|

시장보고서

상품코드

1871192

수소 연료전지 자동차 냉각 시스템 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Hydrogen Fuel Cell Vehicle Cooling System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

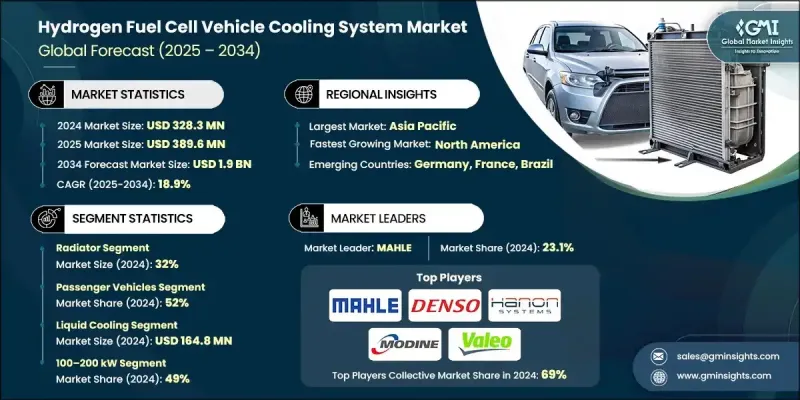

세계의 수소 연료전지 자동차 냉각 시스템 시장은 2024년 3억 2,830만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 18.9%를 나타내 19억 달러에 이를 것으로 예상됩니다.

이러한 대폭적인 확대는 수소 연료전지 차량의 보급 확대, 지속 가능한 운송 수단에 대한 관심 증가, 성능과 내구성을 향상시키는 고효율 열 관리 시스템에 대한 수요 증가에 의해 추진되고 있습니다. 냉각 기술, 재료 및 시스템 설계의 지속적인 발전이 시장 개척을 지원하고 있으며 제조업체는 견고하고 확장 가능하며 에너지 효율적인 솔루션을 생산할 수 있습니다. 이러한 혁신은 수소자동차의 열 밸런스 유지, 종합적인 신뢰성 향상, 세계적인 안전·배출 가스 규제에의 적합 확보에 필수적입니다. 상용차 fleet의 전동화와 수소 이동성 인프라의 급속한 진화에 따라 효과적인 냉각 시스템에 대한 수요는 계속 증가하고 있습니다. 자동차 제조업체 및 부품 공급업체는 향후 운송 생태계에서 지속가능성, 효율성 및 성능을 추구하는 차세대 연료전지 차량을 개발하기 위해 AI 구동형 및 경량 열 관리 기술을 강조합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 3억 2,830만 달러 |

| 예측 금액 | 19억 달러 |

| CAGR | 18.9% |

수소 연료전지 자동차 냉각 시스템은 라디에이터, 열교환기, 냉각수 펌프, 전자 제어 장치, 열전도 재료 등을 포함하며 전력 전자, 배터리 및 연료전지의 이상적인 작동 온도를 유지하는 데 매우 중요한 역할을 합니다. 효율적인 열 관리는 안정적인 전력 공급과 부품의 긴 수명화를 보장할 뿐만 아니라 과열 및 기계적 열화 위험의 최소화에도 기여합니다. 시장의 급속한 성장은 기술 발전, 환경 규제 강화 및 제로 방출 운송 솔루션으로의 전환 가속과 밀접한 관련이 있습니다.

라디에이터 부문은 2024년에 32%의 점유율을 차지했으며 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 20.1%를 나타낼 것으로 예측됩니다. 이는 주요 차량 시스템의 온도 안정화, 원활한 에너지 흐름 확보, 최적의 성능 유지에 매우 중요한 역할을 하기 때문입니다. 라디에이터는 상용 및 승용 수소 연료전지 차량 모두에서 주요 OEM 제조업체 및 Tier 1 공급업체에 널리 채택되었습니다. 하이브리드 기술과 액체 냉각 기술을 채용한 첨단 라디에이터 설계는 뛰어난 방열성, 높은 동작 신뢰성, 차량 수명 향상을 실현하여 수소 이동성 상황에서 최적의 선택이 되었습니다.

승용차 부문은 2024년에 52%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 18.4%를 나타낼 전망입니다. 이 부문의 이점은 효율적이고 낮은 배출 가스 차량에 대한 세계 관심 증가와 수소 동력 승용차에 대한 첨단 냉각 시스템의 통합으로 인한 것입니다. 이 시스템은 배터리와 연료전지의 성능을 최적화하여 신뢰성 향상, 안전 강화, 차량 내구성 개선을 실현합니다. 환경에 배려한 차량에 대한 소비자 수요와 정부 주도의 지속가능성 정책이 함께 이 카테고리의 견조한 성장을 지지하고 있습니다.

