|

시장보고서

상품코드

1892666

고체 배터리 전해질 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Solid State Battery Electrolyte Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

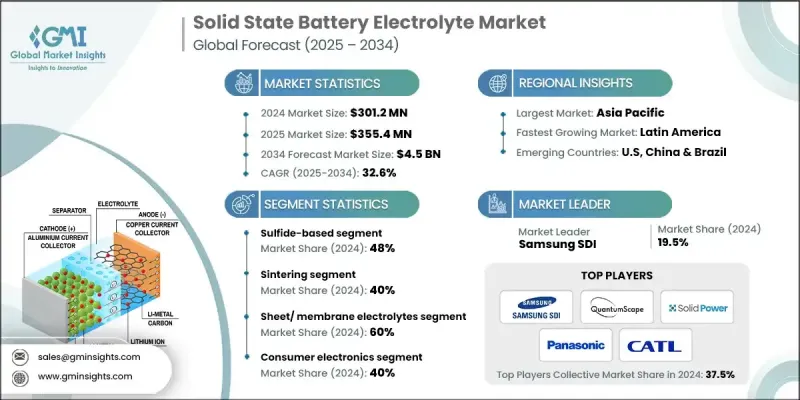

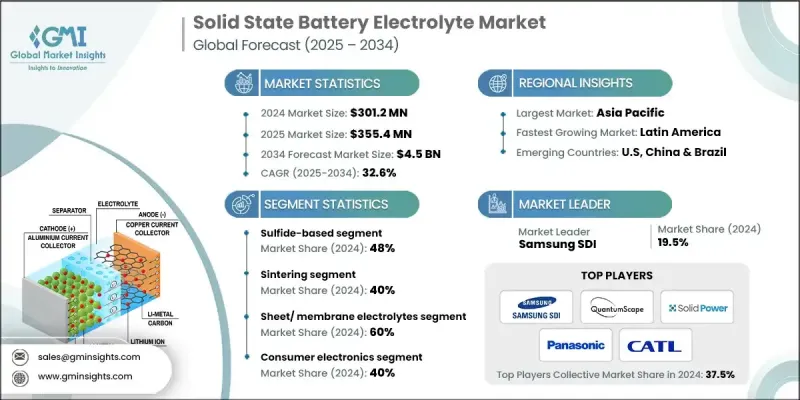

세계의 고체 배터리 전해질 시장은 2024년에 3억 120만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 32.6%로 성장하여 45억 달러에 이를 것으로 예측됩니다.

아시아태평양이 가장 빠르게 성장할 것으로 예상되며, 중국이 황화물 전해질 및 고분자 전해질에 대한 투자를 주도하고 있으며, 북미와 유럽에서도 눈에 띄는 활동이 전개되고 있습니다. 라틴아메리카와 중동 및 아프리카도 풍부한 리튬 자원, 전기자동차 보급 확대, 국내 재생에너지 정책으로 인해 새로운 생산능력을 견인할 수 있는 강력한 잠재력을 보여주고 있습니다. 기술 발전, 대규모 배터리 제조 및 규제 지원으로 인해 전 세계적으로 고체 전해질 채택이 가속화되고 있습니다. 컴퓨터 스크리닝과 머신러닝을 활용하여 높은 이온 전도성과 강화된 전기화학적 안정성을 가진 물질의 발견이 진행되고 있습니다. 계면 설계, 입계 최적화, 리튬 금속 음극용 보호 코팅 등의 혁신 기술을 통해 안전성, 사이클 수명, 에너지 밀도를 향상시켜 전기자동차, 가전제품, 에너지 저장 시스템에 폭넓게 적용할 수 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 연도 시장 규모 | 3억 120만 달러 |

| 예측 금액 | 45억 달러 |

| CAGR | 32.6% |

2024년 산화물 전해질 부문은 8,430만 달러를 차지했습니다. 이들 소재는 우수한 기계적 강도, 전기화학적 안정성, 리튬 금속 음극과의 호환성을 갖추고 있어 자동차 및 가전제품의 용도에 적합합니다. 그러나 소결 온도가 높고 고유한 취성이 있기 때문에 제조가 복잡합니다.

박막 전해질 부문은 경량 구조, 높은 부피 에너지 밀도, 균일한 이온 수송 특성으로 인해 2024년 6,020만 달러의 가치를 지닙니다. 이러한 박막은 결함 없는 균일한 층을 구현하기 위해 물리적 기상증착법(PVD) 또는 원자층 증착법(ALD)을 통해 제조되지만, 생산 규모를 확대하는 데는 비용이 많이 들고 어려움이 따릅니다.

