|

시장보고서

상품코드

1797821

봉합사 앵커 장치 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Suture Anchor Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

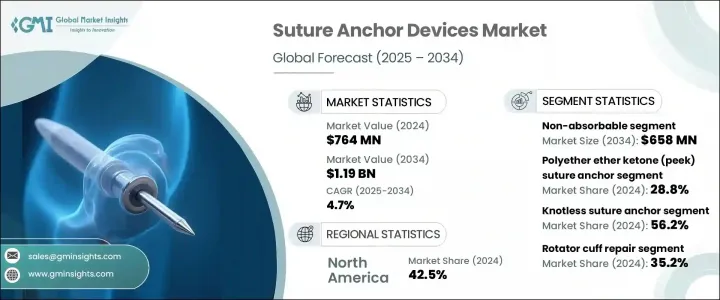

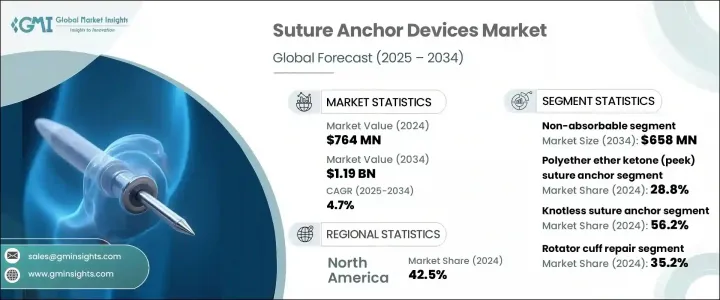

세계의 봉합사 앵커 장치 시장은 2024년 7억 6,400만 달러로 평가되었으며, CAGR 4.7%로 성장하여 2034년까지 11억 9,000만 달러에 이를 것으로 추정됩니다.

이 성장은 주로 스포츠와 관련된 부상 발생률 증가와 힘줄 판 수복술, 아킬레스 건증 치료, 십자 인대 재건술과 같은 봉합사 앵커 장치를 일반적으로 사용하는 수술 증가로 이어집니다. 이 임플란트는 힘줄과 인대와 같은 연조직을 뼈에 부착하여 정형외과 수술에 중요한 역할을합니다. 또한 노년 인구의 확대도 노화와 관련된 질병에 더 많은 수술과 개입이 필요하기 때문에 시장 성장에 크게 기여하고 있습니다. 업계의 주요 기업으로는 Arthrex, Zimmer Biomet, Smith & Nephew, Stryker 등이 있습니다. 수술 및 재료의 혁신과 함께 봉합사 앵커 장치는 고정 강도, 생체 적합성 및 사용 편의성을 향상시키기 위해 진화를 계속하고 있습니다.

봉합사 앵커는 외과 수술 중 연부 조직을 뼈에 고정하기 위한 것으로 현대 정형외과 및 스포츠 의학에서 필수적인 도구입니다. 재료과학의 진보로 기계적 강도와 생체적합성이 강화된 앵커가 개발되어 보다 나은 치료 성적과 환자 만족도의 향상을 보장하고 있습니다. 이러한 기구는 성공적인 복구를 위해 정확성과 조직 보존이 중요한 저침습 수술에 필수적입니다. 회복 시간의 단축과 수술 정밀도의 향상이 점점 중시되고 있는 가운데, 고품질의 봉합사 앵커 장치에 대한 수요는 증가의 한계를 추구하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 6,400만 달러 |

| 예측 금액 | 11억 9,000만 달러 |

| CAGR | 4.7% |

2024년 봉합사 앵커 장치 시장은 비흡수성 부문이 4억 2,610만 달러를 차지하고 시장을 독점했습니다. 이 분야는 2034년까지 6억 5,800만 달러에 이르고, CAGR 4.5%를 보일 것으로 예측됩니다. 비흡수성 앵커는 뛰어난 기계적 강도와 장기 고정 능력으로 인해 힘줄 및 관절 입술 수리와 같은 고부하 정형외과 수술에서 선호됩니다. 티타늄과 PEEK(폴리에테르 에테르 케톤)와 같은 높은 생체적합성, 방사선 투과성, 안정된 성능을 가진 소재의 지속적인 사용이 비흡수성 앵커 수요를 견인하고 있습니다. 이 자료는 앵커가 장기간에 걸쳐 확실하게 작동하고 수리 조직에 영구적 인지지를 제공합니다.

