|

시장보고서

상품코드

1892799

에톡실레이트 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Ethoxylates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

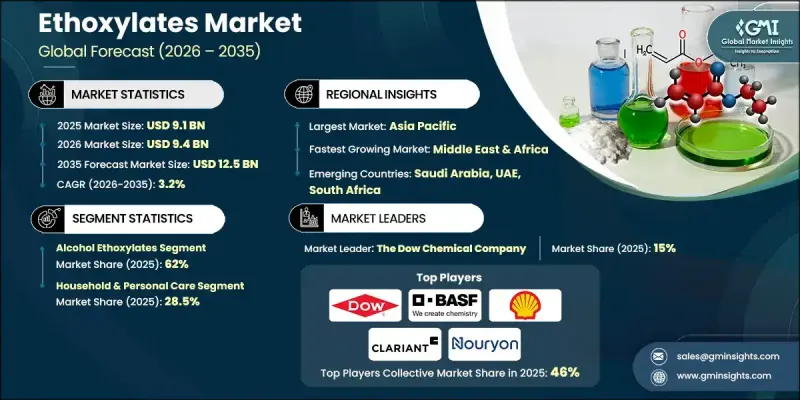

세계의 에톡실레이트 시장은 2025년에 91억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 3.2%를 나타내 125억 달러에 이를 것으로 예측됩니다.

에톡실레이트 산업은 광범위한 산업용 및 소비자용도에서 매우 중요한 역할을 합니다. 시장 평가에는 생산 동향, 가격 패턴, 지역별 소비량 및 여러 제품군 및 용도에 대한 수요가 포함됩니다. 성장은 보다 광범위한 화학 산업의 혁신을 기반으로 개인 관리, 농약 및 산업 제조 분야의 확대와 밀접하게 연동하고 있습니다. 유통은 확립된 화학 제조 기지, 농업 활동, 견조한 소비재 산업을 통해 아시아태평양, 북미, 유럽에 고도로 집중하고 있습니다. 중동, 아프리카, 라틴아메리카의 신흥 시장에서는 증가하는 소비자 수요에 대응하기 위해 국내 생산이 확대되어 성장에 기여하고 있습니다. 이로 인해 세계공급과 소비가 점차 다양해지고 있습니다. 알코올 에톡실레이트는 성능 효율, 규제 준수, 비용 우위로부터 주류를 차지하고 있지만, 특수 등급은 기술 사양에 따라 프리미엄 가격이 설정되어 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 가치 | 91억 달러 |

| 예측 금액 | 125억 달러 |

| CAGR | 3.2% |

알코올 에톡실레이트 부문은 2025년에 62%의 점유율을 차지했고 2035년까지 연평균 복합 성장률(CAGR) 2.7%를 나타낼 것으로 예측됩니다. 탁월한 유화성 및 세척 특성으로 대부분의 세척제 및 개인 관리 제품의 주요 성분으로 사용됩니다. 지방 아민계 에톡실레이트는 농약의 확산과 침투성을 증가시키기 때문에 농약 용도에서 여전히 필수적입니다. 게다가, 메틸 에스터계 에톡실레이트는 화장품 및 산업용 분야에서 저자극성과 환경적 이점을 겸비한 지속가능한 대안으로 부상하고 있습니다.

가정용 및 퍼스널케어 용도 부문은 2025년에 28.5%의 점유율을 차지했고, 2026년부터 2035년에 걸쳐 CAGR 2.6%를 나타낼 것으로 전망되고 있습니다. 에톡실레이트는 샴푸, 세척제, 스킨케어 제품에서 유화, 세척, 배합 안정성에 필수적입니다. 농약 분야에서 에톡실레이트는 정밀 농업에서 농약의 효능을 높이는 습윤제 역할을 합니다. 업스트림의 석유 및 가스 분야에서는 굴삭 유체 첨가제나 해유제로서 이용되어 추출 프로세스의 운용 신뢰성을 향상시킵니다.

