|

시장보고서

상품코드

1822616

교통 신호 제어기 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Traffic Signal Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

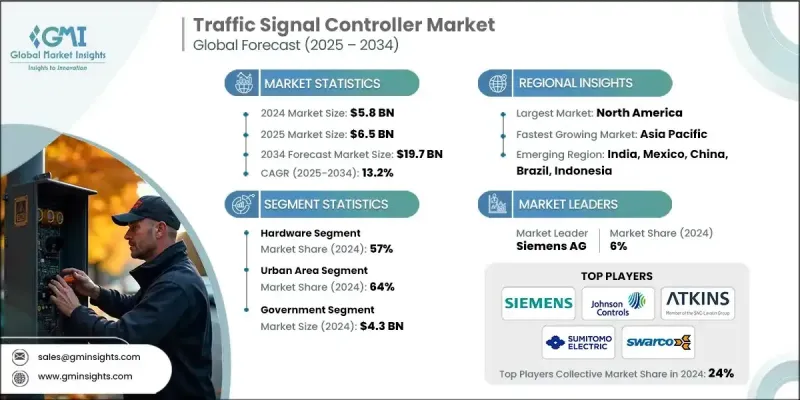

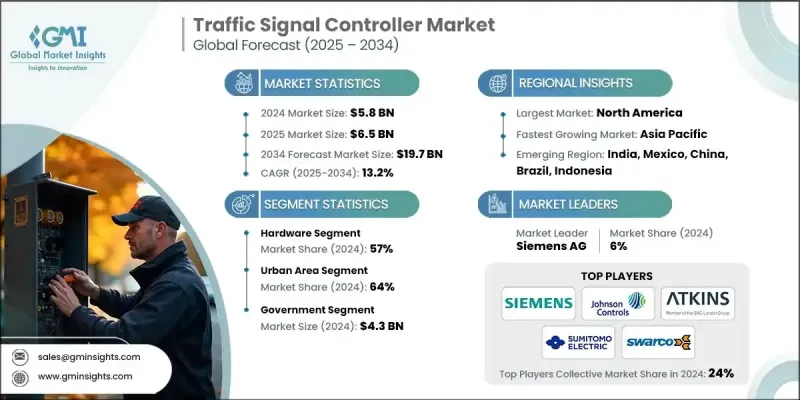

세계의 교통 신호 제어기 시장 규모는 2024년 58억 달러로 평가되었고, CAGR은 13.2%를 나타낼 것으로 예측되며 2034년 197억 달러로 성장할 전망입니다.

도시 인구가 계속 증가함에 따라, 도시들은 차량 소유와 도로 사용의 급격한 증가를 경험하고 있으며, 이는 광범위한 교통 체증과 기존 교통 인프라에 대한 압박 증가로 이어지고 있습니다. 기존의 고정 시간 신호등은 현대 도시 교통 패턴의 복잡성과 변동성을 처리하기에 더 이상 충분하지 않습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 58억 달러 |

| 예측 금액 | 197억 달러 |

| CAGR | 13.2% |

하드웨어 수요 증가

하드웨어 부문은 구형 아날로그 시스템을 지능형 디지털 제어기로 꾸준히 교체함에 따라 2024년 견고한 점유율을 유지했습니다. 이러한 현대식 장치는 실시간 센서, 적응형 신호 타이밍 기능, 원격 연결 기능을 갖추고 있습니다. 제조업체들은 도시 교통 시스템의 증가하는 요구를 충족시키기 위해 내구성, 모듈식 설계, 기존 인프라와의 통합 용이성에 주력하고 있습니다.

도시 지역의 채택 증가

도시 지역 부문은 높은 차량 밀도, 복잡한 교통 패턴, 그리고 혼잡 완화를 위한 공공의 압력 증가에 힘입어 2024년 상당한 점유율을 차지했습니다. 지방 자치 단체들은 실시간 교통 상황에 동적으로 대응하여 지연을 최소화하고 이동성을 향상시키는 적응형 교통 제어 기술을 도입하고 있습니다. 지자체들은 통근자 경험과 공공 안전을 개선하기 위한 광범위한 스마트 시티 투자의 일환으로 교통 제어 시스템 업그레이드를 우선시하고 있습니다.

