|

시장보고서

상품코드

1876650

선내 보트 엔진 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Inboard Boat Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

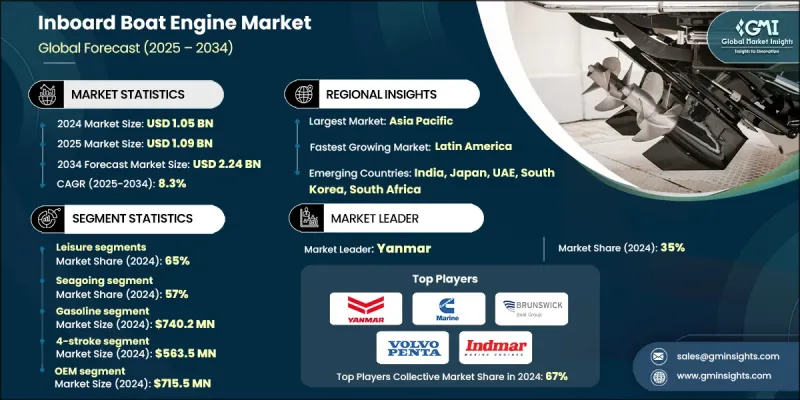

세계의 선내 보트 엔진 시장은 2024년에 10억 5,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.3%로 성장할 전망이며, 22억 4,000만 달러에 이를 것으로 예측되고 있습니다.

세계적인 레크리에이션 보트, 고급 수상정, 해양 관광의 인기에 의해 시장은 확대를 계속하고 있습니다. 토크 향상, 연비 효율화, 배출 가스 삭감을 실현한 고성능 엔진에 대한 소비자 수요의 고조에 따라, 제조업체 각사는 연료 분사식이나 하이브리드 파워트레인을 포함한 선진 추진 기술의 개발을 추진하고 있습니다. 워터 스포츠, 고급 요트, 순시정에 대한 관심의 고조에 더해, 소득 향상에 의한 정기적인 선대 갱신 사이클이 더해져, 엔진의 채용을 한층 더 촉진하고 있습니다. 배출 가스 규제의 강화에 의해 구식 엔진의 교환 및 갱신이 가속되고 있으며, 특히 배출가스 규제 구역(ECA)에서는 규제 적합형 선내 엔진의 안정된 시장이 확보되고 있습니다. 계절성도 수요에 영향을 미치고 있으며, 봄의 취항 준비 및 가을의 월동 준비에 의해 엔진 설치, 유지관리, 수리 서비스 수요가 피크를 맞이합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 10억 5,000만 달러 |

| 예측 금액 | 22억 4,000만 달러 |

| CAGR | 8.3% |

외항 부문은 57%의 점유율을 차지하며, 2034년까지 연평균 복합 성장률(CAGR) 7.5%로 성장할 것으로 예측됩니다. 외항용 선내 엔진은 고속 레크리에이션 보트에서 대형 상업선까지 다양한 선박 유형에 대응하고 있으며, 해수 사용, 장거리 항행, 국제 해사 기준에 적합하도록 최적화된 엔진이 요구됩니다.

레저 분야는 2024년에 65%의 점유율을 차지했으며, 2025-2034년 CAGR 8%로 성장할 것으로 예측됩니다. 하천, 호수 및 운하에 있어서 내륙 레저 활동이, 얕은 항행 대응, 환경 지속가능성 및 레저 선박 시스템과의 제휴를 특징으로 하는 엔진 수요를 견인하고 있습니다. 본 분야에서는 기존 연소 시스템을 넘은 보다 환경에 배려한 추진 기술에 있어서 혁신이 촉진되고 있습니다.

아시아태평양의 선내 보트 엔진 시장은 2024년에 32.5%의 점유율을 차지했으며, 2025-2034년 9.1%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측됩니다. 중국, 일본, 한국 등의 국가들은 세계의 선박용 엔진 생산을 지배하고 있으며, 많은 새로운 선내 추진 유닛을 생산하고 세계 엔진 공급에 크게 기여하고 있습니다.

