|

시장보고서

상품코드

1871225

그린 합성용 광화학 시약 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Photochemistry Reagents for Green Synthesis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

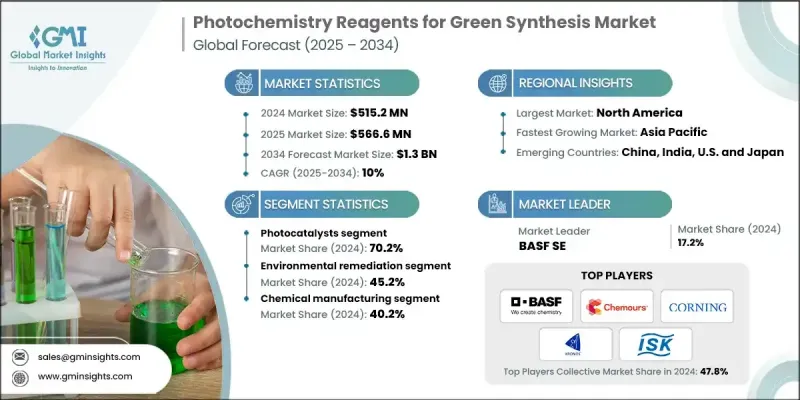

세계의 그린 합성용 광화학 시약 시장은 2024년 5억 1,520만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 10%로 성장하여 13억 달러에 이를 것으로 예측됩니다.

각 산업에 있어서의 지속가능성과 환경에 배려한 제조 수법에 대한 관심의 고조가, 그린 합성용 광화학 시약의 채택을 촉진하고 있습니다. 해로운 용매와 기존의 반응 방법에서보다 깨끗하고 에너지 효율적인 대안으로 전환하는 동안 이러한 시약의 중요성이 커지고 있습니다. 온화한 반응 조건과 우수한 선택성으로 알려진 광 산화 환원 촉매의 사용 확대는이 시장을 견인하는 주요 요인 중 하나입니다. 광화학 시약은 산화·환원 반응 및 CC 결합 형성 반응을 통해 에너지 소비와 폐기물 발생을 최소화하면서 효율적인 화학 변환을 실현합니다. 화학제조에 있어서 환경부하 저감에의 공헌이 평가되어 의약품, 농약, 특수화학제품의 생산에 있어서 수요가 높아지고 있습니다. 본 기술의 장점은 높은 반응 정밀도, 독성 시약의 사용 감소, 저에너지 투입, 상온 상압 조건 하에서의 반응 수행 등을 포함합니다. 지속가능한 화학을 추진하는 세계적인 환경규제와 더불어, 지속적인 조사는 광화학 시약 수요가 가속될 것으로 예상되며, 이 분야는 보다 광범위한 그린케미스트리 상황에서 점점 더 중요한 역할을 하게 됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025년-2034년 |

| 시작 금액 | 5억 1,520만 달러 |

| 예측 금액 | 13억 달러 |

| CAGR | 10% |

광증감제 부문은 2024년에 21.8%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR은 9.7%를 보일 것으로 예측됩니다. 이 카테고리는 주로 의약품과 정밀 화학의 개발에서 부위 특이적인 광 유도 화학 반응을 촉진하는 고급 유기 분자로 구성되어 있습니다. 광감응제가 전자 이동 공정을 가능하게 하는 광 산화환원 촉매의 채택 확대에 의해 종래의 합성 방법으로는 달성할 수 없었던 혁신적인 반응 경로가 열리고 있습니다. 산업이 지속가능하고 고효율적인 생산을 점점 더 중시하는 동안, 이러한 시약에 대한 수요는 급속히 확대되고 있습니다.

2024년 기준에서 정밀화학 및 의약품 합성 분야는 29.8%의 점유율을 차지했고, 2034년까지 연평균 복합 성장률(CAGR) 9.7%로 성장할 것으로 예상됩니다. 이 분야는 의약품 산업이 보다 환경 친화적이고 안전한 제조 기술로 전환하고 있음을 보여줍니다. 광화학 방법은 기존 공정에 비해 우수한 선택성, 폐기물 감소, 환경적 이점을 통해 의약품 원료(API), 중간체, 특수 화합물의 제조에 널리 활용되고 있습니다.

북미의 그린 합성용 광화학 시약 시장은 2024년에 36.9%의 점유율을 획득했으며, 2034년까지 연평균 복합 성장률(CAGR) 10.1%를 보일 것으로 예측됩니다. 이 지역은 견고한 연구 인프라, 신흥 화학 기술의 조기 도입, 그린 케미컬에 대한 강력한 정부 지원의 혜택을 누리고 있습니다. 지속 가능한 제조 방법을 촉진하는 프로그램에 의해 산업계에서는 보다 깨끗하고 안전하고, 효율적인 생산 공정로서 광화학 합성법의 채택이 진행되고 있습니다. 학술계, 산업계, 규제 당국간의 제휴 강화가 계속되어, 이 진화하는 시장에서의 북미의 주도적 입장을 더욱 확고한 것으로 하고 있습니다.