정부 부문의 수요 증가

정부 부문은 공공 도로 및 교통 인프라 관리의 주체로서 2024년 상당한 점유율을 기록했습니다. 연방, 주, 지방 기관들은 인프라 법안 및 스마트 시티 보조금을 통해 지능형 교통 관리 시스템에 적극적으로 자금을 지원하고 있습니다. 긴 조달 주기는 여전히 과제이지만, 디지털 인프라에 대한 정책적 관심이 증가하면서 도입이 가속화되고 있습니다.

지역별 인사이트

북미가 유망한 지역으로 상승

2024년 북미 교통 신호 제어기 시장은 도시 교통 체증, 노후화된 인프라, 스마트 시티 프로그램에 대한 광범위한 지원에 힘입어 상당한 점유율을 차지했습니다. 미국은 교통망 현대화를 위한 연방 자금 지원을 통해 도입을 주도하고 있습니다. 민관 협력도 대도시권과 중규모 도시 모두에서 구현을 촉진하는 데 중요한 역할을 하고 있습니다.

교통 신호 제어기 시장의 주요 기업은 유넥스 트래픽, 스와르코, 지멘스, 트래픽 기술, 존슨 컨트롤스, 앳킨스, 스미토모 전기 산업, PTV 그룹, 템플, 이코노라이트입니다.

교통 신호 제어기 시장 기업들은 입지를 공고히 하기 위해 기술 혁신, 전략적 파트너십, 지역 맞춤형 솔루션에 주력하고 있습니다. 선도 기업들은 실시간 교통 최적화를 위해 AI, 머신러닝, 엣지 컴퓨팅을 제어기에 통합하고 있습니다. 시 정부, ITS(지능형 교통 시스템) 공급업체, 통신사와의 파트너십을 통해 기업들은 하드웨어를 종합적인 교통 관리 솔루션과 결합하여 제공할 수 있게 되었습니다. 또한 제조사들은 각 지자체의 특정 규제 및 인프라 요구사항에 맞춰 조정 가능한 확장형 플랫폼을 개발 중입니다. 사이버 보안, 개방형 아키텍처 설계, 원활한 V2X(차량-모든 것 간 통신) 통합에 대한 지속적인 투자는 해당 기업들이 미래 대비형 솔루션을 제공하고 경쟁 우위를 유지하는 데 기여하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 부품 공급업체

- 하드웨어 제공업체

- 최종 용도

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 파괴자

- 공급자의 상황

- 영향요인

- 성장 촉진요인

- 도시화 및 교통 혼잡 증가

- 안전성 및 효율성 개선에 대한 수요

- 교통 제어 기술 발전

- 스마트 시티 이니셔티브 부상

- 업계의 잠재적 위험 및 과제

- 높은 구현 및 유지보수 비용

- 기존 인프라와의 통합 문제

- 시장 기회

- 교통 관리에 AI 및 IoT 도입

- 지속 가능한 도시 이동성에 대한 정부 지원

- 성장 촉진요인

- 기술과 혁신 상황

- 혁신 상황

- NEMA 표준 발전

- TS1에서 TS2로

- TS2에서 ATC로

- 스마트 컨트롤러 통합 기능

- V2X 통신 프로토콜 개발

- 기술 채택과 성숙도 분석

- NEMA TS1 레거시 시스템 단계적 폐지 일정

- TS2 유형 1 시장 침투율

- ATC 표준 채택 곡선

- 스마트/커넥티드 컨트롤러의 성숙도 평가

- V2X 통합 준비 상황 평가

- 혁신 상황

- 규제 상황

- FHWA MUTCD 규제 준수 요건

- NEMA 표준화의 영향

- 규제 의무 준수

- 국제규격의 조화(EN, ISO)

