|

시장보고서

상품코드

1822644

병원 정보 시스템 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Hospital Information System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

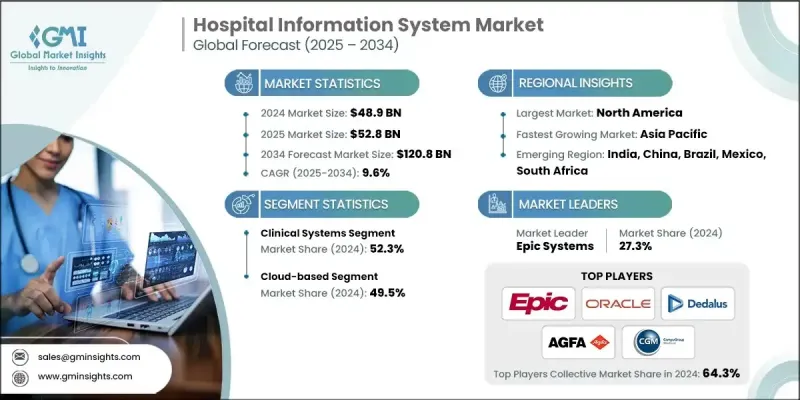

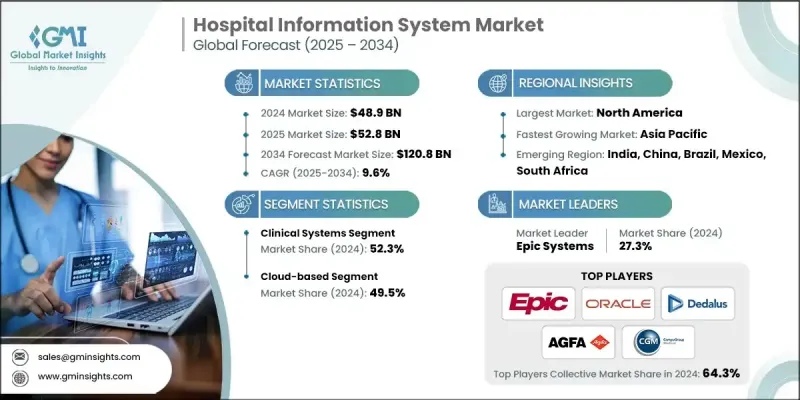

Global Market Insights, Inc.가 발행한 최신 보고서에 따르면 세계 병원 정보 시스템(HIS) 시장은 2024년 489억 달러로 평가되었으며, 2025년 528억 달러에서 2034년까지 1,208억 달러로 성장하고 CAGR 9.6%로 확대될 것으로 예측되고 있습니다.

헬스케어의 디지털화의 진전, 상호 운용가능한 솔루션에 대한 요구 증가, 임상 워크플로우의 최적화에 대한 요구 증가가 세계에서 HIS의 채용을 촉진하고 있습니다. 병원은 환자 기록, 임상 정보, 의료비 청구, 규정 준수를 다루는 통합 소프트웨어 시스템을 선택하는 경향이 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 489억 달러 |

| 예측 금액 | 1,208억 달러 |

| CAGR | 9.6% |

주요 촉진요인

1. 임상 데이터와 관리 데이터의 통합 관리 요구 : 병원은 부서 간에 서로 다른 워크플로우를 통합하기 위해 HIS를 도입하고 있습니다.

2. 만성 질환 증가 및 노화 : 효과적인 환자 추적 및 최적화된 치료에는 고급 의료 정보 플랫폼이 필요합니다.

3. 클라우드 및 AI 기반 시스템 채택 : IT 인프라 비용 절감, 유연성 및 원격 액세스로 클라우드 채택이 대중화되고 있습니다.

4. 컴플라이언스 및 데이터 보안 : 국제 및 지역 규정에 따라 병원은 컴플라이언스를 준수하고 안전하고 감사할 수 있는 시스템을 도입해야 합니다.

주요 기업

- Epic은 2024년 시장 점유율 27.3%로 병원 정보 시스템 시장을 독점했습니다.

