|

시장보고서

상품코드

1892830

상업용 해초 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Commercial Seaweed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

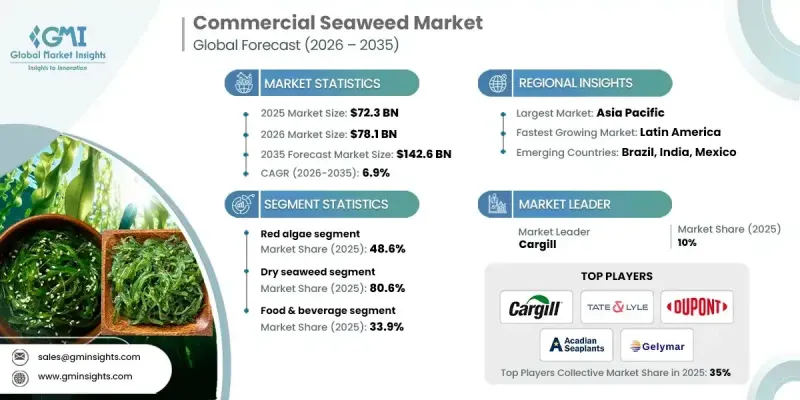

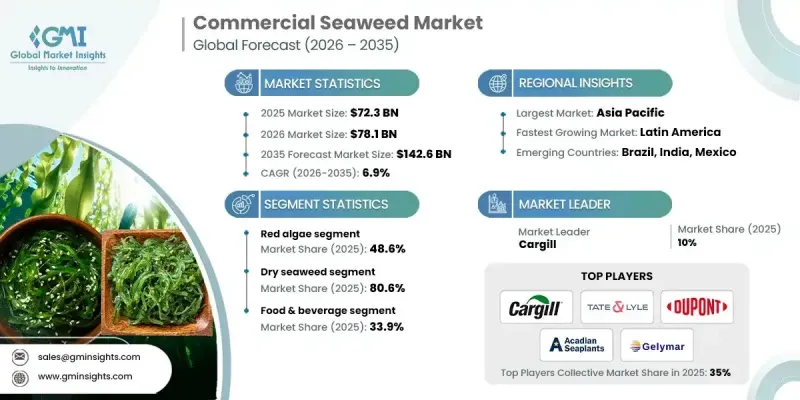

세계의 상업용 해초 시장은 2025년에 723억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.9%로 성장하여 1,426억 달러에 이를 것으로 예측됩니다.

해초류의 기능적 다양성과 지속가능성이 인정받고 다양한 가치사슬에 통합되면서 해초류 시장은 지속적으로 성장하고 있습니다. 수요 증가의 배경에는 식품, 화장품, 산업용 배합제에서 중요한 결합, 안정화, 증점 기능을 수행하는 해초류 유래 수용성 다당류의 이용 증가가 크게 작용하고 있습니다. 이러한 용도는 전 세계 상업용 해초류 매출의 40% 이상을 차지합니다. 동시에 친환경 농업으로의 전환이 해초류 유래 원료의 도입을 가속화하고 있으며, 해초류를 재생형 저환경 농업 모델에 부합하는 자연 유래 솔루션으로 자리매김하고 있습니다. 지속 가능한 농업과의 세계 정책적 연계는 수요를 더욱 강화시키고 있습니다. 이와 함께 해초류 생명공학 분야의 혁신은 시장의 가치 잠재력을 확대하고 있으며, 생산자들은 영양, 건강 및 특수 용도의 고부가가치 화합물을 추출하기 위해 고도의 가공 기술에 투자하고 있습니다. 이러한 발전으로 상업용 해초류 산업은 양 중심의 산업에서 기술 기반의 고부가가치 생태계로 변모하고 있으며, 다양한 최종 용도와 탄탄한 장기적 성장 전망을 특징으로 합니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 723억 달러 |

| 예측 금액 | 1,426억 달러 |

| CAGR | 6.9% |

홍조류 부문은 2025년 48.6%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 6.8%의 성장률을 보일 것으로 전망됩니다. 이러한 우위는 식품, 의약품, 퍼스널케어 제조의 기초 원료로서 하이드로콜로이드 생산에 널리 사용되어 안정적인 세계 수요를 강화하는 데 도움이 되고 있습니다.