세계 선내기 보트 엔진 시장의 주요 기업으로는 Indmar, Chris-Craft, Yanmar, PCM Engines, Perkins Marine, Volvo Penta, Pleasurecraft, Cumins Marine, Brunswick 등이 있습니다. 선내 보트 엔진 분야의 기업들은 그 존재감을 강화하기 위해 연료효율, 토크 출력, 배출 가스 규제에 대한 적합성을 개선하기 위한 연구개발에 투자하고 있습니다. 각 회사는 진화하는 소비자 및 규제의 요구에 부응하기 위해 하이브리드 시스템과 연료 분사 시스템과 같은 첨단 추진 기술을 채택하고 있습니다. 보트 제조업체와 서비스 제공업체와의 전략적 제휴는 유통 네트워크 및 애프터마켓 서비스의 확대에 기여하고 있습니다. 또한 환경 친화적인 엔진 설계 등 지속가능성에 대한 노력에도 주력하고 해양관광 및 레크리에이션용 보트 동향의 고조를 살리기 위해 신흥 시장에도 진출하고 있습니다. 마케팅 캠페인, 고객 교육, 레저 및 외항 부문으로 제품을 다양화함으로써 브랜드 인지도와 경쟁력이 더욱 높아지고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 엔진 제조업체

- 선박 제조업체

- 리셀러

- 애프터마켓 서비스 제공업체님

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 기술 혁신의 요인

- 공급망의 취약성 요인

- 디스랩터

- 기술 주도의 변화

- 대체 연료에 의한 변혁

- 디지털 전환에 의한 변혁

- 공급자의 상황

- 영향 요인

- 성장 촉진요인

- 레크리에이션 보트 활동 증가

- 요트 생산 및 판매 증가

- 상업 해운 사업의 성장

- 성장을 계속하는 관광 분야

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용

- 유지보수 및 운영 상의 복잡성

- 시장 기회

- 성장의 촉매 및 시장 가속 요인

- 계절적인 수요 패턴 및 주기적인 동향

- 성장 촉진요인

- 기술 동향 및 혁신, 에코시스템

- 현행 기술

- 엔진 성능의 동향

- 연료 효율 요건

- 신흥 기술

- 하이브리드 및 전기 구동 시스템의 통합

- 대체 연료 및 멀티 연료 엔진

- 디지털화, IoT 및 예측 분석

- 재료 혁신 및 적층 조형 기술

- 규제 주도의 기술 적응

- 현행 기술

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 가격 설정 : 부문별

- 추진 시스템

- 지역

- 프리미엄 가격 전략 및 그 근거

- 밸류체인 전체에 있어서 코스트 구조 분석

- 용도별 및 지역별 가격 감응도

- 가격 설정 : 부문별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출 및 수입

- 비용 내역 분석

- 설비 투자(Capex) : 엔진, 설치 및 부속품

- 유지 보수 및 수명주기 비용

- 규제 준수 및 인증 비용

- 자금 조달, 감가 상각 및 라이프 사이클 관리

- 용도별 비교 비용 구조

- 주요 비용 요인 및 감응도

- 특허 분석

- 특허 상황의 개요

- 특허출원전략 및 경쟁 환경

- 최근 특허출원-기술 및 OEM 일람표

- 혁신의 거점 및 기술 클러스터

- 전략적 시사

- 지역별 및 기술별 특허 출원 동향(2019-2024년)

- 특허의 절벽 및 전망

- 지속가능성 및 환경면

- 물리적 프로토타입 및 테스트 감소

- 에너지 효율 향상

- 전동화 및 배출 감축 기술에 대한 지원

- 라이프사이클 및 전자폐기물 관리

- 환경 규제에 대한 적합

- 이용 사례

- 도시형 여객 페리용 하이브리드 추진 시스템

- 상용 작업선용 예지 보전

- 슈퍼 요트에 있어서 프리미엄 윤활유 도입

- 에코 투어리즘선용 전동선내기

- 해외 지원선의 규제 적합을 위한 개조

- 베스트 케이스 시나리오(상세판)

- 도시 수로의 완전 전동화

- 세계 선대 전체에 걸친 예지보전 네트워크

- 선박 추진 시스템의 순환형 경제

- 규제 주도에 의한 시장 변혁

- 선박 설계 및 운항에 있어서 디지털 트윈의 통합

- 제품 로드맵의 틀(확장판)

- 혁신 요건 분석

- 규제 주도의 제품 개발

- 성능 향상의 기회

- 지속가능성 및 바이오 솔루션

- 프리미엄 제품 라인 확장

- 바이오 베이스 및 지속 가능한 선박용 윤활유

- 지속가능성 및 바이오 솔루션 로드맵

- 단기(1-3년)

