|

시장보고서

상품코드

1936594

활성 및 지능형 포장 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2026-2035년)Active and Intelligent Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

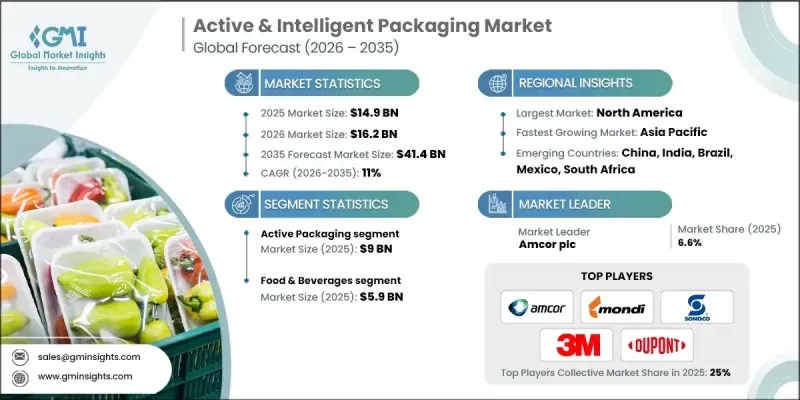

세계의 활성 및 지능형 포장 시장은 2025년에 149억 달러로 평가되었으며, 2035년까지 CAGR 11%로 성장하여 414억 달러에 달할 것으로 예측됩니다.

이 시장의 성장은 소비자의 장기 보존 식품에 대한 수요 증가와 식품의 안전과 품질에 대한 인식이 높아짐에 따라 성장하고 있습니다. 첨단 소재와 센서 기술의 혁신으로 제품의 신선도, 열화 상태, 환경 조건에 대한 실시간 정보를 제공하면서 제품과 능동적으로 상호 작용하는 포장 기술을 실현하고 있습니다. 전 세계적으로 가공식품 및 포장식품의 소비가 확대됨에 따라 제품 품질 보증, 오염 방지, 투명성을 제공하는 포장에 대한 수요가 증가하고 있으며, 도입이 가속화되고 있습니다. 제조업체와 소매업체들도 폐기물 감소, 규제 요건 준수, 공급망 효율성 향상을 위해 능동형 지능형 포장 기술을 채택하고 있습니다. 이러한 소비자 선호도, 규제 압력, 기술 발전의 융합은 향후 10년간 지속가능한 시장 성장의 토대를 마련하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 149억 달러 |

| 예측 금액 | 414억 달러 |

| CAGR | 11% |

활성 포장 부문은 2025년 90억 달러의 시장 규모를 창출했습니다. 활성 포장은 산소 흡수제, 흡습제, 항균제 등의 솔루션을 통해 유통기한 연장, 제품 품질 유지, 오염 방지를 위해 널리 활용되고 있습니다. 포장된 제품과 직접 상호 작용할 수 있는 능력은 식품, 음료, 의약품 등의 분야에서 중요한 이점을 제공합니다. 기업들은 제품의 무결성을 보장하고, 부패를 줄이고, 엄격한 안전 기준을 준수하기 위해 이러한 기술을 점점 더 많이 통합하고 있으며, 이는 전 세계적으로 활성 포장 솔루션에 대한 수요를 더욱 촉진하고 있습니다.

식품 및 음료 부문은 2025년 59억 달러 규모에 도달했습니다. 이 분야는 신선도 표시기, 산소 흡수제, 흡습제, 항균 필름 등의 기술을 채택하여 품질 유지, 유통기한 연장, 식품 안전 규정 준수를 위해 활성 및 지능형 포장 솔루션의 주요 도입처가 되고 있습니다. 이 분야의 기업들은 폐기물을 최소화하고, 재고 관리를 개선하고, 공급망 효율성을 최적화하고, 안전하고 신선한 제품에 대한 소비자의 높은 기대치를 충족시키기 위해 이러한 솔루션 도입에 박차를 가하고 있습니다. 주요 식음료 제조업체들의 포장 기술 혁신과 자동화에 대한 지속적인 투자는 이 분야에서의 우위를 더욱 강화하고 있습니다.

