|

시장보고서

상품코드

1876826

오가노이드 및 스페로이드 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Organoids and Spheroids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

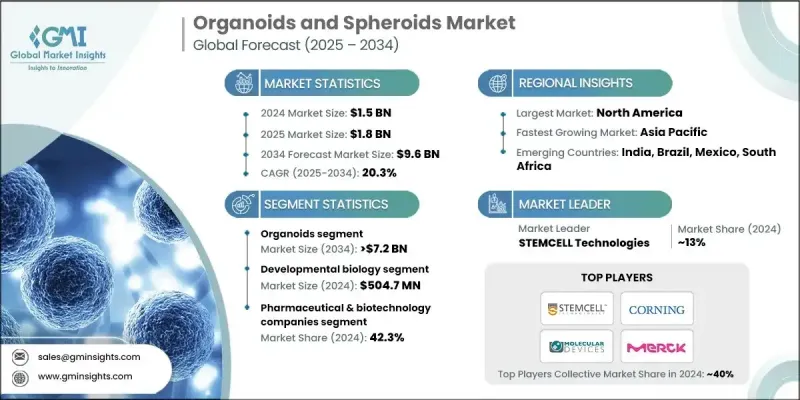

세계의 오가노이드 및 스페로이드 시장은 2024년에 15억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 20.3%로 성장하여 96억 달러에 이를 것으로 예측되고 있습니다.

연구자와 개발자들이 기존 2차원 시스템보다 인간의 생리적 기능을 더 충실하게 재현하는 첨단 3차원 세포 배양 모델에 대한 의존도가 높아짐에 따라 시장 확대가 가속화되고 있습니다. 이러한 전환은 주로 재생의학, 종양학, 신경학 등의 분야에서 보다 정확하고 확장 가능하며 윤리적으로 수용 가능한 전임상 솔루션에 대한 수요에 의해 주도되고 있습니다. 환자 유래 오가노이드와 스페로이드의 채택 확대도 업계 성장에 힘을 보태고 있습니다. 이러한 모델은 개별 치료 반응 및 바이오마커 식별에 대한 귀중한 통찰력을 제공하기 때문입니다. 이러한 플랫폼은 과학자들에게 질병 특이적 돌연변이의 거동과 환자 세포의 약물 반응에 대한 현실적인 가시성을 제공함으로써 표적치료제 개발을 혁신적으로 변화시키고 있습니다. 그 활용이 확대됨에 따라 예측 정확도가 향상되고, 시행착오에 의한 시험에서 흔히 볼 수 있는 비효율성이 감소하고 있습니다. 오가노이드 및 스페로이드 시장은 신약 개발, 독성 평가, 재생 의학, 질병 모델링, 개인 맞춤형 치료 전략 등 광범위한 응용 분야를 포괄하며, 학술, 임상 및 상업 분야에서 강력한 수요를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 15억 달러 |

| 예측 금액 | 96억 달러 |

| CAGR | 20.3% |

유기체 분야는 2024년 76.2%의 점유율을 차지했습니다. 이러한 장점은 오가노이드가 인간 조직의 기능적, 구조적 특징을 재현할 수 있는 능력에서 비롯되며, 이를 통해 질병 기전 및 약물 반응에 대한 보다 신뢰할 수 있는 모델링이 가능하다는 점에서 기인합니다. 특히 종양학 분야에서 연구자들이 환자 고유의 조직을 사용하여 보다 정밀한 치료법 선택을 위한 지침으로 오가노이드를 개인 맞춤형 의료 워크플로우에 통합하는 사례가 증가함에 따라 그 수요는 계속 증가하고 있습니다. 또한, 재생의료 분야에서의 역할 확대도 간, 신경, 장 조직 공학 프로젝트에서 채용을 촉진하고 있습니다.

제약 및 생명공학 기업 부문은 신약 개발, 독성 평가, 맞춤형 치료법 개발에서 3D 시스템에 대한 의존도가 높아짐에 따라 2024년 42.3%의 점유율을 차지했습니다. 이들 조직은 개발 초기 단계의 예측 정확도를 높이고 임상시험의 실패를 줄이기 위해 유기체 및 구체를 기반으로 한 플랫폼을 도입하고 있습니다. 기업들은 3D 배양으로 여러 화합물을 동시에 테스트할 수 있는 고처리량 스크리닝 시스템에 많은 투자를 하고 있습니다.