- Oracle은 Cerner의 확립된 HIS/EHR 지위를 인수하고 클라우드 컴퓨팅, 데이터 분석, AI의 각각의 강점을 활용하고 있습니다.

- Dedalus는 상호 운용성과 오픈 디지털 건강 생태계에 강한 관심을 가진 유럽 시장의 선두 주자입니다.

주요 과제

- 상호 운용성 제약 : 레거시 시스템, 실험실, 이미지 프로세싱, 타사 플랫폼과의 HIS 통합은 계속 어려움을 겪고 있습니다.

- 높은 교육 및 도입 비용 : 사용자 정의, 마이그레이션, 직원에 대한 온보딩 투자는 고액이 될 수 있습니다.

- 보안 및 데이터 프라이버시 위협 : 의료 데이터 유출 및 랜섬웨어에 대한 우려 증가는 컴플라이언스와 보안 클라우드 구축의 추진으로 이어지고 있습니다.

1. 시스템 컴포넌트별 - 임상시스템 증가 추세

2024년 HIS 시장에서는 임상시스템 구성요소가 약 66%에서 가장 큰 점유율을 차지하고 있습니다. EMR, CPOE, LIS, RIS로 대표되는 임상 시스템 구성 요소는 일일 병원 업무의 근간을 지원하는 근로자입니다.

2. 배포별 - 클라우드 기반 솔루션이 대두

클라우드 기반 HIS의 도입은 확장성 향상, 인프라 지원을 위한 자본 지출 감소, 원격 용도 액세스 증가로 가속화되고 있습니다. 각 지역의 병원은 업무, 협업 및 지속적인 치료를 개선하기 위해 클라우드 솔루션을 도입하고 있습니다.

3. 지역별 - 북미가 호조를 유지

북미는 정부의 강력한 지원, 매우 높은 디지털 리터러시, 공립 병원과 사립 병원 모두에 대한 강력한 도입으로 2024년에도 계속해서 최대 시장 점유율을 유지하고 리드를 유지하고 있습니다. 북미는 강력한 헬스케어 인프라, EHR 보급, HIPAA 및 HITECH 등의 정부 규제, 클라우드 기반 의료 IT 솔루션의 존재감이 높아짐에 따라 병원 정보 시스템 시장의 우위를 유지하고 있습니다. 미국 병원과 의료 네트워크는 임상 의사 결정 지원, 집단 건강 분석 및 원격 관리 모듈을 병원의 핵심 시스템에 신속하게 통합합니다.

병원 정보 시스템 시장의 주요 기업으로는 AGFA Healthcare, CAMBIO, ChipSoft, CompuGroup Medical, Dedalus, Docaposte, Engineering Ingegneria Informatica, Epic Systems, InterSystems, Meierhofer AG, NextGen, Nexus, Oracle, SECTRA, Veradigm 등이 있습니다.

이 시장의 주요 HIS 기업은 클라우드 통합, 다른 지역으로의 진출, AI 대응 모듈, 헬스케어 리더와의 협업 계약을 채용하여 경쟁력을 높이고 있습니다. Dedalus와 InterSystems는 클라우드 플랫폼을 성장시키고 상호 운용 기능을 추가합니다. CompuGroup Medical과 AGFA Healthcare는 의사결정 지원 기능을 HIS 플랫폼에 통합합니다. Oracle은 Cerner 인수 후 통합 클라우드와 데이터 분석 기능을 통합하여 궁극적으로 EHR과 포퓰레이션 건강을 통해 가치있는 모듈을 만들려고합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 디지털 헬스 솔루션 도입 확대

- 정부의 대처와 규제

- 헬스케어비 증가

- 통합 건강 관리 시스템에 대한 수요 증가

- 업계의 잠재적 리스크 및 과제

- 구현 및 유지 보수 비용이 증가

- 데이터 보안 및 개인정보 보호에 대한 우려

- 시장 기회

- 정부의 헬스케어 디지털화 이니셔티브 증가

- 분석 및 비즈니스 인텔리전스 툴 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술적 상황

- 현재의 기술 동향

- 신흥기술

- 미래 시장 동향

- 소비자 행동과 동향

- 지역별 병원수

- 병원 디지털 에코시스템 개요

- 전자 의료 기록(EMR) 및 전자 건강 기록(EHR)

