|

시장보고서

상품코드

1876531

자동차 디지털 트윈 하드웨어 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Automotive Digital Twin Hardware Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

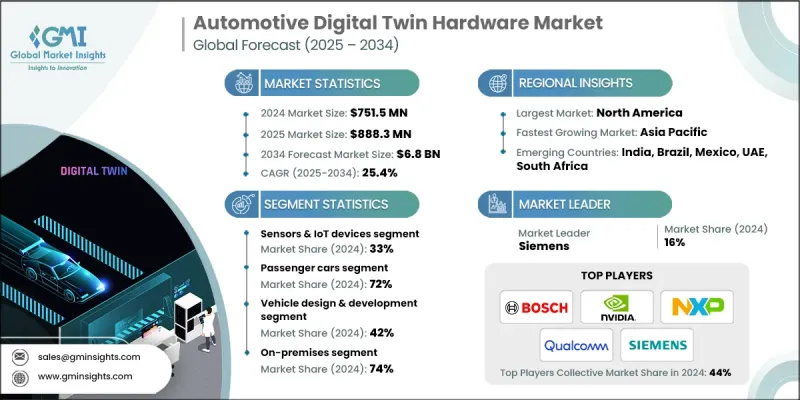

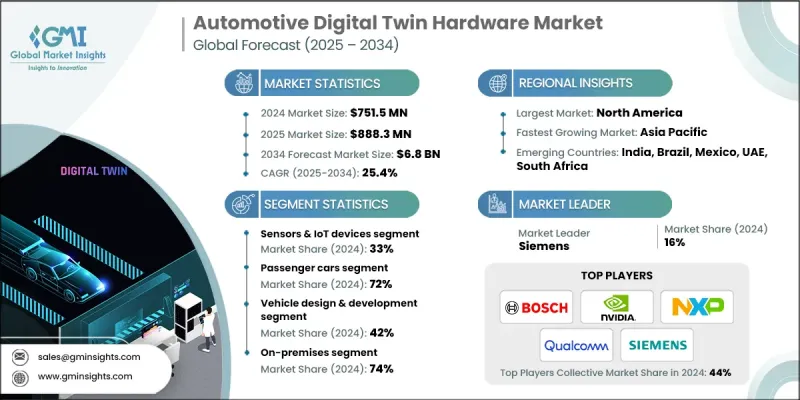

세계의 자동차 디지털 트윈 하드웨어 시장은 2024년에 7억 5,150만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 25.4%를 나타내 68억 달러에 이를 것으로 예측되고 있습니다.

자동차 제조업체 및 Tier 1 공급업체가 고성능 컴퓨팅(HPC) 장치, 센서, GPU, 에지 서버와 같은 고급 시스템을 도입함에 따라 디지털 트윈 하드웨어에 대한 수요가 가속화되고 있습니다. 이러한 하드웨어 구성 요소는 가상 환경에서 실제 세계의 차량 동작을 재현하고 제조업체가 생산 결과를 분석하고 조립 프로세스를 효율화하며 자원 활용도를 향상시킬 수 있습니다. 디지털 트윈 플랫폼은 엔지니어가 생산 라인에 구현하기 전에 조립 워크플로우를 가상적으로 테스트 및 검증할 수 있게 함으로써 노동력의 효율화도 촉진합니다. IoT/IIoT, 인공지능, 인더스트리 4.0 기술의 도입 확대는 자동차 제조를 변화시켜 견고한 디지털 트윈 하드웨어 솔루션의 필요성을 높여주고 있습니다. 차량이 소프트웨어 정의 시스템으로 진화하고 방대한 센서 데이터를 생성함에 따라 디지털 트윈 하드웨어는 실시간 데이터 처리, 예측 분석 및 운영 최적화를 촉진합니다. 자동화, 정밀성, 예지 보전을 중시하는 인더스트리 4.0의 대처에 수반해, 자동차 공장 내에서의 IoT 센서, 엣지 컴퓨팅 디바이스, 산업용 컨트롤러의 통합은 계속 확대되고 있어, 공장 데이터를 실시간으로 시뮬레이션·처리할 수 있는 강력한 컴퓨팅 인프라에 대한 강한 수요를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 7억 5,150만 달러 |

| 예측 금액 | 68억 달러 |

| CAGR | 25.4% |

센서 및 IoT 디바이스 분야는 2024년에 33%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR 25.5%를 나타낼 것으로 예측됩니다. 이 분야는 온도, 진동, 압력 등 실시간 지표를 포착하고 자동차 자산의 물리적 성능을 재현하는 데 중요한 역할을 합니다. 자율주행 기술의 보급이 진행되고 있는 가운데, LiDAR, 레이더, MEMS 부품 등의 고도의 센서의 활용이 가속되고 있어 예측 모델링이나 고장 진단의 고도화를 지지하고 있습니다.

