|

시장보고서

상품코드

1858858

인쇄 전자용 전도성 잉크 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Conductive Inks for Printed Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

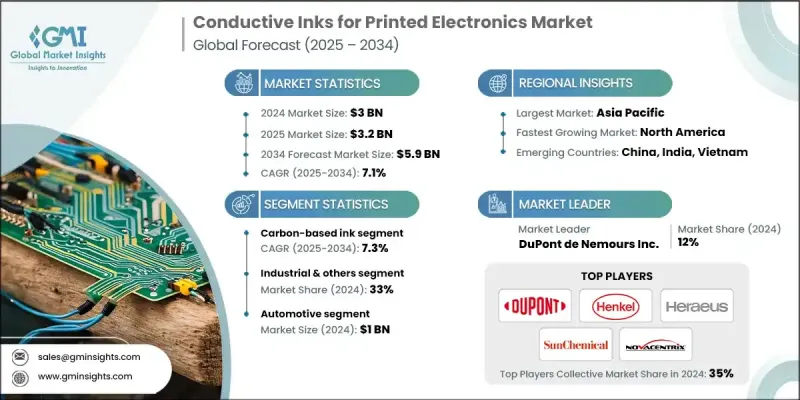

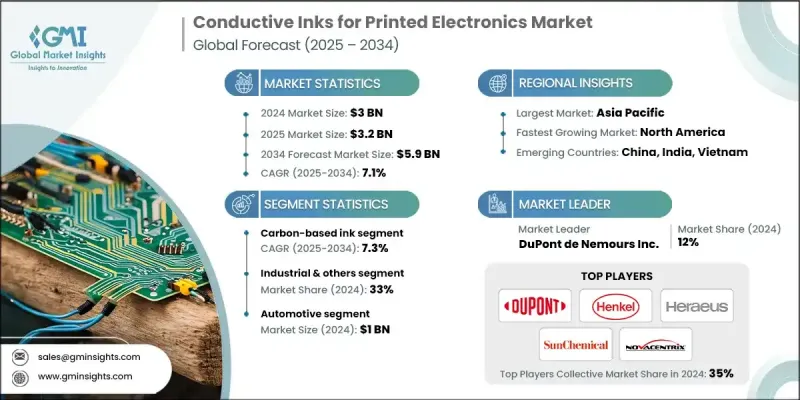

세계의 인쇄 전자용 전도성 잉크 시장 규모는 2024년에 30억 달러로 평가되었고, CAGR 7.1%를 나타내 2034년에는 59억 달러에 이를 것으로 예측되고 있습니다.

이 성장의 배경에는 유연한 전자 제품과 착용 가능한 전자 제품에 대한 수요가 증가하고 있습니다. 동시에 제품 설계의 소형화와 지속가능성에 대한 주목도 높아지고 있습니다. 결과적으로 제조업체와 소비자 모두 종이, 폴리머 및 섬유와 같은 다양한 기판 적합성을 제공하는 환경 친화적인 저 VOC 전도성 잉크로 눈을 돌리고 있습니다. 이러한 요구에 맞추기 위해 효율적으로 생산 규모를 확대하면서 폐기물을 최소화하는 첨가제를 이용한 새로운 생산 방법이 출현하고 있습니다. 각 회사는 은 나노입자, 구리 플레이크, 그래핀, 탄소나노튜브 등의 재료를 이용한 첨단 배합을 도입하여 RFID 태그, 프린트 센서, 플렉서블 회로, 태양전지 등의 고성능 용도를 타겟으로 하고 있습니다. 또한 광소결 잉크와 UV 경화형 잉크는 섬세한 재료에 필수적인 저온 처리에 적합하기 때문에 수요가 높아지고 있습니다. 전도성 잉크는 프린트 히터, IoT 장치, 의료용 일회용 바이오센서 등 다양한 신흥 용도에도 사용되고 있으며, 이들 모두가 시장 확대에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 30억 달러 |

| 예측 금액 | 59억 달러 |

| CAGR | 7.1% |

2024년에는 은 잉크 분야가 80%의 점유율을 차지했습니다. 이는 뛰어난 전도성으로 인해 고성능 용도에 이상적입니다. 은 잉크는 일반적으로 금속은의 80%에 가까운 전도도를 달성하기 때문에 태양광 발전의 금속화, RFID 안테나 제조, 정밀 회로 인쇄 등의 용도에 매우 적합합니다.

