|

시장보고서

상품코드

1928982

중고 트럭 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Used Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

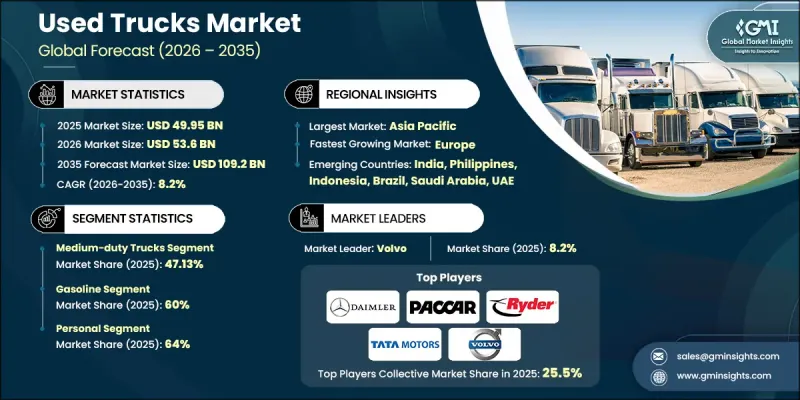

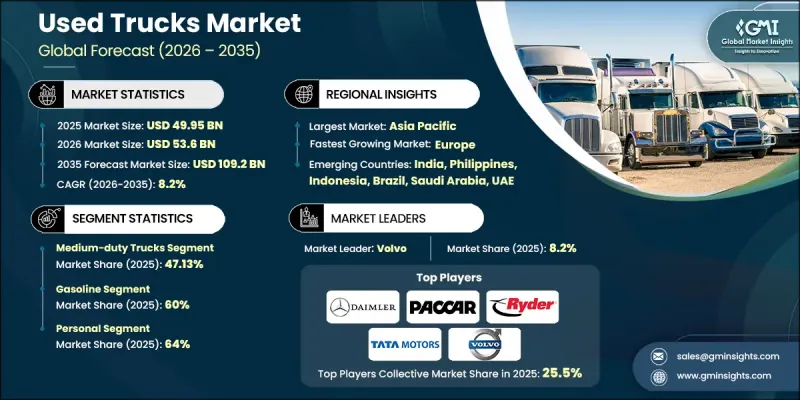

세계의 중고 트럭 시장은 2025년에 499억 5,000만 달러로 평가되었으며, 2035년까지 CAGR 8.2%로 성장하여 1,092억 달러에 달할 것으로 예측됩니다.

차량 가격 상승, OEM의 납기 연장, 자본 보존에 대한 집중과 함께 차량 운영자들은 사업 연속성과 수익률 보호를 위해 2차 시장으로 전환하고 있습니다. 과거에는 잔존 자산으로 여겨졌던 중고 트럭은 현재 물류, 건설, 지자체 서비스, 광업, 농업, 공공사업 등에서 차량 최적화 전략의 필수적인 요소로 자리 잡았습니다. 차량 관리자는 정비 이력이 확인된 차량, 배출가스 기준 적합성, 디지털 개조 대응 능력을 우선적으로 요구하고 있습니다. 텔레매틱스, 예지보전, ADAS 후장, 파워트레인 모니터링의 도입은 차량 수명 연장, 총소유비용 절감, 연비, 운전자 성능, 자산 재배치에 대한 데이터 기반 의사결정을 가능하게 합니다. 초기 소유 경제가 아닌 라이프사이클 중심의 접근 방식은 수요의 역학을 바꾸고 있으며, 도시 및 지역 운송 네트워크에서 운영 유연성과 효율성을 추구하는 비용에 민감한 차량 운영자에게 중고 트럭은 전략적 선택이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시시 가치 | 499억 5,000만 달러 |

| 예측 금액 | 1,092억 달러 |

| CAGR | 8.2% |

중형 트럭 부문은 2025년 47.13%의 점유율을 차지했으며, 2035년까지 연평균 8.1%의 성장률을 기록할 것으로 전망됩니다. 총 중량(GVWR) 10,001-2만 6,000파운드(약 4,536-11,814kg)의 중형 트럭은 다용도성, 연비 효율성, 낮은 취득비용을 겸비하여 도시 물류, 라스트 마일 배송, 건설 지원, 지자체 업무에 적합합니다. 적재 능력과 운영 비용 효율성이 균형을 이루고 있어 중소형 선단 사업자에게 특히 선호되고 있습니다.

