|

시장보고서

상품코드

1871153

자기 치유 조인트 컴파운드 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Self-Healing Joint Compounds Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

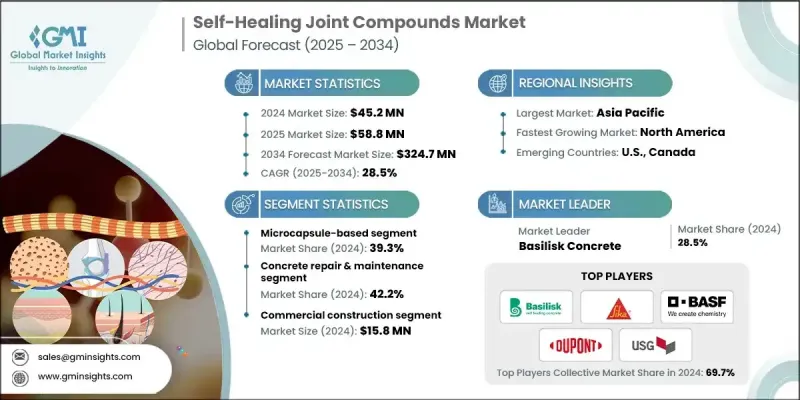

세계 자기 치유 조인트 컴파운드 시장은 2024년 4,520만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 28.5%로 확대되어 3억 2,470만 달러에 이를 것으로 예측됩니다.

내구성, 지속가능성 및 유지보수 비용 절감을 겸비한 스마트 건축자재에 대한 수요가 높아지는 가운데, 이 시장은 급속히 주목을 받고 있습니다. 자기 치유 조인트 컴파운드는 벽, 천장, 구조 접합부의 미세한 균열이나 틈새를 스스로 수복하는 능력으로 인해 주택 및 상업 건축 프로젝트 양쪽에서 채용이 확대되고 있습니다. 동적 폴리머, 임베디드 마이크로캡슐 또는 바이오 수리제를 사용하여 배합된 이러한 재료는 인프라 및 건축물의 내부 구조의 수명을 연장하는 동시에 장기적인 수리 비용을 절감합니다. 지속가능한 건축재료에 대한 세계적인 인식 증가와 폐기물 감소 및 유지관리 비용 절감에 관한 정부의 규제 강화가 함께 채택이 가속화되고 있습니다. 선진국에서는 특히 노후화된 인프라의 재생에 주력하고 있으며, 미래의 개수 사이클을 단축하는 재료에 대한 투자를 촉진하고 있습니다. 마찬가지로 아시아태평양 신흥국에서는 철도, 교통, 도시 인프라 프로젝트에 대한 지출이 증가하고 있으며 시장 확대를 추진하고 있습니다. 건설활동 증가와 성능효율에 대한 관심의 높아짐에 따라, 자기 치유 조인트 컴파운트는 현대 건설에서 표준이 될 것으로 기대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025년-2034 |

| 시작 금액 | 4,520만 달러 |

| 예측 금액 | 3억 2,470만 달러 |

| CAGR | 28.5% |

마이크로캡슐 기반 시스템 부문은 2024년 39.3%의 점유율을 차지했습니다. 이러한 시스템은 기존의 조인트 컴파운드 제형과의 호환성과 비용 효율적인 제조 공정으로 인기가 높습니다. 표준 건식 벽 응용 분야에 원활하게 녹는 능력을 통해 제조업체는 생산 라인에 큰 조정을 하지 않고 자기 치유 특성을 통합 할 수 있습니다. 한편, 고유 폴리머 시스템은 꾸준한 발전을 이루고 있으며, 이식제 없이 여러 개의 자기 치유 사이클을 제공합니다. 이 특성은 유연성과 내구성이 모두 요구되는 고가동 구조 접합부 및 내부 환경에서 특히 가치가 있습니다.

보호 코팅 분야는 2024년 24.1%의 점유율을 차지했습니다. 산업시설이나 해양구조물 등 가혹한 환경에서의 사용 증가는 건축물과 설비 표면의 내습성, 부식성, 내구성 향상에 있어서 유효성을 나타내고 있습니다.

