|

시장보고서

상품코드

1801833

ATP 분석 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)ATP Assay Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

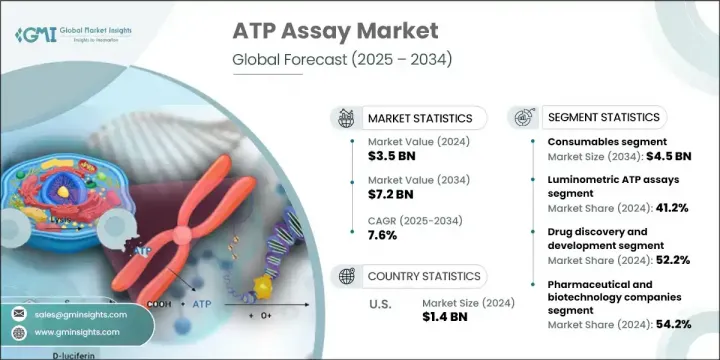

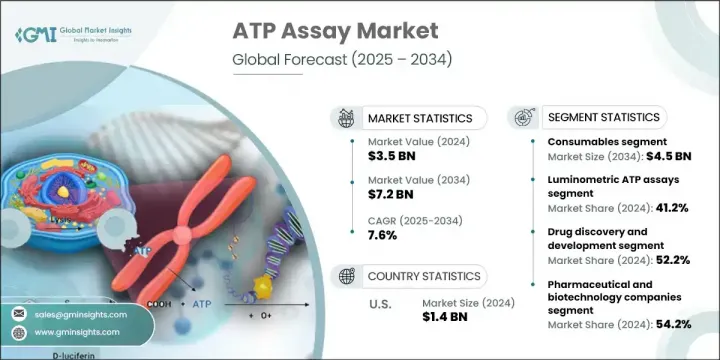

세계의 ATP 분석 시장 규모는 2024년에 35억 달러에 달하고, CAGR 7.6%로 성장할 전망이며 2034년에는 72억 달러에 이를 것으로 추정됩니다.

만성 질환 부담 증가, 맞춤형 치료 수요 확대, 분석 기술의 지속적인 혁신이 시장 성장을 경화 촉진제로 가속화하고 있습니다. 발광 측정 및 효소 검출 플랫폼의 진화는 처리량, 정밀도, 감도를 상당하게 향상시켜 연구, 진단, 의약품 개발 분야 전반에 걸쳐 활용 범위가 확대되고 있습니다. 분광광도계 및 고처리량 발광계와 같은 향상된 실험실 장비는 워크플로우를 간소화하면서 분석 효율성을 높이는 데 기여하고 있습니다.

ATP 분석은 세포 생존력, 에너지 대사, 세포독성 반응의 지표 역할을 하는 아데노신 삼인산(ATP) 수준을 검출하는 데 필수적입니다. 정밀 의학과 생물학적 관련성 테스트로의 전환에 따라 실시간 세포 기반 분석 수요가 증가하고 있습니다. 이러한 테스트를 통해 연구자들은 초기 의약품 개발, 환경 모니터링 및 독성 스크리닝 과정에서 세포 행동, 생존력 및 스트레스 반응을 평가할 수 있습니다. 생명공학 및 의약품 실험실에서 표적 약물 발견과 고처리량 스크리닝에 대한 강조가 커짐에 따라 향후 치료제에 필수적인 신뢰할 수 있고 확장 가능한 생물학적 데이터를 제공하는 데 ATP 분석의 역할이 지속적으로 부각되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 35억 달러 |

| 예측 금액 | 72억 달러 |

| CAGR | 7.6% |

2024년 소모품 부문은 21억 달러를 기록했으며, 2034년까지 연평균 성장률(CAGR) 7.7%로 45억 달러에 도달할 것으로 예상됩니다. 이 부문은 일상적인 절차에 필수적인 분석 키트, 시약 및 특수 실험실 재료에 대한 지속적인 수요로 인해 여전히 우위를 점하고 있습니다. 이러한 품목들은 대부분의 ATP 테스트 워크플로우의 중추를 이루며, 특히 의약품 스크리닝 및 오염 검출 분야에서 여러 플랫폼 전반에 걸쳐 중요합니다. 실험실 운영 규모가 확대됨에 따라 연구 및 진단 용도에서 이러한 재료의 지속적인 사용은 부문의 꾸준한 성장을 뒷받침합니다.