가솔린 트럭 부문은 2025년에 60%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 8.3%로 성장할 것으로 예상됩니다. 접근성, 저렴한 구매 가격, 유지보수의 용이성으로 인해 차량 사업자, 중소기업, 지역 배송 서비스 사업자에게 매우 매력적임. 광범위한 서비스 네트워크와 풍부한 예비 부품은 특히 신흥 시장에서 가솔린 트럭의 매력을 더욱 높이고 있습니다.

중국 중고 트럭 시장은 2025년 65.5%의 점유율을 차지하며 229억 6,000만 달러 규모에 달할 것으로 예상됩니다. 이러한 성장은 E-Commerce, 물류, 지역 간 운송, 인프라 프로젝트의 급속한 확장에 의해 뒷받침되고 있습니다. 신차 가격의 상승은 중소형 사업자의 중고차 매력을 더욱 높여 중대형 중고 트럭에 대한 수요를 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률 분석

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 미치는 요인

- 디스럽션

- 업계에 대한 영향요인

- 성장 촉진요인

- 세계적으로 높아지는 전기·하이브리드 대형 트럭에 대한 수요

- 북미 전역의 화물 운송 활동 확대

- 중소기업 증가 경향

- 아시아태평양의 인프라 개발 활동에 대한 투자 증가

- 업계의 잠재적 리스크와 과제

- 경기후퇴와 저경제 성장

- 규제 준수와 정부 규제

- 시장 기회

- 인증 중고차(CPO) 및 제조업체 보증 포함 중고 트럭 프로그램 확대

- 중소기업 및 개인 사업주의 비용 효율적 플릿 솔루션에 대한 수요 확대

- 선진국에서 신흥 시장에 대한 중고 트럭 크로스보더 거래 증가

- 디지털 리마케팅, 온라인 경매, 데이터 기반 가격 책정의 확대 도입

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- NEVI/IIJA, 첨단 클린 트럭(ACT) 규제

- 유럽

- 독일 : 전기 모빌리티 법(EmoG)

- 영국 : 클린 차량 개조 인증제도(CVRAS), 초저배출 가스 구역(ULEZ)

- 프랑스 : 모빌리티 지향법(LOM법)

- 이탈리아 : 국가 통합 에너지·기후 계획(PNIEC)

- 아시아태평양

- 중국 : 신에너지차(NEV) 의무화 정책

- 인도 : FAME II스킴

- 일본 : 전기자동차(EV)/연료전지자동차(FCV) 도입을 위한 전략적 로드맵

- 호주 : 주 레벨의 무공해차 의무화

- 라틴아메리카

- 브라질 : 국가 전기 모빌리티 정책(PNME)

- 멕시코 : 도시의 무공해차 양도입 프로그램

- 아르헨티나 : 주별 EV 인센티브 규제(부에노스아이레스주)

- 중동 및 아프리카

- UAE : EV 충전 인프라 규제(ADDM/DEWA)

- 사우디아라비아 : 전기자동차 도입에 관한 규제 프레임워크(SASO)

- 남아프리카공화국 : 그린 운송 전략

- 북미

- Porters 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 분석

- 가격 분석

- 지역별

- 연료별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 비용 내역 분석

- 지속가능성과 환경 영향 분석

- 지속가능한 대처

- 폐기물 절감 전략

- 생산의 에너지 효율

- 친환경적인 대처

- 탄소발자국에 관한 고려사항

- 향후 전망과 기회

- 플릿 조달과 구매 행동 분석

- 중고 트럭 구입 결정 기준

- OEM 선정과 브랜드 선호 요인

- 연료, 적재량, 가동 시간이 구매 결정에 미치는 영향

- 잔존 가치와 중고 트럭 시장 시장 역학

- 파이낸스, 리스 및 TaaS(Truck-as-a-Service) 경제성

- 애프터마켓, 서비스 및 부품 경제성

- 파워트레인 전환과 연료 전환 경로

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 제휴·협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 연료별, 2022-2035

- 가솔린

- 디젤

- 전기자동차

- 하이브리드

제6장 시장 추정 및 예측 : 유형별, 2022-2035

- 소형 트럭

- 중형 트럭

- 대형 트럭

제7장 시장 추정 및 예측 : 판매 채널별, 2022-2035

- 프랜차이즈 판매점

- 독립계 판매점

- P2P(Peer-to-Peer)