그린 합성용 광화학 시약 시장에서 적극적으로 사업을 전개하고 있는 주요 기업으로는 크로노스 월드 와이드사, BASF SE, 베네타 머티리얼즈사, 트로녹스 홀딩스사, 코닝사, 헌츠만사, 타이카사, 로몬 빌리온스 그룹사, 이시하라 산업 주식회사, 케무어즈사 등을 들 수 있습니다. 그린 합성용 광화학 시약 시장의 주요 기업은 생산능력 확대, 제품혁신 추진, 파트너십 강화에 주력하여 세계 사업 기반을 확충하고 있습니다. 각 회사는 보다 효율적이고 지속 가능하고 비용 효율적인 광화학 시약 개발을 위해 연구 개발에 많은 투자를 하고 있습니다. 학술기관이나 산업연구기관과의 전략적 제휴에 의해 광 레독스 촉매 기술이나 그린 제조 기술에 있어서의 획기적인 진전이 실현되고 있습니다. 또한 기업은 원료 공급망을 확보하고 품질 안정화를 도모하기 위해 수직 통합 전략을 실시했습니다. 또한, 고성장 시장에서의 사업 확대와 청정 생산 공정의 도입으로, 주요 기업은 급속히 확대하는 그린 케미스트리 분야에서의 경쟁력을 유지하면서 세계 지속가능성 목표에의 적합을 추진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 카테고리별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에 대해서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추정 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- 광촉매

- 이산화티타늄(TiO2)

- 금속 산화물 반도체

- 산화아연(ZnO)

- 삼산화텅스텐(WO3)

- 산화철(Fe2O3)

- 탄소 기반 광촉매

- 광증감제

- 포르피린 및 클로린 유도체

- 전이금속 착물

- 유기 염료 및 발색단

- 광개시제 및 광산/광염기 발생제

- 아실포스핀 옥사이드계

- 오니움 염 광개시제

- 벤조페논 및 티옥산톤 유도체

제6장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 환경 복구

- 수처리·정화

- 도시 하수 처리

- 산업 배수 처리

- 지하수 정화

- 공기 정화·휘발성 유기 화합물(VOC) 분해

- 실내 공기질 관리

- 산업 배출물 관리

- 대기오염물질의 분해

- 토양 정화·오염물질 분해

- 수처리·정화

- 정밀화학 및 의약품 합성

- 의약품 원약(API) 제조

- 후기 단계의 기능화

- 입체 선택적 변환

- 특수화학제품의 제조

- 농약 중간체

- 향료 및 향미 화합물

- 염료 및 안료 합성

- 그린 산화·환원 공정

- 의약품 원약(API) 제조

- 폴리머·재료 화학

- UV 경화형 코팅·잉크

- 광중합과 3D 프린팅

- 표면 기능화 및 수정

- 기타

제7장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 화학제품 제조

- 기초화학제품 제조

- 특수화학제품 제조

- 의약품 제조

- 폐기물 처리·수복

- 제조 및 전자 제품

- 연구개발

- 기타

제8장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- BASF SE

- Chemours Company

- Corning Incorporated

- Huntsman Corporation

- Ishihara Sangyo Kaisha Ltd.

- Kronos Worldwide Inc.

- Lomon Billions Group Co. Ltd.

- Tayca Corporation

- Tronox Holdings PLC

- Venator Materials PLC

The Global Photochemistry Reagents for Green Synthesis Market was valued at USD 515.2 million in 2024 and is estimated to grow at a CAGR of 10% to reach USD 1.3 Billion by 2034.

The growing focus on sustainability and environmentally responsible manufacturing practices across industries is propelling the adoption of photochemical reagents in green synthesis. These reagents are gaining prominence as industries move away from harmful solvents and conventional reaction methods toward cleaner, energy-efficient alternatives. The increasing use of photoredox catalysts, known for their mild reaction conditions and exceptional selectivity, is one of the major factors driving this market forward. Through oxidation, reduction, and C-C bond-forming reactions, photochemistry reagents make it possible to achieve efficient chemical transformations while minimizing energy consumption and waste generation. Their role in reducing the environmental footprint of chemical manufacturing has made them increasingly desirable in the production of pharmaceuticals, agrochemicals, and specialty chemicals. The technology's benefits include high reaction precision, reduced use of toxic reagents, low energy input, and reactions conducted under ambient conditions. Continuous research, combined with global environmental regulations promoting sustainable chemistry, is expected to accelerate demand for photochemistry reagents, making this segment an increasingly vital part of the broader green chemical landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $515.2 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 10% |

The photosensitizers segment held 21.8% share in 2024 and is projected to grow at a CAGR of 9.7% during 2025-2034. This category consists of advanced organic molecules that drive site-specific, light-triggered chemical reactions, primarily in the development of pharmaceuticals and fine chemicals. The growing adoption of photoredox catalysis, where photosensitizers enable electron transfer processes, is unlocking innovative reaction pathways that traditional synthesis methods cannot achieve. As industries increasingly prioritize sustainable and high-efficiency production, demand for these reagents continues to expand rapidly.

