|

시장보고서

상품코드

1936513

방음벽 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Acoustic Barrier Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

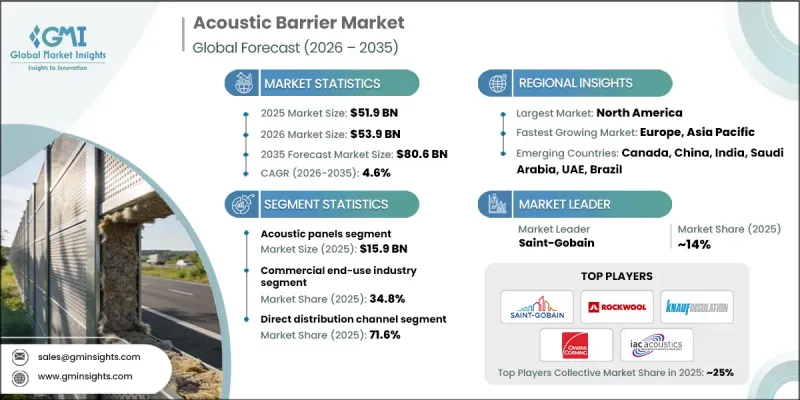

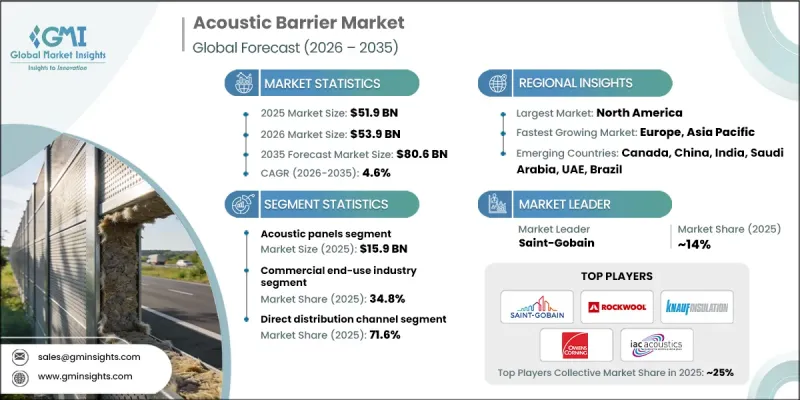

세계의 방음벽 시장은 2025년에 519억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.6%로 성장할 전망이며, 806억 달러에 이를 것으로 예측됩니다.

시장의 성장은 급속한 도시화, 교통 인프라 확대, 소음 공해의 건강에 대한 악영향 인식 증가에 의해 견인되고 있습니다. 세계 정부와 지자체는 고속도로, 철도, 공항, 산업 지대에서 보다 엄격한 소음 규제를 실시하고 있으며, 고성능 방음벽 수요를 크게 밀어 올리고 있습니다. 또한 스마트 시티 개념과 지속 가능한 인프라 프로젝트의 도입으로 첨단 소음 감소 솔루션의 배치가 가속화되고 있습니다. 제조업체 각사는 환경 기준 및 안전 기준에 적합하고, 내구성 및 내후성이 뛰어나며, 경관에 조화된 제품의 개발에 주력하고 있어, 방음벽은 현대의 도시 및 인프라 개발에 있어서 중요한 구성 요소가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 519억 달러 |

| 예측 금액 | 806억 달러 |

| CAGR | 4.6% |

음향 패널 부문은 2024년에 159억 달러 시장 규모를 창출했습니다. 높은 채용률은 범용성, 모듈 설계, 상업 시설, 공공 시설, 주택 환경에서의 잔향 제어 및 음질 개선 효과에 기인합니다. 벽걸이식 및 천장 장착형 음향 패널은 명확한 음성 전달 및 거주자의 편안함이 중요한 사무실, 접객 시설, 교육 기관 및 엔터테인먼트 시설에서 널리 사용됩니다. 오픈 플랜 아키텍처와 웰니스 지향 건축 디자인의 동향이 높아짐에 따라 성능과 시각적 매력을 결합한 고급 음향 패널 솔루션에 대한 수요가 계속 강화되고 있습니다.