2024년 미국의 자기 치유 조인트 컴파운드 시장은 1,580만 달러로 평가되었습니다. 북미는 인프라 근대화에 대한 강력한 투자와 내구성이 뛰어나 낮은 VOC(휘발성 유기 화합물)인 재료를 추진하는 정부 주도의 대처에 의해 업계를 선도하고 있습니다. 이 지역에서는 공급업체, 대학, 재료 개발 기업 간의 활발한 실증 프로그램, 연수 워크숍, 연구 개발 협력이 실시되고 있으며, 이러한 노력에 의해 건식 벽 마무리, 실란트, 코팅 용도에 있어서의 제품 채용이 촉진되고, 미국은 첨단 자기 치유 기술의 거점으로서의 지위를 확립하고 있습니다.

세계의 자기 치유 조인트 컴파운드 시장에서 주요한 역할을 하는 기업으로는 CertainTeed Gypsum, DuPont de Nemours Inc., Sika AG, United States Gypsum Company (USG), BASF SE, ITW Performance Polymers, Autonomic Materials Inc., Applied Nanotech Holdings Inc., National Gypsum Company, Basilisk Concrete 등을 들 수 있습니다. 주요 기업은 시장의 지위를 강화하기 위해 기술 혁신, 지속 가능한 배합, 전략적 제휴에 주력하고 있습니다. 많은 기업들이 수리 효율, 제품 수명 및 환경 적합성을 향상시키기 위해 첨단 고분자 화학 및 나노 기술에 대한 투자를 추진하고 있습니다. 화학기업과 건설자재 제조업체와의 제휴로, 자기 치유 솔루션의 상업화와 대규모 도입이 가속화되고 있습니다. 또한 기업은 주요 인프라 시장, 특히 북미와 아시아태평양에 생산 거점을 설치함으로써 지역적인 존재를 확대하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속 가능한 저 VOC 건축자재로의 이행

- 스마트하고 지속 가능한 건설의 성장

- 구조 건전성 모니터링을 위한 스마트 센서 통합

- 업계의 잠재적 위험 및 과제

- 규제의 복잡성과 컴플라이언스 비용

- 기존 재료와의 호환성에 관한 과제

- 시장 기회

- 그린빌딩 인증 확대

- 스마트 빌딩 기술과의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 기술 유형별

- 미래 시장 동향

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경적 측면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협력관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 기술 유형별, 2021-2034년

- 주요 동향

- 마이크로 캡슐 기반 시스템

- 세균 및 생물학적 시스템

- 폴리머 기반의 내재적 치유

- 혈관 네트워크 시스템

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 석고 보드 조인트 마무리

- 콘크리트 보수 및 유지보수

- 보호 코팅 시장 분석

- 구조용 실란트

제7장 시장 추계 및 예측 : 최종 이용 산업별, 2021-2034년

- 주요 동향

- 주택건설

- 상업건축

- 인프라 및 토목 공사

- 산업시설

- 해양 및 연안

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Applied Nanotech Holdings, Inc.

- Autonomic Materials, Inc.

- BASF SE

- Basilisk Concrete

- CertainTeed Gypsum

- DuPont de Nemours, Inc.

- ITW Performance Polymers

- National Gypsum Company

- Sika AG

- United States Gypsum Company(USG)

The Global Self-Healing Joint Compounds Market was valued at USD 45.2 million in 2024 and is estimated to grow at a CAGR of 28.5% to reach USD 324.7 million by 2034.

