|

시장보고서

상품코드

1844335

픽업 트럭 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Pickup Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

픽업 트럭 세계 시장 규모는 2024년에 2,156억 달러로 평가되었고, CAGR 3.3%로 성장하여 2034년에는 3,028억 달러에 이를 것으로 예측됩니다.

세계 자동차 산업에서 중요한 부문인 픽업트럭은 개인, 상업, 산업, 레크리에이션 등 다양한 용도의 차량으로 계속 성장하고 있습니다. 소비자들은 실용성과 일상적인 사용성을 결합하여 공간, 견고함, 편안함을 하나의 패키지로 제공하는 트럭에 점점 더 매력을 느끼고 있습니다. 이 부문은 환경 규제뿐만 아니라 기술 혁신과 구매자의 관심 증가로 인해 전기 및 하이브리드 엔진 장착 옵션에 대한 관심이 높아지면서 발전하고 있습니다. 자동차 제조업체는 강력한 견인력과 적재 능력을 유지하면서 고급 편의사양, 인포테인먼트, 첨단 안전 시스템을 통합하여 픽업트럭을 가족과 차량 소유자 모두에게 매력적으로 만들고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 2,156억 달러 |

| 예측 금액 | 3,028억 달러 |

| CAGR | 3.3% |

업계는 전기 모빌리티로 크게 전환하고 있으며, 제조업체들은 환경 목표와 미래 규제 요건에 대응하기 위해 EV 기술에 투자하고 있습니다. 업계 전반의 혼란에 대응하기 위해 많은 기업들이 개발 비용을 절감하고 공급망을 간소화하기 위해 제휴 관계를 맺었습니다. 이번 제휴는 커넥티드 기술, 전동화, 다양한 디자인 기능을 통합하고, 고객 참여를 촉진하며, 빠르게 변화하는 자동차 환경에 적응하기 위해 이루어졌습니다.

2024년에는 개인용 카테고리가 61%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR)은 3%로 성장할 것입니다. 이러한 리더십은 출퇴근, 가족 여행, 아웃도어 라이프스타일을 쉽게 소화할 수 있는 다목적 차량에 대한 수요 증가에 따른 것입니다. 구매자는 편의성을 희생하지 않는 성능 중심의 트럭을 원하고 있으며, 제조업체는 고급형 모델에 고급스러운 인테리어, 터치스크린 컨트롤, 스마트 안전 기능, 최고급 인포테인먼트를 도입하고 있습니다. 이러한 취향의 변화에 따라 픽업트럭의 이미지는 실용적인 기계에서 일상에서 사용하는 라이프스타일 차량으로 재구성되고 있습니다.

풀사이즈 픽업 부문은 2024년 55%의 점유율을 차지했으며, 2025-2034년 연평균 복합 성장률(CAGR) 2.6%를 보일 것으로 예측됩니다. 풀 사이즈 픽업은 강도, 공간, 견인 능력으로 인해 널리 선호되고 있습니다. 제조업체들은 EV 드라이브트레인, 커스터마이징 기능, 주행거리 확대, 정교한 성능 패키지를 제공하는 전용 트림을 통해 이들 모델을 업그레이드하고 있습니다. 풀 사이즈 픽업의 고급 트림의 매력은 고객의 기대치를 높이고, OEM은 편의성, 로열티 혜택, 디지털 우선의 서비스 솔루션을 추가하여 종합적인 소유 경험을 개발하도록 장려하고 있습니다.

미국 픽업트럭 시장 점유율은 90%, 2024년 시장 규모는 998억 달러에 달했습니다. 이 부문은 풀사이즈 트럭에 대한 문화적, 기능적 선호가 확산되면서 미국에서 가장 많이 팔리는 자동차 카테고리로 남아있습니다. 개인용 및 레저용으로의 이용이 눈에 띄게 증가하고 있으며, 고사양의 전동화 모델에 대한 소비자의 의욕이 급증하고 있습니다. 자동차 제조업체들은 새로운 소비자를 끌어들이고 충성도를 유지하기 위해 첨단 파생 차종과 기술력이 풍부한 트림을 출시하고 있습니다.