- 중기(3-7년)

- 장기(7-15년)

- 고성능 선박 엔진 용도

- 전략적 시사

- OEM 및 공급자용

- 오퍼레이터 및 플릿 관리자용

- 정책 입안자 및 투자자용

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 확대 계획 및 자금 조달

- 프리미엄 포지셔닝 전략

- 전략적 OEM 파트너십 기회

- 기술 기준 및 인증 요건

- 전략적 시장 기회

- 프리미엄 포지셔닝 전략

- 기술 제휴의 기회

- 지역적 확대의 우선순위

- 제품 포트폴리오의 갭 분석

- 유통 채널 최적화

제5장 시장 추계 및 예측 : 수운별(2021-2034년)

- 주요 동향

- 외항

- 내륙

제6장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 가솔린

- 디젤

- 전기식

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 레저

- 화물 수송

- 여객 수송

- 어업

- 정부기관용

제8장 시장 추계 및 예측 : 엔진별(2021-2034년)

- 주요 동향

- 2스트로크

- 4스트로크

- 전기자동차

제9장 시장 추계 및 예측 : 출력별(2021-2034년)

- 주요 동향

- 저출력

- 중출력

- 고출력

제10장 시장 추계 및 예측 : 이그니션별(2021-2034년)

- 주요 동향

- 전기자동차

- 매뉴얼

제11장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제12장 시장 추계 및 예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제13장 기업 프로파일

- 세계 기업

- Caterpillar

- Cummins

- Volvo Penta

- Yanmar

- MAN Energy Solutions

- MTU(Rolls-Royce Power Systems)

- Wartsila

- Mercury Marine(Brunswick)

- Hyundai Heavy Industries

- Mitsubishi Heavy Industries

- Scania

- FPT Industrial

- Deutz

- General Motors

- Ilmor Engineering

- Steyr Motors

- 지역 제조업체

- Beta Marine

- Nanni Industries

- Moteurs Baudouin

- Northern Lights

- Westerbeke

- Indmar Products

- PCM(Pleasurecraft Marine)

- Marine Power

- Fairbanks Morse Defense

- VM Motori

- Daihatsu Diesel

- Niigata Power Systems

- Doosan Infracore

- 신흥 제조업체

- Weichai Power

- Yuchai(Guangxi Yuchai Machinery)

- OXE Marine

The Global Inboard Boat Engine Market was valued at USD 1.05 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 2.24 billion by 2034.

The market is expanding owing to the growing popularity of recreational boating, luxury watercraft, and marine tourism worldwide. Rising consumer demand for high-performance engines with improved torque, fuel efficiency, and reduced emissions is driving manufacturers to develop advanced propulsion technologies, including fuel-injected and hybrid powertrains. Increasing interest in water sports, luxury yachts, and patrol vessels, combined with consistent fleet renewal cycles fueled by higher incomes, is further boosting engine adoption. Regulatory frameworks enforcing stricter emission standards are accelerating the replacement and upgrading of older engines, ensuring a stable market for compliant inboard systems, particularly in designated Emission Control Areas. Seasonality plays a role in demand, with spring commissioning and fall winterization creating peaks in engine installations, maintenance, and repair services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.05 Billion |

| Forecast Value | $2.24 Billion |

| CAGR | 8.3% |

The seagoing segment held a 57% share and is expected to grow at a CAGR of 7.5% through 2034. Seagoing inboard engines cater to diverse vessel types, ranging from high-speed recreational boats to large commercial ships, requiring engines optimized for saltwater use, extended trip durations, and compliance with international maritime standards.

The leisure segment held a 65% share in 2024 and is projected to grow at a CAGR of 8% from 2025 to 2034. Inland leisure activities on rivers, lakes, and canals are driving demand for engines designed for shallow water operations, environmental sustainability, and connectivity with recreational vessel systems. This segment is fostering innovation in greener propulsion technologies that go beyond conventional combustion systems.

Asia-Pacific Inboard Boat Engine Market accounted for a 32.5% share in 2024 and is expected to grow at a CAGR of 9.1% between 2025 and 2034. Countries such as China, Japan, and South Korea dominate global marine engine production, producing many new inboard propulsion units and contributing significantly to the worldwide engine supply.

