|

시장보고서

상품코드

1822602

자가 혈당 측정 기기 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Self-Monitoring Blood Glucose Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

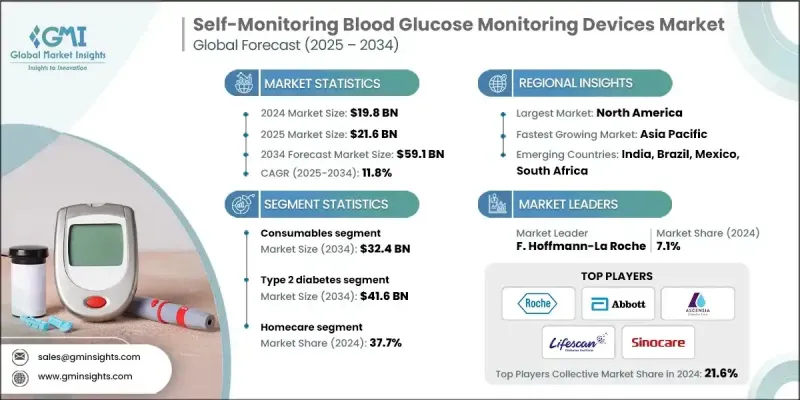

Global Market Insights Inc.가 발행한 최신 보고서에 따르면 세계의 자가 혈당 측정 기기 시장은 2024년에 198억 달러로 평가되었고, CAGR 11.8%로 2025년 216억 달러, 2034년에는 591억 달러로 성장할 것으로 예측되고 있습니다.

특히 신흥 시장에서 1형 및 2형 당뇨병 환자의 세계적인 급증은 매일 포도당 추적을 위한 편리하고 신뢰할 수 있는 SMBG 장치에 대한 수요를 촉진하고 있습니다. 좌식 생활 스타일, 건강에 해로운 식생활, 비만률의 상승이 당뇨병 이환율의 상승에 기여하고 있기 때문에 젊은층이나 폭넓은 층에서 당뇨병으로 진단되는 사람이 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 198억 달러 |

| 예측 금액 | 591억 달러 |

| CAGR | 11.8% |

소모품 수요 증가

소모품 부문은 2024년에 눈에 띄는 점유율을 차지했으며, 검사 스트립, 란셋 및 제어 솔루션이 견인했습니다. 이 품목은 매일 모니터링에 필수적이므로 수요는 항상 높으며 시장의 꾸준한 성장을 이끌고 있습니다. 검사 스트립은 교체 사이클이 빈번하기 때문에 소모품 판매의 대부분을 차지합니다. 소비자가 보다 정확하고 편리한 검사를 추구하는 동안, 각 회사는 보다 적은 양의 혈액 샘플로 신속한 결과를 얻을 수 있는 스트립을 생산하도록 기술 혁신을 진행하고 있습니다. 소모품 부문의 확대는 환자의 어드히어런스 유지에 필수적이며, 장기적인 고객 로열티 확보를 목표로 하는 업계 각사로부터 계속해서 엄청난 투자를 모으고 있습니다.

2형 당뇨병의 유병률 상승

2형 당뇨병 부문은 생활습관과 관련된 당뇨병 환자의 세계 증가를 반영하여 2024년에 큰 수익을 올렸습니다. 2형 당뇨병 환자는 종종 다이어트 및 약물 요법과 병행하여 병리학을 효과적으로 관리하기 위해 정기적인 포도당 모니터링이 필요합니다. 이 분야는 질병 관리에 대한 의식이 향상되고 건강 관리 제공업체가 합병증 예방에서 혈당 조절의 중요성을 강조함에 따라 급성장하고 있습니다. 2형 당뇨병 환자에게 SMBG 기기는 합리적인 가격으로 사용하기 쉽기 때문에 필수 도구입니다.

홈 케어가 견인 역할에

재택 케어 분야는 환자 중심의 원격 의료 관리 동향에 견인되어 2024년에 큰 점유율을 차지했습니다. 편의성, 프라이버시, 원격 의료 서비스의 지속적인 확대가 동기 부여되어 집에서 편안하게 혈당을 모니터링하는 것을 선호하는 개인이 증가하고 있습니다. 이 부문은 의료 전문가와 실시간 데이터 공유를 가능하게 하는 스마트폰 지원 장치 및 디지털 건강 플랫폼과 같은 기술적 진보의 혜택을 누리고 있습니다. 재택치료의 채택은 또한 임상 장소 이외의 만성 질환 관리를 점점 더 중요하게 만들고 있습니다.

