|

시장보고서

상품코드

1876591

액랭식 EV 충전 케이블 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Liquid-Cooled EV Charging Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 액랭식 EV 충전 케이블 시장은 2024년에 20억 3,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 16.5%를 나타내 108억 8,000만 달러에 달할 것으로 예측되고 있습니다.

초고속 직류 충전 인프라의 급속한 배치로 EV 충전 환경은 크게 변화하고 있습니다. 액체 냉각 충전 케이블은 150kW에서 1.5MW 이상의 고전류 용량을 지원하여 컴팩트한 설계를 유지하면서 보다 빠르고 안전한 충전을 가능하게 합니다. 이러한 케이블을 통해 사업자와 네트워크 공급자는 케이블의 무게나 발열 위험을 증가시키지 않고 충전 시간을 대폭 단축할 수 있습니다. 이 기술은 또한 설치 면적의 효율화, 고출력 충전기의 운용·보수의 간소화, 대규모 플릿 전동화 및 고속도로 회랑의 개발을 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 20억 3,000만 달러 |

| 예측 금액 | 108억 8,000만 달러 |

| CAGR | 16.5% |

제조업체와 OEM 제조업체가 메가와트급 수요 증가에 대응하기 위해 사업 규모를 확대하는 가운데, 시장에서는 투자와 생산 확대가 가속하고 있습니다. 다수의 생산업체와 충전 인프라 통합 사업자가 제조 설비를 업그레이드하고 액체 냉각 부품의 파일럿 생산을 시작함과 동시에 커넥터 및 냉각 시스템 공급업체와 제휴하여 350kW에서 1,000kW 이상까지 충전 시스템의 도입을 가속화하고 있습니다. 트럭, 버스 및 배송 차량을 포함한 상용 전기 수송으로의 전환 확대는 액체 냉각 충전 솔루션의 주요 성장 촉진요인이 되었습니다. 대형 충전 용도는 안정적인 열 성능을 요구하며, 가혹한 작동 환경에서 장비 수명 연장과 효율적인 열 조절을 추구하는 사업자에게 액체 냉각 케이블은 이상적인 선택입니다.

2024년 기준에서 승용차 부문은 71%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 16.2%를 나타낼 것으로 예측됩니다. 이 부문의 압도적인 이점은 세계 전기자동차 보급의 급속한 발전과 초급속 충전 옵션에 대한 수요 증가와 밀접한 관련이 있습니다. 자동차 제조업체가 고전압 시스템의 통합을 진행하는 중, 급속 충전시의 효율적인 열 관리가 매우 중요합니다. 액체 냉각 케이블은 안전하고 컴팩트한 전력 공급을 가능하게 하고, 시스템 안전성과 성능 신뢰성을 유지하면서 보다 높은 에너지 통과량과 충전 시간 단축을 실현합니다.

레벨 3 부문은 66%의 점유율을 차지했으며 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 17.5%를 나타낼 것으로 예측됩니다. 이 부문의 이점은 차량의 다운타임을 크게 줄이는 초고속 직류 충전을 실현하는 능력 때문입니다. 전기자동차의 보급 확대에 따라, 특히 공공 충전 시설이나 고속도로 충전 시설에 있어서, 350kW를 넘는 고출력 충전 수요가 급증하고 있습니다. 액냉식 케이블은 대전류시의 열효율 관리, 신뢰성과 안전성 확보, 연속적인 고부하 사이클 하에서도 케이블 수명을 연장하는 점에서 이 분야에서 매우 중요한 역할을 하고 있습니다.

미국의 액랭식 EV 충전 케이블 시장은 85%의 점유율을 차지했으며, 2024년에는 5억 5,440만 달러 규모에 이르렀습니다. 미국 시장 확대의 배경에는 연방 정부 및 주 정부의 시책에 의한 전국 규모의 고속 충전 네트워크 정비가 진행되고 있는 것을 들 수 있습니다. 공공 네트워크와 함대 네트워크 모두에서 메가와트급 인프라의 급속한 발전은 고전압 및 고전류에 대응할 수 있는 선진적인 액냉 케이블 시스템 수요를 환기하고 있습니다. 이러한 솔루션은 안전성, 성능 및 내구성을 향상시키고 대규모 공공 및 상업 충전 환경에서 매우 중요합니다.

