|

시장보고서

상품코드

1876593

식품 압출기 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Food Extrusion Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

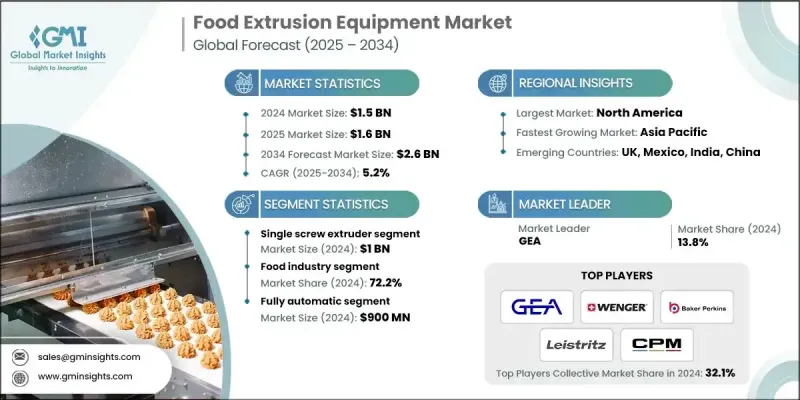

세계의 식품 압출기 시장은 2024년에 15억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 5.2%를 나타내 26억 달러에 이를 것으로 예측됩니다.

식물 유래의 고기 및 어패류 대체품에 대한 소비자의 관심의 높아짐은 특수 압출 기술에 큰 기회를 가져오고 있습니다. 고수분 압출 조리(HMEC) 기술을 통해 대체 단백질 제품에서 섬유질로 고기와 같은 식감을 실현할 수 있어 고수분 고기 대체품(HMMA)용으로 설계된 첨단 2축 압출기 수요를 촉진하고 있습니다. 지속 가능한 동물 유래가 아닌 단백질을 요구하는 소비자에 의한 플렉시탈리안식이로의 이행도, 이 동향을 한층 더 뒷받침하고 있습니다. 동시에 뛰어난 맛과 영양가를 겸비한 스낵에의 기호의 고조도, 압출 기술과의 궁합이 양호합니다. 이 공정에서는 온도·압력·원료 조성을 정밀하게 제어함으로써 저지방·고단백·고섬유의 식품 제조가 가능해집니다. 압출 성형은 여러 제조 공정을 단일 작업으로 통합하는 효율적이고 연속적인 방법을 제공하여 에너지 및 물 소비를 크게 줄이는 동시에 바닥 면적과 생산 속도를 최적화합니다. 이러한 이점으로 인해 압출 성형은 경쟁이 심한 식품 제조 환경에서 비용 효율적이고 지속 가능한 옵션이 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 15억 달러 |

| 예측 금액 | 26억 달러 |

| CAGR | 5.2% |

2024년 단축 압출기 부문은 10억 달러의 매출을 창출했습니다. 그 성장은 주로 투자 요건의 낮음과 조작의 간편함에 의해 견인되고 있으며, 중소기업(SME)이나 개발도상지역의 제조업자에게 매력적인 선택이 되고 있습니다. 이 시스템은 대규모 자본 지출 없이 생산 확대 및 현대화를 목표로 하는 기업에게 실용적이고 저렴한 입구를 제공합니다.

전자동 시스템 부문은 2024년 9억 달러의 매출을 창출했습니다. 자동 압출기의 채용 증가로 제품의 균일성, 정확성 및 전반적인 효율성이 크게 향상되었습니다. 센서, 프로그래머블 로직 컨트롤러(PLC), 실시간 모니터링 툴과 같은 고급 자동화 기술을 통해 제조업체는 온도, 공급 속도, 압력, 수분 등 주요 생산 변수를 엄격하게 관리할 수 있습니다. 최소한의 운영자 개입으로 이러한 시스템은 인적 오류의 위험을 크게 줄여 대량 생산에서도 균일한 제품 품질을 보장합니다.

