|

시장보고서

상품코드

1797888

소포 분류 시스템 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Parcel Sorting System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

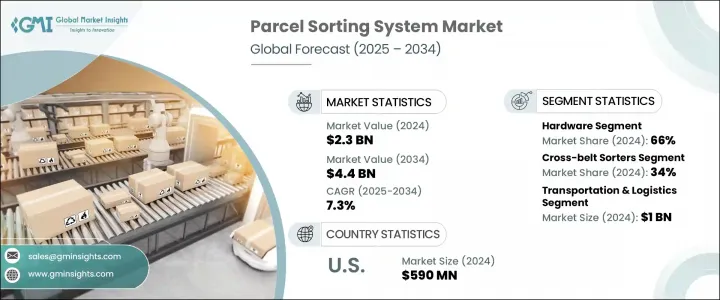

세계의 소포 분류 시스템 시장 규모는 2024년에 23억 달러로 평가되었고, CAGR 7.3%를 나타내 2034년에는 44억 달러에 이를 것으로 추정되고 있습니다.

이러한 꾸준한 성장은 물류 및 전자상거래 분야에서 보다 빠르고 스마트하며 비용 효율적인 솔루션에 대한 수요가 증가하고 있는 것이 주요 요인입니다. 소포의 양이 계속 증가함에 따라 고객의 기대가 높아짐에 따라 물류 사업자는 과거의 수작업에서 고급 자동화 기술로 이동하고 있습니다. 인공지능, 머신러닝, 클라우드 파워 플랫폼의 통합은 속도 향상, 오류 최소화, 전반적인 업무 효율성 향상으로 분류 작업을 변화시키고 있습니다. 실시간 적응성과 물류 허브 전체에서의 원활한 처리가 우선사항의 핵심이 되고, 지능적인 자동화가 최신의 소포 처리 전략의 중심적인 특징이 되고 있습니다.

자동화된 모바일 로봇과 AI 주도 시스템은 처리 시간을 단축하고 물류 업무의 효율성을 높입니다. 또한 기업은 IoT와 디지털 트윈 기술을 활용하여 예지보전을 가능하게 하고 장비의 가동시간과 신뢰성 향상에 도움을 줍니다. 성능 추적 및 사전 활성 시스템 경고 혁신은 운영 지연을 피하고 처리량을 극대화하기 위해 배포되었습니다. 이러한 기술 중심의 진보는 물류 자동화가 보조 작업에서 고도로 협조적이고 지능적인 생태계로 진화하고 있음을 반영합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 23억 달러 |

| 예측 금액 | 44억 달러 |

| CAGR | 7.3% |

하드웨어 분야는 2024년에 66%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 7%를 나타낼 것으로 예측됩니다. 증가하는 소포량에 대응하기 위해 모듈식이고 확장성이 높은 하드웨어의 요구가 높아지고 있어 물리적인프라에 대한 투자가 활발해지고 있습니다. 이 시스템은 빠르고 정밀한 운영을 위해 설계되었으며 세계적으로 주문 크기와 빈도가 계속 증가하는 동안 효율적인 물류 성능을 유지하는 데 필수적입니다.

분류 유형 중 크로스벨트 부문은 2024년에 34%의 점유율을 차지했고, 2034년까지의 CAGR은 8%를 나타낼 것으로 예측되고 있습니다. 다양한 형태와 크기의 짐을 정확하게 구분할 수 있는 한편, 섬세한 물건에는 상냥한 취급을 유지할 수 있기 때문에 대량의 짐을 취급하는 물류 센터의 최유력 후보가 되고 있습니다. 그 다용도를 통해 물류 공급자는 세계 전자상거래의 성장에 따라 증가하는 다양한 유형의 소포를 다룰 수 있으며 장기 적응성을 보장 할 수 있습니다.

미국의 소포 분류 시스템 시장 점유율은 80%로 2024년 시장 규모는 5억 9,000만 달러였습니다. 이 나라의 리더십은 물류 자동화의 적극적인 도입, 강력한 전자상거래 생태계, 스마트 창고 인프라에 대한 지속적인 투자로 인한 것입니다. 기업은 지능형 소프트웨어 플랫폼과 함께 첨단 장비를 도입하여 생산성을 높이고 분류 능력을 관리하며 광범위한 정착 네트워크에서 유통을 최적화하고 있습니다.

