|

시장보고서

상품코드

1858832

우주용 전원 시장 : 시장 기회 및 촉진요인, 산업 동향 분석, 예측Space Power Supply Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast |

||||||

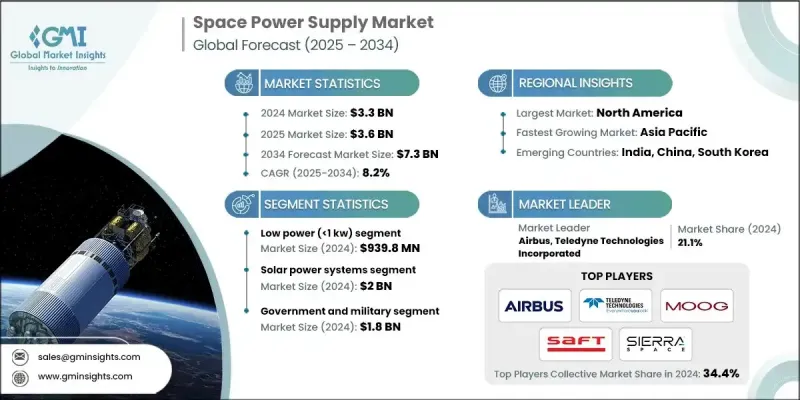

세계의 우주용 전원 시장은 2024년에는 33억 달러로 평가되었고, CAGR 8.2%로 성장할 전망이며, 2034년에는 73억 달러에 이를 것으로 예측되고 있습니다.

시장 성장은 위성 발사 증가, 태양광 발전 기술의 향상, 큐브 샛과 소형 위성 수요 증가, 지속가능성에 증가에 의해 추진되고 있습니다. 상업 임무의 가속 및 다양한 유형의 위성 운영을 지원하는 효율적인 전력 시스템에 대한 수요는 지속적으로 장기적인 기회를 창출하고 있습니다. 특히 통신, 지구 감시, 항법 등의 용도를 향한 대형 위성군의 급속한 전개가 수요를 더욱 밀어 올리고 있습니다. 북미는 첨단 항공우주 생태계, 풍부한 자금 지원, 최첨단 연구 투자, 국방 인프라에서 AI의 조기 채용으로 세계 상황을 선도하고 있습니다. 이 시장은 또한 공공기관과 민간우주기술 개발 기업 간의 전략적 제휴로부터 이익을 얻고 있습니다. 특히 방위 및 정보 시스템에서 AI 통합에 대한 정부 투자는 이 지역의 차세대 우주기술과 우주 자산의 미래에 있어 리더십을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 33억 달러 |

| 예측 금액 | 73억 달러 |

| CAGR | 8.2% |

저출력(1kW) 부문은 2024년 9억 3,980만 달러를 차지했습니다. 이 카테고리는 소형 위성 및 단기 임무와의 호환성으로 계속 번영하고 있습니다. 가볍고 비용 효율적인 전력 솔루션을 제공하므로 제한된 자원으로 운영되는 상업 및 과학 임무에 이상적입니다. 각 제조업체는 시스템 비용을 줄이면서 전력 밀도와 효율을 높이는 데 주력하고 있습니다. 큐브 싯이나 학술 용도를 목표로 하는 개발자에게 신뢰할 수 있는 컴팩트한 시스템 설계는 여전히 중요한 우선순위입니다.

태양광 발전 시스템 분야는 2024년 20억 달러에 달했습니다. 이 성장은 깨끗한 에너지원의 사용 증가, 성숙해지고 있는 태양광 발전 기술, 우주 공간에서의 태양광 조사가 중단되지 않는 이점과 관련되어 있습니다. 이러한 시스템은 커뮤니케이션, 방위, 조사 등의 임무에 점점 더 통합되어 있습니다. 각 회사는 태양전지판의 효율 향상, 질량 경감, 가혹한 우주 환경에 대응하기 위한 시스템 내구성 향상에 주력하고 있습니다. 이러한 진보는 임무의 수명을 연장하고 전반적인 전개 비용을 낮추는 열쇠입니다.

