|

시장보고서

상품코드

1876647

트럭용 메가와트 충전 시스템 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Truck Megawatt Charging System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

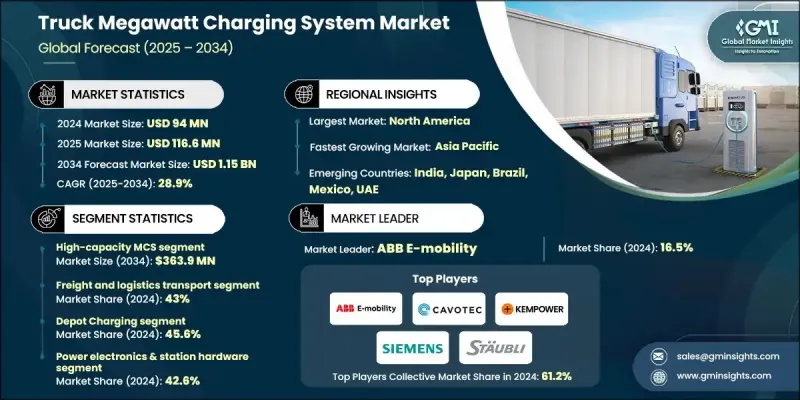

세계의 트럭용 메가와트 충전 시스템 시장은 2024년에 9,400만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 28.9%로 성장할 전망이며, 11억 5,000만 달러에 이를 것으로 예측됩니다.

전기 대형 트럭 및 산업용 운송 차량으로의 전환이 가속화되고 있는 가운데 대형 배터리 팩을 지원할 수 있는 고출력 충전 인프라에 대한 수요가 증가하고 있습니다. 메가와트 충전 시스템은 플릿의 다운타임 감소, 운영 효율성 향상, 안정적인 물류 성능 유지에 기여합니다. 사업자가 지속가능성 목표 및 장기적인 효율화 목표를 달성하기 위해 노력하면서 MCS는 상용 플릿 전동화 전략의 필수 요소가 되고 있습니다. 배출량 감축을 목적으로 한 정부 규제 및 지원적인 재정적 인센티브가 함께 MCS 인프라의 도입을 더욱 가속화하고 있습니다. 대형 차량의 전동화에 초점을 맞춘 정책 요건의 확대는 네트워크 사업자나 플릿에 공공의 고출력 충전 회랑의 도입을 촉구하고 있습니다. 액냉식 커넥터 설계, 대용량 배터리, 차세대 파워 일렉트로닉스의 진보는 메가와트급 충전의 실용성을 계속 강화하는 동시에, 전체적인 안전성을 향상시켜, 대규모 플릿 운용을 지원하는 스마트 에너지 관리 플랫폼과의 통합을 가능하게 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 9,400만 달러 |

| 예측 금액 | 11억 5,000만 달러 |

| CAGR | 28.9% |

2MW에서 4MW의 출력 범위를 제공하는 고용량 메가와트 시스템 부문은 23.5%의 점유율을 차지했으며, 2034년까지 3억 6,390만 달러에 달할 것으로 예측됩니다. 500kW에서 1MW 범위의 엔트리 레벨 MCS 솔루션은 기존의 DC 급속 충전기와 본격적인 메가와트급 스테이션 사이의 격차를 메우며, 전력 인프라에 큰 부담을 주지 않으면서 지역 및 도시의 차량군 전동화를 위한 보다 저렴한 옵션을 제공합니다. 이러한 시스템은 MCS 수요가 세계적으로 확대되고 있는 가운데 중형 차량 및 도입 초기 단계의 대형 차량에 널리 적합합니다.

화물 및 물류 용도 부문은 2024년에 43%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 30.1%로 확대가 전망됩니다. 장거리 수송, 지역 배송, 라스트 마일 배송에 있어서 차량의 전동화가 진행되고 있는 가운데, 주요 산업 회랑 전역에서의 MCS 설치 수요가 계속해서 높아지고 있습니다. 규제 기세로 사업자는 예측 가능한 화물 루트를 따라 충전소에 투자를 촉구하고 유통 허브 및 상업 운송 네트워크 전반에 걸쳐 확장 가능한 제로 방출 운송으로의 전환을 촉진하고 있습니다.

