|

시장보고서

상품코드

1928962

왕복 엔진 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Reciprocating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

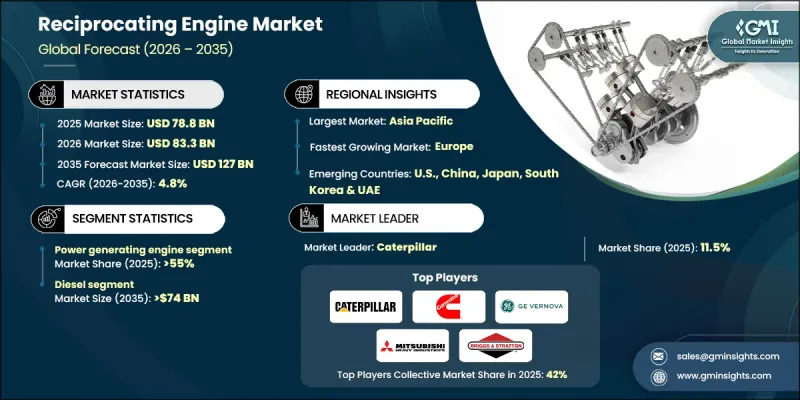

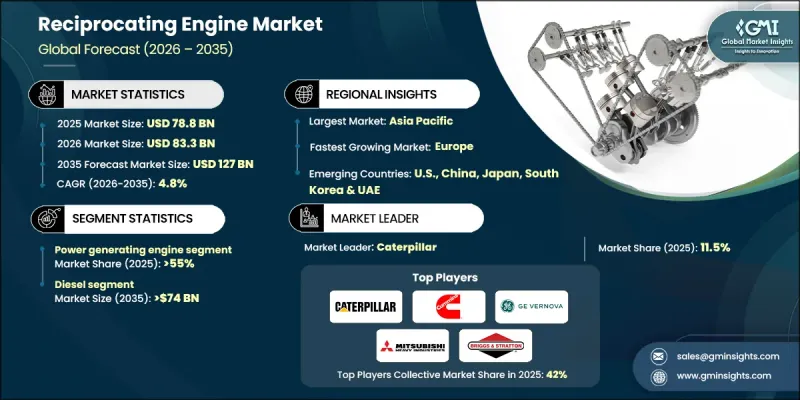

세계의 왕복 엔진 시장은 2025년에 788억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.8%로 성장하여 1,270억 달러에 이를 것으로 예측되고 있습니다.

시장 성장은 모듈형 및 간소화된 엔진 설계의 지속적인 혁신에 힘입어 이루어지고 있으며, 이러한 혁신은 뛰어난 운영 유연성과 손쉬운 유지보수를 제공합니다. 연료 효율 기술의 도입 증가와 엄격한 배출가스 규제는 차세대 왕복 엔진의 발전을 이끌고 있습니다. 첨단 디지털 모니터링 시스템과 예지보전 도구의 통합으로 신뢰성이 향상되고 다운타임이 최소화됩니다. 현대의 왕복 엔진은 견고한 엔지니어링과 운영 전략을 결합하여 다양한 응용 분야에서 일관되고 효율적인 동력을 제공합니다. 연소 효율 향상, 열적 안정성 유지, 다중 연료 유형에 대한 대응을 실현하고 있습니다. 산업용, 상업용, 분산형 발전 시스템에 이르기까지 다양한 응용 분야에서 이 엔진은 에너지 탄력성을 지원하는 동시에 재생에너지원과의 원활한 통합을 가능하게 합니다. 하이브리드 기술, 연료 최적화 및 제어 시스템의 발전으로 성능이 더욱 향상되어 비상 전원 및 연속 발전 모두에 이상적인 선택이 되었습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 788억 달러 |

| 예측 금액 | 1,270억 달러 |

| CAGR | 4.8% |

전력 부문은 2025년 시장 점유율 55%를 기록했으며, 2035년까지 연평균 4%의 성장률을 보일 것으로 예상됩니다. 이러한 성장은 안정적인 전력 솔루션에 대한 수요 증가, 유연한 모듈형 설계, 그리고 분산형 발전 시스템의 도입 확대에 힘입은 것입니다. 이 부문의 왕복 엔진은 빠른 시동, 고효율, 재생에너지와의 통합성이 뛰어나기 때문에 선호되고 있습니다.