제8장 시장 추정 및 예측 : 규모별, 2022-2035

- 풀 사이즈

- 중규모

- 컴팩트

제9장 시장 추정 및 예측 : 연령별, 2022-2035

- 3년

- 5-10년

- 10년 이상

제10장 시장 추정 및 예측 : 구동 방식별, 2022-2035

- 이륜구동

- 사륜구동

제11장 시장 추정 및 예측 : 용도별, 2022-2035

- 개인용

- 상업용

- 건설 및 중기

- 농업 및 농경

- 조경 및 야외 서비스

- 유틸리티 및 자치체용 용도

제12장 시장 추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제13장 기업 개요

- 세계 플레이어

- Copart

- Daimler

- Hino Motors

- Isuzu Motors

- Navistar International

- PACCAR

- Penske Used Trucks

- Ritchie Bros. Auctioneers

- Ryder System

- TATA Motors

- Volvo Trucks

- 지역 플레이어

- Arrow Truck Sales

- Enterprise Truck Rental

- International Used Trucks

- Knight-Swift Transportation

- Mascus

- Schneider National

- TruckPaper

- Werner Enterprises

- 신흥 기업

- J.D. Power

- Carvana

- Manheim

The Global Used Trucks Market was valued at USD 49.95 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 109.2 billion by 2035.

Increasing vehicle prices, long OEM delivery times, and a focus on capital preservation are driving fleet operators toward the secondary market to maintain operational continuity and protect profit margins. Once viewed as residual assets, used trucks are now integral to fleet optimization strategies across logistics, construction, municipal services, mining, agriculture, and utilities. Fleet managers are prioritizing vehicles with verified service histories, compliance with emission standards, and the ability to accommodate digital retrofits. The adoption of telematics, predictive maintenance, ADAS retrofits, and powertrain monitoring enhances vehicle longevity, reduces total cost of ownership, and enables data-driven decisions for fuel efficiency, driver performance, and asset redeployment. This lifecycle-oriented approach, rather than first-ownership economics, is reshaping demand dynamics, making used trucks a strategic choice for cost-conscious fleet operators seeking operational flexibility and efficiency in urban and regional transportation networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $49.95 Billion |

| Forecast Value | $109.2 Billion |

| CAGR | 8.2% |

The medium-duty segment held 47.13% share in 2025 and is projected to grow at a CAGR of 8.1% through 2035. Medium-duty trucks, with GVWR ranging from 10,001-26,000 lbs, offer versatility, fuel efficiency, and lower acquisition costs, making them ideal for urban logistics, last-mile deliveries, construction support, and municipal applications. These trucks are particularly favored by small and medium-sized fleet operators due to their balance of payload capacity and operational cost-effectiveness.

The gasoline trucks segment accounted for 60% share in 2025 and is expected to grow at a CAGR of 8.3% from 2026 to 2035. Their widespread availability, lower purchase price, and ease of maintenance make them highly appealing to fleet operators, small businesses, and local delivery services. Broad service networks and abundant spare parts further enhance the attractiveness of gasoline trucks, particularly in emerging markets.

China Used Trucks Market held 65.5% share, generating USD 22.96 billion in 2025. The growth is supported by rapid expansion in e-commerce, logistics, regional transportation, and infrastructure projects. Rising new truck prices have further increased the appeal of pre-owned vehicles among small- and medium-sized operators, fueling demand for medium- and heavy-duty used trucks.

Major players in the Global Used Trucks Market include Enterprise Truck Rental, PACCAR, Daimler, Penske Used Trucks, Ryder System, Schneider National, Ritchie Bros. Auctioneers, TATA Motors, Werner Enterprises, and Volvo Trucks. Companies in the Global Used Trucks Market strengthen their presence through strategic fleet acquisition, digital integration, and after-sales services. Emphasis on telematics, predictive maintenance, and vehicle certification ensures reliability and builds customer trust. Expanding geographic reach and diversifying inventory across duty classes meet regional demand. Partnerships with logistics, construction, and municipal operators enhance market penetration. Companies also focus on value-added services such as financing, warranty programs, and fleet management solutions to improve customer retention and increase total cost-of-ownership transparency.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Fuel

- 2.2.4 Sales Channel

- 2.2.5 Size

- 2.2.6 Age

- 2.2.7 Drive

- 2.2.8 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for electric & hybrid heavy-duty trucks across the globe

- 3.2.1.2 Growing freight transportation activities across North America

- 3.2.1.3 The rising number of small and medium-sized businesses

- 3.2.1.4 Rising investments in infrastructure development activities in Asia Pacific

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Economic downturns and low economic growth

- 3.2.2.2 Regulatory compliance and government regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of certified pre-owned (CPO) and OEM-backed used truck programs

- 3.2.3.2 Growing demand for cost-effective fleet solutions among SME and owner-operators

- 3.2.3.3 Rising cross-border trade of used trucks from developed to emerging markets

- 3.2.3.4 Increasing adoption of digital remarketing, online auctions, and data-driven pricing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 NEVI / IIJA, Advanced Clean Trucks (ACT) Regulation.