중국의 수소 연료전지 자동차 냉각 시스템 시장은 41%의 점유율을 차지하며 9,970만 달러의 규모가 되었습니다. 이 나라의 주도적 입장은 수소 연료 차량 플릿의 급속한 보급과 깨끗한 이동성 솔루션을 촉진하는 강력한 정책 인센티브에 의해 지원됩니다. 이 지역의 광대한 자동차 제조거점과 차세대 차량 기술에 대한 투자 확대가 그 우위성을 더욱 강화하고 있습니다. 아시아태평양은 대규모 생산 능력, 인프라 확충, 상용차 및 승용차 양쪽의 플릿에 있어서 선진 냉각 시스템의 광범위한 도입에 지지되어 수소 자동차 개발의 주요 거점으로 계속되고 있습니다.

세계의 수소 연료전지 자동차 냉각 시스템 시장에서 주요 기업으로는 Bosch, BMW, Denso, Hanon Systems, Hyundai Motor, Continental, MAHLE, Modine, Toyota Motor, Valeo 등이 참가하고 있습니다. 시장에서의 지위를 강화하기 위해, 주요 제조업체는 혁신, 협업, 생산 능력 확대에 초점을 맞춘 전략적 노력을 조합하여 추진하고 있습니다. 각 회사는 수소자동차용 열관리 재료의 개량, 냉각효율의 향상, 시스템통합의 개선을 목적으로 연구개발에 많은 투자를 하고 있습니다. 제품 개발의 가속과 시스템 호환성의 최적화를 도모하기 위해, 자동차 제조업체나 기술 개발 기업과의 제휴가 구축되고 있습니다. 많은 기업들은 효율 기준과 지속가능성 목표를 달성하기 위해 경량 재료와 디지털 열 제어 솔루션을 강조합니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 수소 연료전지 자동차의 보급 확대

- 냉각 시스템의 기술적 진보

- 엄격한 규제 요건

- 플릿 전동화와 상용 차량 도입

- 업계의 잠재적 위험 및 과제

- 고비용 시스템

- 제한된 인프라와 공급망

- 시장 기회

- 커넥티드카 기술과의 통합

- 상용 및 대형 차량 용도로의 전개

- 연료전지차의 보급 확대

- 열 관리 기술의 기술적 진보

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 국제 규격의 틀

- 지역 규제 프레임워크

- 안전성과 성능 기준

- 인증 및 시험 프로토콜

- 장래의 규제의 진화

- 정부 보조금 및 인센티브가 기술 도입에 미치는 영향

- 지역별 수소연료 보조금 및 세액공제

- 인프라 투자 및 도입 촉진책

- 냉각 시스템 사양 및 연구 개발에 미치는 영향

- 인센티브에 의한 생산량의 가속

- 정책의 영향을 받는 공급자 선정 기준

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현행 기술의 평가

- 기술 성숙도 평가

- 혁신 및 생태계 분석

- 특허정세와 지적재산

- 미래의 혁신 로드맵

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 주요 냉각 기술을 보호하는 중요한 특허

- 특허 만료 로드맵과 연구개발 기회

- 빈 영역의 특정과 혁신의 갭

- 라이선싱 계약 및 크로스 라이선스 계약

- 신흥특허권자와 파괴적 기술

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 위험 평가 프레임워크

- 최상의 시나리오

- 수소 연료전지 시스템의 열 거동과 발열 프로파일

- 다른 운전 조건에서의 발열량

- 열 사이클 효과

- 시스템의 응답 시간과 효율 지표

- 배터리 열 관리 시스템과의 통합

- 듀얼 열부하 관리

- 하이브리드 연료전지·배터리 아키텍처

- 시스템간 열교환 전략

- 제어 통합 및 최적화

- 콜드 스타트 및 극한 환경 하에서의 성능

- 내구성 시험 기준과 검증 프로토콜

- 제조 공정의 혁신과 생산의 확장성

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대계획과 자금조달

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 라디에이터

- 냉각수 펌프

- 열교환기

- 냉각 팬

- 밸브 및 센서

- 기타

제6장 시장 추계·예측 : 냉각 기술별(2021-2034년)

- 주요 동향

- 액체 냉각

- 하이브리드 냉각

- 공냉식

제7장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- SUV

- 세단

- 해치백

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 특수 차량

제8장 시장 추계·예측 : 출력별(2021-2034년)

- 주요 동향

- 100-200kW

- 100kW 미만

- 200kW 이상

제9장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 개인 교통수단

- 대중교통

- 산업용

- 군사 및 방위

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- 세계 기업

- BMW

- Daimler

- 포드모터

- General Motors

- Honda Motor

- 현대자동

- Mercedes-Benz

- Stellantis

- Toyota Motor

- Volvo

- 지역 기업

- Aisin

- Bosch

- Continental

- Cummins

- Denso

- Hanon Systems

- MAHLE

- Modine

- Plug Power

- Valeo

- 신흥기업

- Eberspacher

- Hanon Systems

- Sanden

- Scania

- Webasto

The Global Hydrogen Fuel Cell Vehicle Cooling System Market was valued at USD 328.3 million in 2024 and is estimated to grow at a CAGR of 18.9% to reach USD 1.9 Billion by 2034.

