|

시장보고서

상품코드

1876614

처리 및 처분 시추 폐기물 관리 시장 : 시장 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Treatment and Disposal Drilling Waste Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

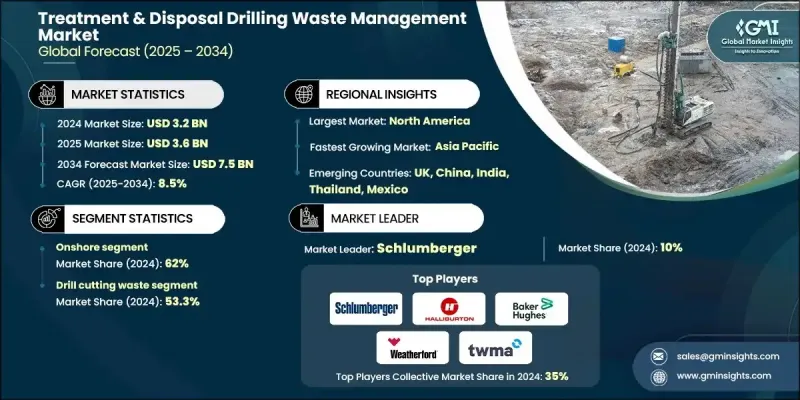

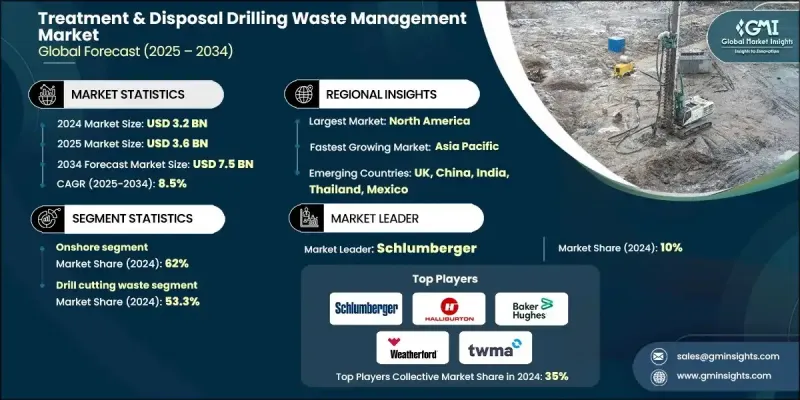

세계의 처리 및 처분 시추 폐기물 관리 시장은 2024년에 32억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.5%로 성장할 전망이며, 75억 달러에 달할 것으로 예측되고 있습니다.

이 업계의 확대는 전 세계적으로 엄격한 환경 규제의 영향을 받고 있습니다. 이에 따라 석유 및 가스 사업자는 유해 폐기물 처리, 배출 삭감, 수질 오염 방지에 관해 보다 엄격한 기준에 대한 대응을 강요받고 있습니다. 이러한 규제의 진화는 혁신적인 폐기물 처리 시스템과 컴플라이언스 기반에 대한 대규모 투자를 촉진하고 있습니다. 매립 처분 회피, 배출 규제, 재활용 시책을 중시하는 틀이 업계 전체의 서비스 모델을 재구축하고 있습니다. 게다가 확대 생산자 책임 및 폐기물 최소화 목표에 대한 주목의 고조에 따라 유전 사업자는 지속 가능한 기술을 업무 프로세스에 통합하도록 촉구되고 있습니다. 수압 파쇄법이나 수평 시추와 같은 비 기존 시추 수법이 보급됨에 따라, 시추 폐기물의 양과 복잡성은 현저하게 증가하고 있습니다. 이러한 기술은 오염된 시추 폐기물, 진흙물, 생산수를 보다 많이 발생시키기 때문에 고도의 처리, 봉쇄 및 재활용 시스템의 필요성이 강해지고 있습니다. 북미와 아시아의 셰일 오일 타이트 오일 탐사의 지속적인 확대는 향후 수년간 시추 폐기물 관리 솔루션 수요를 가속화할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 시 가치 | 32억 달러 |

| 예측 금액 | 75억 달러 |

| CAGR | 8.5% |

육상 부문은 2024년에 62%의 점유율을 차지하였고, 2034년까지 연평균 복합 성장률(CAGR) 8%로 성장할 것으로 예측됩니다. 육상 시추 폐기물 관리의 급증은 기존 탐사보다 더 많은 양의 시추 폐기물, 생산수 및 시추 유체를 생산하는 비재래형 에너지 생산의 확대로 인한 것입니다. 치밀한 혈암층에서 발생하는 폐기물의 복잡성으로 인해 원심 분리, 응고, 바이오레미디에이션 등의 고급 처리 기술이 요구되고 있습니다.