- 원격 의료 및 원격 환자 모니터링

- 사이버 보안 및 데이터 보호

- Porter's Five Forces 분석

- PESTEL 분석

- EMR에 AI 통합

- 갭 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 시스템 컴포넌트별, 2021-2034년

- 주요 동향

- 임상 시스템

- 전자 의료 기록(EMR) 및 전자 건강 기록(EHR)

- 방사선 정보 시스템(RIS)

- 약국 정보 시스템

- 검사 정보 시스템(LIS)

- 기타 임상 시스템

- 관리 및 백오피스 시스템

- 재무 및 청구

- 공급망 관리

- 시설관리 및 인사

- 운영 시스템

- 입퇴원 및 전원(ADT) 및 침대 관리 시스템(BMS)

- 운영 표준 지원 및 스케줄 시스템

- 환자용 기술

- 모바일 헬스 용도

- 환자 포털

- 통합층

- 인터페이스 엔진 및API

- 의료 정보 교환(HIE)

- 데이터 및 보안

- 임상 데이터 저장소

- 아이덴티티와 액세스 관리(IAM)

- 일반 데이터 보호 규칙(GDPR(EU 개인정보보호규정))

제6장 시장 추계 및 예측 : 전개별, 2021-2034년

- 주요 동향

- 클라우드 기반

- 웹 기반

- On-Premise

제7장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- AGFA Healthcare

- CAMBIO

- ChipSoft

- CompuGroup Medical

- Dedalus

- Docaposte

- Engineering Ingegneria Informatica

- Epic Systems

- InterSystems

- Meierhofer AG

- NextGen

- Nexus

- Oracle

- SECTRA

- Veradigm

The global hospital information system (HIS) market was valued at USD 48.9 billion in 2024 and is projected to grow from USD 52.8 billion in 2025 to USD 120.8 billion by 2034, expanding at a CAGR of 9.6%, according to the latest report published by Global Market Insights, Inc.

Growing healthcare digitization, increasing requirements for interoperable solutions, and mounting need for optimized clinical workflows are driving the adoption of HIS around the world. Hospitals are increasingly opting for integrated software systems to handle patient records, clinical information, medical billing, and regulatory adherence.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48.9 Billion |

| Forecast Value | $120.8 Billion |

| CAGR | 9.6% |

Key Drivers:

1. Requirement for integrated clinical and administrative data management: Hospitals are implementing HIS in order to integrate disparate workflows across departments.

2. Increased burden of chronic diseases and aging population: Effective patient tracking and optimized treatment require advanced health information platforms.

3. Cloud and AI-based systems' adoption: Cloud adoption is becoming popular with lower IT infrastructure expense, flexibility, and remote access.

4. Compliance and data security: International and regional regulations are forcing hospitals to implement compliant, secure, and auditable systems.

Key Players:

- Epic dominates the hospital information system market with a 27.3% market share in 2024.

- Oracle is harnessing its purchase of Cerner's established HIS/EHR position together with its respective strengths in cloud computing, data analytics, and AI.

- Dedalus is a European market leader with a strong focus on interoperability and open digital health ecosystems.

Key Challenges:

- Interoperability constraints: HIS integration with legacy systems, labs, imaging, and third-party platforms continues to be challenging.

- High training and implementation expenses: Initial investments in customization, migration, and employee onboarding can be high.

- Security and data privacy threats: Increasing fears of health data breaches and ransomware are driving increased compliance and secure cloud deployments.

1. By System Component - Clinical Systems on the Rise

Clinical system components made up the largest share of the HIS market at approximately 66% in 2024. The clinical system components represented by EMR, CPOE, LIS, and RIS are the hard-working foundations of daily hospital operations.

