|

시장보고서

상품코드

1892748

자전거 변속기 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bicycle Derailleur Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

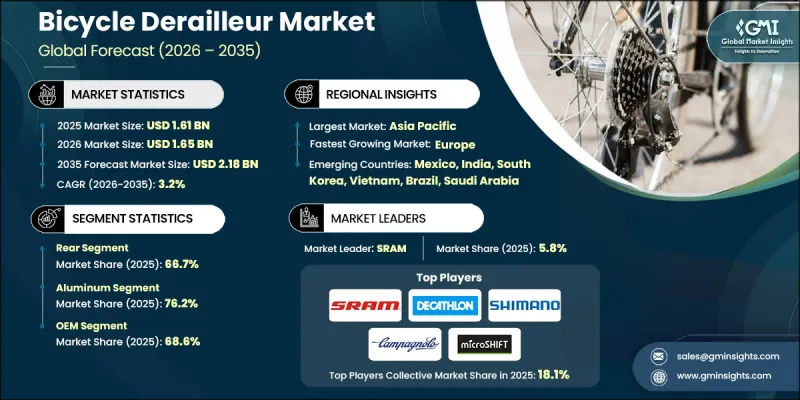

세계의 자전거 변속기 시장은 2025년에 16억 1,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.2%로 성장하여 21억 8,000만 달러에 이를 것으로 예측됩니다.

자전거 산업의 성장은 페달의 속도와 기어 전환을 관리하는 핵심 요소인 변속기를 포함한 첨단 부품에 대한 수요를 직접적으로 촉진하고 있습니다. 제조업체는 더 부드러운 변속, 유지 보수 감소, 성능 향상을 위해 경량화, 강도 향상, 고정밀화에 초점을 맞추었습니다. 전기 자전거, 자갈 자전거, 산악 자전거에 대한 관심이 높아지면서 더 높은 토크, 더 넓은 기어 범위, 거친 지형에 대응할 수 있는 변속기에 대한 수요가 증가하고 있습니다. 애프터마켓에서의 커스터마이징도 주요 촉진요인입니다. 사이클리스트들이 자신의 라이딩 스타일에 부합하고 자전거의 성능을 최적화하는 부품을 찾는 경향이 강해졌기 때문입니다. 이러한 추세는 내구성, 무게 효율성, 지속가능성을 향상시키면서도 합리적인 가격을 유지하기 위한 소재와 디자인의 지속적인 혁신으로 보완되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 16억 1,000만 달러 |

| 예측 금액 | 21억 8,000만 달러 |

| CAGR | 3.2% |

비용과 편의성은 시장 성장에 있어 매우 중요한 역할을 하고 있습니다. 변속기 제조업체는 가볍고 내구성이 뛰어나며 합리적인 가격의 부품을 개발하고 있습니다. 온라인 스토어와 자전거 매장에서 쉽게 구할 수 있어 라이더의 구매와 설치가 간편해졌습니다. 브랜드 간 경쟁으로 인해 제조업체들은 성능, 무게, 비용의 균형을 맞춘 알루미늄, 스틸, 복합소재의 변속기를 제공해야 하는 상황에 처해 있습니다. 환경에 대한 인식이 높아짐에 따라, 친환경에 대한 의식이 높은 소비자층에게 어필하기 위해 재생 소재의 사용을 장려하고 있습니다.

뒷변속기 부문은 2025년 66.7%의 점유율을 차지할 것으로 예상되며, 이는 다단 변속 시스템에서 뒷변속기의 중요성을 반영합니다. 변속 작업의 대부분은 리어 카세트에서 이루어지기 때문에 로드바이크, 산악자전거, 하이브리드 자전거, 자갈 자전거, 전기자전거, 전기자전거를 불문하고 뒷 변속기가 가장 널리 사용되고 있습니다. 한편, 앞 변속기는 점차 퇴출되고 있습니다.

알루미늄 부문은 철강 및 탄소섬유에 비해 비용 효율성, 내식성, 내구성이 뛰어나 2025년 76.2%의 점유율을 차지할 것으로 예측됩니다. 그러나 알루미늄 가격의 변동으로 인해 제조업체가 대체 소재를 고려해야 하는 경우도 종종 발생합니다.