미국의 식품 압출기 시장은 2024년 81.8%의 점유율을 차지하며 4억 2,000만 달러를 창출했습니다. 일본 시장은 첨단 제조 능력, 엄격한 규제 기준, 자동화 및 식품 안전에 대한 강한 주력을 특징으로 합니다. 스낵, 시리얼, 반려동물 식품, 대체 단백질 등의 범주를 포함한 성숙한 가공 식품 분야는 높은 처리량, 일관된 품질 및 FDA 및 USDA가 규정한 규제 지침을 준수하는 압출 시스템에 대한 투자를 계속 추진하고 있습니다.

세계의 식품 압출기 시장에서 사업을 전개하고 있는 주요 기업에는 Bausano, Bonnot, GEA, Buhler, CPM, B&P Littleford, Cowin Extrusion, Leistritz, Baker Perkins, Wenger, Legris, Coperion, Steer World, Xtrutech, Xinda Corp 등이 있습니다. 이러한 기업들은 이러한 진화 상황에서 우위를 유지하기 위해 지속적인 혁신과 기술 발전에 주력하고 있습니다. 세계 식품 압출기 시장의 주요 제조업체는 세계 존재감을 강화하기 위한 전략적 노력에 주력하고 있습니다. 많은 기업들이 새로운 재료를 처리하고 식물 유래 제품의 식감 제어를 강화할 수 있는 기계를 설계하기 위해 연구 개발에 많은 투자를 하고 있습니다. 또한 기업은 기술 포트폴리오를 확대하고 새로운 지역 시장에 진출하기 위해 전략적 파트너십과 제휴를 맺고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 플랜트 기반 혁명

- 보다 건강 지향으로 기능성이 있는 스낵에 수요

- 운용 효율성과 범용성

- 업계의 잠재적 위험 및 과제

- 고액의 자본 투자와 운영 비용

- 운용상의 복잡성과 스킬 갭

- 기회

- Industry 4.0 통합

- 신규 원료의 개발과 업사이클링

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 기기별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- 갭 분석

- 리스크 평가 및 경감책

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수 및 합병

- 파트너십 및 협력

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 장치 유형별(2021-2034년)

- 주요 동향

- 단일 나사 압출기

- 이중 나사 압출기

제6장 시장 추계·예측 : 조작 모드별(2021-2034년)

- 주요 동향

- 수동식

- 반자동식

- 전자동식

제7장 시장 추계·예측 : 용량별(2021-2034년)

- 주요 동향

- 3,000kg/h 미만

- 3,000-10,000kg/h

- 10,000kg/h 초과

제8장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 반려동물 사료 및 수산 사료

- 곡물 및 스낵

- 식물성 단백질

- 식품 원료

- 기타(과자류 등)

제9장 시장 추계·예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 식품 산업

- 동물 사료 산업

- 기타(연구 기관 등)

제10장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 간접 판매

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- B&P Littleford

- Baker Perkins

- Bausano

- Bonnot

- Buhler

- Coperion

- Cowin Extrusion

- CPM

- GEA

- Legris

- Leistritz

- Steer World

- Wenger

- Xinda Corp.

- Xtrutech

The Global Food Extrusion Equipment Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 2.6 billion by 2034.

Increasing consumer interest in plant-based alternatives to meat and seafood is creating substantial opportunities for specialized extrusion technologies. High moisture extrusion cooking (HMEC) is enabling manufacturers to achieve fibrous, meat-like textures in alternative protein products, fueling demand for advanced twin-screw extruders designed for high moisture meat analogues (HMMA). The shift toward flexitarian diets, driven by consumers looking for sustainable, animal-free protein options, is further supporting this trend. At the same time, the rising preference for snacks that combine great taste with nutritional benefits aligns well with extrusion technology. This process enables the creation of low-fat, high-protein, and high-fiber foods through precise control of temperature, pressure, and ingredient composition. Extrusion offers an efficient, continuous method that merges several manufacturing stages into a single operation, significantly reducing energy and water consumption while optimizing floor space and production speed. These advantages make extrusion a cost-effective and sustainable choice in a highly competitive food manufacturing environment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 5.2% |

