|

시장보고서

상품코드

1858998

혈관 폐쇄 기기 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Vascular Closure Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

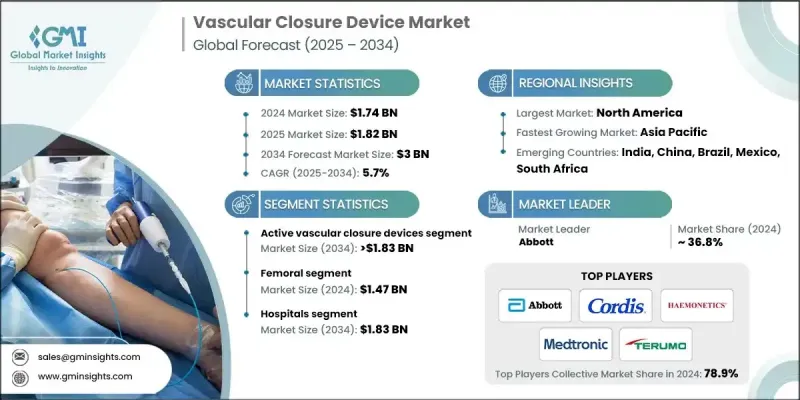

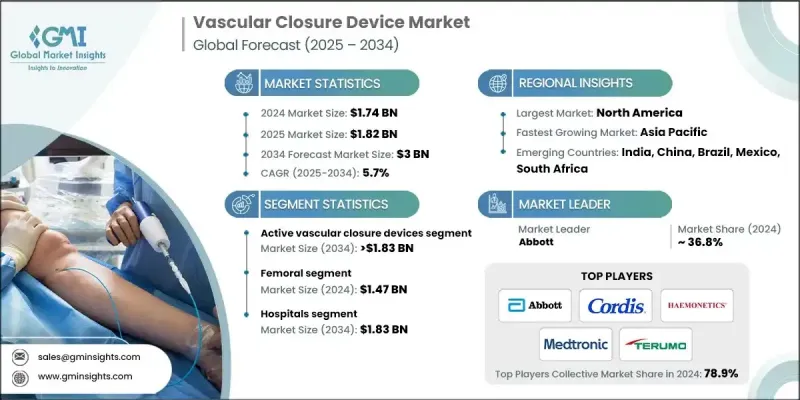

세계의 혈관 폐쇄 기기 시장은 2024년에 17억 4,000만 달러로 평가되었고 CAGR 5.7%를 나타내 2034년에는 30억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 심혈관 질환의 유병률 증가, 인터벤셔널 심장학 및 방사선학적 치료 증가, 외래 환자 및 당일 퇴원 치료 수요 증가 등 몇 가지 요인에 기인합니다. 혈관 폐쇄 기기는 카테터 치료 후 동맥 천자를 기계적 클립, 봉합사 또는 콜라겐 플러그 중 하나를 사용하여 밀봉하도록 설계된 필수 의료기기입니다. 이러한 기구는 수동 압박과 같은 전통적인 방법에 비해 보다 빠르고 효율적인 지혈을 제공하고, 지혈에 필요한 시간을 단축하고, 환자의 다운타임을 최소화합니다. 관상동맥질환과 심부전과 같은 심혈관질환이 세계적으로 증가함에 따라 혈관조영과 인터벤셔널 수술이 보다 많이 실시되고 있어 혈관 폐쇄 기기 수요를 더욱 밀어 올리고 있습니다. 게다가 생체흡수성 폐쇄 기기나 혈관외 밀봉 시스템 등의 기술 혁신은 출혈과 감염 등의 합병증에 대처함으로써 VCD의 채용을 확대하고 환자의 결과를 개선하여 시장 성장을 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 17억 4,000만 달러 |

| 예측 금액 | 30억 달러 |

| CAGR | 5.7% |

능동적 혈관 폐쇄 기기는 우수한 효능, 빠른 지혈 시간 및 합병증 발생률이 낮기 때문에 2024년에는 59.3%의 점유율을 차지했습니다. 봉합사 기반 및 콜라겐 기반 장치를 포함한 능동적 혈관 폐쇄 기기는 혈관 접근 부위를 폐쇄하는 능력으로 인해 더 빠른 회복 및 보다 효율적인 카테터 치료를 가능하게 하기 위해 의사가 점점 더 선호되고 있습니다. 이 분야는 카테터 실험실의 성능 향상과 수술 시간 단축을 가능하게 함으로써 앞으로도 주도권을 유지할 것으로 예측됩니다.