승용차 부문은 2024년에 72%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR 25.7%를 나타낼 전망입니다. 이러한 이점은 시스템 연결성 향상, 전동화 동향, ADAS(첨단 운전자 보조 시스템)의 진보에 기인하고 있습니다. 자동차 제조업체는 GPU, IoT 대응 센서, 엣지 컴퓨팅 시스템을 도입하여 실시간 차량 시뮬레이션을 실시하여 설계 정밀도와 생산 효율을 모두 향상시키고 있습니다. 소프트웨어 정의 차량으로의 전환이 진행됨에 따라 예지 보전, 가상 검증 및 무선 소프트웨어 업데이트를 지원하는 디지털 트윈 기술의 필요성이 더욱 커지고 있습니다.

북미의 자동차 디지털 트윈 하드웨어 시장은 2024년 34%의 점유율을 차지했습니다. 이 지역의 성장은 커넥티드카, 자율주행차, 전기자동차기술의 강력한 채용에 견인되고 있습니다. 자동차 제조업체 및 부품 공급업체는 디지털화된 공장 환경과 실시간 시뮬레이션을 실현하기 위해 GPU 기반 컴퓨팅, 저지연 에지 하드웨어, IoT 센서 네트워크에 많은 투자를 하고 있습니다. AI 가속 프로세서와 모듈식 하드웨어 시스템의 급속한 발전은 지역 자동차 에코시스템 전체에서 설계 정확도, 운영 효율성, 생산 신뢰성을 더욱 향상시키고 있습니다.

세계의 자동차 디지털 트윈 하드웨어 시장에서 활동하는 주요 기업으로는 Bosch, Continental, General Electric, IBM, Molex, NVIDIA, NXP Semiconductors, PTC, Qualcomm, Siemens 등이 있습니다. 세계 자동차 디지털 트윈 하드웨어 시장의 주요 기업은 세계 프레즌스 확대를 위해 몇 가지 전략적 노력에 주력하고 있습니다. 확장성이 뛰어난 고성능 컴퓨팅 플랫폼 개발을 위한 연구 개발(R&D)에 대한 대규모 투자와 실시간 분석과 예측 인사이트를 제공하는 AI 구동 시뮬레이션 도구를 통합하고 있습니다. 자동차 제조업체 및 기술 제공업체와의 전략적 제휴 및 파트너십은 생산 및 설계 최적화를 위한 맞춤형 디지털 트윈 솔루션의 공동 개발을 추진하고 있습니다. 또한 공급망 강화를 위해 제조 능력의 확대와 지역별 유통 네트워크의 확충에도 주력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 고성능 컴퓨팅(HPC)과 GPU 하드웨어의 통합

- 엣지 컴퓨팅 및 IoT/IIoT 디바이스 도입

- AI 및 머신러닝 하드웨어의 진보

- 자율주행차 및 커넥티드카 개발의 확대

- Industry 4.0 및 스마트 제조 도입

- 업계의 잠재적 위험 및 과제

- 하드웨어 및 인프라의 고비용

- 이종 시스템 간의 데이터 상호 운용성

- 시장 기회

- AI 가속 시뮬레이션 하드웨어

- 엣지 컴퓨팅과 클라우드 컴퓨팅 인프라 통합

- 전기자동차 및 배터리 시스템에서 디지털 트윈 하드웨어 확장

- 5G 및 초저지연 네트워크 도입

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 연방규제환경

- 국제규격(ISO, SAE)