북미 고체 배터리 전해질 시장은 2024년 30%의 점유율을 차지했습니다. 이 지역의 성장은 전기자동차 보급 확대, 에너지 저장 수요, 가전기기 사용 증가에 의해 뒷받침되고 있습니다. 미국 시장은 정부 지원 프로그램 및 자금 조달 이니셔티브와 더불어 QuantumScape, Solid Power, Factorial Energy와 같은 기업들의 투자로 혜택을 누리고 있습니다. 캐나다는 공공 연구기관과 대학이 참여하는 공동 프로토타입 규모의 생산시설을 통해 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)

(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산 및 예측 : 재료 유형별, 2021-2034

- 주요 동향

- 산화물계 고체 전해질

- Garnet-type (LLZO)

- NASICON-type (LATP, LAGP)

- Perovskite-type (LLTO)

- LiPON (Lithium Phosphorus Oxynitride)

- 황화물계 고체 전해질

- Argyrodite Family (Li6PS5X)

- LGPS Family (Li10GeP2S12 & Derivatives)

- Thio-LISICON (Li3PS4, Li4-xGe1-xPxS4)

- 고분자계 고체 전해질

- PEO(폴리에틸렌 옥시드)

- PC(폴리카보네이트) 및 PAN(폴리 아크릴로니트릴)

- 복합 폴리머 전해질(CPE)

- 하이브리드 전해질(폴리머+무기질)

- 할로겐 화물계 고체 전해질

- 염화물계(Li3YCl6, Li3InCl6, Li2ZrCl6)

- 취화물계(Li3YBr6)

- 혼합 할로겐계(Li3Y(Br3Cl3))

제6장 시장 추산 및 예측 : 제조 공정별, 2021-2034

- 주요 동향

- 물리적 기상 성장법(PVD) 및 원자층 증착법(ALD)

- 테이프 캐스팅 및 스크린 인쇄

- 소결 및 열간 프레스

- 기존 소결

- 핫 프레스

- 스파크 플라즈마 소결(SPS)

- 상온 소결

- 용액 주조 및 폴리머 가공

제7장 시장 추산 및 예측 : 형태별, 2021-2034

- 주요 동향

- 박막 전해질(10μm 미만)

- 시트/막 전해질(10-100μm)

- 벌크/펠릿 전해질(100μm 이상)

제8장 시장 추산 및 예측 : 용도별, 2021-2034

- 주요 동향

- 전기자동차

- 가전제품

- 에너지 저장 시스템

- 의료기기

- 항공우주 및 방위

제9장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 개요

- Ampcera Inc.

- Blue Solutions SAS

- Contemporary Amperex Technology Co., Limited(CATL)

- Idemitsu Kosan Co., Ltd.

- Ionic Materials Inc.

- Murata Manufacturing Co., Ltd.

- Panasonic Holdings Corporation

- QuantumScape Corporation

- SAMSUNG SDI

- Solid Power Inc.

The Global Solid State Battery Electrolyte Market was valued at USD 301.2 million in 2024 and is estimated to grow at a CAGR of 32.6% to reach USD 4.5 billion by 2034.

The Asia-Pacific region is expected to see the fastest growth, with China leading investments in sulfide and polymer electrolytes, followed by notable activity in North America and Europe. Latin America and the Middle East & Africa also show strong potential due to abundant lithium resources, rising electric vehicle adoption, and domestic renewable energy initiatives, which will drive new production capacity. Technological advancements, large-scale battery manufacturing, and regulatory support are accelerating the adoption of solid-state electrolytes worldwide. Computational screening and machine learning are being leveraged to discover materials with high ionic conductivity and enhanced electrochemical stability. Innovations such as interface engineering, grain boundary optimization, and protective coatings for lithium metal anodes are improving safety, cycle life, and energy density, enabling broader applications in electric vehicles, consumer electronics, and energy storage systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $301.2 Million |

| Forecast Value | $4.5 Billion |

| CAGR | 32.6% |

In 2024, the oxide electrolytes segment accounted for USD 84.3 million. These materials offer exceptional mechanical strength, electrochemical stability, and compatibility with lithium metal anodes, making them ideal for automotive and consumer electronics applications. However, high sintering temperatures and inherent brittleness make their manufacturing complex.

The thin-film electrolytes segment was valued at USD 60.2 million in 2024 owing to their lightweight structure, high volumetric energy density, and uniform ion transport. These films are produced through physical vapor deposition (PVD) or atomic layer deposition (ALD) to achieve defect-free, homogeneous layers, though scaling production is costly and challenging.