- 투자 평가

- 정부 투자 프로그램

- 연방 고속도로 신탁 기금 배분

- 인프라 투자 및 일자리 법안 영향

- 주 교통부 자본 지출 분석

- 지방채 자금 조달의 동향

- 민간 투자

- 스마트 교통 솔루션 벤처 캐피털

- 기업의 R&D 투자 패턴

- 공공-민간 협력 모델

- 기술 도입 동향

- 정부 투자 프로그램

- 자금 조달 분석

- 국제적인 자금원

- 세계은행 인프라 프로젝트

- 개발 노력

- 유럽투자은행 프로그램

- 양자간 개발 협정

- 자금 조달의 과제와 기회

- 예산 제약 영향 분석

- 대체 자금 조달 메커니즘

- 보조금 및 보조금 프로그램

- ROI 기반 투자 정당화

- 국제적인 자금원

- 이용 사례와 용도 시나리오

- 도시 교차로 관리

- 교통량이 많은 통로 제어

- 보행자 밀집 상업 지구

- 스쿨 존 안전 용도

- 고속도로 및 간선도로 적용

- 고속도로 진입로 계량 시스템

- 간선도로 조정 네트워크

- 공사 구역의 교통 관리

- 긴급 사태 및 공공 안전 이용 사례

- 긴급 차량 우선 통행 시나리오

- 대피 경로 관리

- 사고 대응 조정

- 교통 및 멀티 모달 용도

- 버스 고속 전용 차로 우선 시스템

- 경전철 통합

- 복합 모드 교통 허브

- 스마트 시티 통합 시나리오

- 커넥티드 차량 통신

- 실시간 교통 데이터 분석

- 환경 영향 감시

- 베스트 케이스 시나리오 분석

- 최적의 기술 스택 전개

- 최대 ROI 달성 조건

- 이상적인 구현 타임라인

- 성능 벤치마크 목표

- 확장성 성공 요인

- 도시 교차로 관리

- 소비자 행동과 시장 채택 분석

- 최종 용도 결정 공정

- 주 교통부(DOT) 조달 기준

- 지방 정부 선정 요소인

- 연방 기관 요구사항 평가

- 기술의 채택 패턴

- 얼리어댑터의 특징

- 주류 시장 침투 촉진요인

- 지연된 부문의 전환 전략

- 벤더 선정 기준 분석

- 기술 사양 요건

- 비용 고려 및 예산 제약

- 지원 및 유지보수 기대치

- 상호 운용성과 표준 준수

- 시장 도입의 장벽

- 예산 배분의 과제

- 기술적 복잡성에 대한 우려

- 교육 및 인증 요건

- 최종 용도 결정 공정

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산 과정의 에너지 효율성

- 친환경 이니셔티브

- 탄소발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 하드웨어

- 제어장치

- 검출기

- 캐비닛

- 기타

- 소프트웨어

- 중앙 교통 관리

- 에지/컨트롤러 펌웨어

- 사이버 보안 및 장치 관리

- 기타

- 서비스

- 전문 서비스

- 관리형 서비스

제6장 시장 추계 및 예측 : 제어 시스템별(2021-2034년)

- 주요 동향

- 고정시간

- 작동식

- 적응형

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 도시

- 교외

제8장 시장 추계 및 예측 : 전개별(2021-2034년)

- 주요 동향

- 신규 설비

- 개조/현대화

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 정부

- 대중교통(TSP)

- 긴급 서비스(EVP)

- 시/지방 교통국(DOT)

- 민간 계약자

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계의 톱 기업

- SWARCO

- Siemens

- Cubic Transportation Systems

- Econolite

- Peek Traffic

- Traffic Technologies

- 지역 기업

- Sumitomo Electric

- Yunex Traffic

- Kapsch TrafficCom

- JENOPTIK Traffic

- Dahua Technology

- Hikvision

- JENOPTIK Traffic Solutions

- Aldridge Traffic Controllers

- Applied Information Inc

- Indra Sistemas

- 신흥 기업

- Teledyne FLIR Systems

- Cisco Systems

- Iteris

- Q-Free

- TransCore

- EFKON

The Global Traffic Signal Controller Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 13.2% to reach USD 19.7 billion by 2034.

As urban populations continue to grow, cities are experiencing a sharp rise in vehicle ownership and road usage, leading to widespread congestion and increased pressure on existing traffic infrastructure. Traditional, fixed-time traffic signals are no longer sufficient to handle the complexity and variability of modern urban traffic patterns.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $19.7 Billion |

| CAGR | 13.2% |

Growing Demand in Hardware

The hardware segment held a robust share in 2024, driven by the steady replacement of outdated analog systems with intelligent, digital controllers. These modern units are equipped with real-time sensors, adaptive signal timing capabilities, and remote connectivity features. Manufacturers are focusing on durability, modular design, and ease of integration with existing infrastructure to meet the growing needs of urban transportation systems.

Increasing Adoption in Urban Areas

The Urban areas segment held a significant share in 2024, driven by higher vehicle density, complex traffic patterns, and increasing public pressure to reduce congestion. City governments are deploying adaptive traffic control technologies that respond dynamically to real-time traffic conditions, minimizing delays and enhancing mobility. Municipalities are prioritizing traffic control upgrades as part of broader smart city investments, aiming to improve commuter experience and public safety.

