|

시장보고서

상품코드

1876788

디지털 병리학 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Digital Pathology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

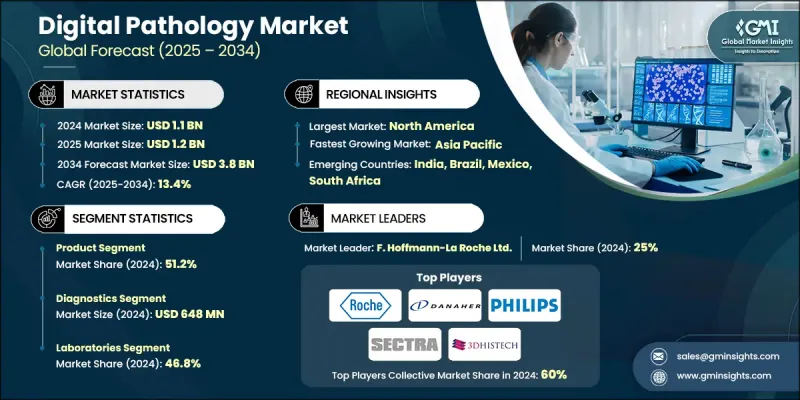

세계의 디지털 병리학 시장은 2024년 11억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 13.4%로 성장할 전망이며, 38억 달러에 이를 것으로 예측됩니다.

이러한 성장은 디지털 솔루션의 도입 확대, 진단 인프라의 현대화, 전자 건강 기록(EHR)과의 통합, 창약 및 동반자 진단에서의 이용 증가에 의해 추진되고 있습니다. 디지털 병리학은 디지털 이미징 기술을 사용하여 병리학 슬라이드 및 관련 데이터를 스캔, 분석 및 관리하는 기술입니다. 이를 통해 원격 진단, AI 지원을 통한 해석, 원활한 EHR 통합이 가능합니다. 조직 샘플의 디지털화는 진단 정확도 향상, 병리학의 워크플로우 효율화, 연구개발 지원으로 이어집니다. 이 시장은 병리학 슬라이드 데이터의 획득, 저장, 검색, 공유, 분석을 위한 하드웨어 및 소프트웨어 솔루션을 모두 대상으로 합니다. 특히 종양 진단 분야의 지속적인 기술 혁신이 시장을 견인하고 있으며, 제약회사 및 연구기관이 디지털 병리학을 활용하여 의약품 개발의 효율화 및 정밀의료 접근법의 개선을 도모하는 움직임이 가속화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 시 가치 | 11억 달러 |

| 예측 금액 | 38억 달러 |

| CAGR | 13.4% |

제품 부문은 2024년 51.2%의 점유율을 차지했으며, 워크플로우 최적화 및 진단 정확도 향상을 실현할 수 있습니다. 스캐너는 원격 진단 및 텔레파트로지를 가능하게 하여 물리적 슬라이드를 운반할 필요성을 줄입니다. 슬라이드 관리 시스템은 데이터 처리를 간소화하고 기지 간의 연계를 개선하며 전반적인 효율성을 향상시킵니다. 기타 제품은 일상 업무를 자동화하고 인적 오류를 최소화하며 진단을 가속화합니다. 이것은 고용량 임상 환경에서 매우 중요합니다.

진단 부문은 2024년 6억 4,800만 달러로 평가되었습니다. 이 부문은 임상 워크플로우 내에서 질병 검출을 위한 디지털화된 조직 슬라이드의 해석에 초점을 맞추었습니다. 병리 의사는 종양, 감염, 염증성 질환 등의 이상을 확인하기 위해 AI 기반 분석 도구로 강화된 디지털 이미지에 의존하며 기존 현미경 기반 워크플로를 대체합니다.

북미의 디지털 병리학 시장은 2024년 33.4%의 점유율을 차지했습니다. 미국의 성장은 창약, 동반자 진단 및 보다 빠르고 정확한 조직 분석 기법을 추구하는 연구 기관의 채택 확대에 의해 견인되고 있습니다. 바이오메디컬 연구 및 의약품 개발에 대한 연방 정부의 투자는 지역 전반에 걸쳐 디지털 병리학 기술의 확대를 더욱 강화하고 있습니다.