미국의 우주용 전원 2024년 시장 규모는 12억 달러에 달했습니다. 이 성장을 뒷받침하는 것은 우주 인프라의 급속한 업그레이드, 배터리 재활용에 중점을 둡니다. 제조업체 각사는 지속 가능하고 모듈화된 첨단 전력 기술에 중점을 두어 진화하는 요구에 대응하는 설계를 정돈하고 있습니다. 이러한 개발은 장기간의 미션을 지원하고, 규제의 이행을 용이하게 하며, 미션의 유연성 및 환경 스튜어드십에 중점을 둔 미래 대응 가능한 우주 환경을 실현하는 것을 목적으로 하고 있습니다.

세계 우주용 전원 시장의 혁신과 성장을 견인하는 주요 기업은 L3Harris Technologies, Inc., Renesas Electronics Corporation, GomSpace, Moog Inc., Rocket Lab USA, Airbus, NanoAvionics, EnerSys, VPT, Inc., DHV Technology, Modular Devices Inc. ET SPACE POWER, INC.、Teledyne Technologies Incorporated、Saft、Sierra Space Corporation、Apcon AeroSpace &Defence GmbH、GSYuasa Lithium Power、EaglePicher Technologies、AAC Clyde Space、Spectrolab、AZUR SPACE Solar Power GmbH 등이 있습니다. 우주용 전원 시장에서 사업을 전개하는 기업은 기술 혁신, 지속가능성, 세계 우주 미션과의 전략적 연계를 통해 전진하고 있습니다. 많은 기업들이 연구개발에 많은 투자를 하고, 소형 및 대형 우주선에 적합한 고효율로 경량인 전력 시스템을 개발하고 있습니다. 태양광 발전의 성능 향상, 배터리의 장수명화, 고방사선 환경 하에서의 열부하의 저감에 중점을 두고 있습니다. 궤도에서의 서비스 및 재사용성을 지원하기 위해 모듈식 시스템 설계가 채택되었습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 증가하는 위성 배치

- 솔라 패널 기술의 진보

- 소형 위성 및 큐브사트의 성장

- 지속 가능한 에너지 솔루션에 대한 수요 증가

- 상업 우주 미션 확대

- 업계의 잠재적 위험 및 과제

- 높은 개발 및 도입 비용

- 기술적 과제 및 신뢰성 문제

- 시장 기회

- 배터리 기술의 진보

- 전력 시스템의 소형화

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신의 전망

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품별

- 가격 전략

- 새로운 비즈니스 모델

- 컴플라이언스 요건

- 국방 예산 분석

- 세계의 방위비 동향

- 국방예산의 지역 배분

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 주요 방위 현대화 프로그램

- 예산 예측(2025-2034년)

- 업계 성장에 미치는 영향

- 국가별 방위 예산

- 공급망의 강인성

- 지정학적 분석

- 노동력 분석

- 디지털 변혁

- M&A, 전략적 파트너십 상황

- 위험 평가 및 관리

- 주요 계약 실적(2021-2024년)

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 시장 집중도 분석

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 실적 비교

- 수익

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 범위의 넓이

- 기술

- 혁신

- 지리적 존재 비교

- 세계 실적 분석

- 서비스 네트워크

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더

- 과제

- 팔로워

- 틈새 기업

- 전략적 전망 매트릭스

- 실적 비교

- 주요 발전(2021-2024년)

- 합병 및 인수

- 파트너십 및 협업

- 기술적 진보

- 사업 확대 및 투자 전략

- 지속가능성에 대한 노력

- 디지털 변혁에의 대처

- 신흥 및 벤처기업의 경쟁 환경

제5장 시장 추계 및 예측 : 전원별(2021-2034년)

- 주요 동향

- 태양광 발전 시스템

- 원자력 발전 시스템

- 배터리 시스템

- 연료 전지

- 하이브리드 시스템

제6장 시장 추계 및 예측 : 전력 용량별(2021-2034년)

- 주요 동향

- 저전력(1 kw 미만)

- 중전력(1-20kw)

- 고출력(20-100 kw)

- 초고출력(100 kw 초과)

제7장 시장 추계 및 예측 : 플랫폼별(2021-2034년)

- 주요 동향

- LEO(저궤도)

- MEO(중궤도)

- GEO(정지궤도)

- 심우주

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 인공위성

- 통신 분야

- 지구 관측

- 네비게이션(GNSS)

- 과학 및 기상 관측

- 기타

- 우주 정거장 및 허비타트

- ISS 및 상업 예정 스테이션

- 루나 게이트웨이

- 기타

- 탐사기 및 심우주 탐사기

- 행성 간 탐사기

- 로버

- 발사 로켓

- 기타

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 정부 및 군수

- 민간 사업자

- 연구기관

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 주요 기업

- Airbus

- L3 Harris Technologies, Inc.

