|

시장보고서

상품코드

1892807

자동차 메모리 반도체 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Memory Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

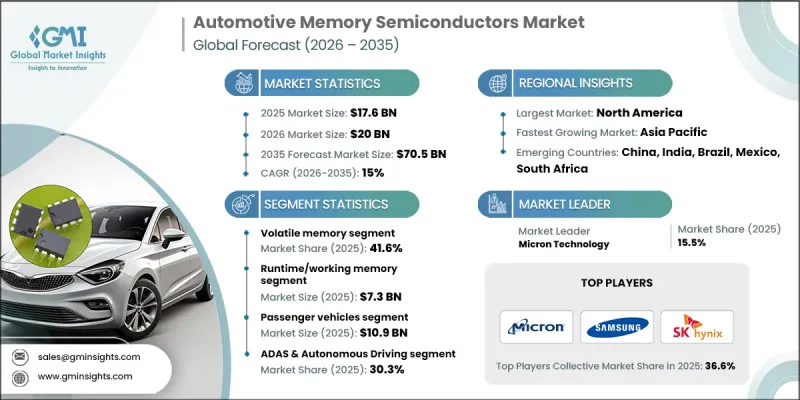

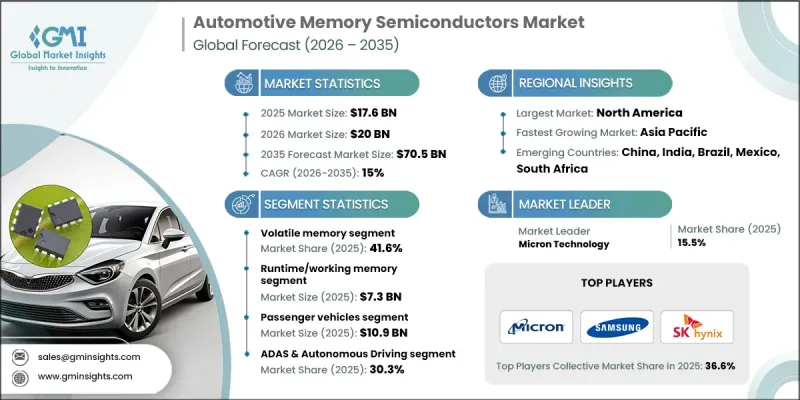

세계의 자동차 메모리 반도체 시장은 2025년에 176억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 15%로 성장하여 705억 달러에 이를 것으로 예측됩니다.

첨단 자동차용 일렉트로닉스에 대한 수요 증가, 전기차 생산 확대, 커넥티드 모빌리티 시스템의 급속한 보급으로 업계는 강력한 성장세를 보이고 있습니다. 이러한 부품들은 ADAS, 차량용 엔터테인먼트 플랫폼, 진화하는 자율주행 기능에서 필수 불가결한 요소로 자리 잡고 있습니다. 지능형 센서와 고속 데이터 처리에 대한 의존도가 높아짐에 따라, 차세대 차량에서 실시간 워크로드를 지원할 수 있는 메모리의 필요성이 가속화되고 있습니다. 자동화가 진행됨에 따라 차량에는 대용량화, 저지연화, 장기 내구성을 실현하는 메모리 아키텍처가 요구되고 있습니다. 이러한 변화로 인해 제조업체들은 엄격한 안전 및 신뢰성 기준을 충족하는 자동차 등급 부품 개발을 추진하고 있습니다. 또한, 전기차 및 하이브리드 모델로의 전환 가속화도 큰 기회를 창출하고 있습니다. 전동화 차량은 복잡한 전자 제어 장치와 배터리 관리 시스템에 의존하고 있으며, 안전, 효율성 및 시스템 작동을 지속적으로 모니터링하기 위해서는 고성능 메모리가 필수적이기 때문입니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 176억 달러 |

| 예측 금액 | 705억 달러 |

| CAGR | 15% |

2025년 휘발성 메모리 부문은 41.6%의 점유율을 차지할 것으로 예측됩니다. 그 중요성은 현대 자동차의 실시간 작동 및 단기 데이터 부하 처리에서 핵심적인 기능을 수행한다는 데서 비롯됩니다. 주요 휘발성 메모리인 DRAM은 차량 센서, 인포테인먼트 컨트롤러, 에너지 관리 장치, 기타 미션 크리티컬한 모듈 간의 빠른 상호 작용을 가능하게 합니다. 속도, 반응성, 최적화된 전력 사용량은 지능형 커넥티드 차량 플랫폼에 필수적인 요소입니다.