- 3.4.2 Europe

- 3.4.2.1 Germany: Electric Mobility Act (EmoG)

- 3.4.2.2 UK: Clean Vehicle Retrofit Accreditation Scheme (CVRAS), Ultra-Low Emission Zone (ULEZ)

- 3.4.2.3 France: Mobility Orientation Law (LOM Act)

- 3.4.2.4 Italy: National Integrated Plan for Energy and Climate (PNIEC)

- 3.4.3 Asia Pacific

- 3.4.3.1 China: New Energy Vehicle (NEV) Mandate

- 3.4.3.2 India: FAME II Scheme

- 3.4.3.3 Japan: Strategic Roadmap for EV/FCV Deployment

- 3.4.3.4 Australia: State-Level Zero-Emission Vehicle Mandates

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Electric Mobility Policy (PNME)

- 3.4.4.2 Mexico: Urban Zero-Emission Fleet Programs

- 3.4.4.3 Argentina: Provincial EV Incentive Regulations (Buenos Aires)

- 3.4.5 MEA

- 3.4.5.1 UAE: EV Charging Infrastructure Regulation (ADDM/DEWA)

- 3.4.5.2 Saudi Arabia: EV Deployment Regulatory Framework (SASO)

- 3.4.5.3 South Africa: Green Transport Strategy

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Pricing Analysis

- 3.9.1 By region

- 3.9.2 By fuel

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.14 Fleet procurement & buying behavior analysis

- 3.14.1 Purchase decision criteria for Used trucks

- 3.14.2 OEM selection and brand preference factors

- 3.14.3 Impact of fuel, payload, and uptime on buying decisions

- 3.15 Residual value & used truck market dynamics

- 3.16 Financing, leasing & Truck-as-a-Service (TaaS) economics

- 3.17 Aftermarket, service & parts economics

- 3.18 Powertrain transition & fuel migration pathways

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Diesel

- 5.4 Electric

- 5.5 Hybrid

Chapter 6 Market Estimates & Forecast, By Type, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Light-duty truck

- 6.3 Medium-duty truck

- 6.4 Heavy-duty truck

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Franchised Dealer

- 7.3 Independent Dealer

- 7.4 Peer-to-peer

Chapter 8 Market Estimates & Forecast, By Size, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Full-size

- 8.3 Mid-size

- 8.4 Compact

Chapter 9 Market Estimates & Forecast, By Age, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Up to 3 years

- 9.3 5-10 years

- 9.4 Above 10 years

Chapter 10 Market Estimates & Forecast, By Drive, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Two-wheel drive

- 10.3 Four-wheel drive

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 Personal

- 11.3 Commercial

- 11.3.1 Construction and heavy equipment

- 11.3.2 Agriculture and farming

- 11.3.3 Landscaping and outdoor services

- 11.3.4 Utility and municipal use

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Philippines

- 12.4.7 Indonesia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 Copart

- 13.1.2 Daimler

- 13.1.3 Hino Motors

- 13.1.4 Isuzu Motors

- 13.1.5 Navistar International

- 13.1.6 PACCAR

- 13.1.7 Penske Used Trucks

- 13.1.8 Ritchie Bros. Auctioneers

- 13.1.9 Ryder System

- 13.1.10 TATA Motors

- 13.1.11 Volvo Trucks

- 13.2 Regional Players

- 13.2.1 Arrow Truck Sales

- 13.2.2 Enterprise Truck Rental

- 13.2.3 International Used Trucks

- 13.2.4 Knight-Swift Transportation

- 13.2.5 Mascus

- 13.2.6 Schneider National

- 13.2.7 TruckPaper

- 13.2.8 Werner Enterprises

- 13.3 Emerging Players

- 13.3.1 J.D. Power

- 13.3.2 Carvana

- 13.3.3 Manheim