|

시장보고서

상품코드

1801878

관절경 검사 기구 시장 기회와 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Arthroscopy Instruments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

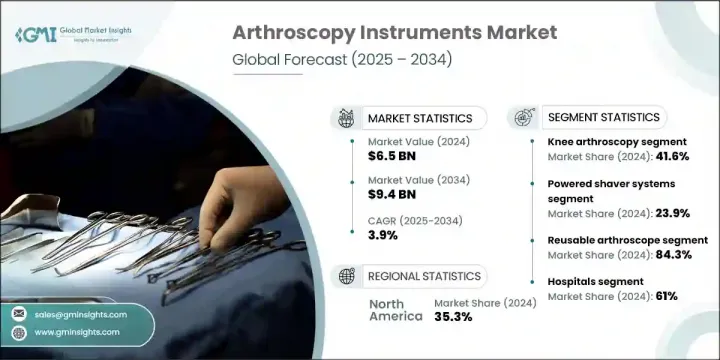

관절경 검사 기구 세계 시장 규모는 2024년에 65억 달러로 평가되었고, CAGR 3.9%로 성장하여 2034년에는 94억 달러에 이를 것으로 예측됩니다.

관절 관련 질환의 비율 증가, 노인 인구 증가, 스포츠 부상 증가는 이 시장을 이끄는 주요 요인 중 하나입니다. 최소침습 수술로의 전환이 진행되고 있으며, 관절경 수술은 회복시간 단축, 입원기간 단축, 수술 후 합병증 감소 등의 장점으로 인해 선호되는 수술법으로 각광받고 있습니다. 또한, 시각화 기술의 발전, 로봇 공학의 통합, 일회용 기구의 중요성으로 인해 관절경 수술은 크게 변화하고 있습니다. 관절 문제의 조기 치료 및 진단에 대한 환자의 인식이 높아짐에 따라 이러한 기기에 대한 세계 수요가 증가하고 있습니다.

특히 도시 지역에서는 외래수술센터(ASC)가 빠르게 확장되어 외래 관절경 검사의 주요 거점이 되어 시장 성장에 더욱 기여하고 있습니다. 신흥국의 의료 인프라 확대와 지출 증가는 공공 및 민간 의료 부문에서 관절경 기술 및 기기의 광범위한 채택을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 65억 달러 |

| 예측 금액 | 94억 달러 |

| CAGR | 3.9% |

전기 면도기 시스템은 최소 침습적 관절 수술에서 정확한 조직 및 뼈 절제술에 필수적인 역할을 하기 때문에 2024년에는 23.9%의 점유율을 차지할 것으로 예측됩니다. 뛰어난 효율성, 취급 용이성, 첨단 시각화 시스템과 원활하게 통합할 수 있는 능력으로 최신 관절경 수술에서 선호되는 도구가 되었습니다. 외래 수술센터에서 사용이 늘고 있는 것도 수술 시간을 단축하는 동시에 정확도와 시술 성공률을 높이기 위해 보급을 촉진하고 있습니다.

무릎 관절경 검사 부문은 2024년 41.6%로 가장 큰 시장 점유율을 차지했는데, 이는 전 세계적으로 무릎 관련 부상 및 골관절염 사례가 많기 때문으로 분석됩니다. 이 부문은 스포츠 참여자 증가, 고령자 증가, 저침습적 개입으로의 광범위한 변화로 인해 이익을 얻고 있습니다. 인대파열이나 연골 손상에는 관절경 수술이 일상적으로 사용되고 있으며, 가장 많이 시행되는 수술법입니다. 수술법, 도구, 회복 결과의 개발은 선진국과 개발도상국 모두에서 관절경 수술의 우위를 지속적으로 뒷받침하고 있습니다.

