Biomerica, bioMerieux, Bio-Rad Laboratories, Coris BioConcept, Danaher, DiaSorin, Merck KGaA, Meridian Bioscience, Techlab, Thermo Fisher Scientific 등이 있습니다. 장 질환 검사 시장에서의 지위를 강화하기 위해 각 회사는 지속적인 혁신과 첨단 진단 기술의 개발에 주력하고 있습니다. 이것에는 연구 개발(R&D)에 대한 고액의 투자가 포함되어, 특히 포인트 오브 케어 환경 전용의 검사 키트의 정밀도, 스피드, 사용하기 쉬움을 향상시키고 있습니다. 또한 정부기관, 연구기관, 헬스케어 공급자와의 전략적 제휴도 시장 확대의 열쇠가 됩니다. 기업들은 또한 저렴한 가격에 사용하기 쉬운 진단 솔루션을 제공함으로써 장 질환 발생률이 높은 신흥 시장에서의 존재감을 높이고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 장 질환의 이환율 증가

- 진단 기술의 기술적 진보

- 예방 헬스케어 서비스 수요 증가

- 헬스케어비 및 투자 증가

- 업계의 잠재적 위험 및 과제

- 장 질환 검사와 관련된 높은 비용

- 테스트 절차의 복잡성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 미국

- 유럽

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 질환별(2021-2034년)

- 주요 동향

- 세균성 장 질환

- 살모넬라

- 대장균

- 캄필로박터

- 크로스트리듐 디피실

- 세균성 이질

- 리스테리아

- 바이러스성 장 질환

- 로타바이러스 감염증

- 노로바이러스 감염증

- 기생충성 장질환

- 디알디아증

- 아메바증

- 크립토스포리듐증

제6장 시장 추계 및 예측 : 검사 유형별(2021-2034년)

- 주요 동향

- 면역 측정

- 분자

- 기존

- 크로마토그래피 및 분광분석

- 기타 검사의 유형

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 진단실험실

- 조사 및 학술 기관

- 기타 최종 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott Laboratories

- Becton, Dickinson and Company

- Biomerica

- bioMerieux

- Bio-Rad Laboratories

- Coris BioConcept

- Danaher

- DiaSorin

- Merck KGaA

- Meridian Bioscience

- Techlab

- Thermo Fisher Scientific

The Global Enteric Disease Testing Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 3.3 billion by 2034. This growth is driven by the increasing prevalence of enteric infections, greater awareness, surveillance initiatives, and technological advancements in diagnostic testing. Enteric diseases, often occurring in low- and middle-income countries, are commonly linked to inadequate sanitation and contaminated water. These infections are recurrent, with endemic persistence, highlighting the need for timely, accurate diagnostics. Early detection is crucial in facilitating effective interventions that improve patient outcomes and support better disease control efforts.

Additionally, the rise in demand for capsule endoscopy, ingestible sensors, and drug delivery systems has spurred the need for accurate testing of enteric devices. This includes evaluating factors like dissolution, transit time, and localized release within gastrointestinal structures, further driving market expansion. Enteric disease testing refers to diagnostic methods used to identify infections caused by bacteria, viruses, or parasites that affect the digestive tract. Tests are used to detect conditions like diarrhea, cholera, typhoid, and dysentery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 4.2% |

The immunoassay segment dominated the market, generating USD 790.6 million in 2024, and is projected to grow at a CAGR of 4.3% through 2034. Immunoassays are widely used for detecting enteric pathogens and are particularly prevalent in low-resource settings, including point-of-care environments. They are the primary method for surveillance and outbreak response, especially for bacterial toxins and viral infections like rotavirus and norovirus.

The hospitals segment led the market in 2024 with a revenue of USD 998.3 million and is expected to grow at a CAGR of 4.4% during 2025-2034. As major centers for acute care and emergency interventions, hospitals handle many severe gastrointestinal cases, especially those related to foodborne diseases. Most urgent cases are processed in hospital-based labs, reflecting the crucial role of these institutions in enteric disease testing.

U.S. Enteric Disease Testing Market was valued at USD 822.4 million in 2024. The country sees millions of foodborne illness cases annually, driven by pathogens like Salmonella, E. coli, and Norovirus. Addressing this public health challenge requires regular, accurate enteric disease testing. Programs from organizations like the CDC and FDA, such as FoodNet and PulseNet, play a vital role in outbreak detection and the development of advanced diagnostic tests. These agencies drive the innovation necessary to improve diagnostic speed and accuracy.

Key players in the Enteric Disease Testing Market include Abbott Laboratories, Becton, Dickinson and Company, Biomerica, bioMerieux, Bio-Rad Laboratories, Coris BioConcept, Danaher, DiaSorin, Merck KGaA, Meridian Bioscience, Techlab, and Thermo Fisher Scientific. To strengthen their position in the enteric disease testing market, companies are focusing on continuous innovation and the development of advanced diagnostic technologies. This includes investing heavily in research and development (R&D) to improve the accuracy, speed, and ease of use of testing kits, particularly for point-of-care settings. Strategic collaborations with government agencies, research institutions, and healthcare providers are also key to expanding their market footprint. Companies are also increasing their presence in emerging markets where the incidence of enteric diseases is high by providing affordable, easy-to-use diagnostic solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Disease trends

- 2.2.3 Test type trends

- 2.2.4 End use trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of enteric diseases

- 3.2.1.2 Technological advancements in diagnostic technologies

- 3.2.1.3 Growing demand for preventive healthcare services

- 3.2.1.4 Rising healthcare expenditure and investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with enteric disease testing

- 3.2.2.2 Complexity of testing procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Bacterial enteric disease

- 5.2.1 Salmonella

- 5.2.2 E. coli

- 5.2.3 Campylobacter

- 5.2.4 C. difficile

- 5.2.5 Shigellosis

- 5.2.6 Listeria

- 5.3 Viral enteric disease

- 5.3.1 Rotavirus infection

- 5.3.2 Norovirus infection

- 5.4 Parasitic enteric disease

- 5.4.1 Giardiasis

- 5.4.2 Amebiasis

- 5.4.3 Cryptosporidiosis

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunoassay

- 6.3 Molecular

- 6.4 Conventional

- 6.5 Chromatography & spectrometry

- 6.6 Other test types

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic laboratories

- 7.4 Research & academic institutes

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Becton, Dickinson and Company

- 9.3 Biomerica

- 9.4 bioMerieux

- 9.5 Bio-Rad Laboratories

- 9.6 Coris BioConcept

- 9.7 Danaher

- 9.8 DiaSorin

- 9.9 Merck KGaA

- 9.10 Meridian Bioscience

- 9.11 Techlab

- 9.12 Thermo Fisher Scientific