세계 픽업트럭 시장에서 적극적으로 경쟁하고 있는 주요 기업으로는 닛산, Stellantis(Ram Trucks), 포드, 알파 자동차, 도요타, 혼다, 시보레, GMC, 볼링거, 카누 등이 있습니다. 경쟁이 치열한 픽업트럭 시장에서 입지를 유지하고 강화하기 위해 주요 제조업체들은 여러 가지 전략적 이니셔티브를 추진하고 있습니다. 환경 규제와 지속가능한 모빌리티에 대한 고객의 기대에 부응하기 위해 전동화 차량 플랫폼과 배터리 기술에 많은 투자를 하고 있습니다. 동시에 각 업체들은 특정 고객의 라이프스타일에 맞추어 고급화 및 성능 위주의 트림으로 제품 라인을 확장하고 있습니다. 전략적 제휴와 합작투자는 제품 개발 가속화, 생산 최적화, 공급망 탄력성 강화에 기여하고 있습니다. 또한, 많은 기업들은 고객 충성도와 장기적인 참여를 높이기 위해 소비자 직접 판매의 디지털 소매 플랫폼을 구축하고 애프터 서비스를 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 원재료 공급자

- 제조업체

- 도매업체

- 최종 용도

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 파괴적 변화

- 공급업체 상황

- 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 현재 기술

- 파워트레인 기술 진화

- 전동 픽업 트럭 배터리 기술

- 자율주행 통합

- 커넥티비티 및 인포테인먼트 시스템

- 첨단 운전자 보조 시스템(ADAS)

- 신기술

- 경량 소재와 구조

- 제조 기술 진보

- 충전 인프라 개발

- V2G 기술

- 무선(OTA) 업데이트 기능

- 성장 가능성 분석

- 규제 상황

- CAFE 연비 기준

- EPA 배출 규제

- NHTSA 안전기준

- 주 레벨 ZEV 의무화

- 상용차 규제

- 향후 규제 동향

- 가격 동향 분석

- 부문별 가격 추이

- 지역별 가격차

- 트림 레벨별 가격 전략

- 전기자동차와 내연기관차 가격 균형 타임라인

- 플릿 가격과 소매가격 동향

- 옵션 및 액세서리 가격

- 생산 및 판매 통계

- 세계의 생산능력 분석

- 제조 공장 가동률

- 모델별 판매 대수 동향

- 계절적인 판매 패턴

- 재고 관리 분석

- 생산 유연성 평가

- 공급망 리드타임

- 비용 내역 분석

- 차량 개발비

- 제조 비용 구조

- 재료비 분석

- 인건비 평가

- 기술 통합 비용

- 규제 준수 비용

- 특허 및 혁신 분석

- 파워트레인 기술 특허

- 전기자동차 특허

- 자율주행 특허

- 경량 구조 특허

- 제조 공정 특허

- OEM별 특허 포트폴리오 분석

- Porter의 Five Forces 분석

- PESTEL 분석

- 지속가능성과 환경 측면

- 환경 영향 평가와 수명주기 분석

- 사회적 영향과 지역사회와의 관계

- 거버넌스와 기업 책임

- 지속가능기술 개발

- 투자 상황 분석

- OEM 자본 투자 패턴

- 전기자동차에 대한 투자

- 제조 시설에 대한 투자

- 연구개발 투자 배분

- 합병사업 및 파트너십 투자

- 고객 행동 분석

- 구입 결정 요인

- 브랜드 로열티 패턴

- 사용 패턴 분석

- 교환 사이클 동향

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획과 자금조달

제5장 시장 추산·예측 : 사이즈별, 2021년-2034년

- 주요 동향

- 소형

- 중형

- 대형

제6장 시장 추산·예측 : 파워트레인별, 2021년-2034년

- 주요 동향

- 가솔린

- 디젤

- 전기

- 하이브리드

제7장 시장 추산·예측 : 촉진 능력별, 2021년-2034년

- 주요 동향

- 경량 견인 픽업 트럭(최대 7,500 파운드)