미국 자전거 변속기 시장은 2025년 3억 4,320만 달러에 달할 것으로 예측됩니다. OEM 판매가 시장을 독점하고 있으며, 특히 로드바이크, 산악자전거, 전기자전거 분야에서는 주요 브랜드와 소매점에서 판매하는 신차에 대부분의 변속기가 사전 장착되어 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 기술 로드맵과 진화

- 기술 도입 수명주기 분석

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 특허 분석

- 소비자 인사이트와 행동 분석

- 고객 경험 매핑

- 사용자 과제점

- 프리미엄화 동향

- 구매 결정 동기 부여 요인

- 지속가능성과 순환형 경제 기회

- 재료 지속가능성

- 애프터마켓 재활용·재생 활용 기회

- 친환경 변속기 설계 프레임워크

- 전기자전거 모터 토크가 변속기 수명과 지속가능성에 미치는 영향

- OEM 파트너십 현황과 조달 전략

- 자전거 브랜드 조달 패턴

- OEM 선정 기준

- 변속기 브랜드의 전략적 조달 기회

- OEM와 공급업체 의존 리스크

- 시장 혼란 시나리오 분석

- 벨트 구동 시스템에의 이동

- 재료 부족 또는 탄소 가격 변동

- 세계의 자전거 보조금 프로그램 영향

- 지정학적 공급 리스크

- 제품 교환 및 고장 패턴 분석

- 자전거 유형별 교체율

- 마모 및 열화 특성

- 유지관리 빈도 매핑

- 조기 고장에 영향을 미치는 요인

- 최선 시나리오

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획과 자금조달

- 벤더 선정 기준

제5장 시장 추산 및 예측 : 제품별, 2022-2035

- 주요 동향

- Front

- Rear

제6장 시장 추산 및 예측 : 규모별, 2022-2035

- 주요 동향

- Short

- Medium

- Long Cage

제7장 시장 추산 및 예측 : 메커니즘별, 2022-2035

- 주요 동향

- 수동/기계식

- 전자기기

- 자동식

- 하이브리드

제8장 시장 추산 및 예측 : 재료별, 2022-2035

- 주요 동향

- 알루미늄

- 탄소섬유

- 강재

제9장 시장 추산 및 예측 : 자전거별, 2022-2035

- 주요 동향

- 로드 바이크

- 마운틴 바이크

- 하이브리드 바이크

- 전기 자전거

- 그래블바이크

제10장 시장 추산 및 예측 : 판매채널별, 2022-2035

- 주요 동향

- OEM

- 애프터마켓

제11장 시장 추산 및 예측 : 최종 용도별, 2022-2035

- 주요 동향

- 프로 사이클리스트

- 애호가

- 일반/통근 이용자

제12장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제13장 기업 개요

- Global companies

- Shimano

- SRAM

- Campagnolo

- MicroSHIFT

- Full Speed Ahead

- SunRace

- KMC Chain Industrial

- SR Suntour

- The Hive

- Decathlon

- Regional companies

- Box Components

- Cane Creek Cycling Components

- Paul Component Engineering

- Ritchey Design

- Gipiemme

- Garbaruk

- Wolf Tooth Components

- CeramicSpeed

- Emerging companies

- ROTOR

- L-TWOO Sports Technology

- WHEELTOP

- Praxis Cycles

- Gevenalle

- Archer Components

- Sensah

- S-Ride

The Global Bicycle Derailleur Market was valued at USD 1.61 billion in 2025 and is estimated to grow at a CAGR of 3.2% to reach USD 2.18 billion by 2035.

The growth of the bicycle industry has directly fueled the demand for advanced components, with derailleurs being a critical element that manages pedal speed and gear transitions. Manufacturers are focusing on creating lighter, stronger, and more precise derailleurs to provide smoother shifting, reduced maintenance, and enhanced performance. Rising interest in e-bikes, gravel bikes, and mountain biking has increased demand for derailleurs that can handle higher torque, broader gear ranges, and challenging terrain. Aftermarket customization is another major driver, as cyclists increasingly seek components that match their riding style and optimize bike performance. These trends are complemented by the continuous innovation in materials and design to improve durability, weight efficiency, and sustainability while maintaining affordability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.61 Billion |

| Forecast Value | $2.18 Billion |

| CAGR | 3.2% |

Cost and convenience play a pivotal role in market growth. Derailleur makers are developing components that are lightweight, long-lasting, and budget-friendly. Easy availability through online stores and bicycle shops simplifies purchase and installation for riders. Brand competition has pushed manufacturers to offer aluminum, steel, and composite derailleurs that balance performance, weight, and cost. Growing environmental awareness is encouraging the use of recycled materials to appeal to eco-conscious consumers.

The rear derailleur segment held 66.7% share in 2025, reflecting its essential role in multi-gear drivetrains. Most shifting occurs at the rear cassette, making rear derailleurs the most widely used across road, mountain, hybrid, gravel, and e-bikes, while front derailleurs are gradually being phased out.

The aluminum segment held a 76.2% share in 2025, due to its cost-effectiveness, corrosion resistance, and durability compared to steel or carbon fiber. However, fluctuations in aluminum pricing occasionally push manufacturers to explore alternative materials.

U.S. Bicycle Derailleur Market reached USD 343.2 million in 2025. OEM sales dominate the market, as most derailleurs are pre-installed on new bicycles sold by major brands and retailers, particularly in road, mountain, and e-bike segments.