In 2024, the single-screw extruders segment generated USD 1 billion. Their growth is largely driven by lower investment requirements and operational simplicity, making them an attractive choice for small and medium-sized enterprises (SMEs) and manufacturers in developing regions. These systems provide a practical and affordable entry point for businesses seeking to expand or modernize production without large capital expenditures.

The fully automatic systems segment generated USD 900 million in 2024. The increasing adoption of automated extruders has greatly enhanced product consistency, precision, and overall efficiency. Advanced automation technologies, including sensors, programmable logic controllers (PLCs), and real-time monitoring tools, allow manufacturers to maintain strict control over key production variables such as temperature, feed rate, pressure, and moisture. With minimal operator intervention, these systems significantly reduce the risk of human error and ensure uniform product quality across large production volumes.

United States Food Extrusion Equipment Market accounted for 81.8% share in 2024, generating USD 420 million. The country's market is characterized by advanced manufacturing capabilities, stringent regulatory standards, and a strong focus on automation and food safety. A mature processed food sector, including categories like snacks, cereals, pet food, and alternative proteins, continues to drive investments in extrusion systems that offer high throughput, consistent quality, and compliance with regulatory guidelines set by the FDA and USDA.

Leading companies operating in the Global Food Extrusion Equipment Market include Bausano, Bonnot, GEA, Buhler, CPM, B&P Littleford, Cowin Extrusion, Leistritz, Baker Perkins, Wenger, Legris, Coperion, Steer World, Xtrutech, and Xinda Corp. These players are focusing on continuous innovation and technical advancement to stay ahead in this evolving landscape. Major manufacturers in the Global Food Extrusion Equipment Market are focusing on a mix of strategic initiatives to strengthen their global presence. Many are investing heavily in research and development to design machines capable of handling novel ingredients and delivering enhanced texture control for plant-based products. Companies are also entering strategic partnerships and collaborations to expand their technology portfolios and reach new regional markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Mode of operation

- 2.2.4 Capacity

- 2.2.5 Application

- 2.2.6 End use industry

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 The plant-based revolution

- 3.2.1.2 Demand for better for you and functional snacks

- 3.2.1.3 Operational efficiency and versatility

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital investment and operating costs

- 3.2.2.2 Operational complexity and skill gap

- 3.2.3 Opportunities

- 3.2.3.1 Integration of industry 4.0

- 3.2.3.2 Development for novel ingredients and upcycling

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Gap Analysis

- 3.9 Risk assessment and mitigation

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Single screw extruder

- 5.3 Twin screw extruder

Chapter 6 Market Estimates and Forecast, By Mode of Operation Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Fully automatic

Chapter 7 Market Estimates and Forecast, By Capacity, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Below 3,000 kg/hr

- 7.3 3,000-10,000 kg/hr

- 7.4 Above 10,000 kg/hr

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Pet food & aqua feed

- 8.3 Cereals & snacks

- 8.4 Plant-based proteins

- 8.5 Food ingredients

- 8.6 Others (confectionery products, etc.)

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Food industry

- 9.3 Animal feed industry

- 9.4 Others (research institutions, etc.)

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 B&P Littleford

- 12.2 Baker Perkins

- 12.3 Bausano

- 12.4 Bonnot

- 12.5 Buhler

- 12.6 Coperion

- 12.7 Cowin Extrusion

- 12.8 CPM

- 12.9 GEA

- 12.10 Legris

- 12.11 Leistritz

- 12.12 Steer World

- 12.13 Wenger

- 12.14 Xinda Corp.

- 12.15 Xtrutech