The significant expansion is fueled by the growing adoption of hydrogen fuel cell vehicles, the rising focus on sustainable transportation, and the increasing need for high-efficiency thermal management systems that boost performance and durability. The market's development is being supported by continuous advancements in cooling technologies, materials, and system designs, enabling manufacturers to produce robust, scalable, and energy-efficient solutions. These innovations are essential for maintaining the thermal balance of hydrogen-powered vehicles, improving overall reliability, and ensuring compliance with global safety and emission regulations. The demand for effective cooling systems continues to rise alongside the electrification of commercial fleets and the rapid evolution of hydrogen mobility infrastructure. Automakers and component suppliers are emphasizing AI-driven and lightweight thermal management technologies to deliver next-generation fuel cell vehicles designed for sustainability, efficiency, and performance in future transportation ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $328.3 Million |

| Forecast Value | $1.9 Billion |

| CAGR | 18.9% |

Hydrogen fuel cell vehicle cooling systems, which include radiators, heat exchangers, coolant pumps, electronic control units, and thermal interface materials, play a crucial role in maintaining the ideal operating temperature of power electronics, batteries, and fuel cells. Efficient thermal management not only ensures steady power delivery and component longevity but also minimizes the risk of overheating and mechanical degradation. The market's rapid growth is closely linked to technological advancements, stricter environmental mandates, and the accelerating transition toward zero-emission transportation solutions.

The radiator segment accounted for a 32% share in 2024 and is projected to grow at a CAGR of 20.1% between 2025 and 2034. This segment dominates due to its vital role in stabilizing the temperature of key vehicle systems, ensuring smooth energy flow, and optimal performance. Radiators are widely adopted by leading OEMs and Tier-1 suppliers for both commercial and passenger hydrogen fuel cell vehicles. Advanced radiator designs featuring hybrid and liquid-cooled technologies offer superior heat dissipation, increased operational reliability, and improved vehicle longevity, making them the preferred choice in the hydrogen mobility landscape.

The passenger vehicle segment held a 52% share in 2024 and is expected to grow at a CAGR of 18.4% through 2034. This segment's dominance is attributed to rising global interest in efficient, low-emission vehicles and the integration of advanced cooling architectures into hydrogen-powered passenger cars. These systems optimize the performance of batteries and fuel cells, providing greater reliability, enhanced safety, and improved vehicle durability. The combination of consumer demand for environmentally responsible vehicles and government-driven sustainability policies continues to support strong growth in this category.

China Hydrogen Fuel Cell Vehicle Cooling System Market held a 41% share, generating USD 99.7 million. The country's leadership is driven by the rapid adoption of hydrogen-powered fleets and strong policy incentives that promote cleaner mobility solutions. The region's vast automotive manufacturing base and growing investments in next-generation vehicle technologies further strengthen its dominance. Asia Pacific remains a key hub for hydrogen vehicle development, supported by large-scale production capabilities, infrastructure expansion, and widespread deployment of advanced cooling systems across both commercial and passenger fleets.

Major companies operating in the Global Hydrogen Fuel Cell Vehicle Cooling System Market include Bosch, BMW, Denso, Hanon Systems, Hyundai Motor, Continental, MAHLE, Modine, Toyota Motor, and Valeo. To reinforce their market position, leading manufacturers are pursuing a combination of strategic initiatives focused on innovation, collaboration, and capacity expansion. Companies are investing heavily in research and development to advance thermal management materials, enhance cooling efficiency, and improve system integration for hydrogen-powered vehicles. Partnerships with automotive OEMs and technology developers are being established to accelerate product development and optimize system compatibility. Many players emphasize lightweight materials and digital thermal control solutions to meet efficiency standards and sustainability targets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Cooling technology

- 2.2.4 Vehicle

- 2.2.5 Power output

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of hydrogen fuel cell vehicles

- 3.2.1.2 Technological advancements in cooling systems

- 3.2.1.3 Stringent regulatory mandates

- 3.2.1.4 Fleet electrification and commercial vehicle deployment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system costs

- 3.2.2.2 Limited infrastructure and supply chain

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with connected vehicle technologies