북미의 에톡실레이트 시장은 2025년 19.7%의 점유율을 차지하며 급속히 확대되었습니다. 첨단 화학 제조 능력과 강력한 지속가능성 규제로 지역은 전략적 성장 기지가 되었습니다. 환경규제에 적합한 제제 및 특수화학제품의 혁신에 대한 수요는 산업용도를 목표로 하는 고성능 에톡실레이트에 기회를 가져왔습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 친환경 계면활성제에 대한 수요 증가

- 소비자의 기호의 변화

- 브랜드의 지속가능성에 대한 노력

- 업계의 잠재적 위험 및 과제

- APE/NPE에 관한 환경 문제

- 수생독성

- 시장 기회

- 바이오베이스 에톡실레이트 시장 확대

- 특수 에톡실레이트 제품 개발

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술 및 혁신 현황

- 현재 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 확대 계획

제5장 시장 추계·예측 : 제품별(2022-2035년)

- 알코올 에톡실레이트

- 천연 알코올 에톡실레이트

- 합성 알코올 에톡실레이트

- 직쇄형 알코올 에톡실레이트(LAE)

- 분지형 알코올 에톡실레이트(BAE)

- 지방 아민 에톡실레이트

- 지방산 에톡실레이트

- 메틸 에스터 에톡실레이트(MEE)

- 글리세라이드 에톡실레이트

- 알킬페놀 에톡실레이트(APEs)

- 노닐페놀 에톡실레이트(NPEs)

- 옥틸페놀 에톡실레이트(OPEs)

- 기타

- 탄산염 에톡실레이트(CO2 베이스)

- 효소 생산 에톡실레이트

- 고순도 제약 등급 에톡실레이트

제6장 시장 추계·예측 : 용도별(2022-2035년)

- 가정용 및 퍼스널케어

- 세탁 및 식기 세척 세제

- 산업용 및 기관용 세정제

- 퍼스널케어

- 농약

- 제초제

- 살균제

- 살충제

- 비료 및 미량 영양소

- 석유 및 가스

- 증진유전회수(EOR)

- 거품 제어 및 습윤제

- 윤활제 및 유화제

- 유화분리

- 제약

- 약물 용해화 및 전달

- 바이오의약품 및 바이오시밀러

- 부형제 및 유화제

- 의료기기 살균(에틸렌옥사이드 관련)

- 섬유가공

- 세척 및 습윤 처리

- 염색 및 후가공

- 페인트 및 코팅

- 에멀젼 중합

- 습윤제 및 분산제

- 보호 코팅

- 건축용 코팅

- 산업용 코팅

- 펄프 및 제지

- 탈잉크제

- 분산제

- 소포제

- 가죽 가공

- 기타

제7장 시장 추계·예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제8장 기업 프로파일

- BASF SE

- Royal Dutch Shell PLC

- The Dow Chemical Company

- Clariant AG

- Nouryon

- Huntsman International LLC

- Sasol Limited

- Stepan Company

- Evonik Industries AG

- Solvay SA

- INEOS Group Limited

- Croda International PLC

- Arkema SA

- SABIC(Saudi Basic Industries Corporation)

The Global Ethoxylates Market was valued at USD 9.1 billion in 2025 and is estimated to grow at a CAGR of 3.2% to reach USD 12.5 billion by 2035.

The ethoxylates industry plays a pivotal role across a wide range of industrial and consumer applications. Market evaluation includes production trends, pricing patterns, regional consumption, and demand across multiple product families and applications. Growth is closely aligned with the expansion of personal care, agrochemical, and industrial manufacturing sectors, underpinned by innovations in the broader chemicals industry. Distribution is highly concentrated in Asia-Pacific, North America, and Europe due to established chemical manufacturing bases, agricultural activity, and robust consumer goods industries. Emerging markets in the Middle East, Africa, and Latin America are contributing to growth as domestic production scales up to meet increasing consumer demand, gradually diversifying global supply and consumption. Alcohol ethoxylates dominate due to performance efficiency, regulatory compliance, and cost advantages, while specialty grades command premium pricing for technical specifications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.1 Billion |

| Forecast Value | $12.5 Billion |

| CAGR | 3.2% |

The alcohol ethoxylates segment held a 62% share in 2025 and is projected to grow at a CAGR of 2.7% through 2035. They serve as key ingredients in most cleaning and personal care formulations due to their excellent emulsifying and detergent properties. Fatty amine ethoxylates remain essential in agrochemical applications for enhancing pesticide spreading and penetration. Additionally, methyl ester ethoxylates are emerging as a sustainable alternative, combining mildness for cosmetic and industrial uses with ecological advantages.

The household and personal care applications segment held a 28.5% share in 2025, with expected growth at a CAGR of 2.6% from 2026 to 2035. Ethoxylates are critical for emulsification, cleansing, and formulation stability in shampoos, cleansers, and skincare products. In agrochemicals, ethoxylates act as wetting agents that improve pesticide efficacy in precision farming. In upstream oil and gas, they are utilized as additives in drilling fluids and demulsifiers, enhancing operational reliability in extraction processes.