북미 활성 및 지능형 포장 시장은 2025년 31.7%의 점유율을 차지했습니다. 이 지역은 좋은 비즈니스 환경, 식음료 분야에 대한 강력한 투자, 선진적인 물류 인프라, 탄탄한 R&D 생태계의 혜택을 누리고 있습니다. 미국 시장은 활성 포장, 지능형 라벨링, 센서 통합에 중점을 둔 포장 기술 기업, 연구 기관 및 혁신 허브의 강력한 네트워크에 의해 뒷받침됩니다. 이러한 요소들을 통해 기업은 새로운 포장 솔루션을 신속하게 도입할 수 있으며, 제품 안전성, 추적성, 소비자 참여도를 향상시켜 북미를 이 분야의 세계 리더로 자리매김할 수 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 기술 유형별, 2022-2035년

제6장 시장 추정 및 예측 : 기능별, 2022-2035년

제7장 시장 추정 및 예측 : 포장 재료별, 2022-2035년

제8장 시장 추정 및 예측 : 최종 이용 산업별, 2022-2035년

제9장 시장 추정 및 예측 : 지역별, 2022-2035년

제10장 기업 개요

KSM 26.03.12The Global Active & Intelligent Packaging Market was valued at USD 14.9 billion in 2025 and is estimated to grow at a CAGR of 11% to reach USD 41.4 billion by 2035.

The market is driven by rising consumer demand for longer shelf-life food products and increasing awareness about food safety and quality. Advanced materials and innovations in sensor technologies are enabling packaging that actively interacts with products while providing real-time information about freshness, spoilage, or environmental conditions. The growing consumption of packaged and processed foods worldwide is accelerating adoption, as consumers increasingly seek packaging that ensures product quality, prevents contamination, and offers transparency. Manufacturers and retailers are also embracing active and intelligent packaging to reduce waste, meet regulatory requirements, and enhance supply chain efficiency. This convergence of consumer preference, regulatory pressure, and technological advancement is positioning the market for sustained growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.9 Billion |

| Forecast Value | $41.4 Billion |

| CAGR | 11% |

The active packaging segment generated USD 9 billion in 2025. Active packaging is widely utilized for shelf-life extension, maintaining product quality, and preventing contamination through solutions such as oxygen scavengers, moisture absorbers, and antimicrobial agents. Its ability to directly interact with the packaged product provides a critical advantage across sectors like food, beverages, and pharmaceuticals. Companies are increasingly integrating these technologies to ensure product integrity, reduce spoilage, and comply with stringent safety standards, further fueling demand for active packaging solutions globally.

The food & beverages segment reached USD 5.9 billion in 2025. This sector is the primary adopter of active and intelligent packaging solutions, employing technologies like freshness indicators, oxygen scavengers, moisture absorbers, and antimicrobial films to maintain quality, extend shelf life, and ensure compliance with food safety regulations. Companies in this segment are increasingly deploying these solutions to minimize waste, improve inventory management, optimize supply chain efficiency, and meet rising consumer expectations for safe and fresh products. The segment's dominance is reinforced by ongoing investments in packaging innovation and automation by leading food and beverage manufacturers.

North America Active & Intelligent Packaging Market held a 31.7% share in 2025. The region benefits from a favorable business environment, strong investments in the food and beverage sector, advanced logistics infrastructure, and a robust research and development ecosystem. The U.S. market is supported by a strong network of packaging technology firms, research institutions, and innovation hubs that focus on active packaging, intelligent labeling, and sensor integration. These factors enable companies to rapidly deploy new packaging solutions, ensuring product safety, traceability, and enhanced consumer engagement, positioning North America as a global leader in this industry.

Key players in the Global Active & Intelligent Packaging Market include 3M Company, Mondi plc, Huhtamaki Oyj, CCL Industries Inc., Amcor plc, Multisorb Technologies, Inc., Sealed Air Corporation, Stora Enso Oyj, Dai Nippon Printing Co., Ltd., Avery Dennison Corporation, DuPont de Nemours, Inc., Coveris Holdings S.A., Sonoco Products Company, and Constantia Flexibles Group GmbH. Companies in the active and intelligent packaging market are adopting strategies to strengthen their position by investing heavily in research and development for next-generation packaging materials, sensors, and smart labeling technologies. Firms are forming strategic partnerships with food and beverage manufacturers, pharmaceutical companies, and retailers to integrate customized solutions into their supply chains. Expanding production facilities, acquiring innovative startups, and collaborating with technology providers are also key strategies to enhance product offerings.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Technology type trends

