|

시장보고서

상품코드

1892709

전기차 고속충전 배터리 화학 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Fast-Charging EV Battery Chemistries Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

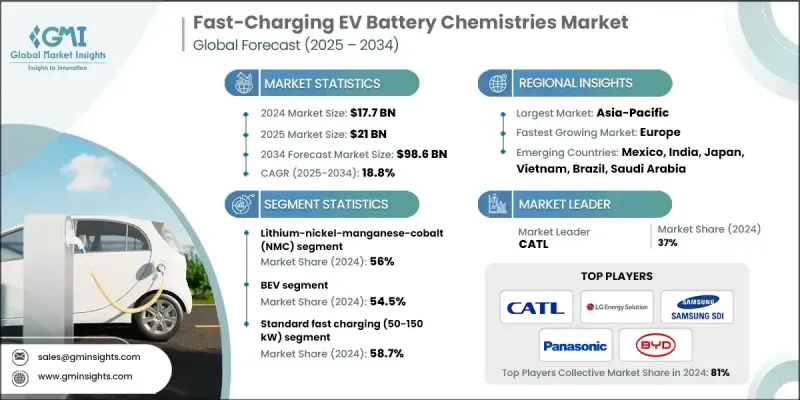

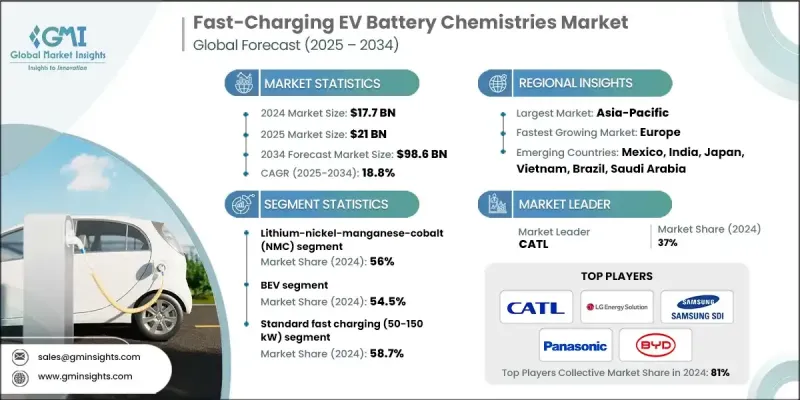

세계의 전기차 고속충전 배터리 화학 시장은 2024년에 177억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 18.8%로 성장하여 986억 달러에 이를 것으로 예측됩니다.

세계 각국 정부와 산업계가 온실가스 배출량 감축과 넷제로 목표 달성에 집중하고 있는 가운데, 전기자동차로의 빠른 전환이 주요 촉진요인으로 작용하고 있습니다. 운송 부문에서만 전 세계 배출량의 25% 이상을 차지하고 있어, EV의 보급은 단순한 소비자의 취향이 아닌 매우 중요한 필요성이 되고 있습니다. 전기차 보유 대수가 증가함에 따라 주행거리에 대한 불안감과 충전 인프라 부족으로 인해 10-30분 만에 10%에서 80%까지 충전할 수 있는 첨단 배터리 화학 기술에 대한 수요가 증가하고 있습니다. 350kW 이상의 시스템 및 800V 플랫폼과 같은 고전압 아키텍처를 포함한 초급속 충전 기술의 혁신으로 단 10-15분 만에 주행거리를 크게 향상시킬 수 있습니다. 이러한 추세는 리튬니켈망간코발트(NMC), 리튬인산철(LFP), 리튬니켈코발트알루미늄(NCA) 등 배터리 화학에 대한 투자를 촉진하고 있습니다. 이 배터리는 더 높은 효율, 더 긴 수명, 더 빠른 충전 시간을 제공할 수 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 177억 달러 |

| 예측 금액 | 986억 달러 |

| CAGR | 18.8% |

리튬-니켈-망간-코발트(NMC) 부문은 2024년 56%의 점유율을 차지했습니다. 전기자동차(EV)의 보급 확대와 리튬 비용의 하락으로 인해 급속 충전 능력으로 자동차 제조업체들이 널리 선호하는 NMC 배터리에 대한 수요가 가속화되고 있습니다.

배터리 전기자동차(BEV) 부문은 2024년 54.5%의 점유율을 차지했습니다. BEV는 대형 배터리 팩을 탑재하고, 충전 시간 단축에 대한 소비자의 기대가 높아지면서 급속 충전 대응 배터리 화학에 대한 수요를 견인하고 있습니다. 리튬 이온 배터리와 리튬 인산철(LFP) 배터리의 화학적 기술 발전으로 충전 속도, 에너지 저장 용량, 배터리 안전성이 향상되고 전체 수명이 연장되었습니다.