미국의 트럭용 메가와트 충전 시스템 시장은 2024년에 87.3%의 점유율을 차지하였고, 2,590만 달러의 수익을 창출했습니다. 캘리포니아는 제로 방출 정책과 인센티브 프로그램에 의해 지원되며 핵심적인 도입 기지로 남아 있습니다. 서해안의 확립된 화물 수송 인프라와 전략적 회랑 개발이 조기 도입을 지원하고, 전국적인 동향 형성에 공헌하는 것과 동시에, 전미에 있어서 상용 차량의 전동화 노력을 가속시키고 있습니다.

세계의 트럭용 메가와트 충전 시스템 시장에서 활동하는 주요 기업으로는 Milence, Siemens Smart Infrastructure, Autel Energy, ABB E-mobility, Cavotec, bp pulse, Huber Suhner, Staubli Electrical Connectors, Power Electronics, Kempower 등이 있습니다. 트럭용 메가와트 충전 시스템 시장에 참가하는 기업은 대형 차량의 요구를 충족시키기 위해 고효율 파워 모듈, 개량형 냉각 기구, 고속 충전 인터페이스 등 선진 충전 기술에 많은 투자를 하고 있습니다. 많은 기업들이 물류 사업자, 트럭 제조업체, 전력 공급사업자와 제휴하여 네트워크 확대의 가속 및 장기 도입 계약의 확보를 도모하고 있습니다. 대형 충전소 수요 증가에 대응하기 위해, 제조 능력의 확대와 비용 구조의 최적화가 여전히 핵심적인 우선 과제입니다. 또한 회사는 화물 운송 회랑을 따라 파일럿 프로그램을 확대하고 상호 운용성 기준을 강화하고 에너지 밸런싱 및 피크 부하 감소를 지원하는 스마트 그리드 관리 도구를 통합하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위 및 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별 및 국가별

- 기본 추정치 및 계산

- 기준 연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측

- 조사의 전제조건 및 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전기 트럭 도입의 확대

- 지원적인 규제 및 정부의 인센티브

- 충전 기술 및 규격의 진보

- 물류 및 화물 회랑의 확대

- OEM 및 충전 제공업체 간 협력

- 업계의 잠재적 위험 및 과제

- 높은 인프라 및 설치 비용

- 계통 용량 및 전력 공급 제약

- 시장 기회

- 재생에너지 및 스마트 그리드와의 통합

- 상호 운용 가능한 충전 네트워크 개발

- 장거리 전기화물 수송 회랑의 성장

- 산업 전화 및 항만 물류

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 데이터 프라이버시 및 규제 준수

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 동향

- 현행 기술

- 신흥 기술

- 특허 분석

- 가격 동향 분석

- 컴포넌트별

- 지역별

- 비용 내역 분석

- 생산 통계

- 생산 거점

- 소비 거점

- 수출 및 수입

- 지속가능성 및 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율화

- 환경에 배려한 대처

- 탄소발자국 고려 사항

- MCS 인프라의 투자 동향 및 자금 조달 분석

- 계통 연계 요건 및 전력 회사와의 제휴 과제

- 전망 및 시장 기회

- 시장 성장 예측 및 시나리오 분석

- 신흥 용도 및 이용 사례 개발

- 규격의 수렴 및 세계한 조화

- 계통 연계 및 스마트 충전의 진화

- 지역별 시장 성숙도 평가

- 성공적인 MCS 도입 사례의 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 뉴스 및 대처

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 출력 레벨별(2021-2034년)

- 주요 동향

- 엔트리 레벨 MCS

- 표준 MCS

- 대용량 MCS

제6장 시장 추계 및 예측 : 충전 장소별(2021-2034년)