- 중형 견인 픽업 트럭(7,501-12,000 파운드)

- 대형 견인 픽업 트럭(12,001 파운드 이상)

제8장 시장 추산·예측 : 드라이브별, 2021-2034

- 주요 동향

- 후륜구동

- 총륜구동

- 사륜구동

제9장 시장 추산·예측 : 용도별, 2021년-2034년

- 주요 동향

- 개인용

- 상업용

- 건설 및 중기

- 농업 및 농경

- 조경 및 야외 서비스

- 유틸리티 및 자치체 이용

제10장 시장 추산·예측 : 지역별, 2021년-2034년

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 개요

- 세계 기업

- Ford

- GMC

- Stellantis(Ram Trucks)

- Toyota

- Nissan

- Honda

- Rivian Automotive

- Tesla

- Isuzu Motors

- Mahindra &Mahindra

- Chevrolet

- 지역 기업

- Great Wall Motors

- Canoo

- Alpha Motor

- Bollinger

- SAIC Motor

- Tata Motors

- Volkswagen Commercial Vehicles

- Mitsubishi Motors

- Hyundai Motor Company

- JAC Motors

- Foton Motor

- SsangYong Motor

- Changan Automobile

- 신규 기업

- Lordstown Motors

- Atlis Motor Vehicles

- Fisker

- Hercules Electric Vehicles

- Nikola

- Workhorse

- XOS

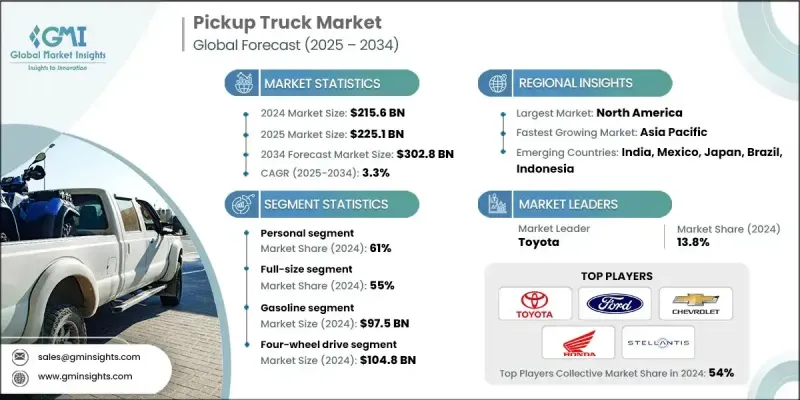

The Global Pickup Truck Market was valued at USD 215.6 billion in 2024 and is estimated to grow at a CAGR of 3.3% to reach USD 302.8 billion by 2034.

As a critical segment within the global automotive industry, pickup trucks continue to gain traction across personal, commercial, industrial, and recreational applications. Consumers are increasingly drawn to trucks that blend utility and everyday usability, offering space, ruggedness, and comfort in one package. The segment is evolving with rising interest in electric and hybrid-powered options, which are gaining momentum not just because of environmental regulations but also due to innovation and growing buyer interest. Automakers are integrating high-end comfort, infotainment, and advanced safety systems while maintaining strong towing and payload capabilities, making pickups appealing to both families and fleet owners.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $215.6 Billion |

| Forecast Value | $302.8 Billion |

| CAGR | 3.3% |

The industry has seen a major shift toward electric mobility, with manufacturers channeling investments into EV technology to address environmental goals and future regulatory requirements. In response to industry-wide disruptions, many companies also established collaborative alliances to reduce development expenses and streamline supply chains. These partnerships resulted in the integration of connected tech, electrification, and versatile design features, driving customer engagement and adapting to the fast-changing auto landscape.

In 2024, the personal-use category held 61% share and will grow at a CAGR of 3% through 2034. This leadership is driven by rising demand for multipurpose vehicles that can handle commuting, family travel, and outdoor lifestyles with ease. Buyers are looking for performance-driven trucks that don't sacrifice convenience, leading manufacturers to introduce luxury-grade interiors, touchscreen controls, smart safety features, and top-tier infotainment in their higher-end variants. These evolving preferences are reshaping the image of pickup trucks from utilitarian machines to well-rounded, daily-use lifestyle vehicles.