북미 유기체 및 구형체 시장은 2024년 42.7%의 점유율을 차지했습니다. 이 지역의 성장은 강력한 생물의학 연구 역량, 획기적인 기술의 신속한 도입, 주요 제약 및 생명공학 개발 기업의 적극적인 참여로 뒷받침되고 있습니다. 암, 신경질환, 소화기 질환의 유병률 증가로 인해 인간과 관련된 전임상 모델의 통합이 더욱 활발해지고 있습니다. 미국과 캐나다에서는 연구 자금의 확충, 환자 유래 바이오뱅크의 확대, 정밀의료 프로그램에서 오가노이드의 광범위한 활용으로 인해 오가노이드 기반 연구 활동이 활발하게 진행되고 있습니다.

유기체 및 구형체 시장 진출 기업으로는 ACRO 바이오시스템즈, AMSBIO, AMSBIO, ATCC, 코닝, 론자, 디피니젠, 분자 장치, 머크 KGaA, 프레리스 바이오로직스, STEMCELL 테크놀로지스 등이 있습니다. 유기체 및 구체 시장 기업들은 3D 배양 플랫폼 확대, 제약 및 생명공학 기업과의 제휴 강화, 자동화 스크리닝 기술에 대한 투자를 통해 경쟁력을 강화하고 있습니다. 많은 기업들이 정밀의료의 노력을 지원하고 차별화된 제품 포트폴리오를 구축하기 위해 질병에 특화된 전문 오가노이드 모델 개발을 진행하고 있습니다. 또한, 제조 공정을 강화하여 확장성, 재현성 및 규제 준수를 보장하며, 이는 신약 개발 및 임상 연구에 광범위하게 적용될 수 있는 필수적인 요소입니다. 학술 기관 및 의료 제공업체와의 전략적 제휴를 통해 다양한 환자 유래 샘플에 대한 접근이 가능해져 개인 맞춤형 치료 도구의 개선이 진행되고 있습니다. 또한, 이미징 기술, 배양 배지, 바이오 프린팅 시스템의 기술적 향상으로 보다 고도화되고 상업적으로 실현 가능한 3D 세포 배양 솔루션을 제공할 수 있게 되었습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 향후 시장 동향

- 기술적 상황

- 현행 기술

- 신기술

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추산·예측 : 유형별, 2021-2034

- 주요 동향

- 오가노이드

- 유형별

- 신경 오가노이드

- 간 오가노이드

- 장 오가노이드

- 기타 오가노이드 유형

- 방법별

- 일반적인 침수 방식의 오가노이드 배양법

- 크립트 오가노이드 배양 기술

- 공기-액체 계면(ALI) 방식

- 기타 오가노이드 배양법

- 소스별

- 1차 조직

- 줄기세포

- 유형별

- 스페로이드

- 유형별

- Multicellular tumor spheroids

- Neurospheres

- Mammospheres

- Hepatospheres

- 방법별

- Micropatterned plates

- Low cell attachment plates

- Hanging drop method

- Other spheroid culture methods

- 소스별

- 세포주

- iPS 세포 유래 세포

- 유형별

제6장 시장 추산·예측 : 용도별, 2021-2034

- 주요 동향

- 발생생물학

- 맞춤형 의료

- 재생의료

- 질환 병리학 연구

- 약제 독성 및 유효성 시험

제7장 시장 추산·예측 : 최종 용도별, 2021-2034

- 주요 동향

- 제약 기업 및 바이오테크놀러지 기업

- 학술기관 및 연구기관

- 병원 및 진단센터

- 기타 최종 용도

제8장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 개요

- ACROBiosystems

- AMSBIO

- ATCC

- Corning

- DefiniGEN

- Lonza

- Merck KGaA

- Molecular Devices

- Prellis Biologics

- STEMCELL Technologies

The Global Organoids and Spheroids Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 20.3% to reach USD 9.6 billion by 2034.

Market expansion is accelerating as researchers and developers increasingly depend on advanced 3D cell culture models that mirror human physiology better than traditional 2D systems. This transition is largely fueled by the need for more accurate, scalable, and ethically acceptable preclinical solutions across areas such as regenerative medicine, oncology, and neurology. Growing adoption of patient-derived organoids and spheroids is also contributing to industry momentum, as these models deliver valuable insights into individual treatment responses and biomarker identification. These platforms are transforming targeted therapy development by giving scientists a realistic view of how disease-specific mutations behave and how patient cells react to drugs. Their growing use provides stronger predictability and decreases the inefficiencies often seen in trial-and-error testing. The organoids and spheroids market covers a broad spectrum of applications, including drug discovery, toxicity evaluation, regenerative medicine, disease modelling, and personalized therapeutic strategies, driving strong demand across academic, clinical, and commercial sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 20.3% |

The organoids segment held a 76.2% share in 2024. Its dominance stems from the ability of organoids to recreate functional and structural features of human tissues, resulting in more reliable modelling of disease mechanisms and drug responses. Demand continues to rise as researchers increasingly integrate organoids into personalized medicine workflows, particularly in oncology, where patient-specific tissue helps guide more precise therapy selection. Their expanding role in regenerative medicine is also spurring adoption across liver, neural, and intestinal tissue engineering initiatives.

