|

시장보고서

상품코드

1936607

자동차용 프리미엄 타이어 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Premium Tires Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

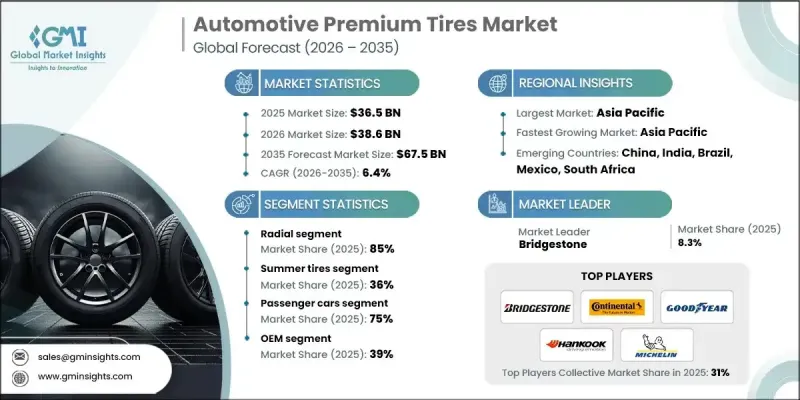

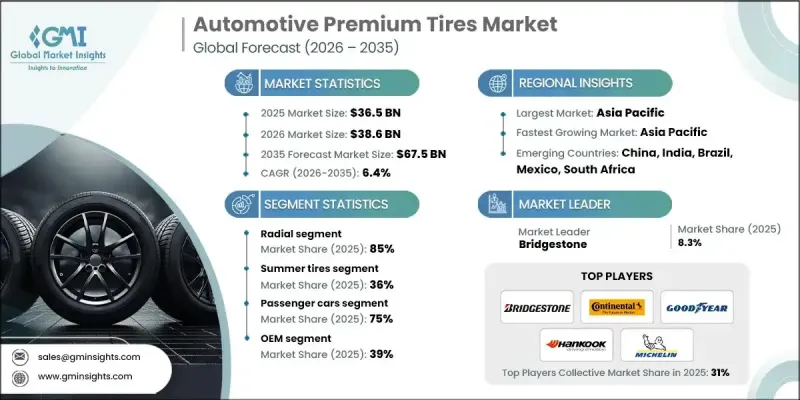

세계의 자동차용 프리미엄 타이어 시장은 2025년에 365억 달러로 평가되었으며, 2035년까지 CAGR 6.4%로 성장하여 675억 달러에 달할 것으로 예측됩니다.

이러한 성장은 고급 승용차 및 다목적 차량(유틸리티 차량)의 판매 증가와 우수한 접지력, 고속 안정성, 세련된 승차감을 제공하는 타이어에 대한 OEM 수요 증가에 힘입은 바 큽니다. 자동차 제조업체들은 현재 프리미엄 타이어를 전체 차량 성능에 필수적인 요소로 인식하고 있으며, 이는 기준 수요를 유지하고 장기적인 고부가가치 공급 계약을 뒷받침하고 있습니다. 소비자들은 제동 효율, 젖은 노면에서의 트랙션, 저소음, 고속 주행 시 안정성에 대한 인식이 높아지고 있습니다. 프리미엄 타이어는 첨단 트레드 패턴과 설계된 고무 배합을 통해 이러한 기대에 부응하고, 고객이 공장 장착 타이어에서 업그레이드하고 높은 교체 비용을 감수하도록 유도하고 있습니다. 이러한 추세는 OEM 수요와 교체 수요를 모두 강화하여 프리미엄 타이어를 선택적 구매가 아닌 가치 중심의 부문으로 자리매김하고 있습니다. 북미와 유럽에서는 차량 노후화로 인해 교체용 타이어 수요의 안정적 사이클이 유지되고 있습니다. 고급차 소유주들은 순정 타이어와 동등하거나 그 이상의 성능을 가진 교체용 타이어를 선택하는 경향이 증가하고 있으며, 이는 애프터마켓의 수익 성장을 촉진하고 성숙한 자동차 시장 전체에서 고성능 타이어 솔루션에 대한 수요를 안정화시키고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 365억 달러 |

| 예측 금액 | 675억 달러 |

| CAGR | 6.4% |

레이디얼 타이어 부문은 2025년 85%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 6.9%의 성장률로 2026년부터 2035년까지 핸들링 정확도, 내구성, 구름 저항 감소 등의 장점에 힘입어 성장할 것으로 예측됩니다. OEM 업체들은 특히 효율성과 승차감이 설계의 중요한 우선순위가 되는 고급차 및 성능 중심 모델에서 레이디얼 타이어의 표준화를 지속적으로 추진하고 있습니다.

여름용 타이어 부문은 2025년 36%의 점유율을 차지했으며, 2035년까지 연평균 5.1%의 성장률을 기록할 것으로 예상됩니다. 이 타이어는 온화한 기후 조건에 맞게 설계되어 고속 주행 시 견인력, 조향 응답성, 안정성을 우선시하며 고급 자동차의 포지셔닝에 부합하는 정교한 주행 경험을 제공합니다.

