|

시장보고서

상품코드

1876828

동반진단 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Companion Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

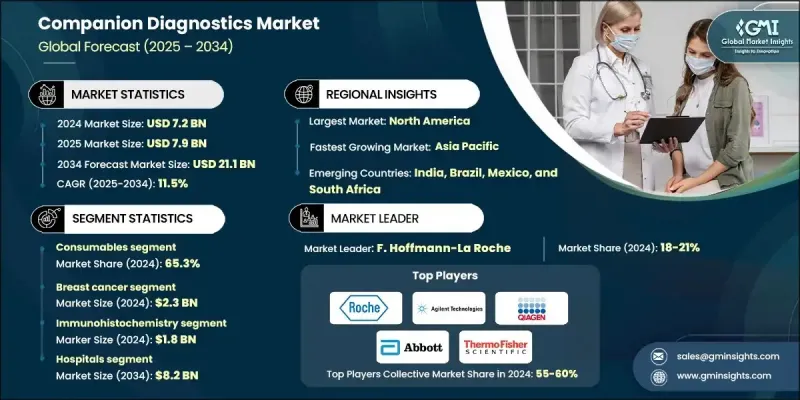

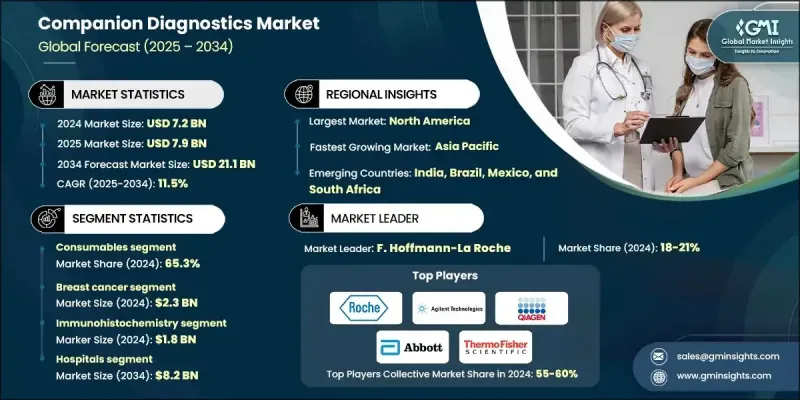

세계의 동반진단 시장은 2024년에 72억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 11.5%로 성장하여 211억 달러에 이를 것으로 예측됩니다.

시장 성장의 주요 요인은 암 발병률 증가, 약물 부작용 증가, 그리고 정밀의료의 급속한 보급입니다. 동반진단은 특정 치료법에 가장 잘 반응할 가능성이 높은 환자를 선별하기 위한 전문적인 의료 검사입니다. 약물 반응에 영향을 미치는 특정 바이오마커나 유전자 변이를 검출하여 보다 정확하고 맞춤 치료 방침을 결정할 수 있습니다. 동반진단약의 활용은 부작용 위험을 줄이고 치료 효과를 향상시키며, 개인맞춤형 헬스케어의 세계적 흐름에 부합하는 것입니다. 특히 종양학, 면역학, 만성질환 관리 분야의 임상 프로토콜에 통합되는 추세는 치료 결과를 최적화하는 데 있어 그 역할이 확대되고 있음을 반영합니다. 약물 부작용은 현대 의료에서 여전히 심각한 문제이기 때문에 규제 당국과 의료 서비스 제공업체 모두 환자 위험을 최소화하고 약물의 안전성을 향상시키는 진단 방법을 채택하는 데 중점을 두고 있습니다. 이러한 인식의 확산은 기술 발전과 바이오마커 연구 확대와 함께 세계 동반진단제 시장의 성장을 지속적으로 견인하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 72억 달러 |

| 예측 금액 | 211억 달러 |

| CAGR | 11.5% |

소모품 부문은 2024년 65.3%의 점유율을 차지했습니다. 이 카테고리에는 진단 검사 수행에 필수적인 카트리지, 분석 시약, 검사 키트, 검체 전처리 재료 등 일회용 제품이 포함됩니다. 임상검사실에서의 소모품에 대한 지속적인 수요는 모든 검사에 필요하기 때문에 안정적인 수익원을 창출하고 있습니다. 진단 장비가 일회성 자본 지출인 반면, 소모품은 지속적인 제품 수요를 보장하기 때문에 이 분야 전체 공급업체와 제조업체에게 중요한 촉진제가 되고 있습니다.

