|

시장보고서

상품코드

1822546

안과용 레이저 시장 : 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)Ophthalmic Lasers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

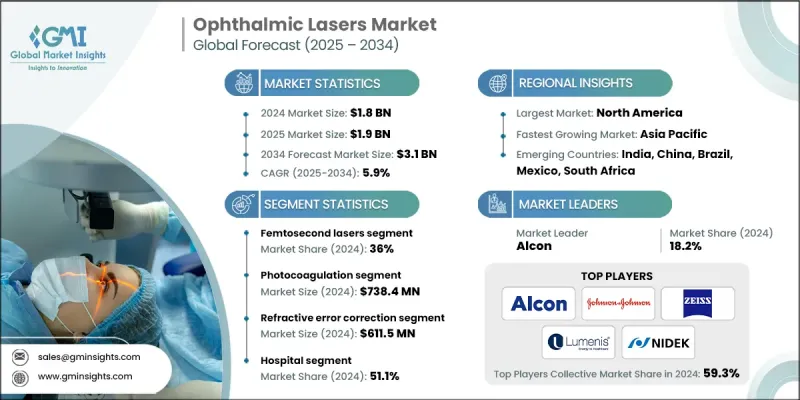

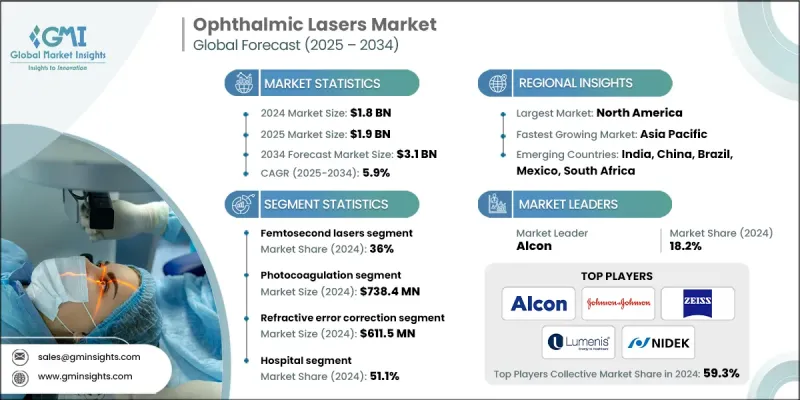

Global Market Insights, Inc.가 발행한 최신 보고서에 따르면 세계의 안과용 레이저 시장은 2024년에 18억 달러로 평가되었으며, CAGR 5.9%로 확대되어 2025년 19억 달러에서 2034년까지 31억 달러로 성장할 것으로 예측되고 있습니다.

이 시장은 시력 장애의 이환율 증가, 노화, 안과 수술용 레이저 시스템의 기술 진보에 의해 큰 성장을 이루고 있습니다.

안과용 레이저는 녹내장, 당뇨병성 망막증, 연령 황반변성(AMD), 굴절 이상과 같은 질환의 치료에 필수적인 것으로 부상하고 있습니다. 안과용 레이저는 정확하고 효과적인 수술을 제공하는 낮은 침습 장비이기 때문에 향후 몇 년 동안 보급이 진행될 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 18억 달러 |

| 예측 금액 | 31억 달러 |

| CAGR | 5.9% |

주요 촉진요인

1. 안질환 증가 : 백내장, 당뇨병성 망막증, 녹내장 증가로 레이저 기반 치료 수요가 증가하고 있습니다.

2. 굴절 교정 수술 증가 : 젊은 세대의 라식과 SMILE 수술에 대한 관심 증가는 펨토초 레이저와 엑시머 레이저의 사용을 촉진합니다.

3. 레이저의 정확성과 안전성 향상 : 새로운 안과용 레이저는 보다 진보된 통제, 더 적은 열 손상, 더 나은 수술 후 결과를 제공하기 위해 안과 의사들 사이에서 지지를 모으고 있습니다.

4. 인구 고령화 : 노화와 관련된 안질환은 특히 고소득 국가와 중소득 국가에서 세계적으로 증가하는 경향이 있습니다.

주요 기업

- Alcon, Johnson & Johnson, ZEISS, LUMENIS, NIDEK 등이 주요 기업으로 시장 전체의 59.3%를 차지하고 있습니다.

- Alcon은 2024년 안과용 레이저 시장에서 18.2%의 점유율을 획득했습니다.

주요 과제

- 장비의 높은 비용 : 안과용 레이저는 고가이기 때문에 저소득 의료시설로의 보급이 저해됩니다.

- 엄격한 규제 당국 승인 : 다양한 시장에서 위기 승인 지연으로 인해 출시 일정이 제한될 수 있습니다.

- 숙련된 전문가 부족 : 고급 레이저 시스템을 사용하려면 전문 교육이 필요하며 지역 및 저개발 지역에서는 여전히 어려움을 겪고 있습니다.