The full-size pickup segment held a 55% share in 2024 and is forecasted to grow at a CAGR of 2.6% between 2025 and 2034. Full-size pickups are widely preferred for their strength, space, and towing capabilities. Manufacturers are upgrading these models with EV drivetrains and exclusive trims offering customized features, expanded range, and sophisticated performance packages. The appeal of luxury trims in full-size pickups has elevated customer expectations, pushing OEMs to develop comprehensive ownership experiences with added convenience, loyalty perks, and digital-first service solutions.

U.S. Pickup Truck Market held 90% share and generated USD 99.8 billion in 2024. The segment remains the country's best-selling vehicle category, due to a widespread cultural and functional preference for full-size trucks. Personal and recreational usage has grown significantly, and consumer appetite for high-spec, electrified models continues to surge. Automakers are launching advanced variants and tech-rich trims to retain loyalty while attracting new audiences.

Major companies actively competing in the Global Pickup Truck Market include Nissan, Stellantis (Ram Trucks), Ford, Alpha Motor, Toyota, Honda, Chevrolet, GMC, Bollinger, and Canoo. To maintain and strengthen their positions in the competitive pickup truck market, leading manufacturers are pursuing multiple strategic initiatives. They are heavily investing in electrified vehicle platforms and battery technology to align with environmental regulations and customer expectations for sustainable mobility. Simultaneously, companies are expanding product lines with luxury-oriented and performance-driven trims tailored for specific customer lifestyles. Strategic alliances and joint ventures are playing a role in accelerating product development, optimizing production, and enhancing supply chain resilience. Additionally, many players are building direct-to-consumer digital retail platforms and enhancing aftersales service offerings to improve customer loyalty and long-term engagement.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.6.1.1 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Size

- 2.2.3 Power Train

- 2.2.4 Towing Capability

- 2.2.5 Drive

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Manufacturer

- 3.1.1.3 Distributor

- 3.1.1.4 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure expansion fuels demand for pickup trucks

- 3.2.1.2 Technological advancements enhance pickup truck efficiency and safety

- 3.2.1.3 Government investments in transportation infrastructure spur demand

- 3.2.1.4 Mining sector growth boosts pickup truck sales

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Economic downturns reduce construction and mining activities

- 3.2.2.2 Stringent emissions regulations increase manufacturing costs

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of electric and hybrid pickup trucks

- 3.2.3.2 Smart fleet management and telematics integration

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Powertrain technology evolution

- 3.3.1.2 Battery technology for electric pickups

- 3.3.1.3 Autonomous driving integration

- 3.3.1.4 Connectivity & infotainment systems

- 3.3.1.5 Advanced Driver Assistance Systems (ADAS)

- 3.3.2 Emerging technologies

- 3.3.2.1 Lightweight materials & construction

- 3.3.2.2 Manufacturing technology advances

- 3.3.2.3 Charging infrastructure development

- 3.3.2.4 Vehicle-to-Grid (V2G) technology

- 3.3.2.5 Over-the-Air (OTA) update capabilities

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 CAFE fuel economy standards