요골동맥 부문은 2025-2034년에 CAGR 4.4%를 나타낼 전망입니다. 요골 동맥 접근은 대퇴 동맥 접근에 비해 출혈성 합병증의 위험이 낮고 회복이 빠르기 때문에 인터벤셔널 심장 병학에서 선호되는 선택이되고 있습니다. 건강 관리 환경에서 수행되는 요골 동맥 치료의 수가 증가함에 따라이 분야의 특수 폐쇄기구에 대한 수요가 촉진되고 있습니다.

북미 혈관 폐쇄 기기 2024년 점유율은 44.9%에 달했습니다. 고급 헬스케어 인프라, 최첨단 카테터 검사실, 고급 기술을 갖춘 인터벤셔널 카디올로지스트가 존재하는 것이 봉합사를 통한 것 및 콜라겐 기반의 것 등 고급 VCD가 널리 받아들여 사용되는 요인이 되고 있습니다. 회복 시간을 단축하고 건강 관리 비용을 줄이기 위한 저침습 심장혈관 수술의 동향은 이러한 장비에 대한 수요를 더욱 밀어 올리고 있습니다.

세계 혈관 폐쇄 기기 시장의 주요 기업으로는 Medtronic, Teleflex, MERIT MEDICAL, Abbott, Rex Medical, Cordis, Ensite Vascular, Terumo, HAEMONETICS, Vivasure Medical, Transluminal Technologies, Vasorum, Tricol Biomedical, Meril 등이 있습니다. 세계 혈관 폐쇄 기기 시장의 기업은 시장에서의 지위를 확고하게 하기 위해 제품의 혁신을 강화하고 환자의 결과를 개선하는 데 주력하고 있습니다. 많은 기업들이 합병증과 회복 시간을 단축하는 첨단 저침습 기술 개발에 투자하고 있습니다. 건강 관리 제공업체 및 연구 기관과의 전략적 제휴 및 공동 연구도 시장에 도달하는 것을 확대하고 임상 검증을 얻기 위해 일반적으로 수행됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심혈관 질환을 앓고 있는 환자 증가

- 노년 인구 증가

- 혈관 폐쇄 기기의 기술적 진보

- 인터벤셔널 카디올로지와 방사선 치료의 건수 증가

- 업계의 잠재적 위험 및 과제

- 절차 후 합병증과 관련된 고위험

- 엄격한 규제 시나리오

- 시장 기회

- 신흥 시장 진출

- 생체 흡수성 폐쇄 기기와 차세대 폐쇄 기기의 개발

- 성장 촉진요인

- 성장 가능성 분석

- 상환 시나리오

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 상황

- 현재의 기술 동향

- 신흥기술

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카·중동·아프리카

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 새로운 디바이스 유형 출시

- 확장 계획

제5장 시장 추계·예측 : 디바이스 유형별(2021-2034년)

- 주요 동향

- 능동적 혈관 폐쇄 기기

- 콜라겐 플러그 매개 장치

- 봉합사 매개 장치

- 스테이플/클립 매개 VCD

- 수동적 혈관 폐쇄 기기

- 지혈 패드/패치

- 압박 장치

제6장 시장 추계·예측 : 접근별(2021-2034년)

- 주요 동향

- 대퇴동맥

- 요골동맥

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래 수술 센터(ASC)

- 기타 최종 사용

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott

- Cordis

- Ensite Vascular

- HAEMONETICS

- Medtronic

- Meril

- MERIT MEDICAL

- Rex Medical

- Teleflex

- TERUMO

- Transluminal Technologies

- Tricol Biomedical

- TZ Medical

- Vasorum

- Vivasure Medical

The Global Vascular Closure Device Market was valued at USD 1.74 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 3 billion by 2034.

