|

시장보고서

상품코드

1892705

지속가능한 단백질 가수분해물 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Sustainable Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

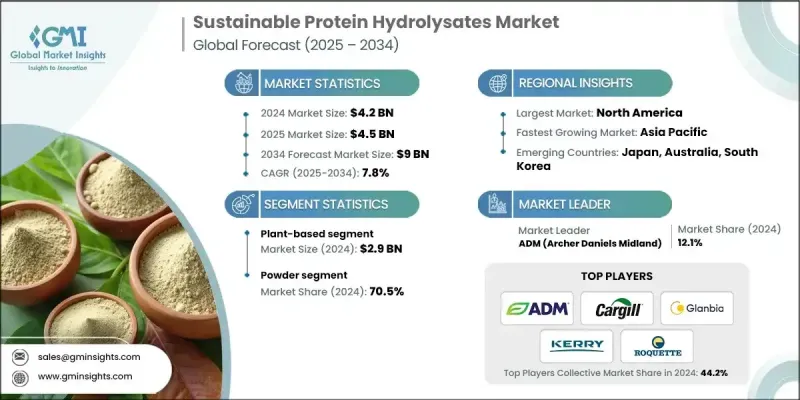

세계의 지속가능한 단백질 가수분해물 시장은 2024년에 42억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 7.8%로 성장하여 90억 달러에 이를 것으로 예측됩니다.

단백질 가수분해물은 지속 가능한 단백질 공급원을 효소 분해하여 얻은 생리활성 펩타이드입니다. 친환경 단백질 원료에 대한 수요 증가에 대응하기 위해 산업계에서는 식물, 곤충, 제품별 단백질 추출에 집중하고 있습니다. 이러한 가수분해물은 우수한 생체 이용률, 기능적 특성, 건강 효과로 인해 주목받고 있으며, 전 세계적으로 증가하는 지속가능성에 대한 관심에 부합하는 제품입니다. 미국 농무부의 지속 가능한 농업 프로그램, 유럽 그린딜 등 순환 경제를 촉진하는 정부의 이니셔티브는 식품, 의약품, 화장품 분야에서의 채택을 촉진하고 있습니다. 북미는 선진적인 생산 인프라와 지원적인 규제로 시장을 선도하고 있으며, 아시아태평양은 혁신적인 가공 기술에 대한 대규모 투자와 엄격한 지속가능성 정책에 힘입어 가장 빠르게 성장하는 지역으로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 42억 달러 |

| 예측 금액 | 90억 달러 |

| CAGR | 7.8% |

식물성 단백질 공급원 부문은 2024년 29억 달러 시장 규모를 창출하며 시장을 장악했습니다. 이는 소비자의 식물성 영양에 대한 강한 전환 경향과 가수분해에 적합한 다양한 단백질 공급원의 가용성을 반영합니다. 콩류, 곡물, 종자 및 기타 농업용 원료는 다양한 아미노산 프로파일과 기능적 이점을 제공하여 다양한 용도에 이상적입니다.

분말형 단백질 가수분해물 부문은 보관 및 운송상의 이점과 제조 유연성으로 인해 2024년 70.5%의 점유율을 차지할 것으로 예측됩니다. 수분 함량이 낮고 장기 보관이 가능한 분말은 식품, 영양 보충제, 사료 배합에서 취급 및 투여를 단순화합니다. 분무 건조, 동결 건조 및 기타 탈수 기술의 발전으로 액체에서 분말로 변환하는 과정에서 생물 활성 화합물과 기능적 특성의 보존이 보장됩니다.

북미의 지속 가능한 단백질 가수분해물 시장은 2025년부터 2034년까지 연평균 7.8%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 이는 자연성, 투명성, 건강 효과를 중시하는 식물 유래 제품 및 클린 라벨 제품에 대한 소비자 인식이 높아진 데 따른 것입니다. 음료 및 식품 산업에서 단백질 가수분해물은 소화성, 무알러지 특성, 지속가능성 지향과의 적합성 때문에 단백질 가수분해물의 채택이 증가하고 있습니다. 효소 가수분해 기술 및 추출 기술의 혁신으로 제품의 품질, 생체 이용률, 기능성을 향상시켜 개인 맞춤형 영양 및 건강 솔루션 개발이 가능합니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 소스별

