|

시장보고서

상품코드

1858829

자동차용 얼터네이터 및 스타터 모터 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Alternator and Starter Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

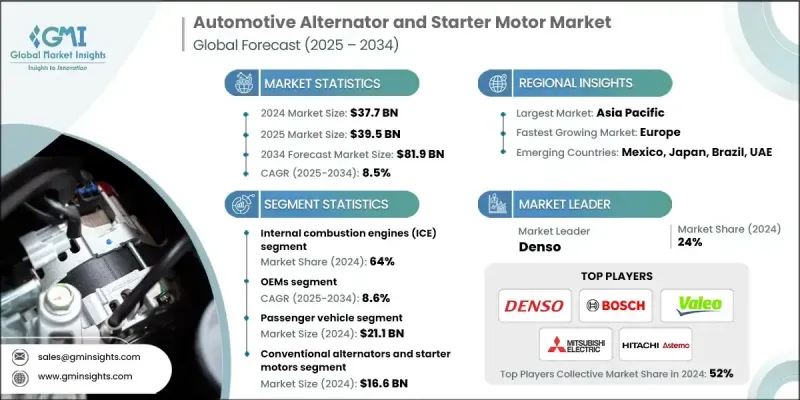

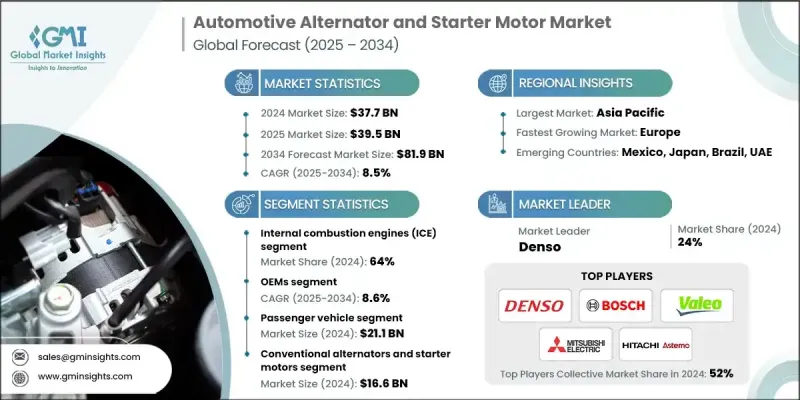

세계의 자동차용 얼터네이터 및 스타터 모터 시장 규모는 2024년 377억 달러로 평가되었고, CAGR 8.5%로 성장할 전망이며, 2034년 819억 달러에 이를 것으로 예측됩니다.

자동차 제조업체는 자동차 전동화의 진전, 하이브리드 자동차 및 전기자동차 수요 증가, 세계 배기 가스 규제 강화에 대응하고 있으며, 시장 성장이 가속화되고 있습니다. 배터리 기술이 지속적으로 발전하고 에너지 효율이 차량 설계의 중심이 됨에 따라 자동차 제조업체는 배출 가스와 연료 소비를 줄이면서 전력 트레인 성능을 높이는 전기 부품을 선호합니다. 통합된 차량 시스템은 얼터네이터 및 스타터 모터에 대한 요구를 증가시키고 있으며, 공급업체는 현대의 모빌리티 동향을 따르는 솔루션을 혁신적으로 제공할 필요가 있습니다. 기술 강화 및 스마트 차량 아키텍처도 이러한 기세에 기여하고 있습니다. 고효율, 경량, 지능형 시스템은 세계 표준 준수, 신뢰성 향상 및 운전 수명 연장을 보장하기 위해 구형 부품을 대체합니다. 자동차 제조업체와 공급업체 모두 산업이 지속 가능한 이동성으로 전환하는 동안 복잡한 전자 기능을 지원하고 엔진 운전을 최적화하며 최신 자동차의 에너지 관리를 강화하는 부품에 많은 투자를 하고 있습니다. 이러한 동향이 진화를 계속하고 있는 가운데, 얼터네이터 및 스타터 모터 기술은 자동차 전체의 성능에 있어서 보다 중심적인 존재가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 377억 달러 |

