|

시장보고서

상품코드

1859010

물류 로봇 시장 기회와 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Logistics Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

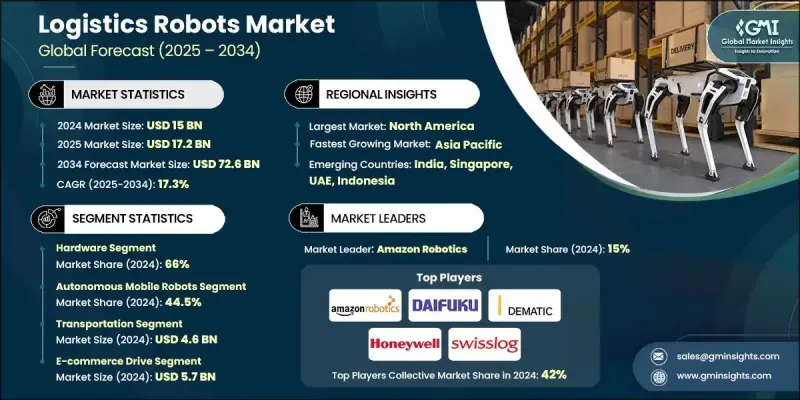

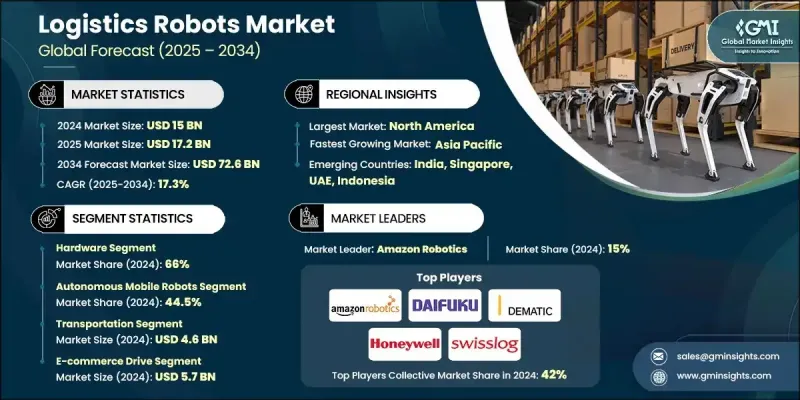

세계의 물류 로봇 시장 규모는 2024년에 150억 달러로 평가되었고, CAGR 17.3%를 나타내 2034년에는 726억 달러에 이를 것으로 예측되고 있습니다.

이 분야는 자동화에 대한 수요 증가, 납기 엄격화, 공급망의 첨단 디지털화에 의해 형성되고 빠르게 진화하고 있습니다. 이 산업은 지리적 통합, 전략적 공급업체와의 관계, 강력한 수직 통합을 특징으로 하는 복잡한 생태계에 의해 정의됩니다. 로봇 기술이 성숙함에 따라 물류 기업은 소비자의 기대에 부응하고 운영 비효율성을 줄이기 위해 자율 시스템으로의 전환을 가속화하고 있습니다. ROI의 가속화와 투자 회수 기간의 단축이 창고 및 배송 센터에 지능형 로봇 시스템의 폭넓은 도입을 촉진하고 있습니다. 이 자동화 파동은 더 높은 처리량, 정확성 향상, 노동력 슬림화를 가능하게 하여 물류 인프라를 재구성하여 궁극적으로 선진국 시장과 신흥국 시장의 성장을 가속하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 150억 달러 |

| 예측 금액 | 726억 달러 |

| CAGR | 17.3% |

2024년 하드웨어 분야 점유율은 66%를 차지했고 2034년까지 연평균 복합 성장률(CAGR)은 16.4%를 나타낼 것으로 예상됩니다. 로봇 플랫폼, 기계 부품 및 이동 시스템은 물류 로봇 솔루션의 기초 레이어를 형성하여 창고 및 마지막 마일 환경에서 원활한 운영을 가능하게 합니다. 로봇동력시스템에 관한 기술의 진보와 연구 이니셔티브는 하드웨어의 비용구조를 재구성하고 있지만, 물류업무에 있어서 인간의 관여는 여전히 총비용의 대부분을 차지하고 있습니다.

자율이동 로봇(AMR) 부문은 2024년에 44.5%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 17.9%를 나타낼 것으로 예측됩니다. AMR은 인공지능, 시각 SLAM 및 적응형 센서 기술을 이용한 고급 네비게이션 시스템을 통해 기존의 자동 유도 차량보다 훨씬 효율적으로 향상됩니다. 이러한 기능은 복잡하고 역동적인 환경에서 실시간 의사결정을 가능하게 하고, 이 분야를 파일럿 단계에서 대규모 상업 배포로 전환시킵니다.