제품 유형별 - 펨토초 레이저가 시장을 독점

펨토초 레이저는 정확성, 최소 침습성, 굴절 교정 수술 및 백내장 수술의 효과로 2024년 제품 카테고리를 선도했습니다. 라식, SMILE 및 각막 절개에서의 사용은 시력 교정에 대한 환자의 관심이 증가함에 따라 전 세계적으로 빠르게 증가하고 있습니다.

기술별 - 광응고술이 널리 채용됨

광응고술은 당뇨병 망막증이나 망막 정맥 폐색증의 치료에 대한 이용이 증가하고 있기 때문에 2024년에도 호조를 유지했습니다. 이 기술은 시력을 위협하는 질병을 장기적으로 안정시킬 수 있기 때문에 망막 전문의들 사이에서 선호됩니다.

용도별 - 굴절이상 교정에 주목

2024년 시장은 굴절이상 교정이 지배적이었습니다. 안경 및 콘택트렌즈를 대체하는 영구적인 시력 교정 솔루션에 대한 수요가 증가함에 따라 특히 도시 지역의 레이저 지원 수술에 대한 수요가 뒷받침되고 있습니다.

최종 용도별 - 병원이 최대 점유율 획득

2024년 병원은 최종 용도 부문을 독점했습니다. 병원 시설은 통합 안과 치료 단위, 유능한 외과의사, 첨단 레이저 장비를 갖추고 있습니다. 또한 병원은 진료 보상상의 이점을 가지고 있으며 선택적 안과 수술과 응급 안과 수술 모두에 대응할 수 있는 능력을 갖추고 있습니다.

북미는 2024년 세계 안과용 레이저 시장에서 가장 큰 지역이였으며, 이는 고급 안과 수술의 광범위한 사용, 높은 근시율 및 백내장률, 그리고 유명한 기업의 존재로 인한 것이었습니다. 미국은 기술 도입, 상환 제도, 정교한 레이저 기반 치료를 갖춘 외래 수술 시설 등의 측면에서 최첨단을 유지하고 있습니다.

주요 기업은 경쟁 우위를 확보하기 위해 새로운 R&D, 전략적 제휴, 새로운 출시를 모색하고 실행하고 있습니다. 예를 들어, Alcon은 최근 백내장과 각막 수술을 위한 차세대 펨토초 레이저로 포트폴리오를 구축했습니다. ZEISS와 Johnson & Johnson은 수술 정밀도를 향상시키는 인공지능 유도 레이저 플랫폼에 주력하고 있습니다. 반대로 Lumenis와 Glaukos는 안과 클리닉 및 병원과 제휴하여 판매 채널을 더 잘 지원하는 것을 목표로합니다. BAUSCH LOMB과 NIDEK은 현지 생산을 모색하고 안과 의사의 훈련을 실시함으로써 신흥 시장에 초점을 맞춘 성장 전략을 실시했습니다. 이를 통해 세계적인 도달 범위가 더욱 넓어질 뿐만 아니라 기술이 진보되고 환자의 치료 성적이 향상됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계의 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 안질환의 유병률 증가

- 저침습 안과 수술 수요 증가

- 레이저 시스템의 기술적 진보

- 선진국 시장에서 보험상환 정세 개선

- 업계의 잠재적 리스크 및 과제

- 안과용 레이저 시스템의 고비용

- 수술 후 합병증, 부작용의 위험

- 시장 기회

- 아시아태평양, 라틴아메리카, 중동 및 아프리카의 신흥 시장

- 아웃리치 프로그램용 휴대 가능하고 컴팩트한 레이저 플랫폼

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 환급 시나리오

- 기술의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 분석 : 제품 유형별, 2024년

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 미래 시장 동향

- 밸류체인 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수합병

- 파트너십 및 협업

- 신제품 유형의 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 펨토초 레이저

- 다이오드 레이저

- 엑시머 레이저

- Nd:YAG 레이저

- 기타 제품 유형

제6장 시장 추계 및 예측 : 기술별, 2021-2034년

- 주요 동향

- 광응고술

- 광파괴술

- 어블레이션

- 기타 기술

제7장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 굴절 이상 교정

- 백내장 수술

- 당뇨병 망막증

- 녹내장

- 기타 용도

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 안과 클리닉

- 외래수술센터(ASC)

- 기타 용도

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Alcon

- BAUSCH LOMB

- Johnson & Johnson

- LUMENIS

- NIDEK

- ZEISS

- 지역 기업

- LIGHTMED

- LUMIBIRD MEDICAL

- Meridian Medical

- TOPCON Healthcare

- 신흥 기업

- ARC LASER

- Glaukos

- IRIDEX

- Ziemer Ophthalmology

The global ophthalmic lasers market was valued at USD 1.8 billion in 2024 and is projected to grow from USD 1.9 billion in 2025 to USD 3.1 billion by 2034, at a CAGR of 5.9%, according to the latest report published by Global Market Insights, Inc. The market is experiencing significant growth with the growing incidence of vision disorders, the aging population, and technological advancements in laser systems for eye procedures.

