|

시장보고서

상품코드

1876657

용제 회수 시스템 시장 : 시장 비즈니스 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Solvent Recovery Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

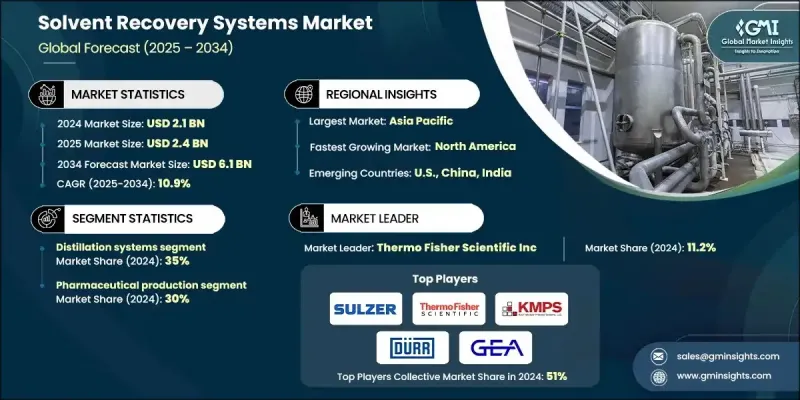

세계의 용제 회수 시스템 시장은 2024년 21억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 10.9%로 성장할 전망이며, 61억 달러에 이를 것으로 예측됩니다.

이러한 견조한 성장 전망은 산업이 지속가능한 운영, 보다 엄격한 환경 관리, 생산 효율 향상으로 빠르게 전환하고 있음을 보여줍니다. 세계 규제 당국은 휘발성 유기 화합물(VOC) 배출량과 유해 폐기물에 대한 엄격한 제한을 계속 시행하고 있으며, 기업이 용제를 폐기하는 대신 회수하는 솔루션의 도입을 촉진하고 있습니다. 지역 및 국가 차원의 환경 규제 프레임 워크에서 컴플라이언스 요구가 증가함에 따라 제조업체는 고성능 회수 시스템에 대한 투자를 추진하는 요인이 되었습니다. 동시에 이러한 솔루션은 상당한 비용 이점을 제공하여 기업이 용제 구매 비용 및 폐기물 관리 비용을 최대 50%까지 절감할 수 있도록 합니다. 또한, 일반적인 투자 회수 기간은 2년 이내에 달성되는 경우가 많습니다. 멤브레인 기술을 이용한 보다 첨단 회수 기술은 기존의 증류법에 비해 에너지 사용량과 자본 지출을 최대 40% 절감하는 기타 혜택을 제공합니다. 산업이 순환 자원 사용에 더 중점을 두는 동안, 용제 회수 시스템은 사업 계획 및 장기 지속가능성 목표의 중요한 요소가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 21억 달러 |

| 예측 금액 | 61억 달러 |

| CAGR | 10.9% |

진공 증류 기술 부문은 고온에서 열화되는 용제에 효과적이기 때문에 2024년에는 25%의 점유율을 차지했습니다. 이 시스템은 감압 하에서 작동하여 용제의 품질을 보호하면서 낮은 온도에서 분리할 수 있습니다. 그 효율은 일반적으로 90-95%에 달하며 엄격한 관리 기준을 필요로 하는 용도에 적합한 순도 수준을 제공합니다.

의약품 제조 부문은 2024년 30%의 점유율을 차지했습니다. 이것은 엄격한 순도 요구 사항과 적절한 제조 규범(GMP) 가이드 라인에 대한 흔들림없는 준수를 배경으로 합니다. 많은 시설에서는 활성 성분의 생산을 지원하기 위해 99% 이상의 순도 수준을 달성할 수 있는 회수 시스템이 필요하며, 이는 진공 증류 및 유기 용제 나노 여과 기술의 채택을 촉진하고 있습니다. 이 시스템은 제품의 무결성을 보호하면서 용제 재사용을 극대화합니다. 또한 종합적인 프로세스 추적을 의무화하는 엄격한 규제 요건에 대응하기 위해 문서화 기능을 내장한 자동화 설비도 필수가 되고 있습니다.