| 예측 금액 | 819억 달러 |

| CAGR | 8.5% |

2024년에는 내연기관(ICE) 부문이 64%의 점유율을 차지했습니다. 전기자동차의 상승에도 불구하고 내연 기관차는 여전히 세계 생산과 판매의 대부분을 차지하고 있습니다. 자동차 OEM과 차량 운행 회사는 입증된 ICE 기술에 계속 의존하고 있으며, 효율적인 에너지 사용, 엔진 신뢰성, 전자화가 진행되는 파워트레인과의 호환성을 지원하는 고성능 얼터네이터 및 스타터 모터가 필요합니다. 제조업체는 기존 차량 시스템과 원활하게 통합할 수 있도록 설계된 내구성과 비용을 최적화한 솔루션으로 대응합니다.

OEM 부문의 점유율은 71%로, 2034년까지 CAGR 8.6%로 성장할 것으로 예측됩니다. 자동차 제조업체는 엄격한 규제 및 효율 기준을 충족하는 고성능 얼터네이터 및 스타터 모터를 공장에서 설치하는 것을 선호하기 때문에 OEM 제조업체 수요는 계속 견조합니다. 계속해서 진화하는 배기가스 규제를 준수하고 차량의 전동화를 지원하며 장기적인 내구성을 제공하는 견고하고 신뢰할 수 있는 컴포넌트를 제공하는 데 중점을 두고 있습니다. OEM은 차세대 자동차의 품질 통합, 시스템 호환성 및 지속적인 성능을 보장하기 위해 부품 공급업체와의 협력을 계속하고 있습니다.

북미의 자동차용 얼터네이터 및 스타터 모터 시장은 2024년 81.1%의 점유율을 차지했으며, 82억 달러를 창출했습니다. 이 나라는 자동차 산업의 확대, 승용차 및 상용차의 보급, 하이브리드차 및 전동화 모델의 채용 증가에 의해 두드러지고 있습니다. 배출가스와 에너지 효율에 대한 강력한 규제 프레임워크가 제조업체에 새로운 기회를 가져오고 있으며, 첨단 얼터네이터 및 스마트 스타터 모터는 소비자의 기대와 정부의 의무를 모두 충족하는 데 필수적입니다.

세계의 자동차용 얼터네이터 및 스타터 모터 시장에서 주목할만한 기업으로는 Delphi Technologies, Robert Bosch, Hyundai Mobis, Hitachi Astemo, Mitsuba, Mitsubishi Electric, Lucas TVS, Denso, Valeo, BorgWarner 등이 있습니다. 세계 자동차용 얼터네이터 및 스타터 모터 시장의 주요 기업은 혁신, 효율성, OEM 요구와 전략적 무결성의 융합에 주력하고 글로벌 발자취를 강화하고 있습니다. 많은 기업들이 하이브리드 자동차, 내연 기관차, 마일드 하이브리드 자동차에 맞는 경량, 소형, 고효율 부품을 개발하고 있습니다. 자동차 제조업체와의 전략적 제휴를 통해 첨단 시스템의 맞춤화 및 원활한 통합이 가능합니다. 스톱 스타트 시스템, 회생 에너지 기능, 예측 진단 등의 스마트 기능도 중시되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 자동차 생산 및 판매 증가

- 전동화 및 하이브리드화 동향

- 차량의 노후화에 의한 애프터마켓 수요

- 기술적 진보

- 업계의 잠재적 위험 및 과제

- 풀 EV로의 시프트가 기존 수요 감소 초래

- 높은 연구개발 비용 및 전환 비용

- 시장 기회

- 세계의 배기가스 규제 강화

- 격렬한 가격 경쟁

- 공급망의 제약

- OEM 통합 및 통합 솔루션 선호

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 자동차 전기 시스템의 SAE 규격

- EPA 배출 가스 기준이 전기 부하에 미치는 영향

- 전기 부품의 NHTSA 안전 기준

- 국제 규격 조화(ISO, IEC)