- 3.5.2 EPA emissions regulations

- 3.5.3 NHTSA safety standards

- 3.5.4 State-Level ZEV mandates

- 3.5.5 Commercial vehicle regulations

- 3.5.6 Future regulatory trends

- 3.6 Price trends analysis

- 3.6.1 Historical price evolution by segment

- 3.6.2 Regional price variations

- 3.6.3 Trim level pricing strategies

- 3.6.4 Electric vs ICE price parity timeline

- 3.6.5 Fleet vs retail pricing dynamics

- 3.6.6 Options & accessories pricing

- 3.7 Production & sales statistics

- 3.7.1 Global production capacity analysis

- 3.7.2 Manufacturing plant utilization

- 3.7.3 Sales volume trends by model

- 3.7.4 Seasonal sales patterns

- 3.7.5 Inventory management analysis

- 3.7.6 Production flexibility assessment

- 3.7.7 Supply chain lead times

- 3.8 Cost breakdown analysis

- 3.8.1 Vehicle development costs

- 3.8.2 Manufacturing cost structure

- 3.8.3 Material cost analysis

- 3.8.4 Labor cost assessment

- 3.8.5 Technology integration costs

- 3.8.6 Regulatory compliance costs

- 3.9 Patent & innovation analysis

- 3.9.1 Powertrain technology patents

- 3.9.2 Electric vehicle patents

- 3.9.3 Autonomous driving patents

- 3.9.4 Lightweight construction patents

- 3.9.5 Manufacturing process patents

- 3.9.6 Patent portfolio analysis by OEM

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Environmental impact assessment & lifecycle analysis

- 3.12.2 Social impact & community relations

- 3.12.3 Governance & corporate responsibility

- 3.12.4 Sustainable technological development

- 3.13 Investment Landscape Analysis

- 3.13.1 OEM capital investment patterns

- 3.13.2 Electric vehicle investment

- 3.13.3 Manufacturing facility investments

- 3.13.4 R&D investment allocation

- 3.13.5 Joint venture & partnership investments

- 3.14 Customer behavior analysis

- 3.14.1 Purchase decision factors

- 3.14.2 Brand loyalty patterns

- 3.14.3 Usage pattern analysis

- 3.14.4 Replacement cycle trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Size, 2021 - 2034 ($ Bn & Units)

- 5.1 Key trends

- 5.2 Compact

- 5.3 Mid-size

- 5.4 Full-size

Chapter 6 Market Estimates & Forecast, By Power Train, 2021 - 2034 ($ Bn & Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

- 6.5 Hybrid

Chapter 7 Market Estimates & Forecast, By Towing Capability, 2021 - 2034 ($ Bn & Units)

- 7.1 Key trends

- 7.2 Light towing pickup trucks (Up to 7,500 lbs)

- 7.3 Medium towing pickup trucks (7,501-12,000 lbs)

- 7.4 Heavy towing pickup trucks (12,001+ lbs)

Chapter 8 Market Estimates & Forecast, By Drive, 2021 - 2034 ($ Bn & Units)

- 8.1 Key trends

- 8.2 Rear-wheel drive

- 8.3 All wheel drive

- 8.4 Four-wheel drive

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Bn & Units)

- 9.1 Key trends

- 9.2 Personal

- 9.3 Commercial

- 9.3.1 Construction and heavy equipment

- 9.3.2 Agriculture and farming

- 9.3.3 Landscaping and outdoor services

- 9.3.4 Utility and municipal use

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn & Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Ford

- 11.1.2 GMC

- 11.1.3 Stellantis (Ram Trucks)

- 11.1.4 Toyota

- 11.1.5 Nissan

- 11.1.6 Honda

- 11.1.7 Rivian Automotive

- 11.1.8 Tesla

- 11.1.9 Isuzu Motors

- 11.1.10 Mahindra & Mahindra

- 11.1.11 Chevrolet

- 11.2 Regional players

- 11.2.1 Great Wall Motors

- 11.2.2 Canoo

- 11.2.3 Alpha Motor

- 11.2.4 Bollinger

- 11.2.5 SAIC Motor

- 11.2.6 Tata Motors

- 11.2.7 Volkswagen Commercial Vehicles

- 11.2.8 Mitsubishi Motors

- 11.2.9 Hyundai Motor Company

- 11.2.10 JAC Motors

- 11.2.11 Foton Motor

- 11.2.12 SsangYong Motor

- 11.2.13 Changan Automobile

- 11.3 Emerging players

- 11.3.1 Lordstown Motors

- 11.3.2 Atlis Motor Vehicles

- 11.3.3 Fisker

- 11.3.4 Hercules Electric Vehicles

- 11.3.5 Nikola

- 11.3.6 Workhorse

- 11.3.7 XOS