미국의 용제 회수 시스템 시장은 2024년에 3억 2,320만 달러의 규모를 기록했으며, 2034년까지 9억 3,000만 달러에 이를 것으로 예측됩니다. 북미는 2024년에 19.8%의 점유율을 차지했으며, 이는 미국 환경보호청(EPA)의 엄격한 지침과 산업의 지속가능성에 대한 노력 강화에 뒷받침되고 있습니다. 휘발성 유기화합물(VOC) 배출을 줄이기 위한 연방규제로 많은 제조 분야에서 시스템 도입이 가속화되고 있습니다. 주요 지역에서 제약 부문이 확대됨에 따라 GMP 및 FDA 요건에 부합하는 회수 솔루션에 대한 수요는 지속적으로 높아 시장 전체의 성장을 추진하고 있습니다.

용제 회수 시스템 시장에 참여하는 주요 기업으로는 Maratek Environmental, Thermo Fisher Scientific, Durr Group, Spooner AMCEC, Sulzer, Hydrite Chemical, HongYi Environmental Equipment, CBG Biotech, Koch Modular Process Systems, OFRU Recycling, GEA Group 등이 있습니다. 이 시장의 기업은 경쟁력 강화를 위해 여러 핵심 전략에 주력하고 있습니다. 많은 기업들이 에너지 효율 향상, 운영 비용 절감, 고순도 회수가 필요한 섬세한 용도에 대응할 수 있는 첨단 분리 기술에 많은 투자를 하고 있습니다. 또한 다양한 산업의 요구에 부응하기 위해 모듈식으로 사용자 정의 가능한 시스템 설계에 주력하고 있습니다. 세계 제조 능력 확대 및 지역 서비스 네트워크 구축은 리드 타임 단축과 고객 지원 강화에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력 관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 규모 및 예측 : 프로세스별(2021-2034년)

- 주요 동향

- 증류 시스템

- 진공 증류 시스템

- 막 분리 시스템

- 마이크로파 증강 회수 시스템

- 흡착 시스템

제6장 시장 규모 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 자동차 제조

- 도장 공장 및 코팅 작업

- 부품 세정 및 탈지

- 조립 공정에 있어서 용제의 혼합 및 재활용

- 배터리 제조(전기자동차 및 하이브리드 자동차용)

- 기타

- 의약품 제조

- 의약품 원약(API) 제조

- 실험실용 용제 회수

- 기타

- 인쇄 및 포장

- 플렉소 인쇄

- 그라비아 인쇄

- 평판 인쇄

- 기타

- 전자기기 제조

- 프린트 기판의 제조 및 세정

- 반도체 웨이퍼 가공

- 기타

- 항공우주 및 방위

- 복합 재료의 제조

- 표면 처리 및 전처리

- 보수, 수리 및 오버홀(MRO)

- 기타

- 화학 처리

- 기타

제7장 시장 규모 및 예측 : 설치 유형별(2021-2034년)

- 주요 동향

- 현장 시스템

- 오프사이트 시스템

제8장 시장 규모 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Sulzer

- Thermo Fisher Scientific

- Koch Modular Process Systems

- Durr Group

- GEA Group

- Hydrite Chemical

- Maratek Environmental

- OFRU Recycling

- HongYi Environmental Equipment

- Spooner AMCEC

- CBG Biotech

- NexGen Enviro Systems

- TruSteel

- CleanPlanet Chemical

- Progressive Recovery

The Global Solvent Recovery Systems Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 10.9% to reach USD 6.1 billion by 2034.

The strong growth outlook shows how quickly industries are moving toward sustainable operations, stricter environmental management, and improved production efficiency. Regulatory bodies worldwide continue enforcing aggressive limits on VOC emissions and hazardous waste, encouraging companies to adopt solutions that recover solvents rather than dispose of them. Increasing compliance demands under regional and national environmental frameworks have pushed manufacturers to invest in high-performance recovery systems. At the same time, these solutions deliver major cost advantages, enabling companies to reduce their solvent purchasing and waste management spending by up to 50%, with typical payback times often occurring within two years. More advanced recovery technologies using membranes now offer additional benefits, cutting energy use and capital expenses by as much as 40% compared with traditional distillation. As industries place greater emphasis on circular resource usage, solvent recovery systems are becoming an essential part of operational planning and long-term sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 10.9% |

The vacuum distillation technologies segment accounted for a 25% share in 2024, as they are effective for solvents that degrade under high heat. These systems operate under reduced pressure, allowing separation at lower temperatures while protecting solvent quality. Their efficiency ratings commonly reach 90-95%, providing purity levels suited for applications that require stringent control standards.

