|

시장보고서

상품코드

1876627

전기자동차 충전 부하 관리 시스템 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Electric Vehicle Charging Load Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

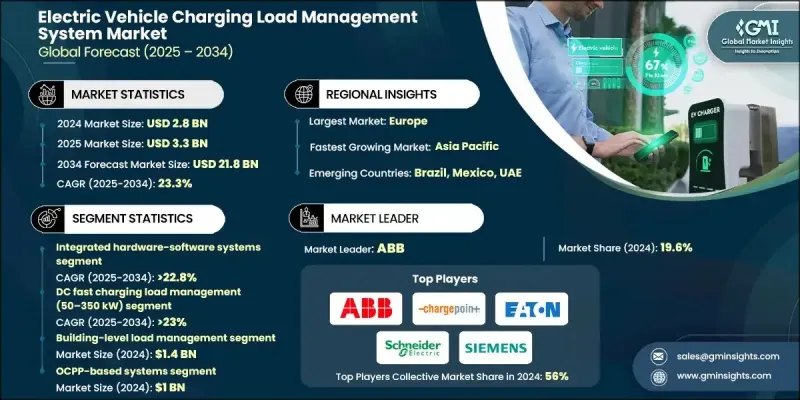

세계의 전기자동차 충전 부하 관리 시스템 시장은 2024년 28억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 23.3%로 성장할 전망이며, 218억 달러에 이를 것으로 예측됩니다.

시장 성장은 전기자동차의 급속한 보급 확대, EV 플릿 확대, 지능형 에너지 관리 솔루션에 대한 수요 증가로 추진되고 있습니다. 충전 인프라, 그리드 연결성, 에너지 저장 시스템이 발전함에 따라 이해관계자들은 운영 효율성 극대화, 스마트 그리드 솔루션 통합, 부하 분산 최적화에 주력하여 신뢰성 있고 비용 효율적인 충전 네트워크를 확보하고 있습니다. 이 분야는 연결성, 자동화 및 데이터 구동형의 운용으로 이행하고 있어, 기존 에너지 관리 수법을 변혁하는 것과 동시에, 충전 네트워크의 모니터링 및 보수 방법의 재정의를 진행하고 있습니다. 디지털 플랫폼, 예측형 에너지 스케줄링, AI 탑재 제어 시스템에 대한 투자 증가는 보다 확장성, 회복력, 효율성이 뛰어난 EV 충전 생태계 구축 기회를 창출하고 있습니다. IoT 연결 충전소, AI 기반 부하 분산 솔루션, 클라우드 지원 에너지 관리 플랫폼의 도입 확대가 업계를 변화시키고 있습니다. 이러한 기술을 통해 전력 수요의 실시간 모니터링, 예측 부하 배분, 전력 회사, 충전 사업자, 플릿 관리자 간의 원활한 연계가 가능합니다. 스마트 미터, 텔레매틱스, AI 분석을 활용하여 사업자는 에너지 효율 향상, 피크 부하 감소, 운영 비용 절감, 보다 스마트하고 강인한 충전 네트워크를 구축할 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 시 가치 | 28억 달러 |

| 예측 금액 | 218억 달러 |

| CAGR | 23.3% |

통합 하드웨어 소프트웨어 시스템 부문은 2024년에 37%의 점유율을 차지하였으며, 2025-2034년 CAGR 22.8%로 성장할 것으로 예측됩니다. 이 부문은 스마트 충전기, 동적 부하 제어 장치, 에너지 저장 인터페이스 및 통신 모듈을 통합 플랫폼에 결합하여 최적의 EV 충전, 전력 시스템의 신뢰성, 에너지 효율을 보장하는 데 핵심적인 역할을 합니다. 고전압 충전 네트워크가 복잡해짐에 따라 정밀한 에너지 분배를 관리하기 위한 AI 구동 제어 알고리즘, 고급 모니터링 시스템, 숙련된 운영자 수요가 증가하고 있습니다.