2. By Deployment - Cloud-Based Solutions on the Rise

Cloud-based HIS deployability is accelerating due to the increased scalability, lower capital expenditures to support the infrastructure, and increased access to remote applications. The hospitals in the Regions are deploying cloud solutions to improve operations, collaboration, and continuum of care.

3. By Region - North America Remains Strong

North America continued to have the largest market share in 2024, maintaining their lead with strong government support, very high levels of digital literacy, and strong uptake in both public and private hospitals. North America maintains its dominance in the hospital information system market with strong healthcare infrastructure, prevalent adoption of EHR, government regulations like HIPAA and HITECH, and increasing presence of cloud-based health IT solutions. American hospitals and health networks are quickly integrating clinical decision support, population health analytics, and remote care modules into their core hospital systems.

Some of the major players in the hospital information system market are AGFA Healthcare, CAMBIO, ChipSoft, CompuGroup Medical, Dedalus, Docaposte, Engineering Ingegneria Informatica, Epic Systems, InterSystems, Meierhofer AG, NextGen, Nexus, Oracle, SECTRA, and Veradigm.

Key HIS players in the market are employing cloud integration, expansions into other geographies, AI-enabled modules, and collaboration agreements with healthcare leaders to create a competitive edge.;Epic Systems continues to lead the North American market with long-term deals with top-performing health systems. Dedalus and InterSystems are growing their cloud platforms and adding interoperability features. CompuGroup Medical and AGFA Healthcare are integrating decision support capabilities into their HIS platforms. Oracle is incorporating its integrated cloud and data analytics capabilities after acquiring Cerner to ultimately produce more valuable modules for EHR and population health.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 System component trends

- 2.2.3 Deployment trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of digital health solutions

- 3.2.1.2 Government initiatives and regulations

- 3.2.1.3 Rising expenditure on healthcare

- 3.2.1.4 Surging demand for integrated healthcare systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation and maintenance costs

- 3.2.2.2 Data security and privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing government healthcare digitization initiatives

- 3.2.3.2 Growing demand for analytics and business intelligence tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Consumer behaviour and trends

- 3.8 No. of hospitals, by Region

- 3.9 Overview of hospital digital ecosystem

- 3.9.1 Electronic medical records (EMR)/electronic health records (EHR)

- 3.9.2 Telemedicine and remote patient monitoring

- 3.9.3 Cybersecurity and data protection

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Integration of AI in EMR

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America & MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By System Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Clinical systems

- 5.2.1 Electronic medical records (EMR)/electronic health records (EHR)

- 5.2.2 Radiology information system (RIS)

- 5.2.3 Pharmacy information system

- 5.2.4 Laboratory information system (LIS)

- 5.2.5 Other clinical systems

- 5.3 Administrative/back-office systems

- 5.3.1 Finance and billing

- 5.3.2 Supply chain management

- 5.3.3 Facilities management/Human resources

- 5.4 Operational systems

- 5.4.1 Admission, discharge, and transfer (ADT)/bed management systems (BMS)

- 5.4.2 Operational standards support/scheduling systems

- 5.5 Patient-facing technologies

- 5.5.1 Mobile health applications

- 5.5.2 Patient portals

- 5.6 Integration layer

- 5.6.1 Interface engines/APIs

- 5.6.2 Health information exchange (HIE)

- 5.7 Data and security

- 5.7.1 Clinical data repository

- 5.7.2 Identity and access management (IAM)

- 5.7.3 General data protection regulation (GDPR)

Chapter 6 Market Estimates and Forecast, By Deployment, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 Web-based

- 6.4 On-premise

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AGFA Healthcare

- 8.2 CAMBIO

- 8.3 ChipSoft

- 8.4 CompuGroup Medical

- 8.5 Dedalus

- 8.6 Docaposte

- 8.7 Engineering Ingegneria Informatica

- 8.8 Epic Systems

- 8.9 InterSystems

- 8.10 Meierhofer AG

- 8.11 NextGen

- 8.12 Nexus

- 8.13 Oracle

- 8.14 SECTRA

- 8.15 Veradigm