- 2.2.3 Functionality trends

- 2.2.4 Packaging material trends

- 2.2.5 End use industry trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Executive decision points

- 2.3.2 Critical Success Factors

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Food Safety and Quality

- 3.2.1.2 Growth of E-Commerce and Cold Chain Logistics

- 3.2.1.3 Advancements in Smart Sensors and RFID Technologies

- 3.2.1.4 Regulatory Focus on Food Waste Reduction and Traceability

- 3.2.1.5 Adoption of Sustainable and Biodegradable Packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Cost and Complexity of Advanced Packaging Technologies

- 3.2.2.2 Recycling and Regulatory Compliance Challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of Digital Technologies and IoT-Enabled Packaging

- 3.2.3.2 Expansion in Pharmaceutical and Healthcare Packaging Applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Measures

- 3.11 Global Consumer Sentiment Analysis

- 3.12 Patent Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit Margin

- 4.3.1.3 R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1 Product Range Breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global Footprint Analysis

- 4.3.3.2 Service Network Coverage

- 4.3.3.3 Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 1.1.1 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Active packaging

- 5.2.1 Oxygen scavengers

- 5.2.2 Moisture absorbers

- 5.2.3 Ethylene absorbers

- 5.2.4 Antimicrobial agents

- 5.2.5 Temperature control packaging

- 5.2.6 Flavor/odor absorbers

- 5.3 Intelligent packaging

- 5.3.1 Time-temperature indicators (TTIS)

- 5.3.2 RFID tags and QR codes

- 5.3.3 Freshness indicators

- 5.3.4 Gas sensors

- 5.3.5 Smart labels

- 5.3.6 Interactive packaging

Chapter 6 Market Estimates and Forecast, By Functionality, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Shelf-life extension

- 6.2.1 Moisture control

- 6.2.2 Oxygen control

- 6.2.3 Ethylene control

- 6.2.4 Antimicrobial protection

- 6.3 Quality assurance

- 6.3.1 Freshness indicators

- 6.3.2 Time-temperature indicators

- 6.4 Traceability & safety

- 6.4.1 RFID tags

- 6.4.2 QR codes

- 6.4.3 Tamper evident packaging

- 6.5 Consumer engagement

- 6.5.1 Interactive packaging

- 6.5.2 Smart labels

Chapter 7 Market Estimates and Forecast, By Packaging Material, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Plastics

- 7.2.1 Polyethylene (PE)

- 7.2.2 Polypropylene (PP)

- 7.2.3 Polyethylene Terephthalate (PET)

- 7.3 Paper & paperboard

- 7.3.1 Corrugated paperboard

- 7.3.2 Cartons

- 7.4 Glass

- 7.4.1 Bottles

- 7.4.2 Jars

- 7.5 Metals

- 7.5.1 Cans

- 7.5.2 Foils

- 7.6 Biodegradable materials

- 7.6.1 Starch-based materials

- 7.6.2 Polylactic acid (PLA)

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food & beverages

- 8.2.1 Perishable foods

- 8.2.2 Processed foods

- 8.2.3 Beverages

- 8.2.4 Bakery and confectionery

- 8.3 Pharmaceuticals & healthcare

- 8.3.1 Medicines

- 8.3.2 Medical devices

- 8.3.3 Nutraceuticals

- 8.4 Personal care & cosmetics

- 8.4.1 Skincare products

- 8.4.2 Haircare products

- 8.4.3 Cosmetics

- 8.5 Consumer electronics

- 8.5.1 Mobile phones

- 8.5.2 Wearable devices

- 8.5.3 Accessories

- 8.6 Logistics & supply chain

- 8.6.1 Warehousing

- 8.6.2 Transportation

- 8.6.3 Retail

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3M Company

- 10.2 Amcor Ltd.

- 10.3 Avery Dennison Corporation

- 10.4 CCL Industries Inc.

- 10.5 Coveris Holdings S.A.

- 10.6 Constantia Flexibles Group GmbH

- 10.7 Dai Nippon Printing Co., Ltd.

- 10.8 DuPont de Nemours, Inc.

- 10.9 Huhtamaki Oyj

- 10.10 Mondi plc

- 10.11 Multisorb Technologies, Inc.

- 10.12 Sealed Air Corporation

- 10.13 Sonoco Products Company

- 10.14 Stora Enso Oyj