가스 엔진 시장은 질소산화물, 이산화황, 미세먼지 배출량 감소에 힘입어 2035년까지 연평균 5.5% 성장할 것으로 예상됩니다. 이러한 친환경적인 작동 방식 덕분에 가스 엔진은 환경 규제 준수 및 글로벌 지속가능성 목표 달성을 중시하는 기업들에게 매력적인 선택지가 되고 있습니다.

북미 왕복 엔진 시장은 에너지 인프라 현대화 노력, 고성능 저배출 엔진 도입, 지속적인 산업 확장 등에 힘입어 2035년까지 200억 달러에 이를 것으로 전망됩니다. 엔진 성능 및 효율성의 지속적인 기술 발전은 이 지역 시장 전망을 더욱 강화할 것으로 예상됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 원재료 가용성과 조달 분석

- 제조능력 평가

- 공급망 회복탄력성와 리스크 요인

- 유통 네트워크 분석

- 규제 상황

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- PESTEL 분석

- 왕복 엔진 비용 구조 분석

- 가격 동향 분석(달러/MW)

- 지역별

- 정격 출력별

- 새로운 기회와 동향

- 디지털화와 IoT 통합

- 신흥 시장에의 진출

- 투자 분석과 전망

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 대시보드

- 전략적 이니셔티브

- 주요 제휴·협력 관계

- 주요 M&A활동

- 제품 혁신과 신제품 발매

- 시장 확대 전략

- 경쟁 벤치마킹

- 혁신과 지속가능성 상황

제5장 시장 규모와 예측 : 연료별(2022-2035년)

- 디젤

- 가스

- 기타

제6장 시장 규모와 예측 : 정격 출력별(2022-2035년)

- 0.5 MW-1 MW

- 1 MW 이상-2MW

- 2 MW 이상-3.5MW

- 3.5 MW 이상-5MW

- 5 MW 이상-7.5MW

- 7.5 MW 이상

제7장 시장 규모와 예측 : 용도별(2022-2035년)

- 전력

- 선박

- 기계

제8장 시장 규모와 예측 : 실린더 구성별(2022-2035년)

- 직렬

- V형

- 래디얼

- 대향 피스톤

제9장 시장 규모와 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 러시아

- 이탈리아

- 스페인

- 네덜란드

- 덴마크

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 태국

- 싱가포르

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 카타르

- 오만

- 쿠웨이트

- 이집트

- 튀르키예

- 남아프리카공화국

- 라틴아메리카

- 브라질

- 아르헨티나

- 칠레

제10장 기업 개요

- AB Volvo Penta

- Briggs &Stratton

- Caterpillar

- Cummins

- GE Vernova

- Guascor Energy

- Honda Motor

- IHI Corporation

- J C Bamford Excavators

- Kawasaki Heavy Industries

- KUBOTA Corporation

- Lister Petter

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Perkins Engines

- Rehlko

- Rolls-Royce

- Wartsila

- Yamaha Motor

- Yanmar Holdings

The Global Reciprocating Engine Market was valued at USD 78.8 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 127 billion by 2035.

The market growth is fueled by continuous innovation in modular and simplified engine designs, which provide greater operational flexibility and ease of maintenance. Increasing adoption of fuel-efficient technologies, coupled with strict emission regulations, is shaping the next generation of reciprocating engines. Integration of advanced digital monitoring systems and predictive maintenance tools is enhancing reliability and minimizing downtime. Modern reciprocating engines combine robust engineering with operational strategies to deliver consistent, efficient power across diverse applications. They improve combustion efficiency, maintain thermal stability, and offer compatibility with multiple fuel types. With applications spanning industrial, commercial, and distributed generation systems, these engines support energy resilience while integrating seamlessly with renewable energy sources. Advancements in hybrid technologies, fuel optimization, and control systems further enhance performance, making them ideal for both standby and continuous power generation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $78.8 Billion |

| Forecast Value | $127 Billion |

| CAGR | 4.8% |

The power segment accounted for 55% share in 2025 and is expected to grow at a CAGR of 4% through 2035. Its expansion is supported by rising demand for reliable power solutions, flexible modular designs, and the increasing deployment of distributed generation systems. Reciprocating engines in this segment are favored for their fast start-up, high efficiency, and compatibility with renewable energy integration.