세계의 액랭식 EV 충전 케이블 시장의 주요 기업으로는 Sumitomo Electric, ABB, Huber+Suhner, Phoenix Contact, TE Connectivity, KemPower, Besen International, Brugg eConnect, Leoni, Sinbon Electronics 등이 있습니다. 이러한 기업들은 기술 혁신과 전략적 확대를 통해 경쟁 우위를 강화하고 있습니다. 액랭식 EV 충전 케이블 시장의 주요 기업은 시장에서의 지위를 강화하기 위해 다양한 전략적 노력을 채택하고 있습니다. 많은 기업들이 유연성과 안전성을 유지하면서 초고전력 레벨을 지원할 수 있는 차세대 케이블을 설계하기 위한 연구개발에 투자하고 있습니다. 충전 시스템 제조업체나 열 관리의 전문가와의 전략적 제휴는 기술의 상업화를 가속시키는 일조가 되고 있습니다. 또한 지역 수요에 대응하고 공급망의 리드 타임을 단축하기 위해 생산 능력의 확대와 현지 생산 거점의 설립도 진행하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 고출력 직류 급속 충전에 대한 수요 증가

- 승용차 및 상용차 부문에 있어서 전기자동차(EV)의 보급 확대

- 충전 인프라 확충에 대한 투자 확대

- 케이블의 내구성 및 열 관리에 있어서 진보

- 지원적인 정부 정책과 배출 감축 목표

- 업계의 잠재적 위험 및 과제

- 복잡한 설치 및 냉각 시스템 통합

- 숙련된 보수 요원의 확보가 곤란한 상황

- 시장 기회

- 메가와트 충전 회랑에서의 액체 냉각 케이블의 통합

- 전기자동차 인프라의 관민 연계 확대

- 경량이고 유연한 케이블 설계에 있어서 기술 혁신

- 차량의 전동화와 디포 충전에 대한 수요 증가

- 비용 최적화 냉각 솔루션을 제공하는 신규 진출기업의 동향

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 분석

- 가격 동향

- 지역별

- 차량별

- 코스트 내역 분석

- 비즈니스 케이스 및 투자 이익률(ROI) 분석

- 총소유비용의 틀

- ROI 산출 조사 방법

- 도입 스케줄과 이정표

- 리스크 평가 및 경감책

- 지속가능성과 환경영향 분석

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 전망과 기회

- 새로운 응용 기회

- 투자요건과 자금조달원

- 리스크 평가 및 경감책

- 시장 진출기업에의 전략적 제안

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수 및 합병

- 제휴 및 공동 사업

- 신제품 발매

- 사업 확장 계획과 자금 조달

제5장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상업용

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 공공 충전소

- 상용차 충전

- 주거용/개인용 충전

- 고속도로 및 장거리 충전 네트워크

제7장 시장 추계·예측 : 충전 레벨별(2021-2034년)

- 주요 동향

- 레벨 1

- 레벨 2

- 레벨 3

제8장 시장 추계·예측 : 케이블 길이별(2021-2034년)

- 주요 동향

- 5미터 미만

- 6-10미터

- 10미터 이상

제9장 시장 추계·예측 : 출력별(2021-2034년)

- 주요 동향

- 교류 충전

- 직류 충전

제10장 시장 추계·예측 : 도체 재료별(2021-2034년)

- 주요 동향

- 구리

- 알루미늄

제11장 시장 추계·예측 : 커넥터별(2021-2034년)