미국은 2024년에 65%의 점유율을 차지해 46억 달러를 창출했습니다. 세계 벤치마크와 비교하면 보급률은 상대적으로 낮지만 미국의 성장은 노동력 부족, 기술적 준비, 자동화에 대한 연방 정부의 지원에 의해 지원됩니다. 견고한 인프라와 정부 출자 혁신 프로그램은 세계 로봇 사정에서 동국의 지위를 지속적으로 강화하고 물류에서 로봇 솔루션의 대규모 도입에 유리한 환경을 창출하고 있습니다.

세계의 물류 로봇 시장 경쟁 구도를 형성하는 주요 업계 기업은 ABB, Yaskawa Electric, Toyota/Bastian, Omron, Daifuku, Amazon Robotics, KUKA/Swisslog, KION/Dematic, Honeywell, AutoStore 등입니다. 그 지위를 강화하기 위해 물류 로봇 기업은 AI를 활용한 자동화, 실시간 데이터 분석, 다양한 물류 이용 사례에 맞는 모듈식 시스템 설계를 우선하고 있습니다. 전략적 합병과 파트너십은 기술 공유 및 지리적 확장을 가능하게 하고 R&D 투자는 다중 용도 기능을 위한 확장 가능한 플랫폼을 창출합니다. 대기업은 또한 전자상거래, 제3자 물류 및 소매 창고 환경에 맞추어 로봇 플릿을 맞춤화하여 장기적인 고객 유지와 운영 ROI 향상을 실현하고 있습니다. 세계 기업은 현지 생산, 서비스 네트워크 확대, 원활한 물류 오케스트레이션 및 예지 보전을 가능하게 하는 통합 디지털 플랫폼을 통해 그 존재감을 더욱 높여 가고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 자율 이동 로봇 제조업체