PEEK 봉합사 앵커 부문은 2024년 28.8%를 차지하며 시장에서 가장 큰 점유율을 차지합니다. PEEK 앵커가 널리 채택되는 것은 강력한 임상 성능, 안전 프로파일 및 비금속성에 의한 외과 의사의 선호 때문입니다. PEEK 앵커는 뛰어난 강도와 방사선 투과성을 갖추고 있으며, 어깨, 무릎, 고관절 수술에 이상적입니다. 장기적인 연구는 PEEK 비매듭 앵커가 생분해성 앵커에 필적하는 성능을 보이는 것을 보여 주며, 정형외과 수술에서 안전하고 신뢰할 수 있는 옵션으로서의 지위가 더욱 확고해집니다.

미국의 봉합사 앵커 장치 2024년 시장 규모는 2억 9,980만 달러. 미국은 로봇 지원 수술과 PEEK 기반 봉합사 앵커와 같은 고급 정형외과 기술의 도입으로 최첨단을 달리고 있습니다. 이 나라의 강력한 규제 틀, 국민의 높은 인지도, 연구 개발에 많은 투자가 시장 성장의 주요 요인입니다. 스포츠 외상과 연령에 따른 근골격계 질환이 증가함에 따라 미국 시장은 공중 보건에 대한 노력과 민간 기술의 혁신으로 지속적인 성장을 기대하고 있습니다.

봉합사 앵커 장치 시장의 기업은 자신의 입지를 강화하고 시장 점유율을 확대하기 위해 다양한 전략을 채택하고 있습니다. 특히 복잡한 수술에 사용되는 봉합사 앵커의 성능과 내구성 향상에 주력하고 있습니다. 또한 많은 기업들이 PEEK 기반 및 생체 흡수성 봉합사 앵커를 도입하여 제품 포트폴리오를 확대하여 이러한 소재에 대한 수요 증가에 대응하고 있습니다. 또 다른 전략은 병원, 정형외과 클리닉, 연구 기관과 전략적 파트너십을 연결하여 자사 제품을 보다 확실하게 보급하는 것입니다. 게다가 현지 제조시설과 유통망에 투자하여 신흥 시장에서의 존재감을 높이는 것도 많은 대기업에 중요한 초점이 되고 있습니다. 이 회사들은 또한 로봇 지원 수술과 같은 기술적 진보를 활용하여 봉합사 앵커 장치를 차세대 수술에 통합하여 정확도 향상과 회복 시간 단축을 실현하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 스포츠 사고 증가

- 고령화 인구 증가

- 저침습 수술 수요

- 앵커 설계의 기술적 진보

- 업계의 잠재적 위험 및 과제

- 고급 앵커와 수술의 높은 비용

- 수술 후 합병증의 위험

- 시장 기회

- AI와 로봇 지원 수술의 통합

- 생체 적합성 및 생체 흡수성 재료의 혁신

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 진보

- 현재의 기술 동향

- 신흥기술

- 공급망 분석

- 가격 분석, 2024년

- 미래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTLE 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 흡수성

- 비흡수성

제6장 시장 추계 및 예측 : 재료별, 2021-2034년

- 주요 동향

- 금속 봉합사 앵커

- 생체 흡수성 봉합사 앵커

- 폴리에테르에테르케톤(PEEK) 봉합사 앵커

- 바이오 복합 봉합사 앵커

- 올소프트 봉합사 앵커

제7장 시장 추계 및 예측 : 매듭 방식별, 2021-2034년

- 주요 동향

- 비매듭 봉합사 앵커

- 매듭 봉합사 앵커

제8장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 회선건판 수복

- 아킬레스건염 수복

- 십자 인대 수리

- 상완 이두근 힘줄 고정술

- 기타 용도

제9장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원 및 진료소

- 외래수술센터(ASC)

- 기타 용도

제10장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Anika Therapeutics

- Arthrex

- ConMed

- Enovis Corporation

- Fuse Medical

- Johnson & Johnson

- MJ Surgical

- NeoSys

- Orthomed

- Ossio

- Parcus Medical

- SBM

- Smith & Nephew

- Stryker Corporation

- Teknimed

- Tulpar Medical Solutions

- Zimmer Biomet

The Global Suture Anchor Devices Market was valued at USD 764 million in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 1.19 billion by 2034. This growth is primarily driven by the increasing incidence of sports-related injuries, as well as the rise in procedures like rotator cuff repair, Achilles tendinosis treatment, and cruciate ligament reconstruction, all of which commonly employ suture anchor devices. These implants play a crucial role in orthopedic surgeries by attaching soft tissues such as tendons and ligaments to bone. The expanding geriatric population is also contributing significantly to market growth, as age-related conditions require more surgeries and interventions. Leading players in the industry include Arthrex, Zimmer Biomet, Smith & Nephew, and Stryker. With innovations in surgical techniques and materials, suture anchor devices continue to evolve to offer improved fixation strength, biocompatibility, and ease of use.