직류 급속 충전 부하 관리 부문(50-350kW)는 2024년에 36%의 점유율을 차지하였고, 2034년까지 연평균 복합 성장률(CAGR) 23%로 성장할 것으로 예측됩니다. 이 부문의 성장은 대용량 충전기 도입, EV 충전 시간 단축 요구 및 그리드 최적화된 스마트 부하 분산 솔루션에 대한 수요에 의해 추진되고 있습니다. 사업자는 충전기의 이용률 향상, 피크 수요 압력의 완화, 운용 효율의 개선을 도모하기 위해 AI를 활용한 부하 최적화, 예측 스케줄링, 실시간 감시, 클라우드 관리 플랫폼에 다액의 투자를 실시했습니다.

독일의 전기자동차 충전 부하 관리 시스템 시장은 2024년 2억 8,780만 달러 규모로 31%의 점유율을 차지했습니다. 이 나라는 강력한 산업 기반, 스마트 그리드 도입의 주도적 입장, 첨단 고출력 충전 기술을 가지고 있습니다. 독일의 주요 동향으로는 AI 기반 부하 분산, 실시간 고속 충전기 모니터링, 예측형 에너지 관리, 상용과 공공 및 플릿 충전 네트워크 전체에서의 V2G(차량에서 그리드로의 전력 공급) 통합 등을 들 수 있습니다.

전기자동차 충전 부하 관리 시스템 시장의 주요 기업으로는 Wallbox NV, Enel X, ABB, EV Connect, Eaton Corporation, Tesla, Schneider Electric SE, ChargePoint Holdings, Siemens AG, Shell Recharge Solutions 등이 있습니다. 이 시장의 기업은 시장에서의 존재감을 강화하기 위해 기술 혁신, 전략적 제휴, 지리적 확대에 주력하고 있습니다. 에너지 사용량과 부하 분산을 최적화하는 AI 구동형, 클라우드 기반, IoT 대응 솔루션의 개발을 위해 연구 개발(R&D)에 투자하고 있습니다. 전력회사, 플릿 사업자, 정부 프로그램과의 연계를 통해 시장 침투의 가속과 규제 변화에 대한 대응을 실현하고 있습니다. 기업은 인프라와 서비스 네트워크를 확대하여 접근성과 운영 효율성을 향상시키고 있습니다. 합병, 인수, 제휴는 제품 포트폴리오의 다양화, 기술력 강화, 시장 점유율 확대에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전기자동차의 보급 확대 및 차량 플릿의 확대

- 첨단 충전 인프라

- IoT 및 AI의 통합

- 전력 계통의 신뢰성 및 에너지 효율

- 업계의 잠재적 위험 및 과제

- 인프라에 대한 많은 투자

- 통합의 복잡성

- 시장 기회

- 예측형 및 원격 관리 서비스

- 지속가능성 및 순환형 경제의 대처

- 소프트웨어 구동형 및 AI 대응 솔루션

- 관민 제휴에 의한 인프라 확장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 전기차 보급 촉진을 위한 정부 정책

- 계통 연계 규칙 및 에너지 관리 기준

- 배출 감축 및 지속가능성에 관한 규제

- 안전성 및 고전압 시스템의 적합성

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 동향

- AI를 활용한 부하 최적화

- IoT를 활용한 감시 및 접속성

- 클라우드 통합형 관리 플랫폼

- 표준 기반 통신 프로토콜

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 비용 내역 분석

- 특허 분석

- 지속가능성 및 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 베스트 케이스 시나리오

- 미래 전망 및 전략적 제안

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 기술 아키텍처별(2021-2034년)

- 주요 동향

- 통합 하드웨어 및 소프트웨어 시스템

- 하드웨어 기반 부하 관리 시스템

- 소프트웨어 기반 부하 관리 시스템

제6장 시장 추계 및 예측 : 전력 관리 레벨별(2021-2034년)

- 주요 동향

- 빌딩 레벨 부하 관리

- 패널 레벨 부하 관리

- 회로 레벨 부하 관리

- 그리드 레벨 부하 관리

제7장 시장 추계 및 예측 : 통신 프로토콜별(2021-2034년)