The market is gaining rapid traction as demand rises for smart construction materials that combine durability, sustainability, and reduced maintenance costs. Self-healing joint compounds are increasingly being adopted across both residential and commercial construction projects for their ability to automatically repair minor cracks and gaps in walls, ceilings, and structural joints. These compounds formulated using dynamic polymers, embedded microcapsules, or bio-based healing agents, help extend the lifespan of infrastructure and building interiors while reducing long-term repair expenses. Growing global awareness of sustainable building materials, alongside stricter government mandates on reducing waste and maintenance costs, is accelerating adoption. Developed economies are particularly focusing on revitalizing aging infrastructure, which is driving investments in materials that reduce future renovation cycles. Similarly, emerging economies in Asia Pacific are boosting spending on railways, transit, and urban infrastructure projects, fueling market expansion. With rising construction activity and heightened focus on performance efficiency, self-healing joint compounds are expected to become a standard in modern construction practices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $45.2 Million |

| Forecast Value | $324.7 Million |

| CAGR | 28.5% |

The microcapsule-based systems segment held a 39.3% share in 2024. These systems are popular due to their compatibility with conventional joint compound formulations and cost-effective manufacturing processes. Their ability to blend seamlessly into standard drywall applications allows manufacturers to integrate self-healing properties without major adjustments to production lines. Meanwhile, intrinsic polymer systems are witnessing steady development, offering multiple self-healing cycles without embedded agents. This feature is especially valuable in high-movement structural joints and interior settings that demand both flexibility and longevity.

The protective coatings segment accounted for 24.1% share in 2024. Their rising use in demanding environments such as industrial and offshore installations highlights their effectiveness in providing moisture resistance, corrosion protection, and extended durability of architectural and equipment surfaces.

U.S. Self-Healing Joint Compounds Market was valued at USD 15.8 million in 2024. North America continues to lead the industry due to strong investment in infrastructure modernization and government-backed initiatives promoting durable, low-VOC materials. The region benefits from active demonstration programs, training workshops, and R&D collaborations between suppliers, universities, and material innovators. These efforts are enhancing product adoption across drywall finishing, sealants, and coatings applications, positioning the U.S. as a hub for advanced self-healing technologies.

Key players operating in the Global Self-Healing Joint Compounds Market include CertainTeed Gypsum, DuPont de Nemours Inc., Sika AG, United States Gypsum Company (USG), BASF SE, ITW Performance Polymers, Autonomic Materials Inc., Applied Nanotech Holdings Inc., National Gypsum Company, and Basilisk Concrete. Leading companies are focusing on technological innovation, sustainable formulations, and strategic collaborations to reinforce their market position. Many are investing in advanced polymer chemistry and nanotechnology to improve healing efficiency, product longevity, and environmental compliance. Partnerships between chemical firms and construction material manufacturers are accelerating commercialization and large-scale deployment of self-healing solutions. Companies are also expanding their regional presence by establishing production facilities close to key infrastructure markets, particularly in North America and Asia Pacific.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology Type

- 2.2.3 Application

- 2.2.4 End use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward sustainable, low-VOC building materials

- 3.2.1.2 Growth of smart & sustainable construction

- 3.2.1.3 Integration of smart sensors for structural health monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory complexity & compliance costs

- 3.2.2.2 Compatibility issues with existing materials

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in green building certifications

- 3.2.3.2 Integration with Smart Building Technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By technology type

- 3.8 Future market trends

- 3.9 Patent Landscape

- 3.10 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.10.1 Major importing countries

- 3.10.2 Major exporting countries

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Microcapsule-based Systems

- 5.3 Bacterial/Biological Systems

- 5.4 Polymer-based Intrinsic Healing

- 5.5 Vascular Network Systems

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Drywall Joint Finishing

- 6.3 Concrete Repair & Maintenance

- 6.4 Protective Coatings Market Analysis

- 6.5 Structural Sealants

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential Construction

- 7.3 Commercial Construction

- 7.4 Infrastructure/Civil Engineering

- 7.5 Industrial Facilities

- 7.6 Marine/Offshore

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Applied Nanotech Holdings, Inc.

- 9.2 Autonomic Materials, Inc.

- 9.3 BASF SE

- 9.4 Basilisk Concrete

- 9.5 CertainTeed Gypsum

- 9.6 DuPont de Nemours, Inc.

- 9.7 ITW Performance Polymers

- 9.8 National Gypsum Company

- 9.9 Sika AG

- 9.10 United States Gypsum Company (USG)