|

시장보고서

상품코드

1876825

재활용 납 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Recycled Lead Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

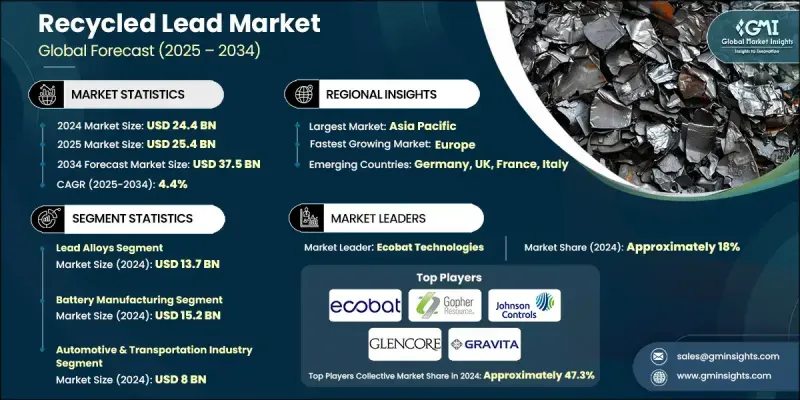

세계의 재활용 납 시장은 2024년에 244억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 4.4%로 성장하여 375억 달러에 이를 것으로 예측됩니다.

재활용 납은 순환 경제에서 중요한 역할을 하고 있으며, 주로 사용한 납 축전지 및 기타 납 함유 제품에서 조달됩니다. 화법야금법이나 습식야금법을 이용한 재활용 공정을 통해 1차 납과 동등한 품질과 성능을 가진 2차 납을 생산합니다. 환경 규제가 강화되고 지속가능성에 대한 관심이 높아짐에 따라, 제조업체들은 재활용 납을 채택하여 탄소 발자국을 줄이고 엄격한 컴플라이언스 기준을 달성하기 위해 노력하고 있습니다. 전기자동차의 보급 확대는 에너지 저장 및 전력계통 안정화 솔루션에서 재활용 납에 대한 수요를 증가시키고 있습니다. 납축전지는 자동차 시스템, 산업용 전원 백업 및 기타 에너지 저장 응용 분야에서 여전히 필수적입니다. 95% 이상의 높은 재활용률은 폐쇄 루프 공급 시스템을 지원하여 1차 납 채굴에 대한 의존도를 낮추는 동시에 비용 효율성과 공급의 신뢰성을 보장합니다. 환경 부하가 적기 때문에 전 세계적인 규제 지원으로 인해 1차 납보다 재활용 납의 사용이 더욱 가속화되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 244억 달러 |

| 예측 금액 | 375억 달러 |

| CAGR | 4.4% |

납 합금은 2024년 137억 달러의 매출을 기록했으며며, 56%의 점유율을 차지할 것으로 예측됩니다. 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.3%를 보일 것으로 예측됩니다. 납 합금은 안티몬, 주석, 칼슘 등의 금속과의 합금화를 통해 구현되는 우수한 기계적 강도, 내식성, 최적화된 전기 전도성으로 시장을 독점하고 있습니다. 이러한 특성으로 인해 자동차 배터리, 에너지 저장 시스템, 높은 내구성과 신뢰성이 요구되는 산업용도에 이상적입니다.

배터리 제조 부문은 2024년 152억 달러(62.4%의 점유율)를 차지했으며, 2034년까지 연평균 4.2%의 성장률을 보일 것으로 전망됩니다. 자동차, 산업 및 에너지 저장 분야에서 납축전지가 광범위하게 사용되고 있는 것이 이 부문의 우위를 뒷받침하고 있습니다. 재활용 납은 1차 납과 동일한 전기화학적 특성을 가지면서도 비용 절감과 환경적 이점을 제공합니다. 납축전지의 높은 재활용률은 견고한 순환 시스템을 유지하여 전 세계 배터리 생산을 위한 재활용 납의 안정적인 공급을 보장합니다.

북미 재활용 납 시장은 2025년부터 2034년까지 연평균 4.5%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이 지역의 성장은 지속 가능한 제조에 대한 기업의 노력, 순환 경제 이니셔티브, 높아진 환경 의식에 의해 뒷받침되고 있습니다. 첨단 납 재활용 기술에 대한 투자가 증가함에 따라 전통적인 1차 납 생산 방식을 점차 대체하고 있으며, 자동차, 산업 및 에너지 저장 용도 전반에 걸쳐 수요를 주도하고 있습니다.