- 주요 동향

- OCPP 기반 시스템

- ISO 15118에 기반한 시스템

- 독자적인 프로토콜 시스템

- IEEE 2030.5 기반 시스템

제8장 시장 추계 및 예측 : 출력별(2021-2034년)

- 주요 동향

- 직류 급속 충전 부하 관리(50-350kW)

- 레벨 2 AC 부하 관리(3.3-22 kW)

- 레벨 1 AC 부하 관리(1.9kW 이하)

- 메가와트급 충전 시스템의 부하 관리(1MW 초과)

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 공공 충전

- 플릿 충전

- 주택용 충전

- 기타

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- 세계 기업

- ABB

- BP Pulse

- ChargePoint Holdings

- Eaton Corporation

- Schneider Electric SE

- Shell Recharge Solutions

- Siemens AG

- Tesla

- 지역 기업

- Allego NV

- EV Connect

- EVBox(ENGIE)

- Gridserve Holdings

- gridX GmbH

- InstaVolt Limited

- SWTCH Energy

- Virta

- Wallbox

- 신흥 기업

- Ampcontrol Pty

- Bolt.Earth

- CyberSwitching

- Enphase Energy

- Wevo Energy

The Global Electric Vehicle Charging Load Management System Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 23.3% to reach USD 21.8 billion by 2034.

The market's growth is propelled by the rapid rise of electric vehicle adoption, expanding EV fleets, and the increasing requirement for intelligent energy management solutions. As charging infrastructure, grid connectivity, and energy storage systems advance, stakeholders are focusing on maximizing operational efficiency, integrating smart grid solutions, and optimizing load distribution to ensure reliable and cost-effective charging networks. The sector is moving toward connected, automated, and data-driven operations, transforming conventional approaches to energy management and redefining how charging networks are monitored and maintained. Rising investments in digital platforms, predictive energy scheduling, and AI-enabled control systems are creating opportunities for more scalable, resilient, and efficient EV charging ecosystems. The increasing deployment of IoT-connected charging stations, AI-based load balancing solutions, and cloud-enabled energy management platforms is reshaping the industry. These technologies facilitate real-time monitoring of grid demand, predictive load allocation, and seamless coordination between utilities, charging operators, and fleet managers. By leveraging smart meters, telematics, and AI analytics, operators can enhance energy efficiency, reduce peak load stress, and lower operational costs, enabling a smarter, more resilient charging network.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $21.8 Billion |

| CAGR | 23.3% |

The integrated hardware-software systems segment accounted for 37% share in 2024 and is expected to grow at a CAGR of 22.8% from 2025 to 2034. This segment is central to ensuring optimal EV charging, grid reliability, and energy efficiency by combining smart chargers, dynamic load controllers, energy storage interfaces, and communication modules into unified platforms. The rising complexity of high-voltage charging networks has increased demand for AI-driven control algorithms, advanced monitoring, and skilled operators to manage precise energy distribution.

The DC fast charging load management segment (50-350 kW) held 36% share in 2024 and is forecasted to grow at a CAGR of 23% through 2034. Growth in this segment is fueled by the deployment of high-capacity chargers, the need for reduced EV charging times, and the demand for grid-optimized, smart load balancing solutions. Operators are investing heavily in AI-powered load optimization, predictive scheduling, real-time monitoring, and cloud management platforms to enhance charger utilization, ease peak demand pressure, and improve operational efficiency.

Germany Electric Vehicle Charging Load Management System Market generated USD 287.8 million and held a 31% share in 2024. The country benefits from strong industrial capabilities, leadership in smart grid adoption, and advanced high-power charging technologies. Trends in Germany include AI-based load balancing, real-time fast charger monitoring, predictive energy management, and vehicle-to-grid (V2G) integration across commercial, public, and fleet charging networks.