Rising Demand in Government

The government segment generated a notable share in 2024, as they are primarily responsible for managing public roadways and transportation infrastructure. Federal, state, and local agencies are actively funding intelligent traffic management systems through infrastructure bills and smart city grants. Long procurement cycles remain a challenge, but increasing policy focus on digital infrastructure is accelerating adoption.

Regional Insights

North America to Emerge as a Lucrative Region

North America traffic signal controller market held a notable share in 2024, fueled by urban congestion, aging infrastructure, and widespread support for smart city programs. The United States is leading the adoption with federal funding directed toward modernizing transportation networks. Private-public collaborations are also playing a critical role in advancing implementation across both large metro areas and mid-sized cities.

Major players in the traffic signal controller market are Yunex Traffic, SWARCO, Siemens, Traffic Technologies, Johnson Controls, Atkins, Sumitomo Electric, PTV Group, Temple, and Econolite.

To solidify their position, companies in the traffic signal controller market are focusing on technological innovation, strategic partnerships, and localized customization. Leading players are integrating AI, machine learning, and edge computing into their controllers to enable real-time traffic optimization. Partnerships with city governments, ITS providers, and telecommunication firms are helping firms bundle their hardware with complete traffic management solutions. Additionally, manufacturers are developing scalable platforms that can be tailored to meet the specific regulatory and infrastructure needs of different municipalities. Ongoing investment in cybersecurity, open architecture designs, and seamless V2X integration is also helping these companies future-proof their offerings and maintain a competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.2.3 GMI proprietary AI system

- 1.2.3.1 AI-Powered research enhancement

- 1.2.3.2 Source consistency protocol

- 1.2.3.3 AI accuracy metrics

- 1.3 Forecast model

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario Analysis Framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research Trail & Confidence Scoring

- 1.6.1 Research Trail Components:

- 1.6.2 Scoring Components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Hardware providers

- 3.1.1.4 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing urbanization and traffic congestion in cities

- 3.2.1.2 Demand for improved safety and efficiency

- 3.2.1.3 Advancements in traffic control technology

- 3.2.1.4 Rise of smart city initiatives

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation and maintenance costs

- 3.2.2.2 Integration challenges with legacy infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of AI and IoT in traffic management

- 3.2.3.2 Government support for sustainable urban mobility

- 3.2.1 Growth drivers

- 3.3 Technology & innovation landscape

- 3.3.1 Innovation Landscape

- 3.3.1.1 NEMA standards evolution

- 3.3.1.2 TS1 to TS2

- 3.3.1.3 TS2 to ATC

- 3.3.1.4 Smart controller integration capabilities

- 3.3.1.5 V2X communication protocol development

- 3.3.2 Technology adoption and maturity analysis

- 3.3.2.1 NEMA TS1 legacy system phase-out timeline

- 3.3.2.2 TS2 Type 1 market penetration rates

- 3.3.2.3 ATC standard adoption curve

- 3.3.2.4 Smart/Connected controller maturity assessment

- 3.3.2.5 V2X integration readiness evaluation

- 3.3.1 Innovation Landscape

- 3.4 Regulatory landscape

- 3.4.1 FHWA MUTCD compliance requirements

- 3.4.2 NEMA standardization impact

- 3.4.3 Regulatory mandate compliance

- 3.4.4 International Standards Harmonization (EN, ISO)

