|

시장보고서

상품코드

1871209

식물성 계란 단백질 분리물 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Plant-Based Egg Protein Isolates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

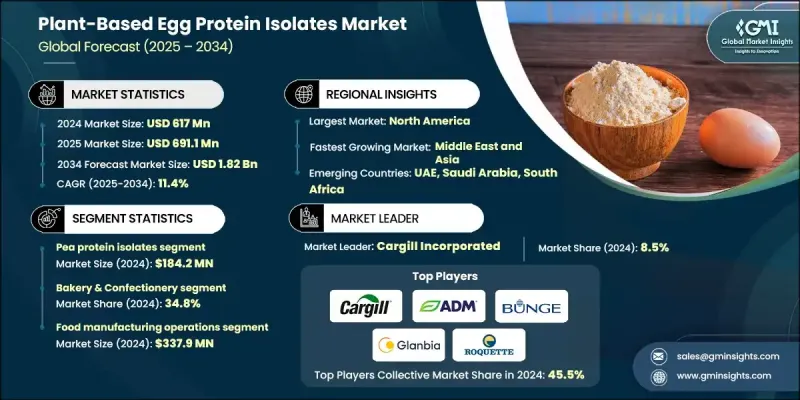

세계의 식물성 계란 단백질 분리물 시장은 2024년 6억 1,700만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 11.4%를 나타내 18억 2,000만 달러에 이를 것으로 예상됩니다.

소비자가 비건, 채식, 플렉시탈리안 등 식생활로 이행하는 움직임이 가속화되는 가운데 시장은 급속히 확대되고 있습니다. 병아리 콩, 녹두, 조류 등의 원료로 제조되는 식물성 계란 단백질은 전통적인 계란을 대체하는 윤리적이고 환경 친화적이며 건강 지향적인 대안으로 널리 채택되었습니다. 이 제품은 콜레스테롤을 포함하지 않으며 지속 가능한 선택을 제공하고 건강과 환경 책임을 중시하는 현대 소비자 가치에 부합합니다. 동물복지에 대한 의식의 고조와 식품생산의 환경부하 저감에 대한 세계적 대처가 함께 수요를 뒷받침하고 있습니다. 제조업체 각사는 기존의 계란의 맛, 식감, 영양가를 재현하기 위해 단백질 공학이나 AI 구동 최적화를 포함한 첨단 가공 기술에 많은 투자를 하고 있습니다. 게다가 하이브리드 단백질 블렌드와 마이크로캡슐화 등의 기술 혁신으로 제품의 안정성, 보존 기간, 풍미 유지성이 향상되어 세계 소비자와 식품 제조업체 모두에게 식물성 계란 단백질의 매력이 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 6억 1,700만 달러 |

| 예측 금액 | 18억 2,000만 달러 |

| CAGR | 11.4% |

완두콩 단백질 분리 부문은 2024년에 1억 8,420만 달러의 수익을 창출했습니다. 식물 유래의 계란 단백질 중에서 완두콩과 대두의 분리물이 시장을 선도하고 있습니다. 그 이유는 비용 효율성, 가공 안정성 및 다양한 식품 시스템과의 호환성에 있습니다. 이 단백질은 건조 및 액체 블렌드에 잘 녹아 베이커리 믹스, 소스, 레디밀(조리된 식품)에 부드러운 블렌딩을 가능하게합니다. 완두콩 단백질은 알레르겐 프리로 맛에 버릇이 없는 것으로부터 선호되고, 대두 단백질은 강력한 유화·결합 능력이 높게 평가되어 종래의 계란과 같은 기능성을 제공합니다.

베이커리·과자류 분야는 2024년에 2억 1,450만 달러 시장 규모를 기록해, 34.8%의 점유율을 차지했습니다. 식물 유래의 계란 단백질은 고품질의 채식주의자 및 알레르겐이없는 구운 과자 제조에 필수적인 기포 형성, 구조 형성 및 수분 보유와 같은 중요한 베이킹 특성을 제공하기 때문에이 분야 수요가 가속화되고 있습니다. 마찬가지로 마요네즈와 유화제품업체도 유화·안정화 특성으로부터 식물성 단백질을 적극적으로 채용하고 있어 원하는 식감과 보존 안정성을 유지하면서 확대하는 클린 라벨의 트렌드에 대응하는 브랜드를 지원하고 있습니다.

미국의 식물성 계란 단백질 분리물 시장은 2024년 2억 2,190만 달러로 평가되었습니다. 북미에서는 소비자가 지속가능성, 알레르겐 프리 영양, 식물 중심의 식생활을 중시하는 경향으로부터 세계적인 보급을 견인하고 있습니다. 미국에서는 소매업과 외식 산업 모두의 혁신이 수요를 견인하고 있으며 레스토랑과 패스트 푸드 체인이 식물성 계란을 메뉴에 도입하고 있습니다. 건강 지향의 대체 식품에 대한 경향과 단백질 강화 음료·구운 과자의 존재감의 높아짐이, 이 지역 전체의 한층 더 성장을 가속하고 있습니다.