음료 및 식품 응용 분야는 2025년 33.9%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 6.8%의 성장률을 보일 것으로 예측됩니다. 해초류는 천연 기능성 원료로 널리 사용되고 있으며, 포장 식품 및 가공 식품 카테고리 전반에 걸쳐 제형의 안정성, 영양 강화 및 클린 라벨 포지셔닝을 지원하고 있습니다.

북미 상업용 해초류 시장은 2025년 11%의 점유율을 차지하며 빠르게 성장하고 있습니다. 이 지역에서는 지속가능한 양식업, 기후 변화 대응 소재, 대체 사료 솔루션에 대한 투자가 증가하고 있으며, 이는 상업적 이용 확대와 다운스트림 분야의 혁신을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 유형별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산 및 예측 : 유형별, 2022-2035

- 주요 동향

- 홍조류

- 갈조류

- 녹조류

제6장 시장 추산 및 예측 : 형태별, 2022-2035

- 주요 동향

- 건조 해초

- 생/신선 해초

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

- 주요 동향

- 식품 및 음료

- 유제품

- 제빵 및 제과

- 가공육 및 수산가공품

- 비건 및 식물성 식품

- 기능성 음료

- 식용 해초 스낵

- 소스, 수프 및 조미료

- 동물사료

- 가축 사료첨가물

- 가금 사료

- 수산양식용 사료

- 반려동물 사료 보충제

- 반추동물용 메탄 저감 사료

- 의약품·퍼스널케어

- 창상 치유 연고

- 약물 전달 시스템

- 스킨케어 로션·크림

- 샴푸 및 컨디셔너

- 항노화 및 항염증 제품

- 구강관리 제품

- 바이오연료

- 바이오에탄올 생산

- 바이오가스 생성

- 조류(Algae) 바이오매스 사전 처리용 투입물

- 하이브리드 재생에너지 혼합 연료

- 기타

- 농업용 바이오 자극제

- 토양 개량제

- 수처리제

- 섬유 산업 응용

- 바이오플라스틱 및 포장재료

제8장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 개요

- Acadian Seaplants

- Algaia

- Cargill

- DuPont

- FMC Corporation

- Gelymar

- Indo Alginate

- Irish Seaweeds

- KIMICA Corporation

- Mara Seaweed

- MCPI(Marine Chemicals &Polymers Industries)

- Ocean Harvest Technology

- Qingdao Gather Great Ocean Algae Industry Group

- Qingdao Seawin Biotech Group

- Seasol

- Seaweed Energy Solutions

- Shaanxi Hongda Phytochemistry Co., Ltd.

- Tate &Lyle

- TBK Manufacturing Corporation(Philippines)

- W Hydrocolloids, Inc.

- Others

The Global Commercial Seaweed Market was valued at USD 72.3 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 142.6 billion by 2035.

The market continues to gain momentum as seaweed becomes increasingly integrated into multiple value chains, supported by its functional versatility and sustainability profile. Demand growth is strongly linked to the rising use of seaweed-derived hydrocolloids that perform essential binding, stabilizing, and thickening functions across food, cosmetics, and industrial formulations. These applications collectively account for more than 40% of global commercial seaweed revenue. At the same time, the transition toward environmentally responsible agricultural practices is accelerating the adoption of seaweed-based inputs, positioning seaweed as a natural solution aligned with regenerative and low-impact farming models. Global policy alignment with sustainable agriculture has further strengthened demand. In parallel, innovation across seaweed biotechnology is expanding the market's value potential, as producers invest in advanced processing to extract high-value compounds for nutrition, health, and specialty applications. These developments are reshaping the commercial seaweed industry from a volume-driven sector into a technology-enabled, high-value ecosystem with diversified end uses and strong long-term growth visibility.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $72.3 Billion |

| Forecast Value | $142.6 Billion |

| CAGR | 6.9% |

The red algae segment held a 48.6% share in 2025 and is expected to grow at a CAGR of 6.8% through 2035. This dominance is supported by its widespread use in hydrocolloid production, which remains a foundational input across food, pharmaceutical, and personal care manufacturing, reinforcing steady global demand.