- 주요 동향

- 디포 충전

- 고속도로 연선 충전

- 산업용 및 터미널 충전

제7장 시장 추계 및 예측 : 시스템 구성 요소별(2021-2034년)

- 주요 동향

- 커넥터 어셈블리

- 충전 케이블

- 파워 일렉트로닉스 및 변전소 하드웨어

- 열 및 안전 관리 시스템

- 소프트웨어 및 통신 모듈

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 화물 및 물류 수송

- 여객 수송

- 산업용 및 건설 차량

- 특수 이동 기기

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 플릿 사업자

- 충전 인프라 제공업체

- 자동차 제조업체(OEM)

- 에너지 및 유틸리티 및 송배전 사업자

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 네덜란드

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- ANZ

- 싱가포르

- 태국

- 베트남

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- ABB

- Eaton

- HUBER SUHNER

- Kempower

- Schneider Electric

- Siemens

- Staubli International

- Tesla

- 지역 기업

- Alpitronic

- Cavotec

- ChargePoint

- Efacec Power Solutions

- Heliox

- Hypercharger

- Milence

- Tritium DCFC

- 신흥 및 틈새 기업

- Blink Charging

- Compleo Charging Solutions

- Delta Electronics

- Electrify Commercial

- IONITY

- Phoenix Contact E-Mobility

- Wallbox

The Global Truck Megawatt Charging System Market was valued at USD 94 million in 2024 and is estimated to grow at a CAGR of 28.9% to reach USD 1.15 billion by 2034.

The transition toward electric heavy-duty trucks and industrial transport vehicles continues to accelerate, creating a growing need for high-power charging infrastructure capable of supporting large battery packs. Megawatt charging systems help fleets reduce downtime, enhance operational efficiency, and maintain reliable logistics performance. As operators work to align with sustainability targets and long-term efficiency goals, MCS is becoming an essential component of commercial fleet electrification strategies. Government regulations aimed at lowering emissions, together with supportive financial incentives, are further accelerating the deployment of MCS infrastructure. Expanded policy mandates focused on the electrification of heavy-duty vehicles are motivating network operators and fleets to introduce public high-power charging corridors. Advancements in liquid-cooled connector designs, large-capacity batteries, and next-generation power electronics continue to strengthen the viability of megawatt-level charging while improving overall safety and enabling integration with smart energy management platforms that support large fleet operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $94 Million |

| Forecast Value | $1.15 Billion |

| CAGR | 28.9% |

The high-capacity megawatt systems delivering between 2 MW and 4 MW segment held 23.5% share and is forecasted to reach USD 363.9 million by 2034. Entry-level MCS solutions ranging from 500 kW to 1 MW bridge the gap between conventional DC fast chargers and full-scale megawatt stations, offering a more affordable path for regional and urban fleet electrification without imposing significant strain on power infrastructure. These systems are widely suited for medium-duty and early-stage heavy-duty vehicle adoption as MCS demand evolves globally.

The freight and logistics applications segment held a 43% share in 2024 and is expected to grow at a CAGR of 30.1% through 2034. Electrification of long-haul, regional distribution, and last-mile fleets continues to drive the need for MCS installations across major industrial corridors. Regulatory momentum is pushing operators to invest in charging stations along predictable freight routes, advancing the shift toward scalable zero-emission transportation across distribution hubs and commercial transport networks.

US Truck Megawatt Charging System Market held a 87.3% share in 2024, generating USD 25.9 million. California remains a core deployment center supported by zero-emission policies and incentive programs. The West Coast's established freight infrastructure and strategic corridor development support early adoption, helping shape national trends and accelerating commercial fleet electrification efforts across the country.