세계의 디지털 병리학 시장의 주요 기업은 3DHISTECH, Dedalus, CellaVision, Danaher Corporation, F. Hoffmann-La Roche Ltd, Fujifilm Holdings Corporation, Glencoe Software Inc., Hamamatsu Photonics K.K., Huron Digital Pathology, Ibex Medical Analytics, Indica Labs Inc., Koninklijke Philips N.V., Mikroscan Technologies Inc., Olympus Corporation (Evident Scientific, Inc.), Paige AI, PathAI, PHC Holding Corporation (Epredia), Proscia, Inc., Sectra AB, and Visiopharm A/S 등을 들 수 있습니다. 세계 디지털 병리 시장의 각 회사는 여러 전략적 노력을 실시하여 시장에서의 기반 강화를 도모하고 있습니다. 진단 정밀도 향상을 위해 선진적인 고해상도 이미징 장치 및 AI 탑재 해석 소프트웨어에 대한 투자를 진행하고 있습니다. 또한 임상 현장이나 의약품 개발 워크플로우에 있어서의 도입 확대를 목표로, 병원, 연구 기관, 제약 기업과의 제휴를 많이 맺고 있습니다. 또한 기술 통합 및 제품 포트폴리오 확충을 목적으로 한 합병 및 인수도 활용되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 디지털 솔루션 도입 확대

- 디지털 병리학에 있어서 진단 인프라의 현대화 진전

- 디지털 병리 시스템과 전자 건강 기록(EHR)과의 통합

- 신약 및 동반자 진단에서 용도 확대

- 업계의 잠재적 위험 및 과제

- 디지털 병리학에 대한 표준 지침의 부족

- 하드웨어 또는 소프트웨어의 도입 및 통합에 따른 고가의 비용

- 시장 기회

- 원격병리학 및 텔레파트로지 솔루션에 대한 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 진보

- 현재 기술 동향

- 신흥 기술

- 공급망 분석

- 상환 시나리오

- 가격 분석(2024년)

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 제품

- 스캐너

- 슬라이드 관리 시스템

- 기타 제품

- 소프트웨어

- 유형

- AI 강화 이미지 분석 소프트웨어

- 데이터 관리 소프트웨어

- 기타 소프트웨어

- 전개 모드

- 클라우드 기반

- 온프레미스

- 유형

- 서비스

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 진단

- 연구

- 교육 및 연수

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 연구기관

- 연구소

- 병리 검사실

- 세포 검사실

- 기타 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- 3DHISTECH

- CellaVision

- Danaher Corporation

- Dedalus

- F. Hoffmann-La Roche Ltd

- Fujifilm Holdings Corporation

- Glencoe Software Inc.

- Hamamatsu Photonics KK

- Huron Digital Pathology

- Ibex Medical Analytics

- Indica Labs Inc.

- Koninklijke Philips NV

- Mikroscan Technologies Inc.

- Olympus Corporation

- Paige AI

- PathAI

- PHC Holding Corporation

- Proscia, Inc.

- Sectra AB

- Visiopharm A/S

The Global Digital Pathology Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 13.4% to reach USD 3.8 billion by 2034.

The growth is fueled by the rising adoption of digital solutions, modernization of diagnostic infrastructure, integration with electronic health records (EHRs), and increasing utilization in drug discovery and companion diagnostics. Digital pathology involves using digital imaging technologies to scan, analyze, and manage pathology slides and related data. It enables remote diagnostics, AI-assisted interpretations, and seamless EHR integration. Digitizing tissue samples enhances diagnostic accuracy, accelerates workflow efficiency for pathologists, and supports research and development. The market encompasses both hardware and software solutions for acquiring, storing, retrieving, sharing, and analyzing pathology slide data. Continuous technological innovations, particularly in oncology diagnostics, are driving the market forward, as pharmaceutical and research institutions increasingly leverage digital pathology to streamline drug development and improve precision medicine approaches.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 13.4% |

The product segment held a 51.2% share in 2024 owing to its ability to optimize workflow and enhance diagnostic precision. Scanners enable remote diagnostics and telepathology, reducing the need to transport physical slides. Slide management systems simplify data handling, improve collaboration across locations, and increase overall efficiency. Other product offerings automate routine tasks, minimize human error, and accelerate diagnosis, which is crucial in high-volume clinical environments.