The food & beverage applications segment held 33.9% share in 2025 and is forecast to grow at a CAGR of 6.8% from 2026 to 2035. Seaweed continues to be widely incorporated as a natural functional ingredient, supporting formulation stability, nutritional enhancement, and clean-label positioning across packaged and processed food categories.

North America Commercial Seaweed Market accounted for 11% share in 2025 and is showing rapid growth. The region benefits from increasing investment in sustainable aquaculture, climate-aligned materials, and alternative feed solutions, driving broader commercial adoption and downstream innovation.

Key companies operating in the Global Commercial Seaweed Market include Cargill, Tate & Lyle, DuPont, FMC Corporation, Algaia, Gelymar, Acadian Seaplants, Irish Seaweeds, KIMICA Corporation, Qingdao Seawin Biotech Group, Ocean Harvest Technology, Seasol, Seaweed Energy Solutions, Indo Alginate, TBK Manufacturing Corporation, W Hydrocolloids, Inc., MCPI, Mara Seaweed, Qingdao Gather Great Ocean Algae Industry Group, and Shaanxi Hongda Phytochemistry. Companies in the Global Commercial Seaweed Market are strengthening their market position by expanding vertically across cultivation, processing, and formulation to secure supply consistency and improve margins. Significant investment is directed toward research and development to unlock high-value extracts and improve processing efficiency. Strategic partnerships with food, agriculture, and wellness manufacturers are helping accelerate commercialization and application development. Firms are also scaling production capacity in high-growth regions to reduce logistics costs and meet rising demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)(Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Red algae

- 5.3 Brown algae

- 5.4 Green algae

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dry seaweed

- 6.3 Wet/Fresh seaweed

Chapter 7 Market Estimates and Forecast, By End use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.2.1 Dairy products

- 7.2.2 Bakery & confectionery

- 7.2.3 Processed meats & seafood

- 7.2.4 Vegan/plant-based foods

- 7.2.5 Functional beverages

- 7.2.6 Edible seaweed snacks

- 7.2.7 Sauces, soups & seasonings

- 7.3 Animal feed

- 7.3.1 Livestock feed additives

- 7.3.2 Poultry feed

- 7.3.3 Aquaculture feed

- 7.3.4 Pet food supplements

- 7.3.5 Methane-reducing feed for ruminants

- 7.4 Pharmaceutical & personal care

- 7.4.1 Wound healing ointments

- 7.4.2 Drug delivery systems

- 7.4.3 Skin care lotions & creams

- 7.4.4 Shampoos & conditioners

- 7.4.5 Anti-aging & anti-inflammatory products

- 7.4.6 Oral care products

- 7.5 Biofuels

- 7.5.1 Bioethanol production

- 7.5.2 Biogas generation

- 7.5.3 Algal biomass pre-treatment inputs

- 7.5.4 Hybrid renewable energy blends

- 7.6 Others

- 7.6.1 Agricultural biostimulants

- 7.6.2 Soil conditioners

- 7.6.3 Water treatment agents

- 7.6.4 Textile industry applications

- 7.6.5 Bioplastics & packaging materials

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Acadian Seaplants

- 9.2 Algaia

- 9.3 Cargill

- 9.4 DuPont

- 9.5 FMC Corporation

- 9.6 Gelymar

- 9.7 Indo Alginate

- 9.8 Irish Seaweeds

- 9.9 KIMICA Corporation

- 9.10 Mara Seaweed

- 9.11 MCPI (Marine Chemicals & Polymers Industries)

- 9.12 Ocean Harvest Technology

- 9.13 Qingdao Gather Great Ocean Algae Industry Group

- 9.14 Qingdao Seawin Biotech Group

- 9.15 Seasol

- 9.16 Seaweed Energy Solutions

- 9.17 Shaanxi Hongda Phytochemistry Co., Ltd.

- 9.18 Tate & Lyle

- 9.19 TBK Manufacturing Corporation (Philippines)

- 9.20 W Hydrocolloids, Inc.

- 9.21 Others