시추 부스러기 부문은 53.3%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 7.8%로 성장할 것으로 예측됩니다. 시추 작업 중에 발생하는 가장 중요한 폐기물 중 하나인 시추 폐기물은 기존의 오프사이트 처분에서 온사이트 처리 및 재이용으로 이행하고 있습니다. 열 탈착 및 고체 제어 시스템과 같은 기술은 시추 현장에서의 직접 처리, 이용 가능한 유체의 회수, 운송 요건의 최소화에 점점 활용되고 있으며, 효율성과 지속가능성을 모두 향상시키고 있습니다.

미국의 처리 및 처분 시추 폐기물 관리 시장은 2024년에 7억 달러 규모에 달했습니다. 이 나라의 성장은 규제 집행 강화와 주요 석유 및 가스 생산 지역에서 시추 활동의 활성화에 의해 견인되고 있습니다. 환경보호청(EPA) 및 토지관리국(BLM)은 메탄 제어 및 폐기물 봉쇄에 관한 새로운 가이드라인을 실시하여 고화처리, 열탈착, 바이오레메디에이션 등 현대적인 처리 기술의 채용을 사업자에게 촉구하고 있습니다.

처리 및 처분 시추 폐기물 관리 시장에서 활동하는 주요 기업으로는 Baker Hughes, Augean Plc, Clean Harbors, Inc., Halliburton, Schlumberger, Weatherford, TWMA, Secure Energy Services, Inc., Ecoserv LLC, Pure Environmental, Milestone Environmental Services, Derrick Equipment Company, Newpark Resources Inc., NOV Inc., GN Solids Control, Imdex Limited, Ridgeline Canada Inc., Select Water Solutions, Soli-Bond, Inc., Tidal Logistics 및 Environmental Development Company Ltd 등이 있습니다. 주요 기업은 기술 혁신, 처리 능력 확대, 전략적 제휴에 주력하여 시추 폐기물 관리 분야의 존재감을 강화하고 있습니다. 각사는 열탈착, 바이오레미디에이션, 원심 분리 등 선진적 처리 기술에 다액의 투자를 하고 비용 효과가 뛰어나 환경 규제에 적합한 솔루션을 제공하기 위해 노력하고 있습니다. 많은 기업들이 탐광 및 생산 기업과의 장기 서비스 제휴를 구축하여 안정적인 수요를 확보함과 동시에 지역적인 사업 기반의 확대를 도모하고 있습니다. 신흥 시추 지역으로의 진출과 디지털 모니터링 시스템의 통합은 기업의 업무 효율성과 폐기물 추적 가능성의 향상에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 새로운 기회 및 동향

- 디지털화 및 IoT 통합

- 신흥 시장 진출

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 노력

- 경쟁 벤치마킹

- 전략적 대시보드

- 혁신 및 기술 동향

제5장 시장 규모 및 예측 : 폐기물별(2021-2034년)

- 주요 동향

- 폐윤활유

- 시추 폐기물

- 기타

제6장 시장 규모 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 온쇼어

- 오프쇼어

제7장 시장 규모 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 라틴아메리카

- 브라질

- 아르헨티나

제8장 기업 프로파일

- Augean Plc

- Baker Hughes

- Clean Harbors, Inc.

- Derrick Equipment Company

- GN Solids Control

- Halliburton

- Imdex Limited

- Newpark Resources Inc.

- NOV Inc.

- Ridgeline Canada Inc.

- Schlumberger

- Secure Energy Services, Inc.

- Select Water Solutions

- Soli-Bond, Inc.

- TWMA

- Weatherford

- Ecoserv LLC

- Milestone Environmental Services

- Pure Environmental

- Tidal Logistics

- Environmental Development Company Ltd

The Global Treatment & Disposal Drilling Waste Management Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 7.5 billion by 2034.