세계의 소포 분류 시스템 시장의 주요 기업으로는 BEUMER Group, Vanderlande, Korber, Honeywell Intelligrated, Daifuku, Interroll Group, Dematic 등이 있습니다. 소포 분류 시스템 업계의 기업은 보다 견고한 시장 포지션을 확보하기 위해 혁신, 확장 및 협업에 중점을 둔 전략적 이니셔티브를 개발하고 있습니다. 각 회사는 AI 기반 자동화, 클라우드 통합 및 실시간 모니터링 기능으로 제품 라인을 강화하고 있습니다. 또한 세계 파트너십 구축, 신흥 시장 진출, AMR, 디지털 트윈, IoT 대응 진단 등 차세대 기술에 대한 투자도 진행되고 있습니다. 많은 기업들이 모듈식 하드웨어 제공 규모를 확대하고 전자상거래, 소매, 제3자물류 고객을 위한 솔루션을 맞춤설정하여 보다 광범위한 채택을 보장합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 제조업체

- 소포 분류 시스템 제조업체

- 테크놀로지 벤더와 개발자

- 시스템 인티그레이터와 컨설턴트

- 유통 파트너와 채널

- 최종 용도

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 파괴자

- 공급자의 상황

- 영향요인

- 성장 촉진요인

- 전자상거래 성장과 마지막 마일 배송 수요

- 노동비용 상승과 노동력 최적화 필요성

- 물류 업무에 있어서의 자동화와 AI의 통합

- 지속가능성 요건과 환경규제

- 업계의 잠재적 위험 및 과제

- 고액의 초기 자본 투자와 ROI의 고려

- 구현 및 유지 보수 비용이 증가

- 시장 기회

- 고도의 분류 요구를 추진하는 전자상거래

- 다양한 사이즈의 짐을 구분할 수 있는 유연한 시스템의 필요성 증가

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술

- 신흥기술

- 특허 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 가격 동향

- 지역별

- 유형별

- 코스트 내역 분석

- 지속가능성 분석

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 하드웨어

- 소프트웨어

- 서비스

제6장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 푸시 트레이 분류기

- 틸트 트레이 분류기

- 크로스 벨트 분류기

- 신발 분류기

- 기타

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 운송 및 물류

- 소매 및 전자상거래

- 식음료

- 의약품

- 기타

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Amazon

- Alstef Group's

- Bastian Solutions(Toyota Advanced Logistics)

- BEUMER Group

- BOWE INTRALOGISTICS

- Daifuku

- Dematic(KION Group)

- Equinox MHE

- Falcon Autotech

- Five Group

- GBI Intralogistics

- GreyOrange

- Honeywell Intelligrated

- Interroll Group

- Korber Supply Chain(formerly Consoveyo)

- Kuecker Pulse Integration(KPI)

- MHS Global

- Okura Yusoki

- Schaefer Systems International(SSI SCHAFER)

- Vanderlande

The Global Parcel Sorting System Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 4.4 billion by 2034. This steady growth is largely driven by the increasing demand for faster, smarter, and more cost-effective solutions in the logistics and e-commerce sectors. As the volume of parcels continues to rise and customer expectations tighten, logistics operators are shifting away from outdated manual methods toward advanced automation technologies. The integration of artificial intelligence, machine learning, and cloud-powered platforms is transforming sorting operations by improving speed, minimizing errors, and enhancing overall operational efficiency. Real-time adaptability and seamless processing across distribution hubs have become core priorities, making intelligent automation a central feature in modern parcel handling strategies.

Automated mobile robots and AI-driven systems are reducing handling time and boosting efficiency across logistics operations. Companies are also leveraging IoT and digital twin technologies to enable predictive maintenance, helping to improve equipment uptime and reliability. Innovations in performance tracking and proactive system alerts are being rolled out to avoid operational delays and maximize throughput. These tech-driven advancements reflect how logistics automation is evolving from assisted tasks to highly collaborative, intelligent ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $4.4 Billion |

| CAGR | 7.3% |

The hardware segment held a 66% share in 2024 and is estimated to grow at 7% CAGR through 2034. The increased need for modular, scalable hardware to handle rising parcel volumes is driving heavy investment in physical infrastructure. These systems are engineered for high-speed, high-accuracy operations and are critical to maintaining efficient logistics performance as order sizes and frequencies continue to rise globally.