Suture anchors are essential tools in modern orthopedic and sports medicine, designed to fasten soft tissue to bone during surgical procedures. Advancements in materials science have led to the development of anchors with enhanced mechanical strength and biocompatibility, ensuring better outcomes and increased patient satisfaction. These devices are integral to minimally invasive surgeries, where precision and tissue preservation are critical for successful recovery. With a growing emphasis on reducing recovery times and improving surgical precision, the demand for high-quality suture anchor devices continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $764 Million |

| Forecast Value | $1.19 Billion |

| CAGR | 4.7% |

The non-absorbable segment dominated the suture anchor devices market in 2024, accounting for USD 426.1 million. This segment is projected to reach USD 658 million by 2034, growing at a CAGR of 4.5%. Non-absorbable anchors are preferred in high-load orthopedic procedures, such as rotator cuff and labral repairs, due to their superior mechanical strength and long-term fixation capabilities. The continued use of materials like titanium and PEEK (polyether ether ketone), which offer high biocompatibility, radiolucency, and consistent performance, is driving the demand for non-absorbable anchors. These materials ensure that the anchors perform reliably over time, providing permanent support to repaired tissues.

The PEEK suture anchor segment held the largest share of the market, accounting for 28.8% in 2024. The widespread adoption of PEEK anchors is attributed to their strong clinical performance, safety profile, and preference among surgeons for their non-metallic nature. PEEK anchors offer excellent strength and radiolucency, making them ideal for use in shoulder, knee, and hip surgeries. Long-term studies have shown that PEEK knotless anchors perform comparably to biodegradable anchors, further cementing their position as a safe and reliable choice for orthopedic procedures.

United States Suture Anchor Devices Market was valued at USD 299.8 million in 2024. The U.S. is at the forefront of adopting advanced orthopedic technologies, including robotic-assisted surgeries and PEEK-based suture anchors. The country's strong regulatory framework, high levels of public awareness, and substantial investments in research and development are major contributors to market growth. With the increasing prevalence of sports injuries and age-related musculoskeletal conditions, the U.S. market is expected to experience sustained growth, driven by both public health initiatives and innovations in private sector technologies.

Major players in the Suture Anchor Devices Market include Smith & Nephew, Stryker Corporation, Zimmer Biomet, Arthrex, and ConMed. Companies in the suture anchor devices market employ a range of strategies to solidify their position and increase market share. A key strategy is the continuous innovation in materials and device design, particularly focusing on improving the performance and durability of suture anchors used in complex surgeries. Many companies are also expanding their product portfolios by introducing PEEK-based and bioabsorbable suture anchors, catering to the growing demand for these materials. Another strategy involves forming strategic partnerships with hospitals, orthopedic clinics, and research institutions to ensure better adoption of their products. In addition, enhancing their presence in emerging markets by investing in local manufacturing facilities and distribution networks is a key focus for many leading players. These companies are also leveraging technological advancements such as robotic-assisted surgery to integrate suture anchor devices into next-gen surgical procedures, ensuring improved accuracy and faster recovery times.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Material trends

- 2.2.4 Tying type trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of sports accidents

- 3.2.1.2 Increasing geriatric population

- 3.2.1.3 Demand for minimally invasive surgeries

- 3.2.1.4 Technological advancements in anchor design

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced anchors and surgery

- 3.2.2.2 Risk of post operative complications

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and robotic assisted surgery

- 3.2.3.2 Innovation in biocompatible and bioabsorbable materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Absorbable

- 5.3 Non absorbable

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Metallic suture anchor

- 6.3 Bio absorbable suture anchor

- 6.4 Polyether ether ketone (PEEK) suture anchor

- 6.5 Bio composite suture anchor

- 6.6 All soft suture anchor

Chapter 7 Market Estimates and Forecast, By Tying Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Knotless suture anchor

- 7.3 Knotted suture anchor

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Rotator cuff repair

- 8.3 Archilles tendinosis repair

- 8.4 Cruciate ligament repairs

- 8.5 Biceps tenodesis

- 8.6 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital and clinics

- 9.3 Ambulatory surgical centres

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Anika Therapeutics

- 11.2 Arthrex

- 11.3 ConMed

- 11.4 Enovis Corporation

- 11.5 Fuse Medical

- 11.6 Johnson & Johnson

- 11.7 MJ Surgical

- 11.8 NeoSys

- 11.9 Orthomed

- 11.10 Ossio

- 11.11 Parcus Medical

- 11.12 SBM

- 11.13 Smith & Nephew

- 11.14 Stryker Corporation

- 11.15 Teknimed

- 11.16 Tulpar Medical Solutions

- 11.17 Zimmer Biomet