This growth can be attributed to several factors, including the rising prevalence of cardiovascular diseases, the growth of interventional cardiology and radiology procedures, and the increasing demand for outpatient and same-day discharge procedures. Vascular closure devices are essential medical tools designed to seal arterial punctures after catheterization procedures, either using mechanical clips, sutures, or collagen plugs. These devices offer quicker and more efficient hemostasis compared to traditional methods like manual compression, reducing the time needed for bleeding cessation and minimizing patient downtime. As cardiovascular diseases like coronary artery disease and heart failure rise globally, more angiographies and interventional procedures are performed, further driving the demand for vascular closure devices. Additionally, innovations such as bioabsorbable closure devices and extravascular sealing systems have expanded the adoption of VCDs by addressing complications like bleeding and infection, which improves patient outcomes and accelerates market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.74 Billion |

| Forecast Value | $3 Billion |

| CAGR | 5.7% |

The active vascular closure devices segment held 59.3% share in 2024, owing to their superior efficacy, faster hemostasis times, and lower complication rates. Active VCDs, including suture-based and collagen-based devices, are increasingly preferred by physicians for their ability to close vascular access sites, enabling faster recovery and more efficient catheterization procedures. This segment is expected to maintain its leadership as it allows for improved cath lab performance and shorter operation times.

The radial artery segment will grow at a CAGR of 4.4% during 2025-2034. Radial access is becoming the preferred choice in interventional cardiology because it carries a lower risk of bleeding complications and allows for faster recovery compared to femoral access. The increasing number of radial artery procedures performed in healthcare settings is driving the demand for specialized closure devices in this area.

North America Vascular Closure Device Market held a 44.9% share in 2024. The presence of advanced healthcare infrastructure, cutting-edge catheterization labs, and highly skilled interventional cardiologists contributes to the widespread acceptance and use of advanced VCDs, such as suture-mediated and collagen-based devices. The trend towards minimally invasive cardiovascular procedures, designed to shorten recovery times and reduce healthcare costs, further boosts the demand for these devices.

Key players in the Global Vascular Closure Device Market include Medtronic, Teleflex, MERIT MEDICAL, Abbott, Rex Medical, Cordis, Ensite Vascular, Terumo, HAEMONETICS, Vivasure Medical, Transluminal Technologies, Vasorum, Tricol Biomedical, and Meril. To solidify their market position, companies in the Global Vascular Closure Device Market focus on enhancing product innovation and improving patient outcomes. Many companies are investing in the development of advanced, minimally invasive technologies that reduce complications and recovery times. Strategic partnerships and collaborations with healthcare providers and research institutions are also common to expand market reach and gain clinical validation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Device type trends

- 2.2.3 Access trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of patients suffering from cardiovascular diseases

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Technological advancements in vascular closure devices

- 3.2.1.4 Rising volume of interventional cardiology and radiology procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk associated with post-procedural complications

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 Development of bioresorbable and next-generation closure devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Vascular closure device market, 2021-2034 (Units)

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New device type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Device Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Active vascular closure devices

- 5.2.1 Collagen plug mediated device

- 5.2.2 Suture-mediated devices

- 5.2.3 Staple/clip-mediated VCD

- 5.3 Passive vascular closure devices

- 5.3.1 Haemostasis pads/patches

- 5.3.2 Compression devices

Chapter 6 Market Estimates and Forecast, By Access, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Femoral

- 6.3 Radial

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 Cordis

- 9.3 Ensite Vascular

- 9.4 HAEMONETICS

- 9.5 Medtronic

- 9.6 Meril

- 9.7 MERIT MEDICAL

- 9.8 Rex Medical

- 9.9 Teleflex

- 9.10 TERUMO

- 9.11 Transluminal Technologies

- 9.12 Tricol Biomedical

- 9.13 TZ Medical

- 9.14 Vasorum

- 9.15 Vivasure Medical