지역별 인사이트

북미가 유망한 지역으로 상승

북미 자가 혈당 측정 기기 시장은 2024년에 주목할만한 점유율을 획득했습니다. 강력한 헬스케어 인프라, 당뇨병 이환율의 높이, 보험 적용 범위의 넓이가 이러한 기기의 왕성한 수요에 기여하고 있습니다. 이 지역의 소비자들은 정확성, 편의성, 디지털 헬스 에코시스템과의 통합을 선호하고 있으며, 이는 제조업체의 급속한 혁신을 뒷받침하고 있습니다. 또한 업계 선도적 인 존재와 확립 된 규제 환경은 고품질 표준과 제품의 신뢰성을 보장합니다.

자가 혈당 측정 기기 시장의 주요 기업은 All Medicus, DarioHealth, B. Braun Melsungen, Ypsomed Holding, Sanofi, Bionime Corporation, AgaMatrix, Nova Biomedical, LifeScan, Arkray, Omnis Health, Sinocare, Abbott Laboratories, F. Hoffmann-La Roche, and Ascensia Diabetes Care Holdings등이 있습니다.

시장 기반을 강화하기 위해 자가 혈당 측정 기기 시장의 각 회사는 혁신, 파트너십 및 환자 참여에 중점을 둡니다. 제품 개발은 정확성, 사용 편의성, 연결성에 중점을 두고 있으며, 많은 제조업체들이 보다 광범위한 디지털 건강 플랫폼과 통합하는 앱 지원 미터를 출시합니다. 의료 서비스 제공업체 및 보험 회사와의 전략적 제휴는 상환 계획 및 번들 관리 프로그램을 통해 장치의 가용성을 확대하고 있습니다. 각 회사는 또한 특히 신흥 시장에서 환자의 리터러시와 충고를 향상시키기 위해 교육 이니셔티브에 투자하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전 세계에서 당뇨병의 유병률이 상승

- 국민의 의식을 높이기 위한 정부의 대처

- 선진국에서의 자가 혈당 측정 기기의 기술 진보

- 업계의 잠재적 위험 및 과제

- 신흥 국가의 고급 장비 및 액세서리의 높은 비용

- 엄격한 규제 요건

- 시장 기회

- 신흥 시장으로 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술적 진보

- 현재의 기술 동향

- 신규기술

- 공급망과 유통분석

- 환급 시나리오

- 가격 분석, 2024

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 대시보드

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 제품별, 2021-2034

- 주요 동향

- 자기 혈당 측정기

- 소모품

- 검사 스트립

- Lancets

제6장 시장 추정 및 예측 : 용도별, 2021-2034

- 주요 동향

- 1형 당뇨병

- 2형 당뇨병

- 임신성 당뇨

제7장 시장 추정 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 진단센터

- 홈케어

- 기타 용도

제8장 시장 추정 및 예측 : 국가별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 네덜란드

- 스웨덴

- 벨기에

- 덴마크

- 핀란드

- 노르웨이

- 리투아니아

- 라트비아

- 에스토니아

- 러시아

- 폴란드

- 스위스

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 대만

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 칠레

- 페루

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 이집트

- 이스라엘

- 쿠웨이트

- 카타르

제9장 기업 프로파일

- Abbott Laboratories

- AgaMatrix

- All Medicus

- Arkray

- Ascensia Diabetes Care Holdings

- B. Braun Melsungen

- Bionime Corporation

- DarioHealth

- F. Hoffmann-La Roche

- LifeScan

- Nova Biomedical

- Omnis Health

- Sanofi

- Sinocare

- Ypsomed Holding

The global self-monitoring blood glucose monitoring devices market was estimated at USD 19.8 billion in 2024 and is expected to grow from USD 21.6 billion in 2025 to USD 59.1 billion in 2034, at a CAGR of 11.8%, according to the latest report published by Global Market Insights Inc.

The global surge in type 1 and type 2 diabetes cases, particularly in emerging markets, is driving demand for convenient and reliable SMBG devices for daily glucose tracking. As sedentary lifestyles, unhealthy diets, and rising obesity rates contribute to a higher incidence of diabetes, more individuals are being diagnosed at younger ages and across wider demographics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $19.8 Billion |

| Forecast Value | $59.1 Billion |

| CAGR | 11.8% |

Rising Demand for Consumables

The consumables segment held a notable share in 2024, driven by test strips, lancets, and control solutions. As these items are essential for daily monitoring, their demand remains consistently high, driving steady market growth. Test strips dominate consumables sales due to their frequent replacement cycles. As consumers seek more accurate and convenient testing, companies are innovating to produce strips that require smaller blood samples and deliver faster results. The consumables segment's expansion is critical for maintaining patient adherence, and it continues to attract substantial investment from industry players aiming to secure long-term customer loyalty.