- 주요 동향

- 유형 1

- 유형 2

- CCS1

- CCS2

- CHAdeMO

- 기타

제12장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- LAMEA 지역

- 브라질

- 멕시코

- 아르헨티나

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제13장 기업 프로파일

- 세계의 기업

- ABB

- Aptiv

- Huawei

- Huber Suhner

- Johnson Electric

- Leoni AG

- Phoenix Contact

- Siemens

- Sinbon Electronics

- TE Connectivity

- Volex

- 지역 기업

- Blink Charging

- Boyd

- BTC Power

- CPC Worldwide

- FreeWire Technologies

- Kempower

- OMG

- Tritium

- Wallbox

- 신흥기업

- AG Electrical

- Cargill

- Engineered Fluids

- E-valucon/Sam Woo Electronics

- i-charging

- Linke Cable Technology

- Senku

- TST Cables

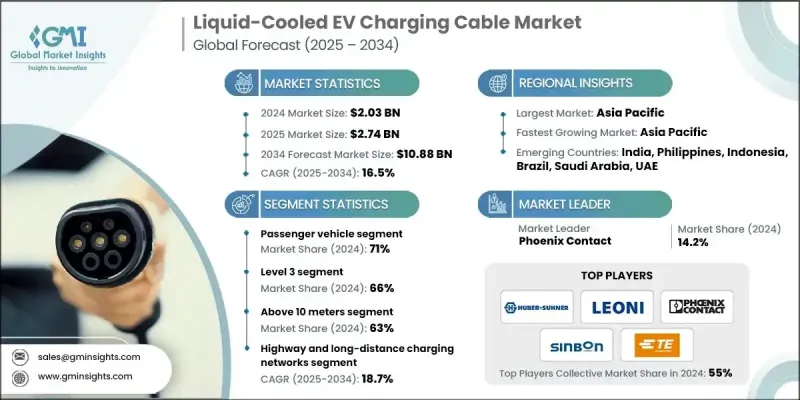

The Global Liquid-Cooled EV Charging Cable Market was valued at USD 2.03 billion in 2024 and is estimated to grow at a CAGR of 16.5% to reach USD 10.88 billion by 2034.

The accelerated deployment of ultra-fast DC charging infrastructure is transforming the EV charging landscape. Liquid-cooled charging cables support high current capacities ranging from 150 kW to more than 1.5 MW, enabling faster and safer charging while maintaining a compact design. These cables allow operators and network providers to reduce charging time significantly without increasing cable weight or heat risks. This technology also optimizes site area usage, simplifies operation and maintenance of high-power chargers, and supports large-scale fleet electrification and highway corridor development.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.03 Billion |

| Forecast Value | $10.88 Billion |

| CAGR | 16.5% |

The market is seeing intensified investments and production expansion as manufacturers and OEMs scale operations to meet rising megawatt-level demand. Numerous producers and charging infrastructure integrators have upgraded manufacturing facilities, initiated pilot-scale production of liquid-cooling components, and partnered with connector and cooling system suppliers to accelerate deployment of charging systems ranging from 350 kW to over 1,000 kW. The growing transition to electric commercial transport, including trucks, buses, and delivery fleets, is a major catalyst for liquid-cooled charging solutions. Heavy-duty charging applications demand consistent thermal performance, making liquid-cooled cables ideal for operators seeking longer equipment lifespan and efficient thermal regulation under demanding operational conditions.

In 2024, the passenger vehicle segment held a 71% share and is anticipated to grow at a CAGR of 16.2% through 2034. The strong dominance of this segment is linked to the rapid global increase in electric car adoption and the rising need for ultra-fast charging options. As automakers continue integrating higher voltage systems, efficient heat management during fast charging becomes critical. Liquid-cooled cables enable safe and compact power delivery, allowing higher energy throughput and shorter charging durations while maintaining system safety and performance reliability.

The level 3 segment held a 66% share and is expected to grow at a CAGR of 17.5% between 2025 and 2034. This segment's leadership stems from its capability to deliver ultra-fast DC charging that significantly minimizes vehicle downtime. With the surge in electric vehicle adoption, demand for high-power charging exceeding 350 kW has risen sharply, especially in public and highway charging applications. Liquid-cooled cables play a vital role in this space by managing heat efficiently during high current flow, ensuring reliable, safe operation, and longer cable service life even under continuous heavy-duty cycles.

United States Liquid-Cooled EV Charging Cable Market held an 85% share, generating USD 554.4 million in 2024. Market expansion in the U.S. is being driven by the nationwide implementation of high-speed charging networks supported by federal and state initiatives. Rapid development of megawatt-scale infrastructure across both public and fleet networks is stimulating demand for advanced liquid-cooled cable systems that can handle high voltage and current levels. These solutions enhance safety, performance, and durability, which are critical in large-scale public and commercial charging environments.

