|

시장보고서

상품코드

1822569

실험실 장비 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Laboratory Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

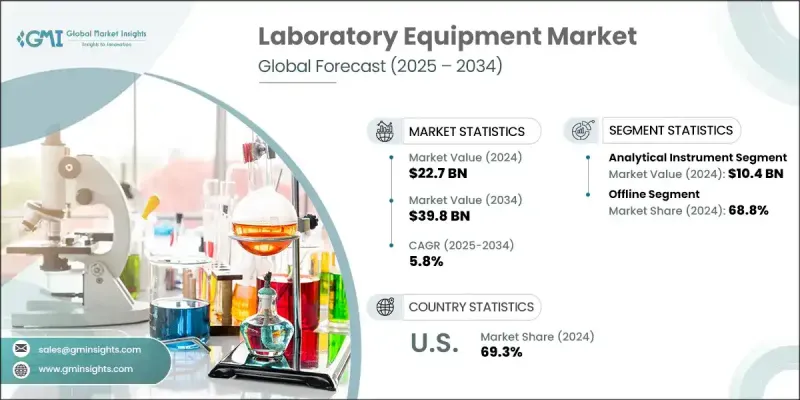

실험실 장비 세계 시장 규모는 2024년에는 227억 달러에 달했고, CAGR 5.8%로 성장하여 2034년에는 398억 달러에 달할 것으로 예측되고 있습니다.

생명공학, 제약 및 생명과학에서 조사 노력의 확대는 여전히 주요 수요 촉진요인이 되고 있습니다. 신약, 진단 및 백신 혁신에 대한 공적 및 민간 투자는 높은 정확성과 신뢰성을 갖춘 고급 실험 장비에 대한 요구를 부추기고 있습니다. 신흥 경제국에서는 정부가 혁신을 추진하기 위해 과학기술을 도입하고 있기 때문에 실험실 인프라의 성장이 급증하고 있습니다. 이와 병행하여 자동화, AI를 활용한 진단, 디지털 접속의 대두가, 부문을 불문하고 검사실의 워크플로우를 재구축하고 있습니다. 이러한 진화하는 시스템은 실시간 데이터 액세스, 원격 모니터링, 예측 진단을 지원하여 성능, 정확성 및 확장성을 향상시킵니다. 실험실 환경은 스마트 테크놀로지와 연결된 장치에 의해 점점 능률화되고, 오류를 최소화하고, 복잡한 업무를 간소화하는 데 도움이 됩니다. 만성 질환의 이환율 증가와 더 빠르고 정확한 진단 기능에 대한 수요는 세계의 의료, 학계, 산업계에서 실험실 기술의 활용 확대에 박차를 가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 227억 달러 |

| 예측 금액 | 398억 달러 |

| CAGR | 5.8% |

2024년 분석기기 부문 매출은 104억 달러였습니다. 이 분야의 이점은 정밀 검사, 품질 보증, 연구 지원에 널리 사용되고 있기 때문입니다. 컴플라이언스 요구 사항이 증가하고 상세한 분자 분석의 중요성이 증가함에 따라 크로마토그래피 및 질량 분석과 같은 도구는 제약, 환경 및 산업 실험실에서 중요한 구성 요소가 되었습니다.

2024년 오프라인 판매 채널의 점유율은 69%였습니다. 직접 대화, 기술 상담, 물리적 설치 지원이 필요하기 때문에 이러한 취향이 계속되고 있습니다. 분광계와 같은 고가치 장비는 전문가의 취급, 교정 및 맞춤형 서비스를 필요로 하는 경우가 많으며, 학술, 임상 및 산업 최종 사용자에게 대면 판매가 더욱 매력적입니다.

미국 실험실 장비 2024년 69.3%의 점유율을 기록했습니다. 이점은 성숙한 R&D 상황, 디지털 실험실 시스템의 보급, 자동화 및 규제 준수에 대한 주력으로 인한 것입니다. 진단, 생명공학 및 제약 부문의 지속적인 수요는 실험실 환경 전반의 제품 혁신과 혁신을 촉진하고 있습니다.

세계의 실험실 장비 시장을 형성하는 주요 기업은Waters Corporation, Atom Scientific Industries, Labman Scientific Instruments, Thermo Fisher Scientific, Sartorius, Danaher Corporation, 3M, GEA, Bruker Corporation, PerkinElmer, Roche, Siemens Healthineers, Agilent Technologies, Becton Dickinson, Abbott Laboratories 등 입니다. 시장 포지션을 강화하기 위해 주요 실험실 장비 제조업체는 제품 혁신, 고급 자동화 및 진단에서 AI 통합을 선호합니다. 이러한 기업들은 기술 포트폴리오를 확대하기 위해 연구개발에 많은 투자를 하고 있으며, 의료, 학술기관, 산업기관과 전략적 파트너십을 맺고 있습니다. 유통망을 확대하고 맞춤형의 까다로운 고객지원을 제공하는 것은 세계적 및 지역적인 수요를 캡처하는데 있어서 계속 중요한 열쇠가 됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 연구개발 활동 증가

- 기술적 진보

- 만성질환의 유병률 증가

- 업계의 잠재적 위험 및 과제

- 고액의 자본 투자

- 규제와 컴플라이언스의 과제

- 기회

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규기술

- 가격 동향

- 지역별

- 기기별

- 규제 상황

- 표준 및 컴플라이언스 요건

- 지역 규제 틀

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 기기종별, 2021-2034

- 주요 동향

- 분석기기

- 분광계(UV-Vis, IR, NMR, 질량 분석계)

- 크로마토그래피 장치(HPLC, GC)

- 현미경(광학 현미경, 전자 현미경)