세계의 식물성 계란 단백질 분리물 시장에서 주요 기업으로서 Roquette Freres, Axiom Foods Inc., Beneo GmbH, Aminola BV, Motif FoodWorks, Glanbia PLC, PURIS Holdings LLC, Archer Daniels Midland Company (ADM), Cargill Incorporated, AGT Food and Ingredients Inc., Bunge Limited, Tate & Lyle, Equinom Ltd., Cosucra Groupe Warcoing SA, Yantai Shuangta Food Co. Ltd., FUJI Plant Protein Labs, VW Ingredients, Verdient Foods, Laybio Natural Ingredients, ETprotein Co. Ltd., Organicway Inc., Burcon NutraScience Corporation, Vestkorn Milling AS 등이 있습니다. 주요 기업은 지속적인 혁신, 파트너십 및 지속가능성에 중점을 둔 전략을 통해 그 존재를 강화하고 있습니다. 주요 제조업체는 식물 유래 계란 단백질의 관능 특성과 영양 프로파일을 향상시키고 기존 계란과의 차이를 줄이기 위해 첨단 연구 개발에 투자하고 있습니다. 식품 제조업체나 기술 기업과의 협업에 의해 베이커리 제품, 음료, 편의점 푸드 등, 제품 용도의 확대가 진행되고 있습니다. 또한 기업은 지속 가능한 조달 관행의 확대와 원료 기반의 다양화를 추진하여 비용 효율성과 공급 안정성 확보에 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 식물 유래 대체품에 대한 소비자 수요 증가

- 식품기술의 진보

- 건강과 웰빙에 대한 소비자의 관심 증가

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용이 시장 확대를 제한

- 주요 식물 원료공급 불안정이 제조에 지장을 초래

- 시장 기회

- 지속가능한 단백질원에 대한 수요확대

- 제품 개량을 가능하게 하는 기술적 진보

- 플렉시탈리안식에의 높은 소비자 지향성

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 식물원료별

- 향후 시장 동향

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에의 배려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계·예측 : 식물 원료별(2021-2034년)

- 주요 동향

- 완두 단백질 분리물

- 대두 단백질 분리물

- 녹두 단백질 분리물

- 병아리콩/콩류 단백질 분리물

- 혼합 식물성 단백질 분리물

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 제빵 및 제과

- 마요네즈 및 유화제품

- 음료 및 영양

- 식물성 육류 및 유제품 대체품

- 외식 및 산업

제7장 시장 추계·예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 식품 제조

- 외식 산업

- 소매 및 소비재

- 영양보조식품

제8장 시장 추계·예측 : 제조 기술별(2021-2034년)

- 주요 동향

- 기존 추출 분리물

- 효소 변형 분리물

- 발효 유래 분리물

- 천연/냉간 가공 분리물

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- AGT Food and Ingredients Inc.

- Aminola BV

- Archer Daniels Midland Company(ADM)

- Axiom Foods Inc.

- Beneo GmbH

- Bunge Limited

- Burcon NutraScience Corporation

- Cargill, Incorporated

- Cosucra Groupe Warcoing SA

- Eat Just, Inc.

- Equinom Ltd.

- ETprotein Co., Ltd.

- FUJI Plant Protein Labs

- Glanbia PLC

- Laybio Natural Ingredients

- Motif FoodWorks

- Organicway Inc.

- PURIS Holdings LLC

- Roquette Freres

- Tate &Lyle

- Verdient Foods

- Vestkorn Milling AS

- VW Ingredients

- Yantai Shuangta Food Co., Ltd

The Global Plant-Based Egg Protein Isolates Market was valued at USD 617 million in 2024 and is estimated to grow at a CAGR of 11.4% to reach USD 1.82 Billion by 2034.

The market is expanding rapidly as consumers increasingly shift toward vegan, vegetarian, and flexitarian diets. Plant-based egg proteins, produced from ingredients such as chickpeas, mung beans, and algae, are widely adopted as ethical, eco-friendly, and health-conscious alternatives to conventional eggs. These products provide a cholesterol-free and sustainable option that aligns with modern consumer values focused on wellness and environmental responsibility. Rising awareness of animal welfare, coupled with the global emphasis on reducing the environmental footprint of food production, is fueling demand. Manufacturers are investing heavily in advanced processing technologies, including protein engineering and AI-driven optimization, to replicate the taste, texture, and nutritional quality of traditional eggs. Additionally, innovations like hybrid protein blends and microencapsulation are helping improve product stability, shelf life, and flavor retention, making plant-based egg proteins increasingly appealing to both consumers and food manufacturers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $617 Million |

| Forecast Value | $1.82 Billion |

| CAGR | 11.4% |

The pea protein isolates segment generated USD 184.2 million in 2024. Among plant-based egg proteins, pea and soy isolates lead the market due to their cost-effectiveness, processing stability, and compatibility with diverse food systems. These proteins blend well into both dry and liquid formulations, allowing smooth incorporation into bakery mixes, sauces, and ready-to-eat meals. Pea protein remains preferred for its allergen-free nature and neutral taste, while soy protein is valued for its strong emulsifying and binding capabilities, offering functionality similar to that of conventional eggs.