North America Ethoxylates Market accounted for a 19.7% share in 2025 and is expanding rapidly. Advanced chemical manufacturing capabilities and strong sustainability regulations make the region a strategic growth hub. Demand for environmentally compliant formulations and specialty chemical innovations provides opportunities for high-performance ethoxylates targeting industrial applications.

Key players in the Global Ethoxylates Market include BASF SE, Arkema SA, Croda International PLC, INEOS Group Limited, Clariant AG, The Dow Chemical Company, Evonik Industries AG, Huntsman International LLC, Nouryon, Royal Dutch Shell PLC, Sasol Limited, Solvay SA, and Stepan Company. Companies in the Global Ethoxylates Market are strengthening their position through multiple strategies. They are investing in research and development to create high-performance and sustainable formulations, expanding production facilities in strategic regions to reduce lead times, and diversifying product portfolios to meet sector-specific needs. Partnerships with end-user industries and distributors enhance market reach, while a focus on regulatory compliance and eco-friendly innovations ensures long-term competitiveness. Firms are also leveraging digitalization and advanced analytics for supply chain optimization and cost efficiency, ensuring timely delivery and improved customer satisfaction across industrial and consumer segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for eco-friendly surfactants

- 3.2.1.2 Consumer preference shift

- 3.2.1.3 Brand sustainability commitments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental concerns regarding APEs/NPEs

- 3.2.2.2 Aquatic toxicity

- 3.2.3 Market opportunities

- 3.2.3.1 Bio-based ethoxylates market expansion

- 3.2.3.2 Specialty ethoxylates development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Alcohol ethoxylates

- 5.2.1 Natural alcohol ethoxylates

- 5.2.2 Synthetic alcohol ethoxylates

- 5.2.3 Linear alcohol ethoxylates (LAE)

- 5.2.4 Branched alcohol ethoxylates (BAE)

- 5.3 Fatty amine ethoxylates

- 5.4 Fatty acid ethoxylates

- 5.5 Methyl ester ethoxylates (MEE)

- 5.6 Glyceride ethoxylates

- 5.7 Alkylphenol ethoxylates (APEs)

- 5.7.1 Nonylphenol ethoxylates (NPEs)

- 5.7.2 Octylphenol ethoxylates (OPEs)

- 5.8 Others

- 5.8.1 Carbonate ethoxylates (CO2-based)

- 5.8.2 Enzymatically produced ethoxylates

- 5.8.3 High-Purity pharmaceutical-grade ethoxylates

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Household & personal care

- 6.2.1 Laundry & dishwashing detergent

- 6.2.2 Industrial & institutional cleaning

- 6.2.3 Personal care

- 6.3 Agrochemicals

- 6.3.1 Herbicides

- 6.3.2 Fungicides

- 6.3.3 Insecticides

- 6.3.4 Fertilizers & micronutrients

- 6.4 Oil & gas

- 6.4.1 Enhanced oil recovery (EOR)

- 6.4.2 Foam control & wetting agents

- 6.4.3 Lubricants & emulsifiers

- 6.4.4 Demulsification

- 6.5 Pharmaceuticals

- 6.5.1 Drug solubilization & delivery

- 6.5.2 Biologics & biosimilars

- 6.5.3 Excipients & emulsifiers

- 6.5.4 Medical device sterilization (EtO-related)

- 6.6 Textile processing

- 6.6.1 Scouring & wetting

- 6.6.2 Dyeing & finishing

- 6.7 Paints & coatings

- 6.7.1 Emulsion polymerization

- 6.7.2 Wetting & dispersing agents

- 6.7.3 Protective coatings

- 6.7.4 Architectural coatings

- 6.7.5 Industrial coatings

- 6.8 Pulp & paper

- 6.8.1 Deinking agents

- 6.8.2 Dispersing agents

- 6.8.3 Defoamers

- 6.9 Leather processing

- 6.10 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 BASF SE

- 8.2 Royal Dutch Shell PLC

- 8.3 The Dow Chemical Company

- 8.4 Clariant AG

- 8.5 Nouryon

- 8.6 Huntsman International LLC

- 8.7 Sasol Limited

- 8.8 Stepan Company

- 8.9 Evonik Industries AG

- 8.10 Solvay SA

- 8.11 INEOS Group Limited

- 8.12 Croda International PLC

- 8.13 Arkema SA

- 8.14 SABIC (Saudi Basic Industries Corporation)