The pharmaceutical and biotechnology companies segment held 42.3% share in 2024 due to growing reliance on 3D systems for drug discovery, toxicity evaluation, and personalized therapy development. These organizations are incorporating organoid- and spheroid-based platforms to enhance prediction accuracy during early development and reduce clinical trial failures. Companies are making sizable investments in high-throughput screening systems that allow simultaneous testing of multiple compounds using 3D cultures.

North America Organoids and Spheroids Market accounted for a 42.7% share in 2024. Regional growth is supported by strong biomedical research capabilities, rapid adoption of breakthrough technologies, and significant participation from leading pharmaceutical and biotech developers. The rising prevalence of cancer, neurological disorders, and gastrointestinal diseases is leading to deeper integration of human-relevant preclinical models. The U.S. and Canada are also witnessing increased activity in organoid-based research because of robust research funding, expanding patient-derived biobanks, and widespread use of organoids in precision medicine programs.

Key Organoids and Spheroids Market participants include ACROBiosystems, AMSBIO, ATCC, Corning, Lonza, DefiniGEN, Molecular Devices, Merck KGaA, Prellis Biologics, and STEMCELL Technologies. Companies in the Organoids and Spheroids Market are strengthening their competitive position by expanding their 3D culture platforms, increasing partnerships with pharmaceutical and biotech firms, and investing in automated screening technologies. Many are developing specialized, disease-focused organoid models to support precision medicine initiatives and create differentiated product portfolios. Firms are also enhancing their manufacturing processes to ensure scalability, reproducibility, and regulatory compliance, which is essential for broader adoption in drug discovery and clinical research. Strategic collaborations with academic institutes and healthcare providers help companies access diverse patient-derived samples, allowing them to refine personalized therapy tools. Additionally, technological upgrades in imaging, culture media, and bioprinting systems are enabling companies to deliver more advanced and commercially viable 3D cell culture solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancement in cell culture technologies

- 3.2.1.2 Increase in demand for personalized medicine

- 3.2.1.3 Rise in prevalence of chronic diseases

- 3.2.1.4 Technological advancement in 3D spheroid systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of robust disease models

- 3.2.2.2 High cost of development and maintenance

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of organoid biobanks and rare disease modeling

- 3.2.3.2 Integration of AI and digital platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Organoids

- 5.2.1 By Type

- 5.2.1.1 Neural organoids

- 5.2.1.2 Hepatic organoids

- 5.2.1.3 Intestinal organoids

- 5.2.1.4 Other organoid types

- 5.2.2 By Method

- 5.2.2.1 General submerged method for organoid culture

- 5.2.2.2 Crypt organoid culture techniques

- 5.2.2.3 Air Liquid Interface (ALI) method

- 5.2.2.4 Other organoid culture methods

- 5.2.3 By Source

- 5.2.3.1 Primary tissues

- 5.2.3.2 Stem cells

- 5.2.1 By Type

- 5.3 Spheroids

- 5.3.1 By Type

- 5.3.1.1 Multicellular tumor spheroids

- 5.3.1.2 Neurospheres

- 5.3.1.3 Mammospheres

- 5.3.1.4 Hepatospheres

- 5.3.2 By Method

- 5.3.2.1 Micropatterned plates

- 5.3.2.2 Low cell attachment plates

- 5.3.2.3 Hanging drop method

- 5.3.2.4 Other spheroid culture methods

- 5.3.3 By Source

- 5.3.3.1 Cell line

- 5.3.3.2 iPSCs derived cells

- 5.3.1 By Type

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Developmental biology

- 6.3 Personalized medicine

- 6.4 Regenerative medicine

- 6.5 Disease pathology studies

- 6.6 Drug toxicity & efficacy testing

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical & biotechnology companies

- 7.3 Academic & research institutes

- 7.4 Hospitals and diagnostic centers

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ACROBiosystems

- 9.2 AMSBIO

- 9.3 ATCC

- 9.4 Corning

- 9.5 DefiniGEN

- 9.6 Lonza

- 9.7 Merck KGaA

- 9.8 Molecular Devices

- 9.9 Prellis Biologics

- 9.10 STEMCELL Technologies