- Moog Inc.

- EnerSys

- Rocket Lab USA

- 지역별 주요 기업

- 북미

- Teledyne Technologies Incorporated

- GSYuasa Lithium Power

- EaglePicher Technologies

- VPT, Inc.

- 유럽

- AAC Clyde Space

- AZUR SPACE Solar Power GmbH

- Apcon AeroSpace & Defence GmbH

- DHV Technology

- Saft

- NanoAvionics

- Modular Devices Inc.

- 8 XP Semiconductor

- Asia-Pacific

- Renesas Electronics Corporation

- GomSpace

- 북미

- 디스랩터 및 틈새 기업

- Sierra Space Corporation

- Spectrolab

- ET SPACE POWER, INC.

The Global Space Power Supply Market was valued at USD 3.3 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 7.3 billion by 2034.

The market growth is propelled by increasing satellite launches, improvements in photovoltaic technologies, rising demand for CubeSats and small satellites, and the growing push toward sustainability. The acceleration of commercial missions and the demand for efficient power systems to support various types of satellite operations continue to create long-term opportunities. Rapid satellite deployment, especially in the form of large constellations for applications in communication, earth monitoring, and navigation, further fuels demand. North America leads the global landscape, owing to its advanced aerospace ecosystem, substantial funding support, cutting-edge research investments, and early adoption of AI in national defense infrastructure. The market is also gaining from strategic collaborations between public agencies and private space technology developers. Government investment in AI integration, especially in defense and intelligence systems, reinforces the region's leadership in next-generation space technologies and futureproofing of space assets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 8.2% |

The low power (1 kW) segment accounted for USD 939.8 million in 2024. This category continues to thrive due to its compatibility with compact satellites and short-term missions. It offers a lightweight and cost-efficient power solution, making it ideal for commercial and scientific missions operating under constrained resources. Manufacturers are focusing on enhancing power density and efficiency while keeping system costs under control. The design of reliable, compact systems remains a critical priority for developers targeting CubeSats and academic applications.

The solar power systems segment reached USD 2 billion in 2024. This growth is linked to the rising use of clean energy sources, maturing photovoltaic technologies, and the advantage of uninterrupted solar exposure in space. These systems are increasingly integrated into communication, defense, and research missions. Companies are focusing efforts on improving solar panel efficiency, reducing mass, and boosting system durability to handle harsh space conditions. These advances are key to extending mission lifespans and lowering overall deployment costs.

United States Space Power Supply Market generated USD 1.2 billion in 2024. This growth is supported by rapid upgrades in space infrastructure, rising emphasis on battery recycling, progressive space regulations, and increased demand for in-orbit services such as refueling. Manufacturers are aligning their designs to meet evolving needs by focusing on sustainable, modular, and advanced power technologies. These developments aim to support long-duration missions, ease regulatory transitions, and enable a future-ready space environment with a strong emphasis on mission flexibility and environmental stewardship.

Leading players driving innovation and growth in the Global Space Power Supply Market include L3Harris Technologies, Inc., Renesas Electronics Corporation, GomSpace, Moog Inc., Rocket Lab USA, Airbus, NanoAvionics, EnerSys, VPT, Inc., DHV Technology, Modular Devices Inc., ET SPACE POWER, INC., Teledyne Technologies Incorporated, Saft, Sierra Space Corporation, Apcon AeroSpace & Defence GmbH, GSYuasa Lithium Power, EaglePicher Technologies, AAC Clyde Space, Spectrolab, and AZUR SPACE Solar Power GmbH. Companies operating in the Space Power Supply Market are advancing through innovation, sustainability, and strategic alignment with global space missions. Many are investing heavily in R&D to develop high-efficiency, lightweight power systems suitable for both small and large spacecraft. A strong focus is placed on enhancing photovoltaic performance, increasing battery life, and reducing thermal loads in high-radiation environments. Modular system design is being embraced to support in-orbit servicing and reusability.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Power source trends