- 커넥티드카의 사이버 보안 규제

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 스마트 교류 발전기 개발 및 가변 출력 제어

- 48V 마일드 하이브리드 시스템 통합

- 브러쉬리스 기술의 진보

- 통합 스타터 및 얼터네이터의 진화

- 에너지 관리 및 배터리 통합

- 예지보전 및 IOT의 통합

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 허브

- 수출입

- 비용 내역 분석

- 특허 분석

- 지속가능성 및 환경 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국

- 위험 평가 프레임워크

- 베스트 케이스 시나리오

- 고객분석 및 구매행동

- OEM 조달 기준 및 의사 결정의 틀

- 애프터마켓 소비자 기호 및 페인 포인트

- 브랜드 로열티 패턴

- 고객 부문별 가격 감응도 분석

- 무역 역학 및 관세 분석

- 수출입 동향 및 무역 흐름

- 지역별 관세 영향

- 무역정책의 변화 및 영향

- 로컬 컨텐츠 요건

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발표

- 확장 계획 및 자금 조달

제5장 시장 추계 및 예측 : 엔진별(2021-2034년)

- 주요 동향

- 내연기관(ICE)

- 하이브리드 엔진

- 전기자동차(EV) 파워트레인

제6장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- SUV

- 세단

- 해치백

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 이륜차

- 오프로드 자동차

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 기존 얼터네이터 및 스타터 모터

- 스마트 얼터네이터 및 스타터 모터

- 회생 제동 시스템

제8장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- 세계 기업

- BorgWarner

- Continental

- Delphi Technologies

- Denso

- Hitachi Astemo

- Lucas Electrical

- Mitsuba

- Mitsubishi Electric

- Robert Bosch

- Valeo

- 지역 기업

- ADVICS

- ASIMCO Technologies

- Cummins

- DB Electrical

- Guangzhou Sivco

- Hella

- Hyundai Mobis

- Lucas TVS

- Prestolite Electric

- 신흥 기업

- Broad-Ocean Technologies

- Controlled Power Technologies

- Ningbo Zhongwang AUTO Fittings

- PHINIA

- Unipoint

The Global Automotive Alternator and Starter Motor Market was valued at USD 37.7 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 81.9 billion by 2034.

Market growth is accelerating as automakers respond to increasing vehicle electrification, rising demand for hybrid and electric vehicles, and tougher global emission norms. As battery technology continues to evolve and energy efficiency becomes central to vehicle design, automotive manufacturers are prioritizing electrical components that enhance powertrain performance while reducing emissions and fuel consumption. Integrated vehicle systems are placing greater demands on alternators and starter motors, pushing suppliers to innovate and deliver solutions that align with modern mobility trends. Technological enhancements and smart vehicle architectures are also contributing to this momentum. High-efficiency, lightweight, and intelligent systems are replacing older components to ensure compliance with global standards, improve reliability, and extend operational lifespan. Both automakers and suppliers are investing heavily in components that support complex electronic functions, optimize engine operations, and enhance energy management in modern vehicles, particularly as the industry transitions toward sustainable mobility. As these trends continue to evolve, alternator and starter motor technologies are becoming more central to overall vehicle performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.7 Billion |

| Forecast Value | $81.9 Billion |

| CAGR | 8.5% |

In 2024, the internal combustion engine (ICE) segment held a 64% share. Despite the rise of electric vehicles, ICE-powered vehicles still dominate global production and sales. Automotive OEMs and fleet operators continue to rely on proven ICE technologies, requiring high-performance alternators and starter motors that support efficient energy use, engine reliability, and compatibility with increasingly electronic powertrains. Manufacturers are responding with durable and cost-optimized solutions engineered for seamless integration with traditional vehicle systems.

The OEM segment held a 71% share and is projected to grow at a CAGR of 8.6% through 2034. Demand from original equipment manufacturers remains strong, as automakers prioritize factory-installed, high-performance alternators and starter motors that meet stringent regulatory and efficiency standards. The focus remains on delivering robust, reliable components that comply with evolving emission norms, support vehicle electrification, and offer long-term durability. OEMs continue to partner with component suppliers to ensure quality integration, system compatibility, and sustained performance in next-generation vehicles.

North America Automotive Alternator and Starter Motor Market held 81.1% share in 2024, generating USD 8.2 billion. The country stands out due to its expansive automotive industry, widespread use of passenger and commercial vehicles, and increasing adoption of hybrid and electrified models. Strong regulatory frameworks around emissions and energy efficiency are creating new opportunities for manufacturers, as advanced alternators and smart starter motors become essential to meet both consumer expectations and government mandates.