2024년 발광 분석 부문은 41.2%의 점유율을 기록했습니다. 이들의 광범위한 채택은 높은 정확도, 빠른 결과, 자동화 호환성에서 비롯됩니다. 높은 감도와 낮은 배경 잡음으로 정량적 데이터를 제공하는 능력 덕분에 대규모 스크리닝 및 실험실 워크플로우에 선호되는 선택입니다. 자동화 시스템과의 쉬운 통합, 실시간 모니터링, 멀티플렉싱 기능으로 대량 연구 환경에서 널리 사용됩니다. 최소한의 수동 처리로 대용량 데이터셋을 효율적으로 처리함으로써 데이터 일관성을 유지하면서 처리량을 상당히 향상시킵니다.

북미의 ATP 분석 시장은 2024년에 42.5%의 점유율을 차지합니다. 이 지역의 고급 연구 인프라, 제약 및 바이오테크 기업의 강력한 입지, 신진 진단 기술의 빠른 도입이 수요를 지속적으로 촉진하고 있습니다. 미국과 캐나다 실험실에서 세포 기반 테스트, 의약품 개발, 오염 검출에 대한 수요 증가가 해당 지역의 주도적 위치를 강화했습니다. 만성 질환 사례 급증과 임상 시험 투자 확대가 학계 및 산업계 전반에서 ATP 분석법 사용 증가에 기여하고 있습니다.

세계의 ATP 분석 시장을 촉진하고 있는 톱 기업에는 Danaher, 3M Company, Promega Corporation, Merck, Thermo Fisher Scientific 등이 있어 세계 시장 점유율의 55%를 차지하고 있습니다. ATP 분석 시장 주요 업체들은 분석 민감도, 확장성, 자동화 호환성에 대한 지속적인 연구개발을 통해 혁신 촉진 성장을 주력하고 있습니다. 기업들은 고처리량 용도를 지원하는 첨단 발광 측정 기술과 마이크로플레이트 기반 시스템을 통합하여 제품 라인을 강화하고 있습니다. 바이오테크 기업 및 연구 기관과의 전략적 협력은 최종 사용자 기반을 확대되다 동시에 브랜드 인지도가 강화되는 데 기여합니다. 인수합병(M&A) 역시 신규 지역적 시장 진출 및 생산 능력 증대를 위한 수단으로 활용되고 있습니다. 기업들은 더 나은 분석 모니터링과 데이터 추적성을 제공하기 위해 디지털 실험실 솔루션과 클라우드 기반 분석에 대한 투자를 늘리고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 질환 부담 증대

- 세포 기반 분석 수요 증가

- 바이오의약품 연구개발 성장

- 분석 포맷 기술 발전

- 업계의 잠재적 위험 및 과제

- 고급 키트의 높은 비용

- 엄격한 규제 지침

- 시장 기회

- 위생 및 환경 모니터링 분야의 폭발적 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 발전

- 현재의 기술 동향

- 신흥기술

- 공급망 분석

- 가격 분석(2024년)

- 장래 시장 동향

- 갭 분석

- 상환 시나리오

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 장비

- 발광계

- 분광광도계

- 소모품

- 시약 및 키트

- 마이크로플레이트

- 기타 소모품

제6장 시장 추계 및 예측 : 분석 유형별(2021-2034년)

- 주요 동향

- 발광 ATP 분석

- 효소 ATP 분석

- 생물 발광 공명 에너지 이동(BRET) ATP 분석

- 세포 기반 ATP 분석

- 기타 분석 유형

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 의약품 발견과 개발

- 오염 검사

- 질병 검출

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 제약 및 생명 공학 기업

- 병원 및 진단 실험실

- 학술연구기관

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 3M Company

- AAT Bioquest

- Abcam

- Agilent Technologies

- Berthold Technologies

- Biotium

- BioVision

- Cayman Chemical

- Cell Signaling Technology

- Charm Sciences

- Danaher Corporation

- Lonza

- Merck

- PCE Instruments

- Promega

- Reddot Biotech

- Revvity

- Thermo Fisher Scientific

The Global ATP Assay Market was valued at USD 3.5 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 7.2 billion by 2034. Market growth is being accelerated by the rising burden of chronic diseases, the growing demand for personalized therapies, and continuous innovation in assay technology. The evolution of luminometric and enzymatic detection platforms is significantly improving throughput, precision, and sensitivity, resulting in expanded use across research, diagnostics, and pharmaceutical development. Enhanced lab instrumentation, like spectrophotometers and high-throughput luminometers, is helping streamline workflows while increasing assay efficiency.