The industry's expansion is influenced by the growing stringency of environmental laws worldwide, which are compelling oil and gas operators to comply with tighter standards on hazardous waste handling, emissions mitigation, and water contamination prevention. These evolving regulations are driving large-scale investments in innovative waste treatment systems and compliance infrastructure. Frameworks emphasizing landfill diversion, emission controls, and recycling initiatives are reshaping service models across the sector. In addition, the increasing focus on extended producer responsibility and waste minimization goals is prompting oilfield operators to integrate sustainable technologies into their workflows. As unconventional drilling methods such as hydraulic fracturing and horizontal drilling become more prevalent, the quantity and complexity of drilling waste have increased significantly. These techniques produce higher levels of contaminated cuttings, muds, and produced water, intensifying the need for advanced treatment, containment, and recycling systems. The continued rise of shale and tight oil exploration across North America and Asia is expected to accelerate demand for drilling waste management solutions over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 8.5% |

The onshore segment accounted for a 62% share in 2024 and is projected to grow at an 8% CAGR through 2034. The surge in onshore drilling waste management stems from the expansion of unconventional energy production, which generates greater volumes of cuttings, produced water, and drilling fluids than traditional exploration. The complexity of waste generated from dense shale formations calls for sophisticated treatment technologies such as centrifugation, solidification, and bioremediation.

The drill cuttings segment held a 53.3% share and is projected to grow at a CAGR of 7.8% through 2034. As one of the most significant waste types produced during drilling operations, drill cuttings are undergoing a shift from conventional offsite disposal to onsite treatment and reuse. Technologies such as thermal desorption and solids control systems are being increasingly utilized to process waste directly at drilling locations, recover usable fluids, and minimize transportation requirements, improving both efficiency and sustainability.

United States Treatment & Disposal Drilling Waste Management Market captured USD 700 million in 2024. The country's growth is driven by regulatory enforcement and elevated drilling activity across key oil- and gas-producing regions. The Environmental Protection Agency (EPA) and the Bureau of Land Management (BLM) have implemented new guidelines addressing methane control and waste containment, pushing operators to adopt modern treatment technologies like solidification, thermal desorption, and bioremediation.

Prominent companies active in the Treatment & Disposal Drilling Waste Management Market include Baker Hughes, Augean Plc, Clean Harbors, Inc., Halliburton, Schlumberger, Weatherford, TWMA, Secure Energy Services, Inc., Ecoserv LLC, Pure Environmental, Milestone Environmental Services, Derrick Equipment Company, Newpark Resources Inc., NOV Inc., GN Solids Control, Imdex Limited, Ridgeline Canada Inc., Select Water Solutions, Soli-Bond, Inc., Tidal Logistics, and Environmental Development Company Ltd. Leading market players are focusing on technological innovation, capacity expansion, and strategic partnerships to reinforce their presence in the drilling waste management landscape. Companies are investing heavily in advanced treatment technologies such as thermal desorption, bioremediation, and centrifugation to deliver cost-effective and environmentally compliant solutions. Many are forming long-term service alliances with exploration and production firms to secure steady demand while enhancing their regional footprint. Expansions into emerging drilling regions and the integration of digital monitoring systems are helping firms improve operational efficiency and waste traceability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Waste trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Waste, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Waste lubricants

- 5.3 Drill cuttings

- 5.4 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Onshore

- 6.3 Offshore

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Augean Plc

- 8.2 Baker Hughes

- 8.3 Clean Harbors, Inc.

- 8.4 Derrick Equipment Company

- 8.5 GN Solids Control

- 8.6 Halliburton

- 8.7 Imdex Limited

- 8.8 Newpark Resources Inc.

- 8.9 NOV Inc.

- 8.10 Ridgeline Canada Inc.

- 8.11 Schlumberger

- 8.12 Secure Energy Services, Inc.

- 8.13 Select Water Solutions

- 8.14 Soli-Bond, Inc.

- 8.15 TWMA

- 8.16 Weatherford

- 8.17 Ecoserv LLC

- 8.18 Milestone Environmental Services

- 8.19 Pure Environmental

- 8.20 Tidal Logistics

- 8.21 Environmental Development Company Ltd