Key players in the Electric Vehicle Charging Load Management System Market include Wallbox N.V., Enel X, ABB, EV Connect, Eaton Corporation, Tesla, Schneider Electric SE, ChargePoint Holdings, Siemens AG, and Shell Recharge Solutions. Companies in the Electric Vehicle Charging Load Management System Market are focusing on technological innovation, strategic partnerships, and geographic expansion to strengthen their market presence. They invest in R&D to develop AI-driven, cloud-based, and IoT-enabled solutions that optimize energy use and load distribution. Collaborations with utilities, fleet operators, and government programs allow faster market penetration and compliance with evolving regulations. Firms are expanding infrastructure and service networks to improve accessibility and operational efficiency. Mergers, acquisitions, and alliances help diversify product portfolios, enhance technological capabilities, and consolidate market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology Architecture

- 2.2.3 Power Management Level

- 2.2.4 Communication Protocol

- 2.2.5 Power Rating

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising EV adoption & fleet expansion

- 3.2.1.2 Advanced charging infrastructure

- 3.2.1.3 IoT & AI integration

- 3.2.1.4 Grid reliability & energy efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure investment

- 3.2.2.2 Complexity of integration

- 3.2.3 Market opportunities

- 3.2.3.1 Predictive & remote management services

- 3.2.3.2 Sustainability & circular economy initiatives

- 3.2.3.3 Software-driven and AI-enabled solutions

- 3.2.3.4 Public-private infrastructure expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Government policies promoting EV adoption

- 3.4.2 Grid codes and energy management standards

- 3.4.3 Emission reduction and sustainability regulations

- 3.4.4 Safety and high-voltage system compliance

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 AI-powered load optimization

- 3.7.2 IoT-enabled monitoring and connectivity

- 3.7.3 Cloud-integrated management platforms

- 3.7.4 Standards-based communication protocols

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Best case scenarios

- 3.14 Future Outlook & Strategic Recommendations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Technology Architecture, 2021 - 2034 ($ Bn)

- 5.1 Key trends

- 5.2 Integrated hardware-software system

- 5.3 Hardware-based load management system

- 5.4 Software-based load management system

Chapter 6 Market Estimates & Forecast, By Power Management Level, 2021 - 2034 ($ Bn)

- 6.1 Key trends

- 6.2 Building-level load management

- 6.3 Panel-level load management

- 6.4 Circuit-level load management

- 6.5 Grid-level load management

Chapter 7 Market Estimates & Forecast, By Communication Protocol, 2021 - 2034 ($ Bn)

- 7.1 Key trends

- 7.2 OCPP-based system

- 7.3 ISO 15118-based system

- 7.4 Proprietary protocol system

- 7.5 IEEE 2030.5-based system

Chapter 8 Market Estimates & Forecast, By Power Rating, 2021 - 2034 ($ Bn)

- 8.1 Key trends

- 8.2 DC fast charging load management (50-350 kW)

- 8.3 Level 2 ac load management (3.3-22 kW)

- 8.4 Level 1 ac load management (≤1.9 kW)

- 8.5 Megawatt charging system load management (>1 MW)

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Bn)

- 9.1 Key trends

- 9.2 Public charging

- 9.3 Fleet charging

- 9.4 Residential charging

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 ABB

- 11.1.2 BP Pulse

- 11.1.3 ChargePoint Holdings

- 11.1.4 Eaton Corporation

- 11.1.5 Schneider Electric SE

- 11.1.6 Shell Recharge Solutions

- 11.1.7 Siemens AG

- 11.1.8 Tesla

- 11.2 Regional Player

- 11.2.1 Allego N.V.

- 11.2.2 EV Connect

- 11.2.3 EVBox (ENGIE)

- 11.2.4 Gridserve Holdings

- 11.2.5 gridX GmbH

- 11.2.6 InstaVolt Limited

- 11.2.7 SWTCH Energy

- 11.2.8 Virta

- 11.2.9 Wallbox

- 11.3 Emerging Players

- 11.3.1 Ampcontrol Pty

- 11.3.2 Bolt.Earth

- 11.3.3 CyberSwitching

- 11.3.4 Enphase Energy

- 11.3.5 Wevo Energy