2025년 시점에서 직접 판매 부문은 71.6%의 점유율을 차지하였으며, 2026-2035년 CAGR 4.6%에서의 성장이 전망되고 있습니다. 직접 판매는 가격 설정, 납기, 제품 사양에 대한 관리를 강화할 수 있으며, 특히 교통, 상업 인프라, 산업 시설의 대규모 프로젝트에서 매우 중요합니다. 이 기술은 신속한 의사소통과 맞춤형 솔루션을 제공하여 중개자에 대한 의존도를 줄이고 지연을 최소화합니다. 또한 턴키 프로젝트 및 통합 서비스 모델의 보급이 진행됨에 따라 공급업체와 고객 간 직접적인 상호작용이 촉진되고 조달 및 설치 프로세스가 효율화됩니다.

북미의 방음벽 시장은 엄격한 환경 소음 규제, 대규모 인프라 갱신, 노후화된 교통 회랑의 대규모 개수 및 갱신 활동에 힘입어 2024년에는 168억 달러 규모에 이르렀습니다. 미국과 캐나다에서는 고속도로 현대화, 도시 교통 시스템, 산업 소음 대책 솔루션에 대한 많은 투자가 계속되고 있습니다. 강력한 규제 집행 및 소음 관련 건강 문제에 대한 높은 사회적 의식이 결합되어 방음벽은 이 지역의 인프라 및 건설 프로젝트에 있어서 표준적인 요건이 되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 도시화 및 인프라 확장

- 환경 규제 및 소음 규제 강화

- 재료 및 기술의 진보

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용 및 설비 투자(CAPEX)의 압력

- 설치 및 구조상의 제약

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 차단 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- 무역 통계

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 배리어 유형별(2022-2035년)

- 방음벽

- 흡음 패널

- 벽걸이식

- 천장 장착형

- 자립식

- 음향 인클로저

- 음향 울타리

- 파티션 벽 및 분리 가능한 시스템

제6장 시장 추계 및 예측 : 재료별(2022-2035년)

- 콘크리트 배리어

- 금속계 배리어

- 투명 및 아크릴 베이스 배리어

- 목재계 배리어재

- 미네랄 울베이스

- 락울

- 글라스울

- 발포체 및 폴리머계 배리어재

- 복합재 및 다층 배리어

제7장 시장 추계 및 예측 : 최종 이용 산업별(2022-2035년)

- 주택용

- 상업용

- 사무실

- 접객 산업

- 소매

- 오락 및 레크리에이션

- 산업용

- 운수 인프라

- 기관용

제8장 시장 추계 및 예측 : 유통 채널별(2022-2035년)

- 직접 판매

- 간접 판매

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 인도네시아

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카(MEA)

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제10장 기업 프로파일

- Durisol

- Echo Barrier

- Gramm Barrier Systems

- IAC

- JFE Metal Products

- K. Schutte GmbH

- Knauf Insulation

- KOCH Finishing Systems

- Kohlhauer

- Nippon Steel Kobelco Metal Products

- Owens Corning

- Rockwool

- Saferoad Noise Protection

- Saint-Gobain

- Weldon

The Global Acoustic Barrier Market was valued at USD 51.9 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 80.6 billion by 2035.

Market growth is driven by rapid urbanization, expanding transportation infrastructure, and rising awareness of the adverse health impacts of noise pollution. Governments and municipal authorities worldwide are enforcing stricter noise control regulations across highways, railways, airports, and industrial zones, significantly boosting demand for high-performance acoustic barriers. Additionally, the adoption of smart city initiatives and sustainable infrastructure projects is accelerating the deployment of advanced noise mitigation solutions. Manufacturers are increasingly focusing on durable, weather-resistant, and aesthetically integrated products that comply with environmental and safety standards, making acoustic barriers a critical component of modern urban and infrastructure development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $51.9 Billion |

| Forecast Value | $80.6 Billion |

| CAGR | 4.6% |

The acoustic panels segment generated USD 15.9 billion in 2024. Their strong adoption is attributed to their versatility, modular design, and effectiveness in controlling reverberation and improving sound quality across commercial, institutional, and residential environments. Wall-mounted and ceiling-mounted acoustic panels are widely used in offices, hospitality venues, educational institutions, and entertainment facilities, where clear speech and occupant comfort are crucial. The growing trend toward open-plan buildings and wellness-oriented architectural designs continues to reinforce demand for advanced acoustic panel solutions that combine performance with visual appeal.