The pharmaceutical manufacturing segment held a 30% share in 2024, driven by demanding purity expectations and unwavering adherence to Good Manufacturing Practice guidelines. Many facilities require recovery systems capable of achieving purity levels above 99% to support active ingredient production, which fuels the adoption of vacuum distillation and organic solvent nanofiltration technologies. These systems safeguard product integrity while maximizing solvent reuse. Automated equipment with built-in documentation capabilities is also becoming essential as companies follow strict regulatory mandates that require comprehensive process tracking.

U.S. Solvent Recovery Systems Market generated USD 323.2 million in 2024 and is projected to reach USD 930 million by 2034. North America held a 19.8% share in 2024, supported by tougher EPA directives and a growing commitment to industrial sustainability. Federal regulations designed to reduce VOC emissions continue to accelerate system installations across many manufacturing segments. As the pharmaceutical sector expands in key regions, demand for recovery solutions that align with GMP and FDA expectations remains high, strengthening overall market growth.

Key companies participating in the Solvent Recovery Systems Market include Maratek Environmental, Thermo Fisher Scientific, Durr Group, Spooner AMCEC, Sulzer, Hydrite Chemical, HongYi Environmental Equipment, CBG Biotech, Koch Modular Process Systems, OFRU Recycling, and GEA Group. Companies in the Solvent Recovery Systems Market rely on several core strategies to expand their competitive standing. Many invest heavily in advanced separation technologies that improve energy efficiency, reduce operating costs, and support high-purity recovery for sensitive applications. Firms also focus on modular and customizable system designs to meet the needs of diverse industries. Expanding global manufacturing capability and building regional service networks help shorten lead times and strengthen customer support.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Process type

- 2.2.2 Application

- 2.2.3 Installation type

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Process Type, 2021-2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Distillation systems

- 5.3 Vacuum distillation systems

- 5.4 Membrane separation systems

- 5.5 Microwave-enhanced recovery systems

- 5.6 Adsorption systems

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Automotive manufacturing

- 6.2.1 Paint shop & coating operations

- 6.2.2 Parts cleaning & degreasing

- 6.2.3 Solvent blending & recycling in assembly

- 6.2.4 Battery manufacturing (EVs & hybrids)

- 6.2.5 Others

- 6.3 Pharmaceutical production

- 6.3.1 Active pharmaceutical ingredient (API) manufacturing

- 6.3.2 Laboratory solvent recovery

- 6.3.3 Others

- 6.4 Printing & packaging

- 6.4.1 Flexographic printing

- 6.4.2 Gravure printing

- 6.4.3 Lithographic printing

- 6.4.4 Others

- 6.5 Electronics manufacturing

- 6.5.1 PCB manufacturing & cleaning

- 6.5.2 Semiconductor wafer processing

- 6.5.3 Others

- 6.6 Aerospace & defense

- 6.6.1 Composite material fabrication

- 6.6.2 Surface treatment & preparation

- 6.6.3 Maintenance, repair & overhaul (MRO)

- 6.6.4 Others

- 6.7 Chemical processing

- 6.7.1 Others

Chapter 7 Market Size and Forecast, By Installation Type, 2021-2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 On-site systems

- 7.3 Off-site systems

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Sulzer

- 9.2 Thermo Fisher Scientific

- 9.3 Koch Modular Process Systems

- 9.4 Durr Group

- 9.5 GEA Group

- 9.6 Hydrite Chemical

- 9.7 Maratek Environmental

- 9.8 OFRU Recycling

- 9.9 HongYi Environmental Equipment

- 9.10 Spooner AMCEC

- 9.11 CBG Biotech

- 9.12 NexGen Enviro Systems

- 9.13 TruSteel

- 9.14 CleanPlanet Chemical

- 9.15 Progressive Recovery