The gas-fired engine segment is expected to grow at a CAGR of 5.5% by 2035, driven by lower emissions of nitrogen oxides, sulfur dioxide, and particulates. These cleaner operations make gas engines an attractive choice for companies prioritizing compliance with environmental regulations and global sustainability objectives.

North America Reciprocating Engine Market is projected to reach USD 20 billion by 2035, driven by modernization efforts in energy infrastructure, adoption of high-performance, low-emission engines, and ongoing industrial expansion. Continuous technological advancements in engine performance and efficiency are expected to strengthen the market outlook across the region.

Major players in the Global Reciprocating Engine Market include AB Volvo Penta, Cummins, GE Vernova, MAN Energy Solutions, Mitsubishi Heavy Industries, Yamaha Motor, Perkins Engines, Honda Motor, Lister Petter, Briggs & Stratton, Rehlko, J C Bamford Excavators, Wartsila, Kawasaki Heavy Industries, KUBOTA Corporation, Caterpillar, Yanmar Holdings, Guascor Energy, and Rolls-Royce.

Companies in the Global Reciprocating Engine Market focus on several strategies to maintain and expand their market position. Product innovation remains central, with firms developing modular, fuel-efficient, and hybrid-compatible engines. Strategic partnerships and collaborations help expand global distribution networks and access new customer segments. Investment in digital technologies, predictive maintenance, and IoT-enabled monitoring improves reliability and customer value. Companies also adopt sustainability-driven strategies, focusing on low-emission engines and compliance with environmental regulations. After-sales services, extended warranties, and technical support enhance customer loyalty. Mergers and acquisitions are leveraged to consolidate market share, expand product portfolios, and strengthen regional presence, while targeted marketing and R&D investments ensure competitiveness in evolving energy and industrial sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Fuel trends

- 2.4 Rated power trends

- 2.5 Application trends

- 2.6 Cylinder configuration trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter';s analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of reciprocating engines

- 3.8 Price trend analysis (USD/MW)

- 3.8.1 By region

- 3.8.2 By rated power

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 Diesel

- 5.3 Gas

- 5.4 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 Power

- 7.3 Marine

- 7.4 Mechanical

Chapter 8 Market Size and Forecast, By Cylinder Configuration, 2022 - 2035 (USD Million & MW)

- 8.1 Key trends

- 8.2 Inline

- 8.3 V-Type

- 8.4 Radial

- 8.5 Opposed piston

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Russia

- 9.3.5 Italy

- 9.3.6 Spain

- 9.3.7 Netherlands

- 9.3.8 Denmark

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Thailand

- 9.4.7 Singapore

- 9.5 Middle East & Africa

- 9.5.1 UAE

- 9.5.2 Saudi Arabia

- 9.5.3 Qatar

- 9.5.4 Oman

- 9.5.5 Kuwait

- 9.5.6 Egypt

- 9.5.7 Turkey

- 9.5.8 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

- 9.6.3 Chile

Chapter 10 Company Profiles

- 10.1 AB Volvo Penta

- 10.2 Briggs & Stratton

- 10.3 Caterpillar

- 10.4 Cummins

- 10.5 GE Vernova

- 10.6 Guascor Energy

- 10.7 Honda Motor

- 10.8 IHI Corporation

- 10.9 J C Bamford Excavators

- 10.10 Kawasaki Heavy Industries

- 10.11 KUBOTA Corporation

- 10.12 Lister Petter

- 10.13 MAN Energy Solutions

- 10.14 Mitsubishi Heavy Industries

- 10.15 Perkins Engines

- 10.16 Rehlko

- 10.17 Rolls-Royce

- 10.18 Wartsila

- 10.19 Yamaha Motor

- 10.20 Yanmar Holdings