The diagnostics segment was valued at USD 648 million in 2024. This segment focuses on interpreting digitized tissue slides for disease detection within clinical workflows. Pathologists rely on digital images, often enhanced with AI-based analysis tools, to identify abnormalities such as tumors, infections, or inflammatory conditions, replacing traditional microscope-based workflows.

North America Digital Pathology Market held a 33.4% share in 2024. Growth in the U.S. is driven by increased adoption in drug discovery, companion diagnostics, and research institutions seeking faster, more accurate tissue analysis methods. Federal investment in biomedical research and drug development further supports the expansion of digital pathology technologies across the region.

Key players in the Global Digital Pathology Market include 3DHISTECH, Dedalus, CellaVision, Danaher Corporation, F. Hoffmann-La Roche Ltd, Fujifilm Holdings Corporation, Glencoe Software Inc., Hamamatsu Photonics K.K., Huron Digital Pathology, Ibex Medical Analytics, Indica Labs Inc., Koninklijke Philips N.V., Mikroscan Technologies Inc., Olympus Corporation (Evident Scientific, Inc.), Paige AI, PathAI, PHC Holding Corporation (Epredia), Proscia, Inc., Sectra AB, and Visiopharm A/S. Companies in the Global Digital Pathology Market are strengthening their foothold by implementing several strategic initiatives. They are investing in advanced, high-resolution imaging devices and AI-powered analysis software to improve diagnostic accuracy. Many are forming partnerships with hospitals, research institutions, and pharmaceutical firms to expand adoption in clinical and drug development workflows. Mergers and acquisitions are being used to consolidate technologies and broaden product portfolios.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Application trend

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of digital solutions

- 3.2.1.2 Growing modernization in diagnostic infrastructure in digital pathology

- 3.2.1.3 Integration of digital pathology systems with electronic health records (EHRs)

- 3.2.1.4 Increasing application in drug discovery and companion diagnostics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of standard guidelines for digital pathology

- 3.2.2.2 High cost associated with the implementation and integration of hardware or software

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for remote pathology and telepathology solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Product

- 5.2.1 Scanners

- 5.2.2 Slide management systems

- 5.2.3 Other products

- 5.3 Software

- 5.3.1 Type

- 5.3.1.1 AI enhanced image analysis software

- 5.3.1.2 Data management software

- 5.3.1.3 Other software

- 5.3.2 Deployment mode

- 5.3.2.1 Cloud-based

- 5.3.2.2 On-premises

- 5.3.1 Type

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostics

- 6.3 Research

- 6.4 Education and training

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Research institutes

- 7.3 Laboratories

- 7.3.1 Pathology labs

- 7.3.2 Cytology labs

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3DHISTECH

- 9.2 CellaVision

- 9.3 Danaher Corporation

- 9.4 Dedalus

- 9.5 F. Hoffmann-La Roche Ltd

- 9.6 Fujifilm Holdings Corporation

- 9.7 Glencoe Software Inc.

- 9.8 Hamamatsu Photonics K.K.

- 9.9 Huron Digital Pathology

- 9.10 Ibex Medical Analytics

- 9.11 Indica Labs Inc.

- 9.12 Koninklijke Philips N.V.

- 9.13 Mikroscan Technologies Inc.

- 9.14 Olympus Corporation

- 9.15 Paige AI

- 9.16 PathAI

- 9.17 PHC Holding Corporation

- 9.18 Proscia, Inc.

- 9.19 Sectra AB

- 9.20 Visiopharm A/S