|

시장보고서

상품코드

1797698

농축 캔 수프 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Condensed Canned Soups Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

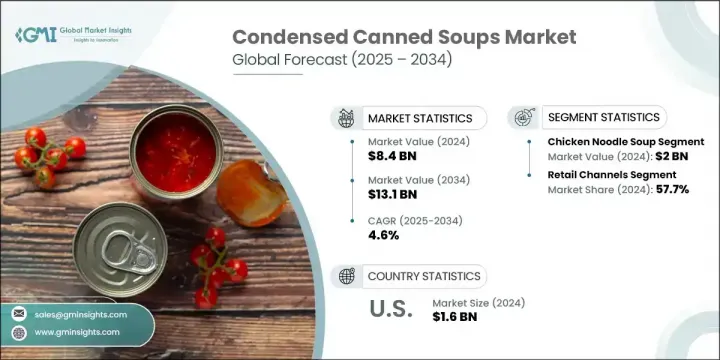

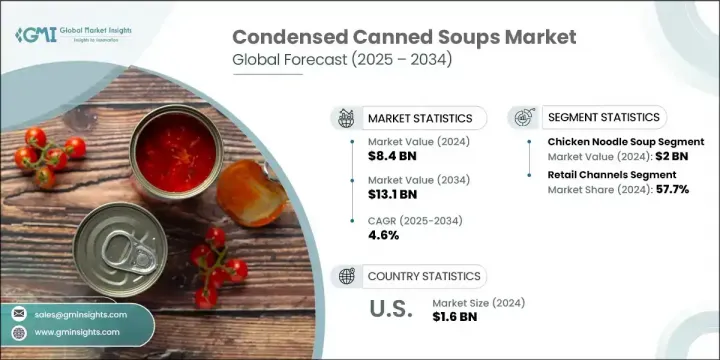

세계의 농축 캔 수프 시장은 2024년에 84억 달러로 평가되어 CAGR 4.6%로 성장할 전망이며 2034년에는 131억 달러에 이를 것으로 추정되고 있습니다.

이러한 수프는 경제성, 간편한 조리법, 긴 유통기한 덕분에 포장 식품 시장에서 여전히 주요 품목으로 자리 잡고 있습니다. 그러나 소비자 선호도가 상당한 변화를 보임에 따라 브랜드들은 제품 포트폴리오를 재구상해야 하는 상황에 직면했습니다. 점점 더 많은 소비자들이 클린 라벨, 천연 재료, 건강 중심 제품을 선택함에 따라 저나트륨 함량, 유기농 인증, 식물성 원료를 강조하는 제품 개편이 이루어지고 있다. 식품 제조업체들은 단순한 편의성 이상의 가치를 제공하는 영양 풍부하고 단백질 강화된 농축 수프로 혁신을 가속화하고 있다.

이러한 제품들은 이제 즉석식사뿐만 아니라 가정 요리 레시피의 다용도 베이스로도 포지셔닝되고 있습니다. 건강을 중시하는 식습관으로 전환하는 소비자가 늘어남에 따라, 강화되고 맞춤화가 가능한 식사 구성 요소에 대한 수요가 가속화되고 있습니다. 이 동향은 특히 아시아태평양 지역을 중심으로 급속히 도시화되는 지역에서 두드러지며, 성장하는 중산층과 빠른 속도의 생활 방식이 영양가 높고 시간을 절약해주는 식사에 대한 수요 증가를 촉진하고 있습니다. 이 지역의 국가들은 변화하는 식습관에 부합하는 편리한 식품 옵션으로 광범위한 전환의 일환으로 농축 수프 소비가 크게 증가하는 것을 목격하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 84억 달러 |

| 예측 금액 | 131억 달러 |

| CAGR | 4.6% |

치킨 누들 수프 부문은 2024년 20억 달러의 매출을 기록했습니다. 토마토, 크림 버섯, 치킨 크림 수프 등 다른 인기 품목들도 단독 식사나 다양한 요리 재료로 활용되며 안정적인 수요를 보이고 있습니다. 건강에 좋은 옵션에 대한 관심이 높아지면서 채소 및 쇠고기 기반 수프의 성장도 촉진되고 있으며, 식물성 중심 및 고단백 선택지도 주목받고 있습니다. 최근 소비자의 기대에 부응하기 위해 브랜드들은 유기농, 알레르기 유발 물질이 적은, 저염 레시피를 도입하기 위해 전통적인 조리법을 재검토하며 맛이나 질감을 손상시키지 않으면서 건강을 중시하는 고객층에게 어필하고 있습니다.