Leading players in the Global Liquid-Cooled EV Charging Cable Market include Sumitomo Electric, ABB, Huber+Suhner, Phoenix Contact, TE Connectivity, KemPower, Besen International, Brugg eConnect, Leoni, and Sinbon Electronics. These companies continue to strengthen their competitive advantage through technological innovation and strategic expansion. Key participants in the Liquid-Cooled EV Charging Cable Market are adopting a range of strategic initiatives to enhance their market position. Many are investing in research and development to design next-generation cables capable of supporting ultra-high power levels while maintaining flexibility and safety. Strategic collaborations with charging system manufacturers and thermal management specialists are helping accelerate technology commercialization. Companies are also expanding production capacities and establishing localized manufacturing hubs to meet regional demand and reduce supply chain lead times.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Charging Level

- 2.2.4 Cable Length

- 2.2.5 Power

- 2.2.6 Application

- 2.2.7 Conductor Material

- 2.2.8 Connector

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-power dc fast charging

- 3.2.1.2 Increasing EV adoption across passenger and commercial segments

- 3.2.1.3 Growing investments in charging infrastructure expansion

- 3.2.1.4 Advancements in cable durability and thermal management

- 3.2.1.5 Supportive government policies and emission reduction targets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex installation and cooling system integration

- 3.2.2.2 Limited availability of skilled maintenance personnel

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of liquid-cooled cables in megawatt charging corridors

- 3.2.3.2 Expansion of public-private partnerships in EV infrastructure

- 3.2.3.3 Technological innovation in lightweight and flexible cable design

- 3.2.3.4 Rising demand for fleet electrification and depot charging

- 3.2.3.5 Entry of new players offering cost-optimized cooling solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By vehicle

- 3.10 Cost breakdown analysis

- 3.11 Business Case & ROI Analysis

- 3.11.1 Total cost of ownership framework

- 3.11.2 ROI calculation methodologies

- 3.11.3 Implementation timeline & milestones

- 3.11.4 Risk assessment & mitigation strategies

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.13.1 Emerging Application Opportunities

- 3.13.2 Investment Requirements & Funding Sources

- 3.13.3 Risk Assessment & Mitigation Strategies

- 3.13.4 Strategic Recommendations for Market Participants

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LAMEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUV

- 5.3 Commercial

- 5.3.1 Light commercial vehicles (LCV)

- 5.3.2 Medium commercial vehicles (MCV)

- 5.3.3 Heavy commercial vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Public Charging Stations

- 6.3 Commercial Fleet Charging

- 6.4 Residential / Private Charging

- 6.5 Highway and Long-Distance Charging Networks

Chapter 7 Market Estimates & Forecast, By Charging Level, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Level 1

- 7.3 Level 2

- 7.4 Level 3

Chapter 8 Market Estimates & Forecast, By Cable Length, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Below 5 meters

- 8.3 6-10 meters

- 8.4 Above 10 meters

Chapter 9 Market Estimates & Forecast, By Power, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 AC charging

- 9.3 DC charging

Chapter 10 Market Estimates & Forecast, By Conductor Material, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Copper

- 10.3 Aluminum

Chapter 11 Market Estimates & Forecast, By Connector, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 Type 1

- 11.3 Type 2

- 11.4 CCS1

- 11.5 CCS2

- 11.6 CHAdeMO

- 11.7 Others

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Philippines

- 12.4.7 Indonesia

- 12.5 LAMEA

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 South Africa

- 12.5.5 Saudi Arabia

- 12.5.6 UAE

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 ABB

- 13.1.2 Aptiv

- 13.1.3 Huawei

- 13.1.4 Huber+Suhner

- 13.1.5 Johnson Electric

- 13.1.6 Leoni AG

- 13.1.7 Phoenix Contact

- 13.1.8 Siemens

- 13.1.9 Sinbon Electronics

- 13.1.10 TE Connectivity

- 13.1.11 Volex

- 13.2 Regional Players

- 13.2.1 Blink Charging

- 13.2.2 Boyd

- 13.2.3 BTC Power

- 13.2.4 CPC Worldwide

- 13.2.5 FreeWire Technologies

- 13.2.6 Kempower

- 13.2.7 OMG

- 13.2.8 Tritium

- 13.2.9 Wallbox

- 13.3 Emerging Players

- 13.3.1 AG Electrical

- 13.3.2 Cargill

- 13.3.3 Engineered Fluids

- 13.3.4 E-valucon / Sam Woo Electronics

- 13.3.5 i-charging

- 13.3.6 Linke Cable Technology

- 13.3.7 Senku

- 13.3.8 TST Cables