The direct distribution segment held 71.6% share in 2025 and is projected to grow at a CAGR of 4.6% from 2026 to 2035. Direct sales offer enhanced control over pricing, delivery schedules, and product specifications, which is especially critical for large-scale projects in transportation, commercial infrastructure, and industrial facilities. This approach enables quicker communication and more customized solutions, reducing reliance on intermediaries and minimizing delays. Furthermore, the increasing prevalence of turnkey projects and integrated service models promotes direct interaction between suppliers and clients, streamlining procurement and installation processes.

North America Acoustic Barrier Market generated USD 16.8 billion in 2024, supported by strict environmental noise regulations, large-scale infrastructure upgrades, and significant retrofit and replacement activities along aging transport corridors. The U.S. and Canada continue to invest heavily in highway modernization, urban transit systems, and industrial noise control solutions. Strong regulatory enforcement, coupled with high public awareness of noise-related health issues, has made acoustic barriers a standard requirement in infrastructure and construction projects across the region.

Key players operating in the Global Acoustic Barrier Market include Saint-Gobain, Rockwool International, Knauf Insulation, Owens Corning, IAC, Durisol, Echo Barrier, Gramm Barrier Systems, Nippon Steel Kobelco Metal Products, Saferoad Noise Protection, KOCH Finishing Systems, Kohlhauer, and JFE Metal Products. Companies in the acoustic barrier market are strengthening their market position by focusing on product innovation, material optimization, and integrated solution offerings. Leading players are investing in advanced materials such as composites, mineral wool, and transparent acrylics to enhance noise attenuation while meeting aesthetic and sustainability requirements. Strategic partnerships with infrastructure developers, government bodies, and EPC contractors are increasingly common to secure long-term projects. Firms are also expanding their portfolios beyond product supply to include acoustic consulting, noise mapping, customized design, and installation services, enabling end-to-end project execution.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Barrier type

- 2.2.3 Material

- 2.2.4 End use industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization & infrastructure expansion

- 3.2.1.2 Tightening environmental & noise regulations

- 3.2.1.3 Advances in materials & technology

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront costs & CAPEX pressures

- 3.2.2.2 Installation & structural constraints

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By barrier type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Barrier Type, 2022 - 2035, (USD Billion) (Thousand Square Meters)

- 5.1 Key trends

- 5.2 Noise barrier walls

- 5.3 Acoustic panels

- 5.4 Wall-mounted

- 5.5 Ceiling-mounted

- 5.6 Free-standing

- 5.7 Acoustic enclosures

- 5.8 Acoustic fencing

- 5.9 Partition walls/demountable systems

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Square Meters)

- 6.1 Key trends

- 6.2 Concrete-based barriers

- 6.3 Metal-based barriers

- 6.4 Transparent/acrylic-based barriers

- 6.5 Wood-based barriers

- 6.6 Mineral wool-based

- 6.6.1 Rock wool

- 6.6.2 Glass wool

- 6.7 Foam/polymer-based barriers

- 6.8 Composite/multi-material barrier

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Billion) (Thousand Square Meters)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.3.1 Office

- 7.3.2 Hospitality

- 7.3.3 Retail

- 7.3.4 Entertainment & recreation

- 7.4 Industrial

- 7.5 Transportation infrastructure

- 7.6 Institutional

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Square Meters)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Square Meters)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Durisol

- 10.2 Echo Barrier

- 10.3 Gramm Barrier Systems

- 10.4 IAC

- 10.5 JFE Metal Products

- 10.6 K. Schutte GmbH

- 10.7 Knauf Insulation

- 10.8 KOCH Finishing Systems

- 10.9 Kohlhauer

- 10.10 Nippon Steel Kobelco Metal Products

- 10.11 Owens Corning

- 10.12 Rockwool

- 10.13 Saferoad Noise Protection

- 10.14 Saint-Gobain

- 10.15 Weldon