산업용도 분야는 2024년에 33%의 점유율을 차지했습니다. 이 성장의 원동력은 태양에너지, 특히 박막 태양전지의 진보이며, 전도성 잉크는 태양전지의 금속 화에 필수적입니다. 이 잉크는 태양전지 모듈의 효율성과 확장성에 중요한 전면 그리드 라인, 후면 접촉 및 상호 연결 시스템을 인쇄하는 데 사용됩니다.

북미의 인쇄 전자용 전도성 잉크 시장은 2024년 30.2%의 점유율을 차지했습니다. 이 지역의 성장은 고도의 5G 시스템의 전개, 자동차의 전동화나 항공우주 용도로의 추진 등 기술적 진보에 의한 점이 큽니다. 북미에서는 우수한 성능 특성을 가진 프리미엄 잉크 수요가 높아지고 있습니다. 또한 경쟁 환경은 재생 에너지와 전기자동차 인프라 홍보를 목표로 정부의 이니셔티브에 의해 형성되어 전도성 잉크 공급업체에 유리한 시장을 형성하고 있습니다.

인쇄 전자용 전도성 잉크 시장의 주요 기업은 Henkel AG & Co.KGaA, DuPont Electronics & Industrial, SPGPrints BV, NovaCentrix, Heraeus Holding GmbH, Advanced Nano Products(ANP), Voltera Inc. Nano Inc., Electronics Incorporated, Agfa-Gevaert Group 등이 있습니다. 인쇄 전자용 전도성 잉크 시장의 기업은 그 존재감을 높이기 위해 환경 친화적이고 고성능인 제품의 개발에 주력하고 있습니다. 많은 기업들이 R&D에 투자하고 신재생에너지와 웨어러블 기술 등 특정 용도에 대응하는 혁신적인 잉크 처방을 창출하고 있습니다. 전략적 제휴 및 협력 관계도 일반적이며 신규 시장 진입과 제품 포트폴리오 확대에 도움이 됩니다. 증가하는 지속가능성에 대한 요구를 충족시키기 위해 낮은 VOC 및 재활용 가능한 잉크 시스템을 도입하는 기업도 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 5G와 mm파 기술의 채용 가속

- 플렉서블 일렉트로닉스와 웨어러블 디바이스의 보급

- 자동차의 전동화와 스마트 차량 통합

- 업계의 잠재적 리스크 및 과제

- 은 가격의 변동과 원료 비용의 압력

- 전도성과 내구성에 있어서 기술적 한계

- 시장 기회

- 구리 잉크 개발 및 비용 절감 가능성

- 지속 가능한 재활용 소재의 혁신

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 기술별

- 향후 시장 동향

- 기술과 혁신의 전망

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 대해서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십

- 신제품 발표

- 확장 계획

제5장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 은 베이스 잉크

- 탄소 베이스 잉크

- 구리 잉크

- 특수 잉크

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 산업 및 기타

- 플렉서블 일렉트로닉스

- 헬스케어

- 자동차

- 태양광 발전

- IoT 및 연결성

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 자동차

- 헬스케어 및 의료기기

- 통신

- 포장

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- DuPont Electronics &Industrial

- Henkel AG &Co. KGaA

- Heraeus Holding GmbH

- Sun Chemical Corporation

- NovaCentrix

- Agfa-Gevaert Group

- Voltera Inc.

- XTPL SA

- Advanced Nano Products(ANP)

- Copprint Technologies

- Electroninks Incorporated

- SPGPrints BV

- C3 Nano Inc.

The Global Conductive Inks for Printed Electronics Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 5.9 billion by 2034.