재활용 납 시장의 주요 기업으로는 엑사이드 테크놀로지스(Exide Technologies), 힌두스탄 징크(Hindustan Zinc Limited), 그라비타 인디아(Gravita India Limited), 에코배트 테크놀로지스(Ecobat Technologies), RSR 코퍼레이션(RSR Corporation), 존슨 컨트롤즈 인터내셔널(Johnson Controls International), 고퍼 리소스(Gofer Resources), 그린리드(Green Lead) 프라임 리드 리사이클, 리드코, 글렌코어(브리타니아 리파인드 메탈스), 아디 인더스트리즈 리미티드, 심바 퍼포먼스 미네랄, 에너시스, 심즈 리미티드 등이 포함됩니다. 세계 재활용 납 시장 내 기업들은 생산능력 확대를 위한 재활용 시설 확장, 고품질 2차 납 생산을 위한 첨단 화공 야금 및 습식 야금 공정 도입, 배터리 제조업체 및 산업 고객과의 전략적 제휴 등 다양한 전략을 통해 시장에서의 입지를 강화하고 있습니다. 많은 기업들이 경쟁 우위를 확보하기 위해 지속가능성을 강조한 브랜딩과 환경 규제 준수에 집중하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 과제와 곤란

- 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협력 관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산·예측 : 제품 유형별, 2021-2034

- 주요 동향

- 연질 및 순납

- 납 합금

- 납-안티몬 합금

- 납 칼슘 합금

- 납 셀렌 및 납 주석 합금

- 커스텀 합금 개발

- 납 산화물

- Red lead oxide (Pb3O4)

- Lead(II) oxide (PbO)

- Lead(IV) oxide (PbO2

- 배터리용 등급 산화물

제6장 시장 추산·예측 : 용도별, 2021-2034

- 주요 동향

- 배터리 제조

- 자동차 배터리 제조

- 산업용 배터리 제조

- 에너지 저장 시스템 통합

- UPS 및 백업 전원 용도

- 방사선 차폐

- 의료시설용 용도

- 원자력 산업 요건

- 산업용 X선 및 비파괴 검사 장비

- 롤 및 압출 제품

- 건설 업계 수요

- 지붕재 및 방수재

- 건축 용도

- 산업용 기기 제조

- 안료 및 화학 화합물

- 산업용 페인트 및 코팅 용도

- 화학 처리 용도

- 특수 산업 용도

- 기타 용도

- 탄약 및 방위

- 케이블 코팅

- 특수 산업 용도

제7장 시장 추산·예측 : 최종 이용 산업별, 2021-2034

- 주요 동향

- 자동차 및 운송 업계

- 에너지 및 발전 산업

- 산업 제조업계

- 건설 및 인프라 산업

- 의료 및 의료기기 산업

- 전자 및 통신 산업

- 기타 산업

제8장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 개요

- Ecobat Technologies

- Gopher Resource

- Glencore(Britannia Refined Metals)

- Gravita India Limited

- Cimbar Performance Minerals

- Sims Limited

- LeadCo

- Exide Technologies

- Hindustan Zinc Limited

- GreenLead

- EnerSys

- Prime Lead Recycling

- Ardee Industries Ltd.

- RSR Corporation

- Johnson Controls International

The Global Recycled Lead Market was valued at USD 24.4 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 37.5 billion by 2034.

Recycled lead plays a crucial role in the circular economy, primarily sourced from spent lead-acid batteries and other lead-containing products. The recycling process, using pyrometallurgical and hydrometallurgical methods, produces secondary lead that matches the quality and performance of primary lead. Rising environmental regulations and sustainability initiatives are driving manufacturers to adopt recycled lead, reducing carbon footprints and meeting strict compliance standards. The growing adoption of electric vehicles is also increasing demand for recycled lead in energy storage and grid stabilization solutions. Lead-acid batteries remain critical for automotive systems, industrial power backups, and other energy storage applications. High recycling rates, often exceeding 95%, support a closed-loop supply system, reducing reliance on primary lead extraction while ensuring cost efficiency and supply reliability. Regulatory support globally further accelerates the use of recycled lead over primary lead due to its lower environmental impact.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.4 Billion |

| Forecast Value | $37.5 Billion |

| CAGR | 4.4% |

The lead alloys generated USD 13.7 billion in 2024, holding a 56% share, and are expected to grow at a CAGR of 4.3% from 2025 to 2034. Lead alloys dominate the market due to their superior mechanical strength, corrosion resistance, and optimized electrical conductivity achieved by alloying with metals like antimony, tin, and calcium. These properties make them ideal for automotive batteries, energy storage systems, and industrial applications requiring high durability and reliable performance.