North America Solid State Battery Electrolyte Market accounted for a 30% share in 2024. Growth in the region is supported by rising electric vehicle adoption, energy storage demand, and consumer electronics applications. The U.S. market benefits from government-backed programs and funding initiatives, alongside investments from companies such as QuantumScape, Solid Power, and Factorial Energy. Canada contributes through collaborative prototype-scale production facilities involving public research institutions and universities.

Key players in the Global Solid State Battery Electrolyte Market include CATL (Contemporary Amperex Technology Co., Limited), Panasonic Holdings Corporation, QuantumScape Corporation, Solid Power Inc., SAMSUNG SDI, Ampcera Inc., Blue Solutions SAS, Idemitsu Kosan Co., Ltd., Ionic Materials Inc., and Murata Manufacturing Co., Ltd. Companies in the Solid State Battery Electrolyte Market strengthen their presence through strategic R&D investments to enhance ionic conductivity, electrochemical stability, and compatibility with lithium metal anodes. They are forming partnerships with automakers, consumer electronics manufacturers, and energy storage providers to accelerate adoption. Additionally, firms focus on scaling production capabilities, pilot programs, and supply chain optimization while leveraging government incentives and funding initiatives.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Manufacturing Process

- 2.2.4 Form Factor

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Automotive OEMs accelerating adoption of solid-state batteries globally

- 3.2.1.2 Non-flammable solid electrolytes enhance safety and reduce thermal risks

- 3.2.1.3 Lithium metal anodes enable higher energy density and extended EV range

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Solid-solid interface resistance limits power density and cycling performance

- 3.2.2.2 Manufacturing scale-up from lab to GWh production remains complex

- 3.2.3 Market opportunities

- 3.2.3.1 Energy storage systems demand growth drives stationary solid-state applications

- 3.2.3.2 Consumer electronics miniaturization creates high-value, compact battery applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Oxide-Based Solid Electrolytes

- 5.2.1 Garnet-type (LLZO)

- 5.2.2 NASICON-type (LATP, LAGP)

- 5.2.3 Perovskite-type (LLTO)

- 5.2.4 LiPON (Lithium Phosphorus Oxynitride)

- 5.3 Sulfide-Based Solid Electrolytes

- 5.3.1 Argyrodite Family (Li6PS5X)

- 5.3.2 LGPS Family (Li10GeP2S12 & Derivatives)

- 5.3.3 Thio-LISICON (Li3PS4, Li4-xGe1-xPxS4)

- 5.4 Polymer-Based Solid Electrolytes

- 5.4.1 PEO (Polyethylene Oxide)

- 5.4.2 PC (Polycarbonate) & PAN (Polyacrylonitrile)

- 5.4.3 Composite Polymer Electrolytes (CPEs)

- 5.4.4 Hybrid Electrolytes (Polymer + Inorganic)

- 5.5 Halide-Based Solid Electrolytes

- 5.5.1 Chloride-based (Li3YCl6, Li3InCl6, Li2ZrCl6)

- 5.5.2 Bromide-based (Li3YBr6)

- 5.5.3 Mixed Halide Systems (Li3Y(Br3Cl3))

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Physical Vapor Deposition (PVD) & Atomic Layer Deposition (ALD)

- 6.3 Tape casting & screen printing

- 6.4 Sintering & hot pressing

- 6.4.1 Conventional sintering

- 6.4.2 Hot pressing

- 6.4.3 Spark Plasma Sintering (SPS)

- 6.4.4 Cold sintering

- 6.5 Solution casting & polymer processing

Chapter 7 Market Estimates and Forecast, By Form Factor, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Thin-film electrolytes (<10 μm)

- 7.3 Sheet/membrane electrolytes (10-100 μm)

- 7.4 Bulk/pellet electrolytes (>100 μm)

Chapter 8 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Electric vehicles

- 8.3 Consumer electronics

- 8.4 Energy storage systems

- 8.5 Medical devices

- 8.6 Aerospace & defense

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Ampcera Inc.

- 10.2 Blue Solutions SAS

- 10.3 Contemporary Amperex Technology Co., Limited (CATL)

- 10.4 Idemitsu Kosan Co., Ltd.

- 10.5 Ionic Materials Inc.

- 10.6 Murata Manufacturing Co., Ltd.

- 10.7 Panasonic Holdings Corporation

- 10.8 QuantumScape Corporation

- 10.9 SAMSUNG SDI

- 10.10 Solid Power Inc.