Rising Prevalence of Type 2 Diabetes

The type 2 diabetes segment generated significant revenues in 2024, reflecting the global rise in lifestyle-related diabetes cases. Patients with type 2 diabetes often require regular glucose monitoring to manage their condition effectively alongside diet and medication. This segment is growing rapidly as awareness about disease management improves and healthcare providers emphasize the importance of glycemic control in preventing complications. The affordability and ease of use of SMBG devices for type 2 diabetes patients make them indispensable tools.

Homecare to Gain Traction

The homecare segment held a significant share in 2024, driven by the trend toward patient-centered and remote healthcare management. More individuals prefer monitoring their blood glucose levels from the comfort of their homes, motivated by convenience, privacy, and the ongoing expansion of telehealth services. This segment benefits from technological advancements, including smartphone-compatible devices and digital health platforms that enable real-time data sharing with healthcare professionals. Homecare adoption also aligns with the increasing emphasis on chronic disease management outside clinical settings.

Regional Insights

North America to Emerge as a Lucrative Region

North America self-monitoring blood glucose monitoring devices market generated a notable share in 2024. Strong healthcare infrastructure, high diabetes prevalence, and widespread insurance coverage contribute to robust demand for these devices. Consumers in this region prioritize accuracy, convenience, and integration with digital health ecosystems, which has pushed manufacturers to innovate rapidly. Additionally, the presence of major industry players and a well-established regulatory environment ensures high-quality standards and product reliability.

Major players in the self-monitoring blood glucose monitoring devices market are All Medicus, DarioHealth, B. Braun Melsungen, Ypsomed Holding, Sanofi, Bionime Corporation, AgaMatrix, Nova Biomedical, LifeScan, Arkray, Omnis Health, Sinocare, Abbott Laboratories, F. Hoffmann-La Roche, and Ascensia Diabetes Care Holdings.

To strengthen their market foothold, companies in the self-monitoring blood glucose monitoring devices market are focusing heavily on innovation, partnerships, and patient engagement. Product development emphasizes accuracy, ease of use, and connectivity, with many manufacturers launching app-enabled meters that integrate with broader digital health platforms. Strategic collaborations with healthcare providers and insurance companies are expanding device accessibility through reimbursement schemes and bundled care programs. Companies are also investing in educational initiatives to improve patient literacy and adherence, especially in emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of diabetes worldwide

- 3.2.1.2 Government initiatives for increasing awareness among people

- 3.2.1.3 Technological advancements of self-monitoring blood glucose monitoring devices in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced devices and accessories in developing countries

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain and distribution analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Self-monitoring blood glucose meters

- 5.3 Consumables

- 5.3.1 Testing strips

- 5.3.2 Lancets

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Type 1 diabetes

- 6.3 Type 2 diabetes

- 6.4 Gestational diabetes

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital

- 7.3 Ambulatory surgical centers

- 7.4 Diagnostic centers

- 7.5 Homecare

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Country, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.3.7 Sweden

- 8.3.8 Belgium

- 8.3.9 Denmark

- 8.3.10 Finland

- 8.3.11 Norway

- 8.3.12 Lithuania

- 8.3.13 Latvia

- 8.3.14 Estonia

- 8.3.15 Russia

- 8.3.16 Poland

- 8.3.17 Switzerland

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Taiwan

- 8.4.7 Indonesia

- 8.4.8 Vietnam

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Colombia

- 8.5.5 Chile

- 8.5.6 Peru

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Turkey

- 8.6.5 Egypt

- 8.6.6 Israel

- 8.6.7 Kuwait

- 8.6.8 Qatar

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AgaMatrix

- 9.3 All Medicus

- 9.4 Arkray

- 9.5 Ascensia Diabetes Care Holdings

- 9.6 B. Braun Melsungen

- 9.7 Bionime Corporation

- 9.8 DarioHealth

- 9.9 F. Hoffmann-La Roche

- 9.10 LifeScan

- 9.11 Nova Biomedical

- 9.12 Omnis Health

- 9.13 Sanofi

- 9.14 Sinocare

- 9.15 Ypsomed Holding