Noteworthy companies in the Global Automotive Alternator and Starter Motor Market include Delphi Technologies, Robert Bosch, Hyundai Mobis, Hitachi Astemo, Mitsuba, Mitsubishi Electric, Lucas TVS, Denso, Valeo, and BorgWarner. Leading companies in the Global Automotive Alternator and Starter Motor Market are focusing on a blend of innovation, efficiency, and strategic alignment with OEM needs to strengthen their global footprint. Many are developing lightweight, compact, and high-efficiency components tailored for hybrid, ICE, and mild-hybrid vehicles. Strategic collaborations with automakers enable customization and seamless integration of advanced systems. Emphasis is also placed on smart features such as stop-start systems, regenerative energy capabilities, and predictive diagnostics.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Engine

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising vehicle production & sales

- 3.2.1.2 Electrification & hybridization trends

- 3.2.1.3 Aftermarket demand from aging fleets

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Shifts toward full EVs reducing traditional demand

- 3.2.2.2 High R&D and transition costs

- 3.2.3 Market opportunities

- 3.2.3.1 Stricter global emission regulations

- 3.2.3.2 Intense price competition

- 3.2.3.3 Supply chain constraints

- 3.2.3.4 OEM consolidation and preference for integrated solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 SAE standards for automotive electrical systems

- 3.4.2 EPA emissions standards impact on electrical load

- 3.4.3 NHTSA safety standards for electrical components

- 3.4.4 International standards harmonization (ISO, IEC)

- 3.4.5 Cybersecurity regulations for connected vehicles

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Smart alternator development & variable output control

- 3.7.2 48v mild hybrid system integration

- 3.7.3 Brushless technology advancement

- 3.7.4 Integrated starter-alternator evolution

- 3.7.5 Energy management & battery integration

- 3.7.6 Predictive maintenance & IOT integration

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Risk Assessment Framework

- 3.14 Best Case Scenarios

- 3.15 Customer Analysis & Buying Behavior

- 3.15.1 OEM procurement criteria and decision frameworks

- 3.15.2 Aftermarket consumer preferences and pain points

- 3.15.3 Brand loyalty patterns

- 3.15.4 Price sensitivity analysis by customer segment

- 3.16 Trade Dynamics & Tariff Analysis

- 3.16.1 Import/export trends and trade flows

- 3.16.2 Tariff impacts by region

- 3.16.3 Trade policy changes and implications

- 3.16.4 Local content requirements

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Engine, 2021 - 2034 ($ Bn & Units)

- 5.1 Key trends

- 5.2 Internal Combustion Engine (ICE)

- 5.3 Hybrid Engines

- 5.4 Electric Vehicle (EV) Powertrains

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Bn & Units)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.2.1 SUV

- 6.2.2 Sedan

- 6.2.3 Hatchback

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

- 6.4 Two-Wheelers

- 6.5 Off-Road Vehicles

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($ Bn & Units)

- 7.1 Key trends

- 7.2 Conventional Alternators and Starter Motors

- 7.3 Smart Alternators and Starter Motors

- 7.4 Regenerative Braking Systems

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($ Bn & Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 BorgWarner

- 10.1.2 Continental

- 10.1.3 Delphi Technologies

- 10.1.4 Denso

- 10.1.5 Hitachi Astemo

- 10.1.6 Lucas Electrical

- 10.1.7 Mitsuba

- 10.1.8 Mitsubishi Electric

- 10.1.9 Robert Bosch

- 10.1.10 Valeo

- 10.2 Regional players

- 10.2.1 ADVICS

- 10.2.2 ASIMCO Technologies

- 10.2.3 Cummins

- 10.2.4 DB Electrical

- 10.2.5 Guangzhou Sivco

- 10.2.6 Hella

- 10.2.7 Hyundai Mobis

- 10.2.8 Lucas TVS

- 10.2.9 Prestolite Electric

- 10.3 Emerging players

- 10.3.1 Broad-Ocean Technologies

- 10.3.2 Controlled Power Technologies

- 10.3.3 Ningbo Zhongwang AUTO Fittings

- 10.3.4 PHINIA

- 10.3.5 Unipoint