- 3.2.3.2 Expansion into commercial and heavy-duty applications

- 3.2.3.3 Growing adoption of fuel cell vehicles

- 3.2.3.4 Technological advancements in thermal management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 International standards framework

- 3.4.2 Regional regulatory frameworks

- 3.4.3 Safety & performance standards

- 3.4.4 Certification & testing protocols

- 3.4.5 Future regulatory evolution

- 3.4.6 Government subsidies and incentive impact on technology adoption

- 3.4.6.1 Hydrogen fuel subsidies and tax credits by region

- 3.4.6.2 Infrastructure investment and deployment incentives

- 3.4.6.3 Impact on cooling system specifications and R&D

- 3.4.6.4 Production volume acceleration from incentives

- 3.4.6.5 Supplier selection criteria influenced by policy

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technology assessment

- 3.7.2 Technology readiness assessment

- 3.7.3 Innovation ecosystem analysis

- 3.7.4 Patent landscape & intellectual property

- 3.7.5 Future innovation roadmap

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.11.1 Critical patents protecting key cooling technologies

- 3.11.2 Patent expiration roadmap and R&D opportunities

- 3.11.3 White space identification and innovation gaps

- 3.11.4 Licensing and cross-licensing arrangements

- 3.11.5 Emerging patent holders and disruptive technologies

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Risk assessment framework

- 3.14 Best case scenarios

- 3.15 Hydrogen fuel cell system thermal behavior and heat generation profiles

- 3.15.1 Heat generation at different operating conditions

- 3.15.2 Thermal cycling effects

- 3.15.3 System response times and efficiency metrics

- 3.16 Integration with battery thermal management systems

- 3.16.1 Dual thermal load management

- 3.16.2 Hybrid fuel cell-battery architectures

- 3.16.3 Cross-system heat exchange strategies

- 3.16.4 Control integration and optimization

- 3.17 Cold start and extreme climate performance

- 3.18 Durability testing standards and validation protocols

- 3.19 Manufacturing process innovations and production scalability

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Radiator

- 5.3 Coolant pump

- 5.4 Heat exchanger

- 5.5 Cooling fans

- 5.6 Valves and sensors

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Cooling Technology, 2021 - 2034 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Liquid cooling

- 6.3 Hybrid cooling

- 6.4 Air cooling

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Mn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 SUV

- 7.2.2 Sedan

- 7.2.3 Hatchback

- 7.3 Commercial Vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

- 7.4 Specialized Vehicles

Chapter 8 Market Estimates & Forecast, By Power Output, 2021 - 2034 ($ Mn, Units)

- 8.1 Key trends

- 8.2 100-200 kW

- 8.3 Below 100 kW

- 8.4 Above 200 kW

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Mn, Units)

- 9.1 Key trends

- 9.2 Private transportation

- 9.3 Public transportation

- 9.4 Industrial

- 9.5 Military & defense

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Mn, Units)

- 10.1 Key trends

- 10.2 Key trends

- 10.3 North America

- 10.3.1 US

- 10.3.2 Canada

- 10.4 Europe

- 10.4.1 UK

- 10.4.2 Germany

- 10.4.3 France

- 10.4.4 Italy

- 10.4.5 Spain

- 10.4.6 Belgium

- 10.4.7 Netherlands

- 10.4.8 Sweden

- 10.5 Asia Pacific

- 10.5.1 China

- 10.5.2 India

- 10.5.3 Japan

- 10.5.4 Australia

- 10.5.5 Singapore

- 10.5.6 South Korea

- 10.5.7 Vietnam

- 10.5.8 Indonesia

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Mexico

- 10.6.3 Argentina

- 10.7 MEA

- 10.7.1 UAE

- 10.7.2 South Africa

- 10.7.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 BMW

- 11.1.2 Daimler

- 11.1.3 Ford Motor

- 11.1.4 General Motors

- 11.1.5 Honda Motor

- 11.1.6 Hyundai Motor

- 11.1.7 Mercedes-Benz

- 11.1.8 Stellantis

- 11.1.9 Toyota Motor

- 11.1.10 Volvo

- 11.2 Regional players

- 11.2.1 Aisin

- 11.2.2 Bosch

- 11.2.3 Continental

- 11.2.4 Cummins

- 11.2.5 Denso

- 11.2.6 Hanon Systems

- 11.2.7 MAHLE

- 11.2.8 Modine

- 11.2.9 Plug Power

- 11.2.10 Valeo

- 11.3 Emerging players

- 11.3.1 Eberspacher

- 11.3.2 Hanon Systems

- 11.3.3 Sanden

- 11.3.4 Scania

- 11.3.5 Webasto