Key players in the Global Inboard Boat Engine Market include Indmar, Chris-Craft, Yanmar, PCM Engines, Perkins Marine, Volvo Penta, Pleasurecraft, Cummins Marine, and Brunswick. To strengthen their presence, companies in the inboard boat engine sector are investing in research and development to improve fuel efficiency, torque output, and emission compliance. Firms are adopting advanced propulsion technologies, including hybrid and fuel-injected systems, to meet evolving consumer and regulatory demands. Strategic partnerships with boat manufacturers and service providers help expand distribution networks and aftermarket services. Companies are also focusing on sustainability initiatives, including environmentally friendly engine designs, and entering emerging markets to capitalize on rising marine tourism and recreational boating trends. Marketing campaigns, customer education, and product diversification into leisure and seagoing segments further enhance brand visibility and competitive positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast

- 1.4 Primary research and validation

- 1.5 Some of the primary sources

- 1.6 Data mining sources

- 1.6.1 Secondary

- 1.6.1.1 Paid Sources

- 1.6.1.2 Public Sources

- 1.6.1.3 Sources, by region

- 1.6.1 Secondary

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Waterways

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 Engine

- 2.2.6 Power

- 2.2.7 Ignition

- 2.2.8 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Engine manufacturers

- 3.1.1.2 Boat manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 Aftermarket service providers

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.5.1 Technology disruption factors

- 3.1.5.2 Supply chain vulnerability factors

- 3.1.6 Disruptors

- 3.1.6.1 Technology-driven disruptions

- 3.1.6.2 Alternative fuel disruptions

- 3.1.6.3 Digital transformation disruptions

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing recreational boating activities

- 3.2.1.2 Rising production and sales of yachts

- 3.2.1.3 Growth in commercial maritime operations

- 3.2.1.4 Growing tourism sector

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost

- 3.2.2.2 Maintenance and operational complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Growth catalysts and market accelerators

- 3.2.3.2 Seasonal demand patterns and cyclical trends

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Engine performance trends

- 3.3.1.2 Fuel efficiency requirements

- 3.3.2 Emerging technologies

- 3.3.2.1 Hybrid and electric integration

- 3.3.2.2 Alternative fuels and multi-fuel engines

- 3.3.2.3 Digitalization, IoT, and predictive analytics

- 3.3.2.4 Materials innovation and additive manufacturing

- 3.3.2.5 Regulatory-driven technology adaptation

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Price trends

- 3.8.1 Pricing, by segment

- 3.8.1.1 Propulsion

- 3.8.1.2 Region

- 3.8.2 Premium pricing strategies and justification

- 3.8.3 Cost structure analysis across value chain

- 3.8.4 Price sensitivity by application and region

- 3.8.1 Pricing, by segment

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Capital expenditure (Capex): Engine, installation & ancillaries

- 3.10.2 Maintenance & lifecycle costs

- 3.10.3 Regulatory compliance & certification costs

- 3.10.4 Financing, depreciation & lifecycle management

- 3.10.5 Comparative cost structure by application

- 3.10.6 Key cost drivers & sensitivities

- 3.11 Patent analysis

- 3.11.1 Patent landscape overview

- 3.11.2 Patent filing strategies & competitive dynamics

- 3.11.3 Recent patent filings - technology & OEM table

- 3.11.4 Innovation hotspots & technology clusters

- 3.11.5 Strategic implications

- 3.11.6 Patent filing trends by region & technology (2019-2024)

- 3.11.7 Patent cliff & future outlook

- 3.12 Sustainability and environmental aspects

- 3.12.1 Reducing physical prototyping and testing

- 3.12.2 Energy efficiency improvements

- 3.12.3 Support for electrification and emission reduction technologies

- 3.12.4 Lifecycle and e-waste management

- 3.12.5 Compliance with environmental regulations

- 3.13 Use cases

- 3.13.1 Hybrid propulsion for urban passenger ferries

- 3.13.2 Predictive maintenance for commercial workboats

- 3.13.3 Premium lubricant adoption in superyachts

- 3.13.4 Electric inboard engines for eco-tourism boats

- 3.13.5 Retrofit for compliance with offshore support vessels

- 3.14 Best case scenarios (expanded)