- 사이버 보안 요건

- 안전 및 규정 준수 기준

- 데이터 프라이버시 규제

- 환경 기준

- 지역별 규제의 차이

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 인공지능의 통합

- 합성 데이터와 시뮬레이션

- 양자 컴퓨팅의 응용 분야

- 고급 보안 기술

- 엣지 컴퓨팅의 진화

- 5G 및 차세대 연결 기술

- 지속가능성 기술

- 가격 동향 분석

- 총소유비용(TCO) 분석

- 하드웨어 조달 비용

- 도입·통합 비용

- 운영 및 유지 보수 비용

- 교육 및 지원 비용

- 특허 분석

- 기술 분야별 특허 포트폴리오 분석

- 특허 출원 동향과 혁신 활동

- 경쟁 특허 정보 분석

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 고객 여정 매핑

- 인지와 발견 단계

- 평가 및 선정 단계

- 도입 및 통합 단계

- 운영 및 최적화 단계

- 투자이익률(ROI) 프레임워크

- ROI 산출 조사 방법

- 회수 기간 분석

- 순 현재가치(NPV) 모델

- 리스크 조정 후 리턴

- 투자 및 자금 조달 분석

- 벤처 캐피탈의 동향

- 전략적 기업 투자

- 정부 자금 프로그램

- M&A 활동과 평가

- IPO 시장 역학

- 사모펀드 참여

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수 및 합병

- 파트너십 및 협력

- 신제품 발매

- 사업 확장 계획과 자금 조달

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 센서 및 IoT 디바이스

- 엣지 컴퓨팅 디바이스

- 연결성 및 네트워크 하드웨어

- 액추에이터 및 제어 시스템

- 고성능 컴퓨팅/시뮬레이션 하드웨어

제6장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 전기자동차(EV)

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 차량 설계 및 개발

- 제조 및 생산 최적화

- 예측 유지보수

- 자율주행차 테스트

- 공급망 및 차량 관리

제8장 시장 추계·예측 : 배포 모드별(2021-2034년)

- 주요 동향

- 클라우드

- On-Premise

- 하이브리드

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계의 기업

- Siemens

- DSpace

- NVIDIA

- PTC

- IBM

- Bosch

- Intel

- NXP Semiconductors

- General Electric

- 지역 기업

- Keysight Technologies

- Altair Engineering

- ETAS

- Vector Informatik

- National Instruments

- Ansys

- Qualcomm

- Continental

- Molex

- 신흥기업

- Threedy

- Neural Concept

- Applied Intuition

- Cognata

- Luminar Technologies

- Mobileye Global

The Global Automotive Digital Twin Hardware Market was valued at USD 751.5 million in 2024 and is estimated to grow at a CAGR of 25.4% to reach USD 6.8 billion by 2034.

The demand for digital twin hardware is accelerating as automotive OEMs and Tier-1 suppliers embrace advanced systems, including high-performance computing (HPC) units, sensors, GPUs, and edge servers. These hardware components replicate real-world vehicle behavior in virtual settings, allowing manufacturers to analyze production outcomes, streamline assembly processes, and improve resource utilization. Digital twin platforms also enhance workforce efficiency by enabling engineers to test and validate assembly workflows virtually before implementing them on production lines. The rising adoption of IoT/IIoT, artificial intelligence, and Industry 4.0 technologies is transforming automotive manufacturing, driving the need for robust digital twin hardware solutions. As vehicles evolve into software-defined systems that generate massive sensor data, digital twin hardware facilitates real-time data processing, predictive analytics, and operational optimization. With Industry 4.0 initiatives emphasizing automation, precision, and predictive maintenance, the integration of IoT sensors, edge computing devices, and industrial controllers within automotive plants continues to grow, creating strong demand for powerful computing infrastructure capable of simulating and processing real-time factory data.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $751.5 Million |

| Forecast Value | $6.8 Billion |

| CAGR | 25.4% |

The sensors and IoT devices segment held a 33% share in 2024 and is anticipated to grow at a CAGR of 25.5% from 2025 to 2034. This segment plays a critical role in capturing real-time metrics such as temperature, vibration, and pressure to replicate the physical performance of automotive assets. With the increasing adoption of autonomous driving technologies, the use of advanced sensors including LiDAR, radar, and MEMS components is accelerating, supporting enhanced predictive modeling and fault diagnostics.

The passenger cars segment held 72% share in 2024 and will grow at a CAGR of 25.7% between 2025 and 2034. This dominance is attributed to greater system connectivity, electrification trends, and advancements in driver assistance systems. Automotive manufacturers are deploying GPUs, IoT-enabled sensors, and edge computing systems to conduct real-time vehicle simulations, improving both design precision and production efficiency. The growing shift toward software-defined vehicles is reinforcing the need for digital twin technologies that support predictive maintenance, virtual validation, and over-the-air software updates.

North America Automotive Digital Twin Hardware Market held 34% share in 2024. The region's growth is driven by the strong adoption of connected, autonomous, and electric vehicle technologies. Automotive OEMs and component suppliers are heavily investing in GPU-powered computing, low-latency edge hardware, and IoT sensor networks to enable digitalized factory environments and real-time simulation. The rapid development of AI-accelerated processors and modular hardware systems is further enhancing design accuracy, operational efficiency, and production reliability across the regional automotive ecosystem.