- 자동 보관 및 검색 시스템 프로바이더

- 로보틱스 소프트웨어 및 AI 플랫폼 개발자

- 창고 인프라 및 자재관리 장비 공급업체

- 시스템 통합자 및 솔루션 제공업체

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 디스랩터

- 공급자의 상황

- 영향요인

- 성장 촉진요인

- 피킹 용도에 있어서 전자상거래 분야의 발전

- 로봇 기술의 진보

- 보급이 진행되는 자율형 창고

- 물류에서의 지속가능성에 대한 의식 증가

- 업계의 잠재적 위험 및 과제

- 구입 및 도입 비용의 높이 물류 로봇

- 고도의 로봇 시스템을 운용 및 보수하는 종업원의 스킬 부족

- 시장 기회

- 물류 로봇의 AI와 IoT의 융합 물류 로봇

- 협동 로봇의 도입

- 성장 촉진요인

- 기술 동향 및 혁신 에코시스템

- 현재의 기술

- 컴퓨터 비전과 물체 인식

- 예측 분석 및 유지보수

- 다기능 로봇 개발

- 인간과 로봇의 협동의 진전

- 새로운 기술

- 5G 커넥티비티 및 통신 시스템

- 디지털 트윈 및 시뮬레이션 기술

- 블록체인과 공급체인의 투명성

- 지속가능성과 녹색기술의 통합

- 현재의 기술

- 성장 가능성 분석

- 규제 상황

- 연방 안전 기준의 틀

- ANSI/RIA R15.06 요구사항

- ANSI R15.08 이동 로봇 규격

- ISO 10218 세계 하모나이제이션

- OSHA 컴플라이언스 요건

- 일반 의무 조항의 적용

- 기계 및 기계 경비 기준

- 전기 안전 요건

- 업계 특유의 규제 요건

- FDA 헬스케어 규제

- 식품안전 및 HACCP 컴플라이언스

- 자동차 업계 표준

- 국제표준의 조화

- ISO 기술위원회 299

- 유럽 규격의 통합

- 지역 적응 요건

- 연방 안전 기준의 틀

- 코스트 내역 분석

- 하드웨어 비용 구성 요소

- 소프트웨어 및 통합 비용

- 인프라 개조 요건

- 유지보수 및 서비스 비용

- Porter's Five Forces 분석

- PESTEL 분석

- 지속가능성과 환경 측면

- 환경영향 평가 및 라이프사이클 분석

- 사회적 영향과 지역사회의 관계

- 거버넌스와 기업 책임

- 지속가능한 기술 개발

- 위험 평가 프레임워크

- 상호 운용성과 표준화의 갭

- 레거시 시스템 호환성의 과제

- 규제 및 컴플라이언스 리스크

- 재무 리스크 경감 전략

- 성능 및 품질 기준

- 위험 평가 방법

- 정밀도 기준

- 업계 특유의 품질 요건

- 안전시험 요건

- 이용 사례

- 아마존의 로봇 도입 모델

- 멀티 SKU 핸들링 및 정렬

- 자동차 제조의 통합

- 헬스케어및제약 용도

- 써드파티 로지스틱스의 최적화

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발표

- 확장계획 및 자금조달

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 하드웨어

- 로봇 플랫폼 및 섀시

- 센서 및 인식 시스템

- 액추에이터 및 조작 시스템

- 기타

- 소프트웨어

- 로봇 운영 체제

- 플릿 관리 소프트웨어

- 창고 관리 통합

- 기타

- 서비스

- 전문

- 관리형

제6장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 자동 유도 차량(AGV)

- 자율 이동 로봇

- 로봇 암

- 기타

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 팔레타이징 및 디팔레타이징

- 픽 앤 플레이스

- 운송

- 기타

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 전자상거래

- 헬스케어

- 소매

- 식음료

- 자동차

- 기타

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- ABB

- Amazon Robotics

- AutoStore

- Daifuku

- Honeywell

- KION/Dematic

- KUKA/Swisslog

- Omron

- Toyota/Bastian

- Yaskawa Electric

- 지역 기업

- Bastian Solutions

- Geek

- GreyOrange

- Locus Robotics

- Vecna Robotics

- 신흥 기업

- VisionNav Robotics

- Berkshire Grey

- Covariant

- Exotec

- River Systems

The Global Logistics Robots Market was valued at USD 15 billion in 2024 and is estimated to grow at a CAGR of 17.3% to reach USD 72.6 billion by 2034.

This sector is evolving rapidly, shaped by growing demand for automation, tighter delivery timelines, and advanced supply chain digitization. The industry is defined by its intricate ecosystem, which is marked by geographic clustering, strategic supplier relationships, and strong vertical integration. As robotics technologies mature, logistics firms are increasingly transitioning toward autonomous systems to meet rising consumer expectations and reduce operational inefficiencies. Accelerated ROI and shrinking payback windows are prompting broader deployment of intelligent robotics systems across warehouse and distribution centers. This wave of automation is reshaping logistics infrastructure by enabling higher throughput, improved accuracy, and leaner workforce dependencies, ultimately fueling growth across developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15 Billion |

| Forecast Value | $72.6 Billion |

| CAGR | 17.3% |

In 2024, the hardware segment held a 66% share and is expected to grow at a CAGR of 16.4% through 2034. Robotic platforms, mechanical components, and mobility systems form the foundational layer of logistics robotics solutions, enabling seamless operation in warehouse and last-mile environments. Technological advancements and research initiatives into robotics power systems are reshaping the hardware cost structures, although human involvement in logistics operations still accounts for a large portion of total expenses.

The autonomous mobile robots (AMRs) segment held a 44.5% share in 2024 and is forecasted to grow at a CAGR of 17.9% between 2025 and 2034. AMRs offer significant efficiency gains over traditional automated guided vehicles due to advanced navigation systems powered by artificial intelligence, visual SLAM, and adaptive sensor technology. These capabilities allow for real-time decision-making in complex, dynamic environments, moving the segment from pilot phases into large-scale commercial deployments.

U.S. Logistics Robots Market held 65% share in 2024, generating USD 4.6 billion. Despite relatively low penetration compared to global benchmarks, growth in the U.S. is underpinned by labor shortages, technological readiness, and federal support for automation. Robust infrastructure and government-funded innovation programs continue to strengthen the country's position in the global robotics landscape, creating a favorable environment for the large-scale implementation of robotic solutions in logistics.

Key industry players shaping the competitive landscape of the Global Logistics Robots Market include ABB, Yaskawa Electric, Toyota/Bastian, Omron, Daifuku, Amazon Robotics, KUKA/Swisslog, KION/Dematic, Honeywell, and AutoStore. To reinforce their position, logistics robotics companies are prioritizing AI-powered automation, real-time data analytics, and modular system designs tailored to various logistics use cases. Strategic mergers and partnerships are enabling technology sharing and geographic expansion, while R&D investments are yielding scalable platforms for multi-application functionality. Leading firms are also customizing robotic fleets to suit e-commerce, third-party logistics, and retail warehouse environments, ensuring long-term client retention and improved operational ROI. Global players are further strengthening their presence through localized production, expanded service networks, and integrated digital platforms that enable seamless logistics orchestration and predictive maintenance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.6.1 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Autonomous mobile robot manufacturers

- 3.1.1.2 Automated storage and retrieval system providers

- 3.1.1.3 Robotics software & AI platform developers

- 3.1.1.4 Warehouse infrastructure & material handling equipment suppliers

- 3.1.1.5 Systems integrators & solution provider

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Developments in e-commerce sector for picking applications