The fine chemical and pharmaceutical synthesis segment held a 29.8% share in 2024, with an expected CAGR of 9.7% through 2034. This segment demonstrates the shift in the pharmaceutical sector toward greener and safer manufacturing technologies. Photochemical methods are being widely utilized in the production of active pharmaceutical ingredients (APIs), intermediates, and specialty compounds due to their superior selectivity, low waste generation, and environmental advantages compared to conventional processes.

North America Photochemistry Reagents for Green Synthesis Market captured a 36.9% share in 2024 and is forecast to grow at a 10.1% CAGR throughout 2034. The region benefits from robust research infrastructure, early adoption of emerging chemical technologies, and strong governmental support for green chemistry. Programs promoting sustainable manufacturing practices are encouraging industries to adopt photochemical synthesis methods for cleaner, safer, and more efficient production processes. The growing collaboration between academia, industry, and regulatory agencies continues to strengthen North America's leadership position in this evolving market.

Key companies actively operating within the Photochemistry Reagents for Green Synthesis Market include Kronos Worldwide Inc., BASF SE, Venator Materials PLC, Tronox Holdings PLC, Corning Incorporated, Huntsman Corporation, Tayca Corporation, Lomon Billions Group Co. Ltd., Ishihara Sangyo Kaisha Ltd., and Chemours Company. Leading companies in the photochemistry reagents for green synthesis market are focusing on expanding production capacities, advancing product innovation, and strengthening partnerships to enhance their global footprint. Firms are heavily investing in research and development to create more efficient, sustainable, and cost-effective photochemical reagents. Strategic collaborations with academic and industrial research institutions are enabling breakthroughs in photoredox catalysis and green manufacturing technologies. Companies are also implementing vertical integration strategies to secure raw material supply chains and ensure quality consistency. Moreover, expanding presence across high-growth markets, coupled with the adoption of cleaner production processes, is helping leading players align with global sustainability goals while maintaining competitiveness in the rapidly expanding green chemistry sector.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product category

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Million & Tons)

- 5.1 Key trends

- 5.2 Photocatalysts

- 5.2.1 Titanium dioxide TiO2)

- 5.2.2 Metal oxide semiconductors

- 5.2.2.1 Zinc oxide (ZnO)

- 5.2.2.2 Tungsten trioxide (WO3)

- 5.2.2.3 Iron oxide (Fe2O3)

- 5.2.3 Carbon-based photocatalysts

- 5.3 Photosensitizers

- 5.3.1 Porphyrin & chlorin derivatives

- 5.3.2 Transition metal complexes

- 5.3.3 Organic dyes & chromophores

- 5.4 Photoinitiators & photoacid/photobase generators

- 5.4.1 Acylphosphine oxide systems

- 5.4.2 Onium salt photoinitiators

- 5.4.3 Benzophenone & thioxanthone derivatives

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Tons)

- 6.1 Key trends

- 6.2 Environmental remediation

- 6.2.1 Water treatment & purification

- 6.2.1.1 Municipal wastewater treatment

- 6.2.1.2 Industrial effluent processing

- 6.2.1.3 Groundwater remediation

- 6.2.2 Air purification & VOC degradation

- 6.2.2.1 Indoor air quality management

- 6.2.2.2 Industrial emission control

- 6.2.2.3 Atmospheric pollutant degradation

- 6.2.3 Soil remediation & contaminant degradation

- 6.2.1 Water treatment & purification

- 6.3 Fine chemical & pharmaceutical synthesis

- 6.3.1 Active pharmaceutical ingredient (API) manufacturing

- 6.3.1.1 Late-stage functionalization

- 6.3.1.2 Stereoselective transformations

- 6.3.2 Specialty chemical production

- 6.3.2.1 Agrochemical intermediates

- 6.3.2.2 Fragrance & flavor compounds

- 6.3.2.3 Dye & pigment synthesis

- 6.3.3 Green oxidation & reduction processes

- 6.3.1 Active pharmaceutical ingredient (API) manufacturing

- 6.4 Polymer & Materials Chemistry

- 6.4.1 UV-curable coatings & inks

- 6.4.2 Photopolymerization & 3D printing

- 6.4.3 Surface functionalization & modification

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million & Tons)

- 7.1 Key trends

- 7.2 Chemical manufacturing

- 7.2.1 Basic chemical manufacturing

- 7.2.2 Specialty chemical manufacturing

- 7.2.3 Pharmaceutical manufacturing

- 7.3 Waste treatment & remediation

- 7.4 Manufacturing & electronics

- 7.5 Research & development

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Chemours Company

- 9.3 Corning Incorporated

- 9.4 Huntsman Corporation

- 9.5 Ishihara Sangyo Kaisha Ltd.

- 9.6 Kronos Worldwide Inc.

- 9.7 Lomon Billions Group Co. Ltd.

- 9.8 Tayca Corporation

- 9.9 Tronox Holdings PLC

- 9.10 Venator Materials PLC