미국의 급속 충전 지원 EV용 배터리 화학물질 시장은 2024년 29억 달러에 달할 것으로 예측됩니다. 인플레이션 억제법(IRA) 등 정부 정책은 세제 혜택 제공과 국내 소재 사용 촉진을 통해 국내 생산을 가속화하고 있습니다. 이러한 노력은 자동차 제조업체들이 비용 절감과 지속가능성을 지원하기 위해 규제 준수 공급망 내에서 NMC, LFP 및 기타 첨단 급속 충전 지원 배터리 화학 물질에 집중하도록 유도하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 기술 로드맵과 진화

- 기술 도입 수명주기 분석

- 가격 동향

- 지역별

- 제품별

- 비용 내역 분석

- 특허 분석

- 소비자 인식과 보급 장벽

- 소비자 충전 시간에 대한 기대치와 허용 반응을 일으키는 최소의 물리량

- 항속거리 불안과 급속 충전 이용 가능성 트레이드 오프

- 급속 충전 기능에 대한 가격 프리미엄 수용도

- 배터리 열화 우려와 보증 기대

- 충전 인프라 접근성에 관한 인식

- 열열화와 안전성 분석

- 세계의 충전 규격 현황

- 전력 레벨 표준화

- 통신 프로토콜

- 메가와트 충전 시스템

- 표준화 갭과 상호운용성 과제

- 수명주기 비용 및 총 소유비용(TCO) 분석

- TCO 조사 방법과 전제조건

- 급속 충전 프리미엄 비용 분석

- 에너지 비용과 충전 효율

- 유지보수 및 교체 비용

- 사례 연구

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획과 자금조달

- 벤더 선정 기준

제5장 시장 추산 및 예측 : 배터리 화학별, 2021-2034

- 주요 동향

- Lithium Iron Phosphate (LFP)

- Lithium-Nickel-Manganese-Cobalt (NMC)

- Nickel-Cobalt-Aluminum (NCA)

- 기타

제6장 시장 추산 및 예측 : 파워트레인별, 2021-2034

- 주요 동향

- BEV(배터리 전기자동차)

- PHEV

- 하이브리드차(HEV)

제7장 시장 추산 및 예측 : 차량별, 2021-2034

- 주요 동향

- 승용차

- SUV

- 세단

- 해치백차

- 상용차

- LCV

- MCV

- 대형 상용차(HCV)

- 이륜차

제8장 시장 추산 및 예측 : 충전 기술별, 2021-2034

- 주요 동향

- 표준 급속 충전(50-150 kW)

- 초급속 충전(150 kW 이상)

제9장 시장 추산 및 예측 : 판매채널별, 2021-2034

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

제11장 기업 개요

- Global companies

- CATL

- LG Energy Solution

- Samsung SDI

- Panasonic Energy

- SK On

- BYD Company

- Tesla

- Farasis Energy

- BorgWarner

- Regional companies

- Northvolt

- CALB

- Gotion High-Tech

- Envision AESC

- EVE Energy

- Automotive Cells Company

- Emerging companies

- QuantumScape

- StoreDot

- Solid Power

- Sila Nanotechnologies

- Factorial Energy

- Enevate

- Amprius Technologies

- ProLogium Technology

- ONE

- Freyr Battery

- Cuberg

- Sunwoda Electronic

The Global Fast-Charging EV Battery Chemistries Market was valued at USD 17.7 billion in 2024 and is estimated to grow at a CAGR of 18.8% to reach USD 98.6 billion by 2034.

The rapid transition toward electric vehicles is a key driver, as governments and industries worldwide focus on reducing greenhouse gas emissions and supporting net-zero targets. The transportation sector alone accounts for over 25% of global emissions, making EV adoption a critical necessity rather than just a consumer preference. As EV ownership rises, range anxiety and limited charging infrastructure have pushed the demand for advanced battery chemistries capable of charging from 10% to 80% in 10-30 minutes. Innovations in ultra-fast charging technologies, including 350 kW+ systems and high-voltage architectures like 800V platforms, are enabling substantial range gains in just 10 to 15 minutes. This trend is propelling investments in battery chemistries such as lithium-nickel-manganese-cobalt (NMC), lithium iron phosphate (LFP), and lithium-nickel-cobalt-aluminum (NCA), which can deliver higher efficiency, longer life, and faster charge times.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.7 Billion |

| Forecast Value | $98.6 Billion |

| CAGR | 18.8% |

The lithium-nickel-manganese-cobalt (NMC) segment held a 56% share in 2024. Increasing EV adoption, combined with declining lithium costs, is accelerating demand for NMC batteries, which are widely preferred by automakers for their rapid charging capabilities.