- pH 미터와 전도도 미터

- 천칭과 계량기기

- 실험기구

- 인큐베이터와 오븐

- 원심분리기

- 정수 시스템

- 오토클레이브와 멸균기

- 냉장고와 냉동고

- 기타

제6장 시장 추정 및 예측 : 자동화 레벨별, 2021-2034

- 주요 동향

- 매뉴얼

- 반자동

- 자동

제7장 시장 추정 및 예측 : 용도별, 2021-2034

- 주요 동향

- 의료 및 임상 실험실

- 제약 및 생명공학 연구소

- 식품 및 음료 테스트

- 화학 및 재료 시험

- 학술 및 교육연구실

- 기타(학술·조사 기관, 환경)

제8장 시장 추정 및 예측 : 최종 이용 산업별, 2021-2034

- 주요 동향

- 헬스케어

- 식음료

- 의약품

- 학술연구기관

- 화학약품

- 기타(수의사 등)

제9장 시장 추정 및 예측 : 유통채널별, 2021-2034

- 주요 동향

- 온라인

- 오프라인

제10장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 3M

- Abbott Laboratories

- Agilent Technologies

- Atom Scientific Industries

- Becton Dickinson

- Bruker Corporation

- Danaher Corporation

- GEA

- Labman Scientific Instruments

- PerkinElmer

- Roche

- Sartorius

- Siemens Healthineers

- Thermo Fisher Scientific

- Waters Corporation

The Global Laboratory Equipment Market was valued at USD 22.7 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 39.8 billion by 2034.

Expanding research efforts in biotechnology, pharmaceuticals, and life sciences continue to be major demand drivers. Public and private investments in drug discovery, diagnostics, and vaccine innovation are fueling the need for advanced lab instruments with high precision and reliability. Emerging economies are witnessing a surge in laboratory infrastructure growth as governments embrace science and technology to drive innovation. In parallel, the rise of automation, AI-powered diagnostics, and digital connectivity is reshaping laboratory workflows across sectors. These evolving systems support real-time data access, remote monitoring, and predictive diagnostics, which improve performance, accuracy, and scalability. Laboratory environments are becoming increasingly efficient through smart technologies and connected devices, which help minimize errors and streamline complex operations. The growing incidence of chronic diseases and the demand for faster, more accurate diagnostic capabilities are adding momentum to the expansion of lab technology use in healthcare, academia, and industry worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.7 Billion |

| Forecast Value | $39.8 Billion |

| CAGR | 5.8% |

In 2024, the analytical instrument segment generated USD 10.4 billion. Its dominance stems from widespread use in precision testing, quality assurance, and research support. With increasing compliance requirements and the growing importance of detailed molecular analysis, tools like chromatography and mass spectrometry have become critical components in pharmaceutical, environmental, and industrial labs.

The offline sales channels held a 69% share in 2024. This preference continues due to the necessity for direct interaction, technical consultation, and physical installation support. High-value instruments such as spectrometers often require expert handling, calibration, and tailored servicing, making face-to-face distribution more appealing for academic, clinical, and industrial end users.

United States Laboratory Equipment Market held a 69.3% share in 2024. Its dominance is attributed to a mature R&D landscape, widespread use of digital lab systems, and a focus on automation and regulatory compliance. Continuous demand from diagnostics, biotech, and pharmaceutical sectors is driving product innovation and transformation across lab environments.

Key players shaping the Global Laboratory Equipment Market include Waters Corporation, Atom Scientific Industries, Labman Scientific Instruments, Thermo Fisher Scientific, Sartorius, Danaher Corporation, 3M, GEA, Bruker Corporation, PerkinElmer, Roche, Siemens Healthineers, Agilent Technologies, Becton Dickinson, and Abbott Laboratories. To reinforce their market position, leading laboratory equipment manufacturers are prioritizing product innovation, advanced automation, and the integration of AI in diagnostics. These companies are heavily investing in R&D to expand their technology portfolios, while also forming strategic partnerships with healthcare, academic, and industrial organizations. Expanding distribution networks and offering tailored, high-touch customer support remain key to capturing global and regional demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Automation level

- 2.2.4 Application

- 2.2.5 End use industry

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising R&D activities

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing prevalence of chronic diseases

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital investment

- 3.2.2.2 Regulatory and compliance challenges

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Analytical instruments

- 5.2.1 Spectrometers (UV-Vis, IR, NMR, mass spectrometers)

- 5.2.2 Chromatography equipment (HPLC, GC)

- 5.2.3 Microscopes (optical, electron)

- 5.2.4 pH meters & conductivity meters

- 5.2.5 Balances & weighing equipment

- 5.3 Laboratory instruments

- 5.3.1 Incubators & ovens

- 5.3.2 Centrifuges

- 5.3.3 Water purification systems

- 5.3.4 Autoclaves & sterilizers

- 5.3.5 Refrigerators & freezers

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Automation Level, 2021 - 2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Automatic

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Medical & clinical laboratories

- 7.3 Pharmaceutical & biotechnology laboratories

- 7.4 Food & beverage testing

- 7.5 Chemical & material testing

- 7.6 Academic & educational laboratories

- 7.7 Others (academic/research institutions, environmental)

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Healthcare

- 8.3 Food and beverages

- 8.4 Pharmaceuticals

- 8.5 Academic/research institutions

- 8.6 Chemicals

- 8.7 Others (Veterinary, etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Abbott Laboratories

- 11.3 Agilent Technologies

- 11.4 Atom Scientific Industries

- 11.5 Becton Dickinson

- 11.6 Bruker Corporation

- 11.7 Danaher Corporation

- 11.8 GEA

- 11.9 Labman Scientific Instruments

- 11.10 PerkinElmer

- 11.11 Roche

- 11.12 Sartorius

- 11.13 Siemens Healthineers

- 11.14 Thermo Fisher Scientific

- 11.15 Waters Corporation