- 향후 시장 동향

- 특허 동향

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추산 및 예측 : 소스별, 2021-2034

- 주요 동향

- 식물 유래

- 대두 단백질 가수분해물

- 완두콩 단백질 가수분해물

- 밀 단백질 가수분해물

- 쌀 단백질 가수분해물

- 헴프 단백질 가수분해물

- 기타 식물 유래 원료

- 동물 유래

- 우유 단백질 가수분해물(유청, 카제인)

- 고기 단백질 가수분해물

- 해양성 단백질 가수분해물(생선, 콜라겐)

- 계란 단백질 가수분해물

- 곤충 유래 단백질 가수분해물

- 귀뚜라미 단백질 가수분해물

- 밀웜 단백질 가수분해물

- 동애등에 단백질 가수분해물

- 기타 곤충 유래 원료

- 기타

제6장 시장 추산 및 예측 : 형태별, 2021-2034

- 주요 동향

- 분말

- 액체

제7장 시장 추산 및 예측 : 가공 방법별, 2021-2034

- 주요 동향

- 효소 가수분해

- 알칼리 가수분해

- 기타

제8장 시장 추산 및 예측 : 용도별, 2021-2034

- 주요 동향

- 식품 및 음료

- 기능성 식품

- 단백질 바 및 스낵

- 음료 및 스무디

- 유아용 영양 제품

- 베이커리 및 제과

- 뉴트라슈티컬 및 식이보충제

- 스포츠 영양 제품

- 건강 보조 식품

- 의료용 식품

- 체중 관리 제품

- 동물 사료 및 반려동물 사료

- 가축 사료 용도

- 수산양식용 사료

- 반려동물 영양학

- 특수 반려동물 사료

- 화장품 및 퍼스널케어

- 안티에이징 제품

- 헤어케어 제제

- 스킨케어 용도

- 자외선 차단제 제품

- 의약품

- 약물 전달 시스템

- 치료용 단백질

- 창상 치유 제품

- 생리활성 펩티드

- 기타

제9장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 개요

- Actus Nutrition

- ADM

- Arla Foods Ingredients

- Cargill

- DSM-Firmenich

- Fonterra Co-operative Group

- FrieslandCampina Ingredients

- Glanbia Nutritionals

- Kemin Industries

- Kerry Group plc

- Roquette Freres

- Spryng

The Global Sustainable Protein Hydrolysates Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 9 billion by 2034.

Protein hydrolysates are bioactive peptides obtained through the enzymatic breakdown of sustainable protein sources. Industries are increasingly focusing on extracting proteins from plants, insects, and by-products to address the rising demand for environmentally conscious protein ingredients. These hydrolysates are gaining traction due to their superior bioavailability, functional properties, and health benefits, which align with the growing global emphasis on sustainability. Government initiatives promoting circular economy practices, such as the U.S. Department of Agriculture's Sustainable Agriculture Programs and the European Green Deal, are driving adoption across food, pharmaceuticals, and cosmetics. North America leads the market due to its advanced production infrastructure and supportive regulations, while Asia Pacific is emerging as the fastest-growing region, driven by large-scale investments in innovative processing technologies and strict sustainability policies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $9 Billion |

| CAGR | 7.8% |

The plant-based protein sources segment generated USD 2.9 billion in 2024 and dominated the market, reflecting a strong consumer shift toward plant-based nutrition and the availability of diverse protein sources suitable for hydrolysis. Legumes, grains, seeds, and other agricultural inputs provide a range of amino acid profiles and functional benefits, making them ideal for various applications.

The powdered protein hydrolysates segment held 70.5% share in 2024 owing to advantages in storage, transport, and flexibility for manufacturing. Long shelf-life powders with low moisture content simplify handling and dosing in food, nutraceutical, and animal feed formulations. Advances in spray drying, lyophilization, and other dehydration techniques ensure the preservation of bioactive compounds and functional properties during conversion from liquid to powder.