유방암 분야는 2024년 23억 달러 시장 규모를 기록했습니다. 유방암의 높은 발병률로 인해 치료 선택에 도움이 되는 특정 분자 마커를 식별할 수 있는 진단 도구에 대한 수요가 증가하고 있습니다. HER2 양성, 호르몬 수용체 양성 등의 아형에 대한 맞춤 치료로 전환이 진행되면서 검사 건수가 증가하고 있습니다. 또한, 제약회사와 진단기기 제조업체의 협력으로 바이오마커 기반 솔루션이 발전하고 있으며, 종양 진단 분야 시장 확대와 기술 혁신을 촉진하고 있습니다.

미국 동반진단 시장은 암 부담 증가와 표적치료에 대한 관심 증가로 2024년 27억 달러 규모에 달했습니다. 미국 전역의 암 발생률이 지속적으로 증가함에 따라 정확하고 효율적인 진단 플랫폼에 대한 수요가 증가하고 있습니다. 동반 진단은 정밀 종양학에 빠르게 통합되어 의사가 종양의 유전 정보와 개별 환자 프로파일에 따라 치료 전략을 맞춤화할 수 있도록 돕고 있습니다. 이 접근법은 치료 성공률을 높이고 부작용을 최소화하여 진단에 기반한 치료는 미국 현대 암 치료의 중심적인 역할을 하고 있습니다.

세계 동반진단 시장에서 사업을 전개하고 있는 주요 기업으로는 화이자, 머크, 아스트라제네카, 써모피셔 사이언티픽, F. 호프만 라 로슈, 애보트 래버러토리스, 암젠, 존슨앤드존슨, 브리스톨 마이어스 스퀴브, 일라이 릴리, 미리어드 제네릭, 가던트 헬스, 재단 의학, 브리스톨마이어스 스퀴브, 일라이 릴리, 가디언 헬스, 가드너 헬스, 재단 의학, 브리스톨마이어스 스퀴브 등이 있습니다. 브리스톨 마이어스 스퀴브, 일라이 릴리 앤 컴퍼니, 미리어드 제네틱스, 가던트 헬스, 파운데이션 메디슨, 바이오젠, 벡톤 딕킨슨 앤 컴퍼니 등이 있습니다. 동반진단 시장의 주요 기업들은 경쟁력을 강화하기 위해 다양한 전략을 채택하고 있습니다. 많은 기업들이 제약사와 장기적인 파트너십을 맺고 신약 출시에 맞추어 표적치료제나 동반진단을 공동 개발하고 있습니다. 또한, 진단 검사의 정확도와 예측 능력을 높이기 위해 바이오마커 발굴과 차세대 시퀀싱 기술에도 많은 투자를 하고 있습니다. 전략적 합병 및 인수를 통해 세계 사업 확장과 제품 포트폴리오의 다각화를 꾀하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 기술 동향

- 현행 기술

- 신기술

- 향후 시장 동향

- 특허 분석

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 공동 사업

- 신제품 발매

- 확대 계획

제5장 시장 추산·예측 : 제품별, 2021-2034

- 주요 동향

- 계측 기기

- 소모품

- 서비스

제6장 시장 추산·예측 : 적응 질환별, 2021-2034

- 주요 동향

- 유방암

- 폐암

- 대장암

- 피부암

- 기타 질환 적응증

제7장 시장 추산·예측 : 기술별, 2021-2034

- 주요 동향

- 면역조직화학

- In situ hybridization

- 중합효소 연쇄반응

- 유전자 배열 결정

- 기타 기술

제8장 시장 추산·예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 진단실험실

- 기타 최종 용도

제9장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 개요

- Abbott Laboratories

- Amgen

- AstraZeneca

- Becton, Dickinson and Company

- Biogen

- Bristol Myers Squibb

- Eli Lilly and Company

- F. Hoffmann-La Roche

- Foundation Medicine

- Guardant Health

- Johnson &Johnson

- Merck

- Myriad Genetics

- Pfizer

- Thermo Fisher Scientific

The Global Companion Diagnostics Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 11.5% to reach USD 21.1 billion by 2034.