2024년 북미 관절경 검사 장비 시장 점유율 35.3% 이러한 리더십은 선진적인 수술 인프라, 첨단 의료기술의 조기 도입, 성형수술의 높은 빈도를 통해 이루어졌습니다. 미국과 캐나다는 정형외과 전문센터와 외래 수술 시설에 지속적으로 투자하고 있으며, 최소 침습적 수술의 광범위한 통합을 가능하게 하고 있습니다. 평균 수명 증가와 골관절염 및 스포츠 부상의 유병률 증가와 함께 이 지역 전체에서 관절경 도구에 대한 수요가 더욱 가속화되고 있습니다.

관절경 검사기기 세계 시장의 주요 참여업체로는 Olympus, Medacta, Smith & Nephew, Medtronic, Hemodia, Stryker, Richard Wolf, CONMED, Karl Storz, Arthrex, Invamed, Zimmer, Biomet, B. Braun, DePuy Synthetics(J&J) Biomet, B. Braun, DePuy Synthes(J&J) 등이 있습니다. 관절경 검사 장비 시장의 주요 기업들은 차세대 수술 기술에 대한 지속적인 투자를 통해 그 입지를 강화하고 있습니다. 로봇 공학, AI 시각화, 일회용 도구와 같은 혁신은 이들 기업이 더 높은 정확도, 더 짧은 회복 기간, 향상된 임상 결과를 제공하는 데 도움을 주고 있습니다. 일부 기업들은 외래수술센터(ASC) 수요 증가에 대응하기 위해 외래 환자 전용 제품 라인을 확장하고 있습니다. 의료기관 및 스포츠 의료 전문가들과의 전략적 제휴를 통해 각 업체들은 진화하는 수술 기법에 맞추어 수술에 특화된 기구를 개발하고 있습니다. 또한 많은 기업들이 지역 유통망을 강화하고 비용 효율적인 기기 라인을 출시하여 고성장 신흥 시장을 공략하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 산업에 대한 영향요인

- 성장 촉진요인

- 산업 잠재적 리스크와 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 기술과 혁신 상황

- 현재 기술 동향

- 신기술

- 공급망 분석

- 소비자 행동 경향

- 시장 진출 전략 분석

- Porter의 Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

- 갭 분석

- 가격 분석, 2024년

- 특허 상황

- 상환 시나리오

- 상환 시책이 시장 성장에 미치는 영향

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정·예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 전동 쉐이버 시스템

- 시각화 시스템

- 관절경

- 유체 관리 시스템

- 관절경 임플란트

- 고주파(RF) 절제 시스템

- 기타

제6장 시장 추정·예측 : 용도별, 2021-2034년

- 주요 동향

- 슬관절경 검사

- 견관절경 검사

- 고관절경 검사

- 기타

제7장 시장 추정·예측 : 사용성별, 2021-2034년

- 주요 동향

- 재이용 관절경

- 일회용 관절경

제8장 시장 추정·예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타

제9장 시장 추정·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 개요

- Arthrex

- B. Braun

- CONMED

- DePuy Synthes(J& J)

- Hemodia

- Invamed

- Karl Storz

- Medacta

- Medtronic

- Olympus

- Richard Wolf

- Smith & Nephew

- Stryker

- Zimmer Biomet

The Global Arthroscopy Instruments Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 9.4 billion by 2034. Rising rates of joint-related conditions, a growing elderly population, and increasing sports injuries are among the major forces driving this market. There is a growing shift toward minimally invasive procedures, and arthroscopy stands out as a preferred approach due to its benefits, such as shorter recovery times, reduced hospital stays, and lower post-operative complications. Additionally, advancements in visualization technologies, robotics integration, and a greater emphasis on disposable devices are transforming arthroscopy procedures. Increasing patient awareness about early treatment and diagnosis of joint issues is also helping to fuel demand for these instruments globally.