Key players active in the Global Automotive Digital Twin Hardware Market include Bosch, Continental, General Electric, IBM, Molex, NVIDIA, NXP Semiconductors, PTC, Qualcomm, and Siemens. Leading companies in the Global Automotive Digital Twin Hardware Market are focusing on several strategic initiatives to expand their global presence. They are investing heavily in R&D to develop scalable, high-performance computing platforms and integrating AI-driven simulation tools to deliver real-time analytics and predictive insights. Strategic collaborations and partnerships with automakers and technology providers are helping them co-develop customized digital twin solutions for production and design optimization. Companies are also emphasizing the expansion of manufacturing capabilities and regional distribution networks to strengthen their supply chains.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.2.5 Deployment Mode

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Integration of high-performance computing (HPC) and GPU hardware

- 3.2.1.2 Adoption of edge computing and IoT/IIoT devices

- 3.2.1.3 Advancements in AI and machine learning hardware

- 3.2.1.4 Expansion of autonomous and connected vehicle development

- 3.2.1.5 Industry 4.0 and smart manufacturing adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High hardware and infrastructure costs

- 3.2.2.2 Data interoperability across heterogeneous systems

- 3.2.3 Market opportunities

- 3.2.3.1 AI-accelerated simulation hardware

- 3.2.3.2 Integration of edge and cloud computing infrastructure

- 3.2.3.3 Expansion of digital twin hardware in EV and battery systems

- 3.2.3.4 Adoption of 5G and ultra-low latency networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Federal regulatory environment

- 3.4.2 International standards (ISO, SAE)

- 3.4.3 Cybersecurity requirements

- 3.4.4 Safety and compliance standards

- 3.4.5 Data privacy regulations

- 3.4.6 Environmental standards

- 3.4.7 Regional regulatory variations

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Artificial intelligence integration

- 3.7.2 Synthetic data and simulation

- 3.7.3 Quantum computing applications

- 3.7.4 Advanced security technologies

- 3.7.5 Edge computing evolution

- 3.7.6 5G and beyond connectivity

- 3.7.7 Sustainability technologies

- 3.8 Price trend analysis

- 3.9 Total cost of ownership (TCO) analysis

- 3.9.1 Hardware acquisition costs

- 3.9.2 Implementation and integration costs

- 3.9.3 Operational and maintenance costs

- 3.9.4 Training and support costs

- 3.10 Patent analysis

- 3.10.1 Patent portfolio analysis by technology area

- 3.10.2 Patent filing trends and innovation activity

- 3.10.3 Competitive patent intelligence

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

- 3.13 Customer journey mapping

- 3.13.1 Awareness and discovery phase

- 3.13.2 Evaluation and selection phase

- 3.13.3 Implementation and integration phase

- 3.13.4 Operation and optimization phase

- 3.14 Return on investment (ROI) framework

- 3.14.1 ROI calculation methodologies

- 3.14.2 Payback period analysis

- 3.14.3 Net present value (NPV) models

- 3.14.4 Risk-adjusted returns

- 3.15 Investment and funding analysis

- 3.15.1 Venture capital trends

- 3.15.2 Strategic corporate investment

- 3.15.3 Government funding programs

- 3.15.4 M&A activity and valuations

- 3.15.5 IPO market dynamics

- 3.15.6 Private equity involvement

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Sensors & IoT devices

- 5.3 Edge computing devices

- 5.4 Connectivity & networking hardware

- 5.5 Actuators & control systems

- 5.6 High-performance computing / simulation hardware

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

- 6.4 Electric vehicles (EVs)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Vehicle design & development

- 7.3 Manufacturing & production optimization

- 7.4 Predictive maintenance

- 7.5 Autonomous vehicle testing

- 7.6 Supply chain & fleet management

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Cloud

- 8.3 On-premises

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Siemens

- 10.1.2 DSpace

- 10.1.3 NVIDIA

- 10.1.4 PTC

- 10.1.5 IBM

- 10.1.6 Bosch

- 10.1.7 Intel

- 10.1.8 NXP Semiconductors

- 10.1.9 General Electric

- 10.2 Regional Players

- 10.2.1 Keysight Technologies

- 10.2.2 Altair Engineering

- 10.2.3 ETAS

- 10.2.4 Vector Informatik

- 10.2.5 National Instruments

- 10.2.6 Ansys

- 10.2.7 Qualcomm

- 10.2.8 Continental

- 10.2.9 Molex

- 10.3 Emerging Players

- 10.3.1 Threedy

- 10.3.2 Neural Concept

- 10.3.3 Applied Intuition

- 10.3.4 Cognata

- 10.3.5 Luminar Technologies

- 10.3.6 Mobileye Global