The battery manufacturing segment accounted for USD 15.2 billion in 2024, representing a 62.4% share, and is projected to grow at a CAGR of 4.2% through 2034. The widespread use of lead-acid batteries across automotive, industrial, and energy storage sectors underpins the dominance of this segment. Recycled lead offers identical electrochemical properties to primary lead, while delivering cost savings and environmental advantages. The high recycling rates of lead-acid batteries maintain a robust closed-loop system, ensuring a steady supply of recycled lead for battery production globally.

North America Recycled Lead Market is expected to grow at a CAGR of 4.5% from 2025 to 2034. Regional growth is supported by corporate adoption of sustainable manufacturing, circular economy initiatives, and rising environmental awareness. Increased investment in advanced lead recycling technologies is gradually replacing conventional primary lead production methods, driving demand across automotive, industrial, and energy storage applications.

Key players in the Recycled Lead Market include Exide Technologies, Hindustan Zinc Limited, Gravita India Limited, Ecobat Technologies, RSR Corporation, Johnson Controls International, Gopher Resource, GreenLead, Prime Lead Recycling, LeadCo, Glencore (Britannia Refined Metals), Ardee Industries Ltd., Cimbar Performance Minerals, EnerSys, and Sims Limited. Companies in the Global Recycled Lead Market are strengthening their market presence through strategies such as expanding recycling facilities to increase production capacity, adopting advanced pyrometallurgical and hydrometallurgical processes for higher-quality secondary lead, and forming strategic partnerships with battery manufacturers and industrial clients. Many firms focus on sustainability-driven branding and compliance with environmental regulations to gain a competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 End use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.2 Pitfalls & Challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Soft/pure lead

- 5.3 Lead alloys

- 5.3.1 Lead-antimony alloys

- 5.3.2 Lead-calcium alloys

- 5.3.3 Lead-selenium & lead-tin alloys

- 5.3.4 Custom alloy development

- 5.4 Lead oxides

- 5.4.1 Red lead oxide (Pb3O4)

- 5.4.2 Lead(II) oxide (PbO)

- 5.4.3 Lead(IV) oxide (PbO2)

- 5.4.4 Battery-grade oxides

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Battery manufacturing

- 6.2.1 Automotive battery production

- 6.2.2 Industrial battery manufacturing

- 6.2.3 Energy storage system integration

- 6.2.4 Ups & backup power applications

- 6.3 Radiation shielding

- 6.3.1 Medical facility applications

- 6.3.2 Nuclear industry requirements

- 6.3.3 Industrial x-ray & ndt equipment

- 6.3.4 Rolls & extruded products

- 6.4 Construction industry demand

- 6.4.1 Roofing & weatherproofing

- 6.4.2 Architectural applications

- 6.4.3 Industrial equipment manufacturing

- 6.5 Pigments & chemical compounds

- 6.5.1 Industrial paint & coating applications

- 6.5.2 Chemical processing uses

- 6.5.3 Specialized industrial applications

- 6.6 Other applications

- 6.6.1 Ammunition & defense

- 6.6.2 Cable sheathing

- 6.6.3 Specialized industrial uses

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive & transportation industry

- 7.3 Energy & power generation industry

- 7.4 Industrial manufacturing industry

- 7.5 Construction & infrastructure industry

- 7.6 Healthcare & medical industry

- 7.7 Electronics & telecommunications industry

- 7.8 Other industries

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Ecobat Technologies

- 9.2 Gopher Resource

- 9.3 Glencore (Britannia Refined Metals)

- 9.4 Gravita India Limited

- 9.5 Cimbar Performance Minerals

- 9.6 Sims Limited

- 9.7 LeadCo

- 9.8 Exide Technologies

- 9.9 Hindustan Zinc Limited

- 9.10 GreenLead

- 9.11 EnerSys

- 9.12 Prime Lead Recycling

- 9.13 Ardee Industries Ltd.

- 9.14 RSR Corporation

- 9.15 Johnson Controls International