소매점 부문은 2024년 57.7%의 점유율을 차지했습니다. 슈퍼마켓, 대형마트, 동네 식료품점은 여전히 주요 유통 채널로 자리매김하며 소비자에게 다양한 브랜드, 가격대, 맛을 제공합니다. 이러한 매장들은 눈에 띄는 제품 진열, 계절별 프로모션, 강력한 자사 브랜드 경쟁을 통해 구매 행동에 영향을 미치며 주류 구매자에게 여전히 중요한 채널로 기능합니다.

북미의 농축 캔 수프 시장은 2024년에 16억 달러를 창출했는데, 이것은 캔이 들어간 수프에 대한 문화적인 친밀감이 강한 것이 요인입니다. 식습관 변화와 건강 의식 증대로 미국 시장은 클린 라벨, 유기농, 식물성 수프에 대한 확고한 수요를 보이고 있습니다. 잘 구축된 유통망과 고급 식품 가공 및 기술에 대한 투자를 바탕으로 미국 기업들은 신흥 동향에 신속히 대응하며 이 분야의 혁신 선두를 유지하고 있습니다.

세계의 농축 캔 수프 시장에 기여하는 주요 기업은 Nestle SA, Amy's Kitchen Inc., BCI Foods Inc., The Kraft Heinz Company, Unilever(Knorr), Campbell Soup Company, General Mills Inc., ConAgra Brands Inc., Baxters Food Group, Vanee Food 농축 캔 수프 시장의 선도 브랜드들은 재포뮬레이션을 통한 제품 다각화를 최우선 과제로 삼고 있으며, 저나트륨, 유기농, 글루텐 프리, 식물성 기반 제품군을 출시하고 있습니다. 많은 기업들이 지속 가능한 포장에 투자하고 변화하는 소비자 선호도를 충족시키기 위해 풍미 프로필을 개선하고 있습니다. 슈퍼푸드, 식물성 단백질, 알레르기 유발 성분이 적은 원료를 통합하기 위한 연구개발(R&D) 역시 혁신을 촉진하고 있습니다. 또한 브랜드들은 공급망을 최적화하고 소매 파트너십을 확대하여 진열대 가시성을 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 촉진요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 제품 유형별 동향

- 유통 채널의 동향

- 포장 형태의 동향

- 지역별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산 에너지 효율

- 환경 친화적 인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측, 제품 유형별(2021-2034년)

- 주요 동향

- 농축 스프의 유형

- 치킨 누들 스프

- 토마토 수프

- 크림 버섯 수프

- 치킨 크림 스프

- 야채 스프

- 쇠고기 기반 수프

- 크림 기반 특제 스프

제6장 시장 추계 및 예측, 유통 채널별(2021-2034년)

- 주요 동향

- 소매 채널

- 슈퍼마켓 및 대형 슈퍼마켓

- 편의점

- 할인 소매업체

- 전문 식품점

- 온라인 소매 및 전자상거래

- 푸드서비스 채널

- 레스토랑과 패스트푸드점

- 시설 내 푸드서비스

- 의료 및 교육시설

- 소비자 직접 판매 채널

제7장 시장 추계 및 예측, 포장 형태별(2021-2034년)

- 주요 동향

- 기존 금속캔

- 표준 사이즈 캔(10.5-11 온스)

- 패밀리 사이즈 캔(18-23온스)

- 업무용 사이즈 캔

- 대체 포장 형식

- 플렉서블 파우치와 스탠드업 파우치

- 무균 카톤 및 테트라팩

- 전자레인지용 용기

- 일회용 컵 및 그릇

제8장 시장 추계 및 예측, 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Campbell Soup Company

- General Mills Inc.(Progresso)

- The Kraft Heinz Company

- Nestle SA

- Unilever(Knorr)

- ConAgra Brands Inc.

- Baxters Food Group

- BCI Foods Inc.

- Vanee Foods Company

- Amy's Kitchen Inc

The Global Condensed Canned Soups Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 13.1 billion by 2034. These soups remain a staple in the packaged food space due to their affordability, ease of preparation, and extended shelf stability. However, consumer preferences have evolved significantly, pushing brands to reimagine their offerings. A growing number of consumers are opting for cleaner labels, natural ingredients, and health-focused variants, leading to product reformulations that emphasize low-sodium content, organic certification, and plant-based ingredients. Food manufacturers are increasingly innovating with nutrient-rich, protein-enhanced condensed soups that offer more than just convenience.