Ambulatory surgical centers, especially in urban settings, are rapidly expanding and becoming major hubs for outpatient arthroscopy, contributing further to market growth. Expanding healthcare infrastructure in emerging economies, alongside rising expenditure, is encouraging broader adoption of arthroscopic techniques and devices across both public and private health sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $9.4 Billion |

| CAGR | 3.9% |

The powered shaver systems captured a 23.9% share in 2024, owing to their essential role in delivering precise tissue and bone resection during minimally invasive joint procedures. Their superior efficiency, ease of handling, and ability to integrate seamlessly with advanced visualization systems make them a preferred tool in modern arthroscopic surgeries. Their growing use in outpatient surgical centers is helping fuel adoption, as they reduce operation time while enhancing precision and procedural success.

The knee arthroscopy segment held the largest market share at 41.6% in 2024, attributed to the high volume of knee-related injuries and osteoarthritis cases globally. The segment benefits from growing sports participation, a rise in elderly populations, and a broader shift toward minimally invasive interventions. Ligament tears and cartilage damage are routinely addressed using arthroscopic methods, making it the most performed procedure. Improvements in techniques, tools, and recovery outcomes continue to support its dominance across both developed and developing regions.

North America Arthroscopy Instruments Market held a 35.3% share in 2024. This leadership is driven by advanced surgical infrastructure, early adoption of cutting-edge medical technologies, and a high frequency of orthopedic procedures. The U.S. and Canada continue to invest in specialty orthopedic centers and outpatient surgical facilities, enabling wide-scale integration of minimally invasive techniques. Rising life expectancy, combined with the increasing prevalence of osteoarthritis and sports injuries, further accelerates the demand for arthroscopic tools across the region.

Key participants in the Global Arthroscopy Instruments Market include Olympus, Medacta, Smith & Nephew, Medtronic, Hemodia, Stryker, Richard Wolf, CONMED, Karl Storz, Arthrex, Invamed, Zimmer Biomet, B. Braun, and DePuy Synthes (J&J). Leading companies in the arthroscopy instruments market are advancing their position through consistent investment in next-generation surgical technologies. Innovations in robotics, AI-driven visualization, and disposable tools are helping these firms offer greater precision, shorter recovery periods, and enhanced clinical outcomes. Several players are expanding their outpatient-specific product lines to meet rising demand from ambulatory surgical centers. Strategic collaborations with healthcare institutions and sports medicine specialists are enabling companies to develop procedure-specific instruments tailored to evolving surgical techniques. Additionally, many are targeting high-growth emerging markets by strengthening regional distribution networks and launching cost-effective instrument lines.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 Usability trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of sports-related injuries and orthopedic disorders

- 3.2.1.2 Growing demand for minimally invasive surgical procedures

- 3.2.1.3 Increasing geriatric population prone to joint diseases

- 3.2.1.4 Advancements in arthroscopic visualization and imaging technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of arthroscopy equipment and implants

- 3.2.2.2 Limited accessibility in low-income and rural regions

- 3.2.3 Market opportunities

- 3.2.3.1 Technological integration with AI and robotic-assisted arthroscopy

- 3.2.3.2 Growth potential in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Consumer behaviour trend

- 3.8 Go-to-market strategy analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Gap analysis

- 3.13 Pricing analysis, 2024

- 3.14 Patent Landscape

- 3.15 Reimbursement scenario

- 3.15.1 Impact of reimbursement policies on market growth

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Powered shaver systems

- 5.3 Visualization systems

- 5.4 Arthroscopes

- 5.5 Fluid management systems

- 5.6 Arthroscopic implants

- 5.7 Radiofrequency (RF) ablation systems

- 5.8 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Knee arthroscopy

- 6.3 Shoulder arthroscopy

- 6.4 Hip arthroscopy

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Reusable arthroscope

- 7.3 Disposable arthroscopes

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arthrex

- 10.2 B. Braun

- 10.3 CONMED

- 10.4 DePuy Synthes (J&J)

- 10.5 Hemodia

- 10.6 Invamed

- 10.7 Karl Storz

- 10.8 Medacta

- 10.9 Medtronic

- 10.10 Olympus

- 10.11 Richard Wolf

- 10.12 Smith & Nephew

- 10.13 Stryker

- 10.14 Zimmer Biomet