Leading companies in the Bicycle Derailleur Market include SRAM, Decathlon, Shimano, Campagnolo, MicroSHIFT, SunRace, FSA, KMC Chain Industrial, SR Suntour, and The Hive. To strengthen their Bicycle Derailleur Market presence, companies are focusing on continuous product innovation by developing lighter, more precise, and durable derailleurs suited for high-performance cycling. Expanding distribution through online and retail channels improves accessibility, while investment in R&D ensures adaptation to evolving biking trends such as e-bikes and gravel/mountain riding. Brands also emphasize sustainability by using recycled and eco-friendly materials. Strategic partnerships and OEM collaborations help secure long-term contracts and visibility among global bicycle manufacturers. Additionally, aftermarket customization options cater to enthusiasts, increasing brand loyalty and driving repeat purchases.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Size

- 2.2.4 Mechanism

- 2.2.5 Material

- 2.2.6 Bicycle

- 2.2.7 Sales Channel

- 2.2.8 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global cycling participation growth

- 3.2.1.2 E-bike market expansion & integration

- 3.2.1.3 Technology advancement in electronic shifting

- 3.2.1.4 Urban mobility & commuting trends

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of premium electronic systems

- 3.2.2.2 Material cost inflation

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets development

- 3.2.3.2 Wireless electronic system democratization

- 3.2.3.3 Sustainability & circular economy integration

- 3.2.3.4 Direct-to-consumer distribution models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology roadmaps & evolution

- 3.7.4 Technology adoption lifecycle analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Patent analysis

- 3.11 Consumer insights & behavioral intelligence

- 3.11.1 Customer experience mapping

- 3.11.2 User pain points

- 3.11.3 Premiumization trend

- 3.11.4 Purchase decision motivators

- 3.12 Sustainability & circular economy opportunities

- 3.12.1 Material sustainability

- 3.12.2 Recycling & refurbishing opportunities in aftermarket

- 3.12.3 Eco-friendly derailleur design frameworks

- 3.12.4 Impact of e-bike motor torque on derailleur lifespan & sustainability

- 3.13 OEM partnership landscape & sourcing strategies

- 3.13.1 Bicycle brand sourcing patterns

- 3.13.2 OEM selection criteria

- 3.13.3 Strategic sourcing opportunities for derailleur brands

- 3.13.4 OEM-supplier dependency risks

- 3.14 Market disruption scenario analysis

- 3.14.1 Shift to belt-drive systems

- 3.14.2 Material shortage or carbon price volatility

- 3.14.3 Impact of global cycling subsidy programs

- 3.14.4 Geopolitical supply risk

- 3.15 Product replacement & failure pattern analysis

- 3.15.1 Replacement rates by bike type

- 3.15.2 Wear & tear characteristics

- 3.15.3 Maintenance frequency mapping

- 3.15.4 Factors influencing early failure

- 3.16 Best case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Front

- 5.3 Rear

Chapter 6 Market Estimates & Forecast, By Size, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Short

- 6.3 Medium

- 6.4 Long Cage

Chapter 7 Market Estimates & Forecast, By Mechanism, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Manual/Mechanical

- 7.3 Electronic

- 7.4 Automatic

- 7.5 Hybrid

Chapter 8 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Aluminum

- 8.3 Carbon fiber

- 8.4 Steel

Chapter 9 Market Estimates & Forecast, By Bicycle, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Road bikes

- 9.3 Mountain bikes

- 9.4 Hybrid bikes

- 9.5 E-bikes

- 9.6 Gravel Bikes

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 Professional Cyclists

- 11.3 Enthusiasts

- 11.4 General/Commuter Users

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.3.8 Benelux

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 ANZ

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global companies

- 13.1.1 Shimano

- 13.1.2 SRAM

- 13.1.3 Campagnolo

- 13.1.4 MicroSHIFT

- 13.1.5 Full Speed Ahead

- 13.1.6 SunRace

- 13.1.7 KMC Chain Industrial

- 13.1.8 SR Suntour

- 13.1.9 The Hive

- 13.1.10 Decathlon

- 13.2 Regional companies

- 13.2.1 Box Components

- 13.2.2 Cane Creek Cycling Components

- 13.2.3 Paul Component Engineering

- 13.2.4 Ritchey Design

- 13.2.5 Gipiemme

- 13.2.6 Garbaruk

- 13.2.7 Wolf Tooth Components

- 13.2.8 CeramicSpeed

- 13.3 Emerging companies

- 13.3.1 ROTOR

- 13.3.2 L-TWOO Sports Technology

- 13.3.3 WHEELTOP

- 13.3.4 Praxis Cycles

- 13.3.5 Gevenalle

- 13.3.6 Archer Components

- 13.3.7 Sensah

- 13.3.8 S-Ride