North America Sustainable Protein Hydrolysates Market will grow at a CAGR of 7.8% between 2025 and 2034, supported by rising consumer awareness of plant-based and clean-label products emphasizing naturalness, transparency, and health benefits. The food and beverage sector increasingly incorporates protein hydrolysates due to their digestibility, allergen-free nature, and alignment with sustainability preferences. Innovations in enzymatic hydrolysis and extraction technologies enhance product quality, bioavailability, and functional performance, enabling the development of personalized nutrition and wellness solutions.

Major players operating in the Global Sustainable Protein Hydrolysates Market include Actus Nutrition, ADM, Arla Foods Ingredients, Cargill, DSM-Firmenich, Fonterra Co-operative Group, FrieslandCampina Ingredients, Glanbia Nutritionals, Kemin Industries, Kerry Group plc, Roquette Freres, and Spryng. Companies in the Sustainable Protein Hydrolysates Market are focusing on strategies such as expanding production capacity, investing in R&D for new protein sources and improved hydrolysis processes, and forming strategic partnerships to enhance distribution networks. They are also emphasizing clean-label and allergen-free product development, entering emerging markets with high growth potential, adopting sustainable and circular economy practices in sourcing and manufacturing, and leveraging digital platforms for consumer engagement and product traceability. Additionally, product innovation aimed at personalized nutrition, functional foods, and nutraceutical applications is helping firms differentiate themselves and strengthen their market presence globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source trends

- 2.2.2 Form trends

- 2.2.3 Processing method trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing consumer demand for sustainable protein solutions

- 3.2.1.2 Regulatory push for circular economy practices

- 3.2.1.3 Technological advances in green processing methods

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment in sustainable processing technologies

- 3.2.2.2 Complex regulatory approval processes

- 3.2.3 Market opportunities

- 3.2.3.1 Untapped potential in insect-based protein hydrolysates

- 3.2.3.2 Waste valorization in food processing industry

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based

- 5.2.1 Soy protein hydrolysates

- 5.2.2 Pea protein hydrolysates

- 5.2.3 Wheat protein hydrolysates

- 5.2.4 Rice protein hydrolysates

- 5.2.5 Hemp protein hydrolysates

- 5.2.6 Other plant sources

- 5.3 Animal-based

- 5.3.1 Milk protein hydrolysates (whey, casein)

- 5.3.2 Meat protein hydrolysates

- 5.3.3 Marine protein hydrolysates (fish, collagen)

- 5.3.4 Egg protein hydrolysates

- 5.4 Insect-based protein hydrolysates

- 5.4.1 Cricket protein hydrolysates

- 5.4.2 Mealworm protein hydrolysates

- 5.4.3 Black soldier fly protein hydrolysates

- 5.4.4 Other insect sources

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid

Chapter 7 Market Estimates and Forecast, By Processing Method, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Enzymatic hydrolysis

- 7.3 Alkaline hydrolysis

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.2.1 Functional foods

- 8.2.2 Protein bars & snacks

- 8.2.3 Beverages & smoothies

- 8.2.4 Infant & baby nutrition

- 8.2.5 Bakery & confectionery

- 8.3 Nutraceuticals & dietary supplements

- 8.3.1 Sports nutrition products

- 8.3.2 Health supplements

- 8.3.3 Medical foods

- 8.3.4 Weight management products

- 8.4 Animal feed & pet food

- 8.4.1 Livestock feed applications

- 8.4.2 Aquaculture feed

- 8.4.3 Companion animal nutrition

- 8.4.4 Specialty pet foods

- 8.5 Cosmetics & personal care

- 8.5.1 Anti-aging products

- 8.5.2 Hair care formulations

- 8.5.3 Skin care applications

- 8.5.4 Sun care products

- 8.6 Pharmaceutical

- 8.6.1 Drug delivery systems

- 8.6.2 Therapeutic proteins

- 8.6.3 Wound healing products

- 8.6.4 Bioactive peptides

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Actus Nutrition

- 10.2 ADM

- 10.3 Arla Foods Ingredients

- 10.4 Cargill

- 10.5 DSM-Firmenich

- 10.6 Fonterra Co-operative Group

- 10.7 FrieslandCampina Ingredients

- 10.8 Glanbia Nutritionals

- 10.9 Kemin Industries

- 10.10 Kerry Group plc

- 10.11 Roquette Freres

- 10.12 Spryng

(주말 및 공휴일 제외)