The battery electric vehicle (BEV) segment held a 54.5% share in 2024. BEVs drive the need for fast-charging battery chemistries due to their larger battery packs and growing consumer expectations for reduced charging times. Advances in lithium-ion and LFP chemistries are enhancing charging speed, energy storage, and battery safety, while extending overall lifespan.

U.S. Fast-Charging EV Battery Chemistries Market reached USD 2.9 billion in 2024. Government policies, such as the Inflation Reduction Act (IRA), are accelerating domestic production by providing tax incentives and promoting the use of local materials. These initiatives are encouraging automakers to focus on NMC, LFP, and other advanced fast-charging battery chemistries within compliant supply chains to reduce costs and support sustainability.

Key players in the Global Fast-Charging EV Battery Chemistries Market include BYD, SK On, Factorial Energy, LG Energy Solution, CATL, Samsung SDI, BorgWarner, Panasonic, Farasis Energy, and EVE Energy. Companies in the Global Fast-Charging EV Battery Chemistries Market are strengthening their positions by investing heavily in R&D to improve energy density, safety, and charge speed. Strategic partnerships with automakers and technology firms help accelerate the commercialization of next-generation chemistries. Many are expanding production capacity in strategic regions to reduce logistics costs and meet local content requirements. Firms are also pursuing patents, licensing agreements, and joint ventures to secure supply chains for critical raw materials while focusing on sustainability and recycling initiatives to appeal to environmentally conscious consumers.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery Chemistry

- 2.2.3 Powertrain

- 2.2.4 Vehicle

- 2.2.5 Charging Technology

- 2.2.6 Sales Channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing consumer demand for reduced charging times

- 3.2.1.2 Government mandates for zero-emission vehicles

- 3.2.1.3 Expansion of high-power charging infrastructure networks

- 3.2.1.4 Declining battery costs enabling fast-charging adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Battery degradation & cycle life concerns with fast charging

- 3.2.2.2 Raw material supply constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Heavy-duty & commercial vehicle electrification

- 3.2.3.2 Extreme fast-charging technology development

- 3.2.3.3 Solid-state battery commercialization

- 3.2.3.4 Vehicle-to-grid (V2G) integration with fast-charging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology roadmaps & evolution

- 3.7.4 Technology adoption lifecycle analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Consumer perception & adoption barriers

- 3.11.1 Consumer charging time expectations & acceptance thresholds

- 3.11.2 Range anxiety vs fast-charging availability trade-off

- 3.11.3 Price premium willingness for fast-charging capability

- 3.11.4 Battery degradation concerns & warranty expectations

- 3.11.5 Charging infrastructure accessibility perception

- 3.12 Thermal degradation & safety analysis

- 3.12.1 Global charging standards landscape

- 3.12.2 Power level standardization

- 3.12.3 Communication protocols

- 3.12.4 Megawatt charging system

- 3.12.5 Standardization gaps & interoperability challenges

- 3.13 Life cycle cost & total cost of ownership (TCO) analysis

- 3.13.1 TCO methodology & assumptions

- 3.13.2 Fast-charging premium cost analysis

- 3.13.3 Energy costs & charging efficiency

- 3.13.4 Maintenance & replacement costs

- 3.14 Case studies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Battery Chemistry, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Lithium Iron Phosphate (LFP)

- 5.3 Lithium-Nickel-Manganese-Cobalt (NMC)

- 5.4 Nickel-Cobalt-Aluminum (NCA)

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Powertrain, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicles

- 7.2.1 SUVs

- 7.2.2 Sedans

- 7.2.3 Hatchbacks

- 7.3 Commercial Vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Two-wheelers

Chapter 8 Market Estimates & Forecast, By Charging Technology, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Standard Fast Charging (50-150 kW)

- 8.3 Ultra-Fast Charging (Above 150 kW)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.4.10 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 CATL

- 11.1.2 LG Energy Solution

- 11.1.3 Samsung SDI

- 11.1.4 Panasonic Energy

- 11.1.5 SK On

- 11.1.6 BYD Company

- 11.1.7 Tesla

- 11.1.8 Farasis Energy

- 11.1.9 BorgWarner

- 11.2 Regional companies

- 11.2.1 Northvolt

- 11.2.2 CALB

- 11.2.3 Gotion High-Tech

- 11.2.4 Envision AESC

- 11.2.5 EVE Energy

- 11.2.6 Automotive Cells Company

- 11.3 Emerging companies

- 11.3.1 QuantumScape

- 11.3.2 StoreDot

- 11.3.3 Solid Power

- 11.3.4 Sila Nanotechnologies

- 11.3.5 Factorial Energy

- 11.3.6 Enevate

- 11.3.7 Amprius Technologies

- 11.3.8 ProLogium Technology

- 11.3.9 ONE

- 11.3.10 Freyr Battery

- 11.3.11 Cuberg

- 11.3.12 Sunwoda Electronic