The bakery and confectionery segment generated USD 214.5 million in 2024 and held a 34.8% share. Demand from this segment is accelerating as plant-based egg proteins provide essential baking characteristics such as aeration, structure, and moisture retention, essential for producing high-quality vegan and allergen-free baked goods. Similarly, mayonnaise and emulsion product manufacturers are increasingly incorporating plant-based proteins for their emulsifying and stabilizing properties, helping brands meet the growing clean-label trend while maintaining desirable texture and shelf stability.

U.S. Plant-Based Egg Protein Isolates Market was valued at USD 221.9 million in 2024. North America continues to lead global adoption as consumers prioritize sustainability, allergen-free nutrition, and plant-forward diets. In the U.S., demand is being driven by both retail and foodservice innovation, with restaurants and quick-service chains integrating plant-based eggs into menus. The trend toward health-driven food alternatives and the growing presence of protein-enriched beverages and baked goods are propelling further growth across the region.

Key players active in the Global Plant-Based Egg Protein Isolates Market include Roquette Freres, Axiom Foods Inc., Beneo GmbH, Aminola BV, Motif FoodWorks, Glanbia PLC, PURIS Holdings LLC, Archer Daniels Midland Company (ADM), Cargill Incorporated, AGT Food and Ingredients Inc., Bunge Limited, Tate & Lyle, Equinom Ltd., Cosucra Groupe Warcoing SA, Yantai Shuangta Food Co. Ltd., FUJI Plant Protein Labs, VW Ingredients, Verdient Foods, Laybio Natural Ingredients, ETprotein Co. Ltd., Organicway Inc., Burcon NutraScience Corporation, and Vestkorn Milling AS. Leading companies are strengthening their presence through continuous innovation, partnerships, and sustainability-focused strategies. Major manufacturers are investing in advanced R&D to enhance the sensory qualities and nutritional profiles of plant-based egg proteins, ensuring closer parity with conventional eggs. Collaborations with food producers and technology firms are helping expand product applications across bakery, beverages, and convenience foods. Firms are also scaling up sustainable sourcing practices and diversifying raw material bases to ensure cost efficiency and supply stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Plant Source

- 2.2.2 Application

- 2.2.3 End use industry

- 2.2.4 Processing technology

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for plant-based alternatives

- 3.2.1.2 Advancements in food technology

- 3.2.1.3 Increasing consumer focus on health and wellness

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1 High production costs limit market expansion

- 3.3.2 Inconsistent supply of key plant ingredients disrupts manufacturing

- 3.4 Market opportunities

- 3.4.1 Growing demand for sustainable protein sources

- 3.4.2 Technological advancements enabling product improvement

- 3.4.3 Rising consumer shift towards flexitarian diets

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By plant source

- 3.11 Future market trends

- 3.12 Patent landscape

- 3.13 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.13.1 Major importing countries

- 3.13.2 Major exporting countries

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.15 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Plant Source, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pea protein isolates

- 5.3 Soy protein isolates

- 5.4 Mung bean protein isolates

- 5.5 Chickpea/legume protein isolates

- 5.6 Blended plant protein isolates

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Bakery & confectionery

- 6.2 Mayonnaise & emulsion products

- 6.3 Beverage & nutrition applications

- 6.4 Plant-based meat & dairy alternatives

- 6.5 Foodservice & industrial applications

Chapter 7 Market Estimates and Forecast, By End use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food manufacturing

- 7.3 Foodservice operations

- 7.4 Retail & consumer products

- 7.5 Nutritional supplements

Chapter 8 Market Estimates and Forecast, By Processing Technology, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Conventional extraction isolates

- 8.3 Enzymatically modified isolates

- 8.4 Fermentation-derived isolates

- 8.5 Native/cold-processed isolates

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGT Food and Ingredients Inc.

- 10.2 Aminola BV

- 10.3 Archer Daniels Midland Company (ADM)

- 10.4 Axiom Foods Inc.

- 10.5 Beneo GmbH

- 10.6 Bunge Limited

- 10.7 Burcon NutraScience Corporation

- 10.8 Cargill, Incorporated

- 10.9 Cosucra Groupe Warcoing SA

- 10.10 Eat Just, Inc.

- 10.11 Equinom Ltd.

- 10.12 ETprotein Co., Ltd.

- 10.13 FUJI Plant Protein Labs

- 10.14 Glanbia PLC

- 10.15 Laybio Natural Ingredients

- 10.16 Motif FoodWorks

- 10.17 Organicway Inc.

- 10.18 PURIS Holdings LLC

- 10.19 Roquette Freres

- 10.20 Tate & Lyle

- 10.21 Verdient Foods

- 10.22 Vestkorn Milling AS

- 10.23 VW Ingredients

- 10.24 Yantai Shuangta Food Co., Ltd