Major players active in the Global Truck Megawatt Charging System Market include Milence, Siemens Smart Infrastructure, Autel Energy, ABB E-mobility, Cavotec, bp pulse, Huber+Suhner, Staubli Electrical Connectors, Power Electronics, and Kempower. Companies participating in the truck megawatt charging system market are investing heavily in advanced charging technologies, including high-efficiency power modules, improved cooling mechanisms, and faster charging interfaces to support heavy-duty fleet requirements. Many firms are forming partnerships with logistics operators, truck manufacturers, and utility providers to accelerate network expansion and secure long-term deployment agreements. Scaling manufacturing capacity and optimizing cost structures remain core priorities to meet rising demand for large-format charging stations. Businesses are also expanding pilot programs along freight corridors, enhancing interoperability standards, and integrating smart-grid management tools to support energy balancing and peak-load reduction.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Power level

- 2.2.2 Charging location

- 2.2.3 System component

- 2.2.4 Application

- 2.2.5 End Use

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in electric truck adoption

- 3.2.1.2 Supportive regulations and government incentives

- 3.2.1.3 Advancements in charging technology and standards

- 3.2.1.4 Expansion of logistics and freight corridors

- 3.2.1.5 Collaboration between OEMs and charging providers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure and installation costs

- 3.2.2.2 Grid capacity and power availability constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with renewable energy and smart grids

- 3.2.3.2 Development of interoperable charging networks

- 3.2.3.3 Growth in long-haul electric freight corridors

- 3.2.3.4 Industrial electrification and port logistics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle east and Africa

- 3.4.6 Data Privacy & Regulatory Compliance

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Patent analysis

- 3.9 Price Trends Analysis

- 3.9.1 By component

- 3.9.2 By region

- 3.10 Cost Breakdown Analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Investment flows & funding analysis in MCS infrastructure

- 3.14 Grid integration requirements & utility coordination challenges

- 3.15 Future outlook and market opportunities

- 3.15.1 Market growth projections & scenario analysis

- 3.15.2 Emerging applications & use case development

- 3.15.3 Standards convergence & global harmonization

- 3.15.4 Grid integration & smart charging evolution

- 3.16 Market maturity assessment by geographic region

- 3.17 Case study analysis of successful MCS deployments

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Power level, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Entry-level MCS

- 5.3 Standard MCS

- 5.4 High-capacity MCS

Chapter 6 Market Estimates & Forecast, By Charging location, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Depot charging

- 6.3 Highway corridor charging

- 6.4 Industrial/terminal charging

Chapter 7 Market Estimates & Forecast, By System component, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Connector assembly

- 7.3 Charging cable

- 7.4 Power electronics & station hardware

- 7.5 Thermal and safety management system

- 7.6 Software & communication module

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Freight and logistics transport

- 8.3 Passenger transport

- 8.4 Industrial and construction vehicles

- 8.5 Specialized mobility equipment

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Fleet operators

- 9.3 Charging infrastructure providers

- 9.4 Vehicle OEM

- 9.5 Energy utilities & grid operators

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Netherlands

- 10.3.8 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 ANZ

- 10.4.5 Singapore

- 10.4.6 Thailand

- 10.4.7 Vietnam

- 10.4.8 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ABB

- 11.1.2 Eaton

- 11.1.3 HUBER+SUHNER

- 11.1.4 Kempower

- 11.1.5 Schneider Electric

- 11.1.6 Siemens

- 11.1.7 Staubli International

- 11.1.8 Tesla

- 11.2 Regional Players

- 11.2.1 Alpitronic

- 11.2.2 Cavotec

- 11.2.3 ChargePoint

- 11.2.4 Efacec Power Solutions

- 11.2.5 Heliox

- 11.2.6 Hypercharger

- 11.2.7 Milence

- 11.2.8 Tritium DCFC

- 11.3 Emerging & Niche Players

- 11.3.1 Blink Charging

- 11.3.2 Compleo Charging Solutions

- 11.3.3 Delta Electronics

- 11.3.4 Electrify Commercial

- 11.3.5 IONITY

- 11.3.6 Phoenix Contact E-Mobility

- 11.3.7 Wallbox