런타임 메모리(작업 메모리) 부문은 2025년 7.3억 달러에 달할 것으로 예측됩니다. 이 부문이 지배적인 위치를 차지하는 이유는 전자 제어 장치, 커넥티비티 시스템, 배터리 모니터링 모듈, 첨단 안전 기술 등에서 즉각적인 데이터 통신과 관련된 가장 까다로운 처리 작업을 수행하기 때문입니다. DRAM은 높은 성능과 안정성으로 인해 런타임 메모리의 기반으로서 중요한 역할을 계속하고 있습니다. 전기자동차(EV), 자율주행 시스템, 통합 커넥티비티 기능의 보급 확대가 이 카테고리의 견고한 수요를 뒷받침하고 있습니다.

북미 자동차 메모리 반도체 시장은 2025년 27.5%의 점유율을 차지할 것으로 예측됩니다. 이 지역에서는 전기차와 자율주행 기술의 보급 확대와 지능형 자동차 플랫폼의 강력한 채택에 힘입어 괄목할 만한 진전을 보이고 있습니다. 첨단 반도체 엔지니어링, 대규모 제조 능력, 메모리 기술 제공 업체의 투자 증가가 결합되어 시장 확장을 강화하고 있습니다. 전기 모빌리티 및 차세대 자동차 혁신에 대한 정책적 지원이 성장을 더욱 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 과거 가격 분석(2022-2024)

- 가격 동향 요인

- 지역별 가격변동

- 가격 예측(2026-2035)

- 가격 전략

- 신흥 비즈니스 모델

- 컴플라이언스 요건

- 지속가능성 대책

- 지속가능한 재료 평가

- 탄소발자국 분석

- 순환형 경제 도입

- 지속가능성 인증과 기준

- 지속가능성 ROI 분석

- 세계 소비자 심리분석

- 특허 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 시장 집중도 분석

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무 실적 비교

- 매출

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인 폭

- 기술

- 혁신

- 지역 존재감 비교

- 세계 전개 분석

- 서비스 네트워크 커버율

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더 기업

- 챌린저

- 팔로워

- 니치 기업

- 전략적 전망 매트릭스

- 재무 실적 비교

- 주요 발전, 2022-2025

- 인수합병(M&A)

- 제휴 및 협력 관계

- 기술적 진보

- 확대와 투자 전략

- 지속가능성 이니셔티브

- 디지털 전환 대처

- 신흥/스타트업 경쟁 동향

제5장 시장 추산 및 예측 : 기술별, 2022-2035

- 주요 동향

- 휘발성 메모리

- DRAM

- SRAM

- 비휘발성 메모리(NVM)

- NOR 플래시

- 낸드플래시

- EEPROM/NVRAM

- 신흥/첨단 메모리

- MRAM

- FRAM

- ReRAM/PCM

- 자동차용 관리 메모리 솔루션

제6장 시장 추산 및 예측 : 기능별 역할, 2022-2035

- 주요 동향

- 시행 환경 및 워킹메모리

- 코드 스토리지

- 데이터 스토리지

제7장 시장 추산 및 예측 : 차종별, 2022-2035

- 주요 동향

- 승용차

- 소형 상용차

- 대형 상용차

제8장 시장 추산 및 예측 : 용도별, 2022-2035

- 주요 동향

- ADAS 및 자율주행

- 인포테인먼트 및 디지털 콕핏

- 파워트레인 및 배터리 관리

- 보디, 섀시 및 안전 전자기기

- 계기 클러스터 및 디스플레이 시스템

- 기타

제9장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

제10장 기업 개요

- Everspin Technologies

- GigaDevice Semiconductor

- Infineon Technologies

- Integrated Silicon Solution(ISSI)

- Kingston Technology

- Kioxia Holdings

- Macronix International

- Micron Technology

- Powerchip Technology

- Renesas Electronics

- Samsung Electronics

- SK hynix

- Swissbit

- Transcend Information

- Western Digital

The Global Automotive Memory Semiconductors Market was valued at USD 17.6 billion in 2025 and is estimated to grow at a CAGR of 15% to reach USD 70.5 billion by 2035.

The industry is experiencing strong momentum driven by rising demand for sophisticated automotive electronics, increasing production of electric vehicles, and the rapid emergence of connected mobility systems. These components are becoming essential in advanced driver-assistance features, in-vehicle entertainment platforms, and evolving autonomous functions. Growing reliance on intelligent sensors and high-speed data processing fuels the need for memory capable of supporting real-time workloads in next-generation vehicles. As automation scales, vehicles require memory architectures that deliver higher capacity, reduced latency, and long-term durability. This shift encourages manufacturers to develop automotive-grade components built to meet rigorous safety and reliability criteria. The accelerating transition toward EVs and hybrid models is also creating significant opportunities, as electrified vehicles depend on complex electronic control units and battery management systems that rely on high-performance memory for continuous monitoring of safety, efficiency, and system behavior.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.6 Billion |

| Forecast Value | $70.5 Billion |

| CAGR | 15% |

The volatile memory segment accounted for 41.6% share in 2025. Its prominence stems from its central function in handling real-time operations and short-term data loads within modern vehicles. DRAM, the primary volatile memory, enables rapid interaction between vehicle sensors, infotainment controllers, energy-management units, and other mission-critical modules. Its speed, responsiveness, and optimized power usage make it fundamental to intelligent, connected vehicle platforms.