Market growth is driven by the rising prevalence of cancer, the growing incidence of adverse drug reactions, and the rapid adoption of precision medicine. Companion diagnostics are specialized medical tests that help identify patients who are most likely to respond positively to a particular therapy. By detecting specific biomarkers or genetic variations that influence drug response, these diagnostics enable more accurate, personalized treatment decisions. The use of companion diagnostics reduces the risk of side effects, enhances therapeutic efficacy, and aligns with the global shift toward individualized healthcare. Their increasing integration into clinical protocols, especially in oncology, immunology, and chronic disease management, reflects their growing role in optimizing treatment outcomes. As adverse drug reactions continue to pose major challenges in modern healthcare, both regulatory agencies and healthcare providers are emphasizing the adoption of diagnostics that minimize patient risk and improve drug safety. This growing awareness, combined with technological progress and the expansion of biomarker research, continues to strengthen the companion diagnostics market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.2 Billion |

| Forecast Value | $21.1 Billion |

| CAGR | 11.5% |

The consumables segment accounted for a 65.3% share in 2024. This category includes single-use products such as cartridges, assay reagents, test kits, and sample preparation materials that are vital for conducting diagnostic assays. The continuous demand for consumables in clinical laboratories drives consistent revenue streams, as they are required for every test performed. Unlike diagnostic instruments, which represent a one-time capital expense, consumables ensure ongoing product demand, making them a crucial growth driver for suppliers and manufacturers across the sector.

The breast cancer segment was valued at USD 2.3 billion in 2024. The widespread incidence of breast cancer has created a strong need for diagnostic tools capable of identifying specific molecular markers that guide therapy selection. The move toward personalized treatment approaches for subtypes such as HER2-positive and hormone receptor-positive breast cancers has resulted in increasing testing volumes. Additionally, collaborations between pharmaceutical and diagnostic companies are advancing biomarker-driven solutions, boosting market expansion and innovation in oncology diagnostics.

U.S. Companion Diagnostics Market reached USD 2.7 billion in 2024, supported by the rising cancer burden and increasing focus on targeted medicine. With cancer rates continuing to rise across the nation, the demand for accurate and efficient diagnostic platforms is intensifying. Companion diagnostics are being rapidly integrated into precision oncology, helping physicians customize treatment strategies based on tumor genetics and individual patient profiles. This approach enhances therapy success rates and minimizes adverse effects, making diagnostic-guided treatment a central part of modern cancer care in the United States.

Leading companies operating within the Global Companion Diagnostics Market include Pfizer, Merck, AstraZeneca, Thermo Fisher Scientific, F. Hoffmann-La Roche, Abbott Laboratories, Amgen, Johnson & Johnson, Bristol Myers Squibb, Eli Lilly and Company, Myriad Genetics, Guardant Health, Foundation Medicine, Biogen, and Becton, Dickinson and Company. Key players in the Companion Diagnostics Market are employing a range of strategies to strengthen their competitive positions. Many are forming long-term collaborations with pharmaceutical firms to co-develop targeted therapies and companion tests that align with new drug launches. Companies are also investing heavily in biomarker discovery and next-generation sequencing technologies to enhance the accuracy and predictive power of diagnostic assays. Strategic mergers and acquisitions are expanding their global reach and diversifying product portfolios.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Products trends

- 2.2.3 Disease indication trends

- 2.2.4 Technology trends

- 2.2.5 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Upward trend in disease prevalence among developing countries

- 3.2.1.2 Surging number of pathology labs and services equipped with advanced diagnostic equipment in North America

- 3.2.1.3 Technological advancements

- 3.2.1.4 Increasing R&D investment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 High cost of product development

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in remote and rural areas

- 3.2.3.2 Integration with digital health platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.3 Consumables

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Disease Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Breast cancer

- 6.3 Lung cancer

- 6.4 Colorectal cancer

- 6.5 Skin cancer

- 6.6 Other diseases indications

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Immunohistochemistry

- 7.3 In situ hybridization

- 7.4 Polymerase chain reaction

- 7.5 Genetic sequencing

- 7.6 Other technologies

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic laboratories

- 8.4 Other End Use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Amgen

- 10.3 AstraZeneca

- 10.4 Becton, Dickinson and Company

- 10.5 Biogen

- 10.6 Bristol Myers Squibb

- 10.7 Eli Lilly and Company

- 10.8 F. Hoffmann-La Roche

- 10.9 Foundation Medicine

- 10.10 Guardant Health

- 10.11 Johnson & Johnson

- 10.12 Merck

- 10.13 Myriad Genetics

- 10.14 Pfizer

- 10.15 Thermo Fisher Scientific