- 3.5 Investment assessment

- 3.5.1 Government investment programs

- 3.5.1.1 Federal highway trust fund allocations

- 3.5.1.2 Infrastructure investment and jobs act impact

- 3.5.1.3 State dot capital expenditure analysis

- 3.5.1.4 Municipal bond financing trends

- 3.5.2 Private sector investment

- 3.5.2.1 Venture capital in smart traffic solutions

- 3.5.2.2 Corporate R&D investment patterns

- 3.5.2.3 Public-private partnership models

- 3.5.2.4 Technology acquisition trends

- 3.5.1 Government investment programs

- 3.6 Funding analysis

- 3.6.1 International funding sources

- 3.6.1.1 World bank infrastructure projects

- 3.6.1.2 Asian development bank initiatives

- 3.6.1.3 European investment bank programs

- 3.6.1.4 Bilateral development agreements

- 3.6.2 Funding challenges and opportunities

- 3.6.2.1 Budget constraint impact analysis

- 3.6.2.2 Alternative financing mechanisms

- 3.6.2.3 Grant and subsidy programs

- 3.6.2.4 Roi-based investment justification

- 3.6.1 International funding sources

- 3.7 Use cases and application scenarios

- 3.7.1 Urban intersection management

- 3.7.1.1 High-volume traffic corridor control

- 3.7.1.2 Pedestrian-heavy commercial districts

- 3.7.1.3 School zone safety applications

- 3.7.2 Highway and arterial applications

- 3.7.2.1 Interstate ramp metering systems

- 3.7.2.2 Arterial coordination networks

- 3.7.2.3 Work zone traffic management

- 3.7.3 Emergency and public safety use cases

- 3.7.3.1 Emergency vehicle preemption scenarios

- 3.7.3.2 Evacuation route management

- 3.7.3.3 Incident response coordination

- 3.7.4 Transit and multi-modal applications

- 3.7.4.1 Bus rapid transit priority systems

- 3.7.4.2 Light rail integration

- 3.7.4.3 Multi-modal transportation hubs

- 3.7.5 Smart city integration scenarios

- 3.7.5.1 Connected vehicle communication

- 3.7.5.2 Real-time traffic data analytics

- 3.7.5.3 Environmental impact monitoring

- 3.7.6 Best case scenario analysis

- 3.7.6.1 Optimal technology stack deployment

- 3.7.6.2 Maximum ROI achievement conditions

- 3.7.6.3 Ideal implementation timeline

- 3.7.6.4 Performance benchmark targets

- 3.7.6.5 Scalability success factors

- 3.7.1 Urban intersection management

- 3.8 Consumer behavior and market adoption analysis

- 3.8.1 End use decision-making process

- 3.8.1.1 State DOT procurement criteria

- 3.8.1.2 Municipal government selection factors

- 3.8.1.3 Federal agency requirements assessment

- 3.8.2 Technology adoption patterns

- 3.8.2.1 Early adopter characteristics

- 3.8.2.2 Mainstream market penetration drivers

- 3.8.2.3 Laggard segment conversion strategies

- 3.8.3 Vendor selection criteria analysis

- 3.8.3.1 Technical specification requirements

- 3.8.3.2 Cost considerations & budget constraints

- 3.8.3.3 Support & maintenance expectations

- 3.8.3.4 Interoperability & standards compliance

- 3.8.4 Market adoption barriers

- 3.8.4.1 Budget allocation challenges

- 3.8.4.2 Technical complexity concerns

- 3.8.4.3 Training & certification requirements

- 3.8.1 End use decision-making process

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Controller units

- 5.2.2 Detectors

- 5.2.3 Cabinets

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Central traffic management

- 5.3.2 Edge/controller firmware

- 5.3.3 Cybersecurity & device management

- 5.3.4 Others

- 5.4 Service

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Control System, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Fixed-time

- 6.3 Actuated

- 6.4 Adaptive

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Urban area

- 7.3 Suburbs area

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 New installations

- 8.3 Retrofits/modernization

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Government

- 9.2.1 Public transit agencies (TSP)

- 9.2.2 Emergency services (EVP)

- 9.2.3 City/municipal DOT

- 9.3 Private contractors

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 SWARCO

- 11.1.2 Siemens

- 11.1.3 Cubic Transportation Systems

- 11.1.4 Econolite

- 11.1.5 Peek Traffic

- 11.1.6 Traffic Technologies

- 11.2 Regional Champions

- 11.2.1 Sumitomo Electric

- 11.2.2 Yunex Traffic

- 11.2.3 Kapsch TrafficCom

- 11.2.4 JENOPTIK Traffic

- 11.2.5 Dahua Technology

- 11.2.6 Hikvision

- 11.2.7 JENOPTIK Traffic Solutions

- 11.2.8 Aldridge Traffic Controllers

- 11.2.9 Applied Information Inc

- 11.2.10 Indra Sistemas

- 11.3 Emerging Players

- 11.3.1 Teledyne FLIR Systems

- 11.3.2 Cisco Systems

- 11.3.3 Iteris

- 11.3.4 Q-Free

- 11.3.5 TransCore

- 11.3.6 EFKON