Ophthalmic lasers have emerged as vital for the treatment of diseases like glaucoma, diabetic retinopathy, age-related macular degeneration (AMD), and refractive errors. Ophthalmic lasers are minimally invasive instruments that deliver precise and effective surgical treatments, and therefore are expected to show increased uptake over the next few years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 5.9% |

Key Drivers:

1. Rising incidences of eye diseases: Increasing numbers of cataracts, diabetic retinopathy, and glaucoma are favoring the demand for laser-based treatments.

2. Rise in refractive surgeries: Increased interest in LASIK and SMILE surgeries among young generations is driving the usage of femtosecond and excimer lasers.

3. Improved precision and safety of lasers: New ophthalmic lasers provide enhanced control, less thermal damage, and better post-op results, thus gaining traction among ophthalmologists.

4. Aging population: Age-related eye conditions are on the rise worldwide, particularly in high-income and middle-income nations.

Key Players:

- Alcon, Johnson & Johnson, ZEISS, LUMENIS, and NIDEK are some of the key players, together commanding 59.3% of the overall market.

- Alcon captured an 18.2% share of the ophthalmic lasers market in 2024.

Key Challenges:

- High cost of equipment: Ophthalmic lasers are expensive, which hinders their penetration in low-income healthcare facilities.

- Strict regulatory approvals: Device approval delays in various markets may limit launch schedules.

- Scarcity of skilled professionals: Specialized training is needed for the use of sophisticated laser systems, which is still an issue in rural and underdeveloped regions.

By Product Type - Femtosecond Lasers Dominate the Market

Femtosecond lasers led the product category in 2024 with their precision, minimal invasiveness, and efficacy in refractive and cataract surgeries. Their use in LASIK, SMILE, and corneal incisions is increasing rapidly due to the increasing patient interest in vision correction continues to rise worldwide.

By Technology - Photocoagulation witnessed widespread Adoption

The photocoagulation segment sustained a strong position in 2024, particularly because of the increasing usage in the treatment of diabetic retinopathy and retinal vein occlusions. The technology is preferred among retinal specialists as it offers long-term stabilization of vision-threatening disease.

By Application - Refractive Error Correction Remains in Focus

Refractive error correction dominated the market in 2024. Growing demand for permanent vision correction solutions to glasses and contact lenses is propelling the demand for laser-assisted procedures, especially in urban areas.

By End Use - Hospitals Captured the Biggest Share

Hospitals dominated the end-use segment in 2024. Hospital facilities have integrated eye care units, qualified surgeons, and high-tech laser equipment. They also offer reimbursement benefits and have the capacity to treat both elective and emergency ophthalmic surgeries.

North America was the biggest player in the global ophthalmic lasers market in 2024, driven by extensive use of advanced ophthalmic surgeries, high myopia and cataract rates, and the presence of prominent players. The U.S. remains at the forefront in terms of technology adoption, reimbursement schemes, and outpatient surgical facilities with sophisticated laser-based treatments.

Top players are exploring and executing new research and development, strategic partnerships, and new launches for competitive advantage. As an example, Alcon has recently built its portfolio with next-generation femtosecond lasers for cataract and corneal surgery. ZEISS and Johnson & Johnson are focused on artificial intelligence-guided laser platforms to improve surgical precision. Conversely, Lumenis and Glaukos aim to partner with eye clinics and hospitals to better support their distribution channels. BAUSCH + LOMB and NIDEK implement growth strategies focused on emerging markets by exploring local production and also training ophthalmologists. This will further global reach but also advance technology and improve patient care outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of eye disorders

- 3.2.1.2 Growing demand for minimally invasive ophthalmic surgeries

- 3.2.1.3 Technological advancements in laser systems

- 3.2.1.4 Improved reimbursement landscape in developed markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of ophthalmic laser systems

- 3.2.2.2 Risk of postoperative complications and side effects

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets in Asia-Pacific, Latin America, and MEA

- 3.2.3.2 Portable and compact laser platforms for outreach programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Pricing analysis, By product type, 2024

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LATAM and MEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Femtosecond lasers

- 5.3 Diode lasers

- 5.4 Excimer lasers

- 5.5 Nd:YAG lasers

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Photocoagulation

- 6.3 Photodisruption

- 6.4 Ablation

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Refractive error correction

- 7.3 Cataract surgery

- 7.4 Diabetic retinopathy

- 7.5 Glaucoma

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ophthalmic clinics

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Alcon

- 10.1.2 BAUSCH + LOMB

- 10.1.3 Johnson & Johnson

- 10.1.4 LUMENIS

- 10.1.5 NIDEK

- 10.1.6 ZEISS

- 10.2 Regional Players

- 10.2.1 LIGHTMED

- 10.2.2 LUMIBIRD MEDICAL

- 10.2.3 Meridian Medical

- 10.2.4 TOPCON Healthcare

- 10.3 Emerging Players

- 10.3.1 A.R.C. LASER

- 10.3.2 Glaukos

- 10.3.3 IRIDEX

- 10.3.4 Ziemer Ophthalmology