Among sorting types, the cross-belt segment held a 34% share in 2024 and is expected to grow at a CAGR of 8% through 2034. Their ability to sort packages of various shapes and sizes with precision, while maintaining gentle handling for delicate items, has made them a top choice for high-volume logistics centers. Their versatility allows logistics providers to handle the growing variety of parcel types driven by global e-commerce growth, ensuring long-term adaptability.

U.S. Parcel Sorting System Market held an 80% share and generated USD 590 million in 2024. The country's leadership stems from its aggressive adoption of logistics automation, a strong e-commerce ecosystem, and continued investments in smart warehouse infrastructure. Companies are deploying advanced equipment alongside intelligent software platforms to improve output, manage sorting capacity, and optimize distribution across vast fulfillment networks.

Leading players in the Global Parcel Sorting System Market include BEUMER Group, Vanderlande, Korber, Honeywell Intelligrated, Daifuku, Interroll Group, and Dematic. To secure a stronger market position, companies in the parcel sorting system industry are deploying strategic initiatives that focus on innovation, expansion, and collaboration. They are enhancing product lines with AI-based automation, cloud integration, and real-time monitoring features. Firms are also forming global partnerships, expanding into emerging markets, and investing in next-gen technologies like AMRs, digital twins, and IoT-enabled diagnostics. Many companies are scaling their modular hardware offerings and customizing solutions for e-commerce, retail, and third-party logistics clients to ensure broader adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Data mining sources

- 1.2.1 Global

- 1.2.2 Regional/Country

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw materials manufacturer

- 3.1.1.2 Parcel sorting system manufacturer

- 3.1.1.3 Technology vendors and developers

- 3.1.1.4 System integrators and consultants

- 3.1.1.5 Distribution partners and channels

- 3.1.1.6 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-commerce growth and last-mile delivery demands

- 3.2.1.2 Rising labor costs and workforce optimization needs

- 3.2.1.3 Automation and ai integration in logistics operations

- 3.2.1.4 Sustainability requirements and environmental regulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment and ROI considerations

- 3.2.2.2 High implementation and maintenance costs

- 3.2.3 Market opportunities

- 3.2.3.1 E-commerce driving advanced sorting needs

- 3.2.3.2 Growing need for flexible systems to sort varied parcel sizes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology & innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 Middle East & Africa

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By type

- 3.10 Cost breakdown analysis

- 3.11 Sustainability analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Push tray sorters

- 6.3 Tilt-tray sorter

- 6.4 Crossbelt sorter

- 6.5 Shoe sorter

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Transportation & Logistics

- 7.3 Retail & E-commerce

- 7.4 Food & Beverage

- 7.5 Pharmaceutical

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 8.1 North America

- 8.1.1 U.S.

- 8.1.2 Canada

- 8.2 Europe

- 8.2.1 UK

- 8.2.2 Germany

- 8.2.3 France

- 8.2.4 Italy

- 8.2.5 Spain

- 8.2.6 Belgium

- 8.2.7 Netherlands

- 8.2.8 Sweden

- 8.3 Asia Pacific

- 8.3.1 China

- 8.3.2 India

- 8.3.3 Japan

- 8.3.4 Australia

- 8.3.5 Singapore

- 8.3.6 South Korea

- 8.3.7 Vietnam

- 8.3.8 Indonesia

- 8.4 Latin America

- 8.4.1 Brazil

- 8.4.2 Mexico

- 8.4.3 Argentina

- 8.5 MEA

- 8.5.1 South Africa

- 8.5.2 Saudi Arabia

- 8.5.3 UAE

Chapter 9 Company Profiles

- 9.1 Amazon

- 9.2 Alstef Group's

- 9.3 Bastian Solutions (Toyota Advanced Logistics)

- 9.4 BEUMER Group

- 9.5 BOWE INTRALOGISTICS

- 9.6 Daifuku

- 9.7 Dematic (KION Group)

- 9.8 Equinox MHE

- 9.9 Falcon Autotech

- 9.10 Five Group

- 9.11 GBI Intralogistics

- 9.12 GreyOrange

- 9.13 Honeywell Intelligrated

- 9.14 Interroll Group

- 9.15 Korber Supply Chain (formerly Consoveyo)

- 9.16 Kuecker Pulse Integration (KPI)

- 9.17 MHS Global

- 9.18 Okura Yusoki

- 9.19 Schaefer Systems International (SSI SCHAFER)

- 9.20 Vanderlande