ATP assays are essential for detecting adenosine triphosphate levels, which act as indicators of cellular viability, energy metabolism, and cytotoxic response. With the shift toward precision medicine and biologically relevant testing, demand for real-time, cell-based assays is rising. These tests enable researchers to assess cellular behavior, viability, and stress responses during early drug development, environmental monitoring, and toxicity screening. The growing emphasis on targeted drug discovery and high-throughput screening in biotechnology and pharmaceutical labs continues to elevate the role of ATP assays in delivering reliable and scalable biological data essential for next-generation therapeutics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 7.6% |

In 2024, the consumables segment generated USD 2.1 billion and will reach USD 4.5 billion by 2034 at a CAGR of 7.7%. This segment remains dominant due to the recurring need for assay kits, reagents, and specialized lab materials essential for routine procedures. These items form the backbone of most ATP testing workflows and are vital across multiple platforms, particularly in drug screening and contamination detection. As laboratories scale their operations, the continued use of these materials in research and diagnostic applications supports steady segmental growth.

The luminometric assays segment held 41.2% share in 2024. Their widespread adoption stems from high accuracy, fast results, and automation compatibility. The ability of these assays to deliver quantitative data with high sensitivity and low background noise makes them the preferred choice for large-scale screening and laboratory workflows. They are widely used in high-volume research settings for their easy integration with automated systems, real-time monitoring, and multiplexing capabilities. Their efficiency in handling large datasets with minimal manual processing significantly improves throughput while maintaining data consistency.

North America ATP Assay Market held 42.5% share in 2024. The region's advanced infrastructure for research, strong presence of pharmaceutical and biotech firms, and rapid uptake of novel diagnostic technologies continue to drive demand. A growing need for cell-based testing, drug development, and contamination detection across labs in the U.S. and Canada has strengthened the region's leadership. The surge in chronic illness cases and expanding investments in clinical trials also contribute to the rising use of ATP assays across academic and industrial sectors.

Top companies driving the Global ATP Assay Market include Danaher, 3M Company, Promega Corporation, Merck, and Thermo Fisher Scientific-together accounting for 55% of global market share. Key players in the ATP assay market are focusing on innovation-driven growth through continuous R&D in assay sensitivity, scalability, and automation compatibility. Companies are enhancing their product lines by integrating advanced luminometric technologies and microplate-based systems that support high-throughput applications. Strategic collaborations with biotech firms and research institutes help expand their End user base while strengthening brand recognition. Mergers and acquisitions are also being used to enter new geographic markets and enhance production capacity. Firms are increasingly investing in digital lab solutions and cloud-based analytics to offer better assay monitoring and data traceability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Assay type trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising burden of chronic diseases

- 3.2.1.2 Growing demand for cell-based assays

- 3.2.1.3 Growth in biopharmaceutical R&D

- 3.2.1.4 Technological advancements in assay formats

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced kits

- 3.2.2.2 Stringent regulatory guidelines

- 3.2.3 Market opportunities

- 3.2.3.1 Explosive growth in hygiene and environmental monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Reimbursement scenario

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.2.1 Luminometers

- 5.2.2 Spectrophotometers

- 5.3 Consumables

- 5.3.1 Reagents and kits

- 5.3.2 Microplates

- 5.3.3 Other consumables

Chapter 6 Market Estimates and Forecast, By Assay Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Luminometric ATP assays

- 6.3 Enzymatic ATP assays

- 6.4 Bioluminescence resonance energy transfer (BRET) ATP assays

- 6.5 Cell-based ATP assays

- 6.6 Other assay types

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Drug discovery and development

- 7.3 Contamination testing

- 7.4 Disease detection

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biotechnology companies

- 8.3 Hospital and diagnostic laboratories

- 8.4 Academic and research institutes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3M Company

- 10.2 AAT Bioquest

- 10.3 Abcam

- 10.4 Agilent Technologies

- 10.5 Berthold Technologies

- 10.6 Biotium

- 10.7 BioVision

- 10.8 Cayman Chemical

- 10.9 Cell Signaling Technology

- 10.10 Charm Sciences

- 10.11 Danaher Corporation

- 10.12 Lonza

- 10.13 Merck

- 10.14 PCE Instruments

- 10.15 Promega

- 10.16 Reddot Biotech

- 10.17 Revvity

- 10.18 Thermo Fisher Scientific