The growth is attributed to the increasing demand for flexible and wearable electronics, which are becoming increasingly popular across various industries. At the same time, there is a growing focus on miniaturization and sustainability in product design. As a result, both manufacturers and consumers are turning toward eco-friendly, low-VOC conductive inks that offer broad substrate compatibility, such as with paper, polymers, and textiles. To align with these needs, new production methods have emerged, utilizing additives to minimize waste while scaling up production efficiently. Companies have introduced advanced formulations with materials like silver nanoparticles, copper flakes, graphene, and carbon nanotubes, targeting high-performance applications such as RFID tags, printed sensors, flexible circuits, and solar cells. Additionally, the demand for photonic sintering and UV-curable inks is rising due to their suitability for low-temperature processing, which is crucial for sensitive materials. Conductive inks are also used in various emerging applications, including printed heaters, IoT devices, and disposable biosensors for healthcare, all contributing to the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 7.1% |

In 2024, the silver ink segment held an 80% share. This is due to its excellent electrical conductivity, which makes it ideal for high-performance applications. Silver inks typically achieve conductivities close to 80% of that of metallic silver, making them highly suitable for uses like photovoltaic metallization, RFID antenna production, and precision circuit printing.

The industrial applications segment held a 33% share in 2024. This growth is driven by advancements in solar energy, particularly in thin-film solar cells, where conductive inks are crucial for metallizing photovoltaic cells. These inks are used to print the front-side grid lines, back-side contacts, and interconnection systems, which are critical for the efficiency and scalability of solar modules.

North America Conductive Inks for Printed Electronics Market held a 30.2% share in 2024. The region's growth is largely driven by technological advancements, including the deployment of advanced 5G systems and the push toward automotive electrification and aerospace applications. North America's demand for premium ink formulations is rising, as these inks are needed for their superior performance characteristics. Additionally, the competitive environment is being shaped by government initiatives aimed at promoting renewable energy and the infrastructure of electric vehicles, creating a favorable market for conductive ink suppliers.

Leading players in the Conductive Inks for Printed Electronics Market include Henkel AG & Co. KGaA, DuPont Electronics & Industrial, SPGPrints B.V., NovaCentrix, Heraeus Holding GmbH, Advanced Nano Products (ANP), Voltera Inc., Sun Chemical Corporation, XTPL S.A., Copprint Technologies, C3 Nano Inc., Electroninks Incorporated, Agfa-Gevaert Group, and others. To bolster their presence, companies in the conductive inks for printed electronics market are focusing on developing eco-friendly and high-performance products. Many companies are investing in R&D to create innovative ink formulations that cater to specific applications, including renewable energy and wearable technology. Strategic partnerships and collaborations are also common, helping businesses access new markets and expand their product portfolios. To meet growing sustainability demands, some companies are introducing low-VOC and recyclable ink systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 5G & mmWave technology adoption acceleration

- 3.2.1.2 Flexible electronics & wearable device proliferation

- 3.2.1.3 Automotive electrification & smart vehicle integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Silver price volatility & raw material cost pressures

- 3.2.2.2 Technical limitations in conductivity & durability

- 3.2.3 Market opportunities

- 3.2.3.1 Copper ink development & cost reduction potential

- 3.2.3.2 Sustainable & recycled material innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By technology

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million & Tons)

- 5.1 Key trends

- 5.2 Silver-based inks

- 5.3 Carbon-based inks

- 5.4 Copper inks

- 5.5 Specialty inks

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Tons)

- 6.1 Key trends

- 6.2 Industrial & others

- 6.3 Flexible electronics

- 6.4 Healthcare

- 6.5 Automotive

- 6.6 Photovoltaics

- 6.7 IoT & connectivity

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million & Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Healthcare & medical device

- 7.4 Telecommunications

- 7.5 Packaging industry

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 DuPont Electronics & Industrial

- 9.2 Henkel AG & Co. KGaA

- 9.3 Heraeus Holding GmbH

- 9.4 Sun Chemical Corporation

- 9.5 NovaCentrix

- 9.6 Agfa-Gevaert Group

- 9.7 Voltera Inc.

- 9.8 XTPL S.A.

- 9.9 Advanced Nano Products (ANP)

- 9.10 Copprint Technologies

- 9.11 Electroninks Incorporated

- 9.12 SPGPrints B.V.

- 9.13 C3 Nano Inc.