- 2.2.2 Power capacity trends

- 2.2.3 Platform trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing Satellite Deployments

- 3.2.1.2 Advancements in Solar Panel Technology

- 3.2.1.3 Growth of Small Satellites and CubeSats

- 3.2.1.4 Rising Demand for Sustainable Energy Solutions

- 3.2.1.5 Expansion of Commercial Space Missions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Development and Deployment Costs

- 3.2.2.2 Technical Challenges and Reliability Issues

- 3.2.3 Market opportunities

- 3.2.3.1 Advancements in Battery Technologies

- 3.2.3.2 Miniaturization of Power Systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Defense Budget Analysis

- 3.13 Global Defense Spending Trends

- 3.14 Regional Defense Budget Allocation

- 3.14.1 North America

- 3.14.2 Europe

- 3.14.3 Asia Pacific

- 3.14.4 Middle East and Africa

- 3.14.5 Latin America

- 3.15 Key Defense Modernization Programs

- 3.16 Budget Forecast (2025-2034)

- 3.16.1 Impact on Industry Growth

- 3.16.2 Defense Budgets by Country

- 3.17 Supply Chain Resilience

- 3.18 Geopolitical Analysis

- 3.19 Workforce Analysis

- 3.20 Digital Transformation

- 3.21 Mergers, Acquisitions, and Strategic Partnerships Landscape

- 3.22 Risk Assessment and Management

- 3.23 Major Contract Awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Power Source, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Solar power systems

- 5.3 Nuclear power systems

- 5.4 Battery systems

- 5.5 Fuel cells

- 5.6 Hybrid systems

Chapter 6 Market Estimates and Forecast, By Power Capacity, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Low power (<1 kw)

- 6.3 Medium power (1-20 kw)

- 6.4 High power (20-100 kw)

- 6.5 Very high power (>100 kw)

Chapter 7 Market Estimates and Forecast, By Platform, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 LEO (low earth orbit)

- 7.3 MEO (medium earth orbit)

- 7.4 GEO (geostationary orbit)

- 7.5 Deep space

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Satellites

- 8.1.1 Communication

- 8.1.2 Earth observation

- 8.1.3 Navigation (GNSS)

- 8.1.4 Scientific & weather monitoring

- 8.1.5 Others

- 8.2 Space stations / habitats

- 8.2.1 ISS and planned commercial stations

- 8.2.2 Lunar gateway

- 8.2.3 Others

- 8.3 Spacecraft / deep-space probes

- 8.3.1 Interplanetary probes

- 8.3.2 Rovers

- 8.4 Launch vehicles

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million)

- 9.1 Government and military

- 9.2 Commercial operators

- 9.3 Research institutions

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company profiles

- 11.1 Global Key Players

- 11.1.1 Airbus

- 11.1.2. L3 Harris Technologies, Inc.

- 11.1.3 Moog Inc.

- 11.1.4 EnerSys

- 11.1.5 Rocket Lab USA

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Teledyne Technologies Incorporated

- 11.2.1.2 GSYuasa Lithium Power

- 11.2.1.3 EaglePicher Technologies

- 11.2.1.4 VPT, Inc.

- 11.2.2 Europe

- 11.2.2.1 AAC Clyde Space

- 11.2.2.2 AZUR SPACE Solar Power GmbH

- 11.2.2.3 Apcon AeroSpace & Defence GmbH

- 11.2.2.4 DHV Technology

- 11.2.2.5 Saft

- 11.2.2.6 NanoAvionics

- 11.2.2.7 Modular Devices Inc.

- 11.2.2. 8 XP Semiconductor

- 11.2.3 Asia-Pacific

- 11.2.3.1 Renesas Electronics Corporation

- 11.2.3.2 GomSpace

- 11.2.1 North America

- 11.3 Disruptors / Niche Players

- 11.3.1 Sierra Space Corporation

- 11.3.2 Spectrolab

- 11.3.3 ET SPACE POWER, INC.