The runtime or working memory segment reached USD 7.3 billion in 2025. This segment dominates because it performs the most demanding processing tasks tied to immediate data communication across electronic control units, connectivity systems, battery oversight modules, and advanced safety technologies. DRAM continues to serve as the backbone of runtime memory due to its high performance and stability. Expanding use of EVs, automated driving systems, and integrated connectivity features continues to support strong demand in this category.

North America Automotive Memory Semiconductors Market held a 27.5% share in 2025. The region is witnessing substantial progress fueled by the widespread adoption of electric and automated vehicle technologies and strong uptake of intelligent car platforms. A combination of advanced semiconductor engineering, large-scale manufacturing strength, and increased investment from memory technology providers is reinforcing market expansion. Policy support for electric mobility and next-generation automotive innovation further accelerates growth.

Key companies active in the Global Automotive Memory Semiconductors Market include Everspin Technologies, Infineon Technologies, Kingston Technology, GigaDevice Semiconductor, Kioxia Holdings, Macronix International, Micron Technology, Integrated Silicon Solution (ISSI), Renesas Electronics, Powerchip Technology, SK hynix, Swissbit, Samsung Electronics, Western Digital, and Transcend Information. Key strategies used by companies in the Global Automotive Memory Semiconductors Market center on enhancing performance capabilities, expanding product durability, and strengthening partnerships across the automotive ecosystem. Many firms are investing in advanced fabrication technologies to boost endurance, reduce latency, and support high-bandwidth applications required by automated and electric vehicles. Companies are also prioritizing automotive-grade qualification standards to improve reliability under extreme conditions. Collaborations with OEMs and Tier-1 suppliers are expanding to ensure seamless integration of memory solutions into complex vehicle architectures. Additionally, businesses are diversifying memory portfolios, optimizing power efficiency, and scaling production capacity to meet rising global demand while improving their competitive position.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Technologies trends

- 2.2.2 Functional Role trends

- 2.2.3 Vehicle Type trends

- 2.2.4 Application trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of Advanced Driver Assistance Systems (ADAS) and autonomous driving

- 3.2.1.2 Growing vehicle electrification (EVs and HEVs)

- 3.2.1.3 Integration of infotainment and connected car systems

- 3.2.1.4 Advancements in automotive-grade memory

- 3.2.1.5 Expansion of vehicle-to-everything (V2X) communication

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and qualification costs of automotive-grade semiconductors

- 3.2.2.2 Rapid technology evolution

- 3.2.3 Market opportunities

- 3.2.4 Emergence of Software-Defined Vehicles (SDVs)

- 3.2.5 Edge AI and Machine Learning in Vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability roi analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technologies, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Volatile Memory

- 5.2.1 DRAM

- 5.2.2 SRAM

- 5.3 Non-Volatile Memory (NVM)

- 5.4 NOR Flash

- 5.5 NAND Flash

- 5.6 EEPROM / NVRAM

- 5.7 Emerging / Advanced Memory

- 5.8 MRAM

- 5.9 FRAM

- 5.10 ReRAM / PCM

- 5.11 Automotive Managed Memory Solutions

Chapter 6 Market Estimates and Forecast, By Functional Role, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Runtime / Working Memory

- 6.3 Code Storage

- 6.4 Data Storage

Chapter 7 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Passenger Vehicles

- 7.3 Light Commercial Vehicles

- 7.4 Heavy Commercial Vehicles

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 ADAS & Autonomous Driving

- 8.3 Infotainment & Digital Cockpit

- 8.4 Powertrain & Battery Management

- 8.5 Body, Chassis & Safety Electronics

- 8.6 Instrument Cluster & Display Systems

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Everspin Technologies

- 10.2 GigaDevice Semiconductor

- 10.3 Infineon Technologies

- 10.4 Integrated Silicon Solution (ISSI)

- 10.5 Kingston Technology

- 10.6 Kioxia Holdings

- 10.7 Macronix International

- 10.8 Micron Technology

- 10.9 Powerchip Technology

- 10.10 Renesas Electronics

- 10.11 Samsung Electronics

- 10.12 SK hynix

- 10.13 Swissbit

- 10.14 Transcend Information

- 10.15 Western Digital