These products are now positioned not only as ready-to-eat meals but also as versatile bases for home-cooked recipes. As more consumers shift toward health-conscious eating, the demand for enriched, customizable meal components has accelerated. This trend is particularly prominent in rapidly urbanizing areas, especially across the Asia-Pacific region, where a growing middle class and fast-paced lifestyles are fueling increased demand for nutritious, time-saving meals. Countries in the region are witnessing a strong uptake in condensed soup consumption as part of the broader shift toward convenient food options that align with evolving dietary habits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 4.6% |

The chicken noodle soup segment generated USD 2 billion in 2024. Other popular varieties include tomato-based, cream of mushroom, and cream of chicken soups, which have proven to be reliable both as standalone meals and as ingredients in broader meal preparation. Rising interest in better-for-you options is also driving growth in vegetable and beef-based soups, while plant-forward and high-protein selections are gaining traction. To align with modern consumer expectations, brands are revisiting traditional formulations to introduce organic, allergen-friendly, and reduced-sodium recipes, expanding their appeal to health-conscious audiences without compromising flavor or texture.

The retail outlets segment held a 57.7% share in 2024. Supermarkets, hypermarkets, and neighborhood grocery stores remain the dominant distribution channels, offering consumers access to various brands, prices, and flavors. These stores benefit from prominent product placement, seasonal promotions, and strong private-label competition, which influence purchasing behavior and keep this channel highly relevant for mainstream buyers.

North American Condensed Canned Soups Market generated USD 1.6 billion in 2024, driven by strong cultural familiarity with canned soups. With changing eating habits and increasing health awareness, the U.S. market shows a solid appetite for clean-label, organic, and plant-based soups. A well-established retail network, along with investments in advanced food processing and technology, allows American companies to respond quickly to emerging trends, keeping the U.S. at the forefront of innovation in this sector.

Key players contributing to the Global Condensed Canned Soups Market include Nestle S.A., Amy's Kitchen Inc., BCI Foods Inc., The Kraft Heinz Company, Unilever (Knorr), Campbell Soup Company, General Mills Inc., ConAgra Brands Inc., Baxters Food Group, and Vanee Foods Company. Leading brands in the condensed canned soups market are prioritizing product diversification through reformulation, introducing low-sodium, organic, gluten-free, and plant-based varieties. Many companies are investing in sustainable packaging and enhancing flavor profiles to meet evolving consumer preferences. Innovation is also fueled by R&D to integrate superfoods, plant proteins, and allergen-friendly ingredients. In addition, brands are optimizing supply chains and expanding retail partnerships for better shelf visibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Distribution channel trends

- 2.2.3 Packaging format trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By product type trends

- 3.8.2 By distribution channel trends

- 3.8.3 By packaging format trends

- 3.8.4 By region

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Condensed soup varieties

- 5.2.1 Chicken noodle soup

- 5.2.2 Tomato soup

- 5.2.3 Cream of mushroom soup

- 5.2.4 Cream of chicken soup

- 5.2.5 Vegetable soup

- 5.2.6 Beef-based soups

- 5.2.7 Cream-based specialty soups

Chapter 6 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Retail channels

- 6.2.1 Supermarkets and hypermarkets

- 6.2.2 Convenience stores

- 6.2.3 Discount retailers

- 6.2.4 Specialty food stores

- 6.2.5 Online retail and e-commerce

- 6.3 Foodservice channels

- 6.3.1 Restaurants and quick service

- 6.3.2 Institutional foodservice

- 6.3.3 Healthcare and educational facilities

- 6.4 Direct-to-consumer channels

Chapter 7 Market Estimates and Forecast, By Packaging Format, 2021-2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Traditional metal cans

- 7.2.1 Standard size cans (10.5-11 oz)

- 7.2.2 Family size cans (18-23 oz)

- 7.2.3 Institutional size cans

- 7.3 Alternative packaging formats

- 7.3.1 Flexible pouches and stand-up pouches

- 7.3.2 Aseptic cartons and tetra packs

- 7.3.3 Microwaveable containers

- 7.3.4 Single-serve cups and bowls

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Campbell Soup Company

- 9.2 General Mills Inc. (Progresso)

- 9.3 The Kraft Heinz Company

- 9.4 Nestle S.A.

- 9.5 Unilever (Knorr)

- 9.6 ConAgra Brands Inc.

- 9.7 Baxters Food Group

- 9.8 BCI Foods Inc.

- 9.9 Vanee Foods Company

- 9.10 Amy’s Kitchen Inc