- 3.14.1 Full electrification of urban waterways

- 3.14.2 Predictive maintenance network across global fleets

- 3.14.3 Circular economy for marine propulsion

- 3.14.4 Regulatory-driven market transformation

- 3.14.5 Digital twin integration in vessel design and operations

- 3.15 Product roadmap framework (expanded)

- 3.15.1 Innovation requirements analysis

- 3.15.2 Regulatory-driven product development

- 3.15.3 Performance enhancement opportunities

- 3.15.4 Sustainability and bio-based solutions

- 3.15.5 Premium product line extensions

- 3.15.6 Bio-based and sustainable marine lubricants

- 3.15.7 Sustainability and bio-based solutions roadmap

- 3.15.7.1 Short-term (1-3 years)

- 3.15.7.2 Medium-term (3-7 years)

- 3.15.7.3 Long-term (7-15 years)

- 3.16 High-performance marine engine applications

- 3.17 Strategic implications

- 3.17.1 For OEMs and suppliers

- 3.17.2 For operators and fleet managers

- 3.17.3 For policymakers and investors

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Premium positioning strategies

- 4.7 Strategic OEM partnership opportunities

- 4.8 Technical standards and certification requirements

- 4.9 Strategic market opportunities

- 4.9.1 Premium positioning strategies

- 4.9.2 Technology partnership opportunities

- 4.9.3 Geographic expansion priorities

- 4.9.4 Product portfolio gap analysis

- 4.9.5 Distribution channel optimization

Chapter 5 Market Estimates & Forecast, By Waterways, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Seagoing

- 5.3 Inland

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Leisure

- 7.3 Transport of goods

- 7.4 Transport of people

- 7.5 Fishing

- 7.6 Government use

Chapter 8 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 2-stroke

- 8.3 4-stroke

- 8.4 Electric

Chapter 9 Market Estimates & Forecast, By Power, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Mid

- 9.4 High

Chapter 10 Market Estimates & Forecast, By Ignition, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 Electric

- 10.3 Manual

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 12.1 North America

- 12.1.1 US

- 12.1.2 Canada

- 12.2 Europe

- 12.2.1 UK

- 12.2.2 Germany

- 12.2.3 France

- 12.2.4 Italy

- 12.2.5 Spain

- 12.2.6 Russia

- 12.2.7 Belgium

- 12.2.8 Netherlands

- 12.2.9 Sweden

- 12.3 Asia Pacific

- 12.3.1 China

- 12.3.2 India

- 12.3.3 Japan

- 12.3.4 Australia

- 12.3.5 Singapore

- 12.3.6 South Korea

- 12.3.7 Vietnam

- 12.3.8 Indonesia

- 12.4 Latin America

- 12.4.1 Brazil

- 12.4.2 Mexico

- 12.4.3 Argentina

- 12.5 MEA

- 12.5.1 South Africa

- 12.5.2 Saudi Arabia

- 12.5.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 Caterpillar

- 13.1.2 Cummins

- 13.1.3 Volvo Penta

- 13.1.4 Yanmar

- 13.1.5 MAN Energy Solutions

- 13.1.6 MTU (Rolls-Royce Power Systems)

- 13.1.7 Wartsila

- 13.1.8 Mercury Marine (Brunswick)

- 13.1.9 Hyundai Heavy Industries

- 13.1.10 Mitsubishi Heavy Industries

- 13.1.11 Scania

- 13.1.12 FPT Industrial

- 13.1.13 Deutz

- 13.1.14 General Motors

- 13.1.15 Ilmor Engineering

- 13.1.16 Steyr Motors

- 13.2 Regional Players

- 13.2.1 Beta Marine

- 13.2.2 Nanni Industries

- 13.2.3 Moteurs Baudouin

- 13.2.4 Northern Lights

- 13.2.5 Westerbeke

- 13.2.6 Indmar Products

- 13.2.7 PCM (Pleasurecraft Marine)

- 13.2.8 Marine Power

- 13.2.9 Fairbanks Morse Defense

- 13.2.10 VM Motori

- 13.2.11 Daihatsu Diesel

- 13.2.12 Niigata Power Systems

- 13.2.13 Doosan Infracore

- 13.3 Emerging players

- 13.3.1 Weichai Power

- 13.3.2 Yuchai (Guangxi Yuchai Machinery)

- 13.3.3 OXE Marine