- 3.2.1.2 Advancements in robotics technology

- 3.2.1.3 Increasing popularity of autonomous warehouses

- 3.2.1.4 Growing awareness towards sustainability practices in logistic handling

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of purchasing and implementing logistics robots

- 3.2.2.2 Lack of employee skills to operate and maintain advanced robotic systems

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and IoT in logistics robots

- 3.2.3.2 Adoption of collaborative robots

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Computer vision & object recognition

- 3.3.1.2 Predictive analytics & maintenance

- 3.3.1.3 Polyfunctional robot development

- 3.3.1.4 Human-robot collaboration advancement

- 3.3.2 Emerging technologies

- 3.3.2.1 5G connectivity & communication systems

- 3.3.2.2 Digital twin & simulation technologies

- 3.3.2.3 Blockchain & supply chain transparency

- 3.3.2.4 Sustainability & green technology integration

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 Federal safety standards framework

- 3.5.1.1 ANSI/RIA R15.06 requirements

- 3.5.1.2 ANSI R15.08 mobile robot standards

- 3.5.1.3 ISO 10218 global harmonization

- 3.5.2 OSHA compliance requirements

- 3.5.2.1 General duty clause application

- 3.5.2.2 Machinery & machine guarding standards

- 3.5.2.3 Electrical safety requirements

- 3.5.3 Industry-Specific Regulatory Requirements

- 3.5.3.1 FDA healthcare regulations

- 3.5.3.2 Food safety & HACCP compliance

- 3.5.3.3 Automotive industry standards

- 3.5.4 International standards harmonization

- 3.5.4.1 ISO technical committee 299

- 3.5.4.2 European standards integration

- 3.5.4.3 Regional adaptation requirements

- 3.5.1 Federal safety standards framework

- 3.6 Cost breakdown analysis

- 3.6.1 Hardware cost components

- 3.6.2 Software & integration expenses

- 3.6.3 Infrastructure modification requirements

- 3.6.4 Maintenance & service costs

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Environmental impact assessment & lifecycle analysis

- 3.9.2 Social impact & community relations

- 3.9.3 Governance & corporate responsibility

- 3.9.4 Sustainable technological development

- 3.10 Risk assessment framework

- 3.10.1 Interoperability & standardization gaps

- 3.10.2 Legacy system compatibility challenges

- 3.10.3 Regulatory & compliance risks

- 3.10.4 Financial risk mitigation strategies

- 3.11 Performance & quality standards

- 3.11.1 Risk assessment methodologies

- 3.11.2 Accuracy & precision standards

- 3.11.3 Industry-specific quality requirements

- 3.11.4 Safety testing requirements

- 3.12 Use Cases

- 3.12.1 Amazon robotics implementation model

- 3.12.2 Multi-SKU handling & sorting

- 3.12.3 Automotive manufacturing integration

- 3.12.4 Healthcare & pharmaceutical applications

- 3.12.5 Third-party logistics optimization

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Robotic platforms & chassis

- 5.2.2 Sensors & perception systems

- 5.2.3 Actuators & manipulation systems

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Robot operating systems

- 5.3.2 Fleet management software

- 5.3.3 Warehouse management integration

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Professional

- 5.4.2 Managed

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn & Units)

- 6.1 Key trends

- 6.2 Automated guided vehicles

- 6.3 Autonomous mobile robots

- 6.4 Robot arms

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn & Units)

- 7.1 Key trends

- 7.2 Palletizing & de-palletizing

- 7.3 Pick & place

- 7.4 Transportation

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By End use, 2021 - 2034 ($Bn & Units)

- 8.1 Key trends

- 8.2 E-commerce

- 8.3 Healthcare

- 8.4 Retail

- 8.5 Food & beverages

- 8.6 Automotive

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn & Units)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 ABB

- 10.1.2 Amazon Robotics

- 10.1.3 AutoStore

- 10.1.4 Daifuku

- 10.1.5 Honeywell

- 10.1.6 KION/Dematic

- 10.1.7 KUKA/Swisslog

- 10.1.8 Omron

- 10.1.9 Toyota/Bastian

- 10.1.10 Yaskawa Electric

- 10.2 Regional players

- 10.2.1 Bastian Solutions

- 10.2.2 Geek+

- 10.2.3 GreyOrange

- 10.2.4 Locus Robotics

- 10.2.5 Vecna Robotics

- 10.3 Emerging players

- 10.3.1 VisionNav Robotics

- 10.3.2 Berkshire Grey

- 10.3.3 Covariant

- 10.3.4 Exotec

- 10.3.5 River Systems