미국 자동차 프리미엄 타이어 시장은 2025년 81억 8,000만 달러에 달했습니다. 국내 시장이 전기자동차 및 대형차종으로 전환하면서 낮은 구름저항, 강화된 적재 능력, 효과적인 소음 제어 기능을 갖춘 프리미엄 타이어에 대한 수요가 증가하고 있습니다. 구매자는 트레드 수명, 에너지 효율성 및 모든 조건에서 성능을 점점 더 중요시하고 있으며, 제조업체는 OEM 및 교체 채널에서 전문 프리미엄 타이어 제품군을 확장하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 타이어별, 2022-2035

제6장 시장 추정 및 예측 : 타이어 구조별, 2022-2035

제7장 시장 추정 및 예측 : 차량별, 2022-2035

제8장 시장 추정 및 예측 : 림 사이즈별, 2022-2035

제9장 시장 추정 및 예측 : 기술별, 2022-2035

제10장 시장 추정 및 예측 : 판매 채널별, 2022-2035

제11장 시장 추정 및 예측 : 지역별, 2022-2035

제12장 기업 개요

KSM 26.03.05The Global Automotive Premium Tires Market was valued at USD 36.5 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 67.5 billion by 2035.

Growth is strongly supported by rising sales of high-end passenger vehicles and utility vehicles, along with increasing OEM demand for tires that deliver superior grip, high-speed stability, and refined ride quality. Automakers now position premium tires as an integral part of overall vehicle performance, which sustains baseline demand and supports long-term, higher-value supply agreements. Consumers show heightened awareness of braking efficiency, traction on wet surfaces, reduced road noise, and stability at elevated speeds. Premium tires address these expectations through advanced tread patterns and engineered rubber blends, encouraging customers to upgrade from factory-fitted tires and accept higher replacement costs. This behavior strengthens both OEM and replacement demand and reinforces premium tires as a value-driven segment rather than a discretionary purchase. In North America and Europe, an aging vehicle fleet supports a consistent cycle of replacement tire demand. Owners of premium vehicles increasingly choose replacement tires that match or exceed original specifications, which drives aftermarket revenue growth and stabilizes demand for high-performance tire solutions across mature automotive markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36.5 Billion |

| Forecast Value | $67.5 Billion |

| CAGR | 6.4% |

The radial tires segment held an 85% share in 2025 and is forecasted to grow at a CAGR of 6.9% from 2026 to 2035, supported by advantages in handling precision, durability, and reduced rolling resistance. OEMs continue to standardize radial tires across luxury and performance-focused models, particularly as efficiency and ride quality become critical design priorities.

The summer tire segment held a 36% share in 2025 and is expected to grow at a CAGR of 5.1% through 2035. These tires are engineered for warm-weather conditions and prioritize traction, steering response, and stability at higher speeds, delivering a refined driving experience that aligns with premium vehicle positioning.

US Automotive Premium Tires Market reached USD 8.18 billion in 2025. As the domestic market shifts toward electric vehicles and larger vehicle formats, demand is rising for premium tires that offer low rolling resistance, enhanced load capacity, and effective noise control. Buyers increasingly value tread life, energy efficiency, and all-condition performance, prompting manufacturers to expand specialized premium tire offerings across OEM and replacement channels.

Key companies operating in the Global Automotive Premium Tires Market include Michelin, Bridgestone, Goodyear Tire & Rubber Company, Continental, Pirelli, Hankook Tire & Technology, Yokohama Rubber Company, Sumitomo Rubber Industries (Dunlop), Apollo Tyres, and Cooper Tire & Rubber Company. Companies in the automotive premium tires market focus on product innovation, OEM collaboration, and portfolio diversification to strengthen their competitive position. Manufacturers invest heavily in advanced materials and compound technologies to improve durability, efficiency, and ride comfort. Strategic partnerships with automakers help secure long-term supply contracts and early inclusion in new vehicle platforms. Firms also expand premium replacement tire ranges to capture higher-margin aftermarket demand. Geographic expansion and localized production reduce supply chain risk and enhance responsiveness to regional demand trends.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Tire

- 2.2.3 Tire construction

- 2.2.4 Rim size

- 2.2.5 Vehicle

- 2.2.6 Technology

- 2.2.7 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising luxury & performance vehicle demand

- 3.2.1.2 Focus on safety, comfort & handling

- 3.2.1.3 Growing vehicle parc in developed markets

- 3.2.1.4 OEM premium positioning

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High price sensitivity limiting adoption in cost-conscious markets

- 3.2.2.2 Volatility in raw material prices impacting margins

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding premium vehicle sales in emerging economies

- 3.2.3.2 EV-specific tire demand

- 3.2.3.3 Aftermarket customization demand

- 3.2.3.4 Smart & sustainable tires

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Department of Transportation (DOT) Standards

- 3.4.1.2 Occupational Safety and Health Administration (OSHA) Guidelines

- 3.4.1.3 U.S. Environmental Protection Agency (EPA)

- 3.4.2 Europe

- 3.4.2.1 EN ISO Tire Standards

- 3.4.2.2 European Union Customs and Safety Regulations

- 3.4.2.3 BS EN / CEN Standards

- 3.4.2.4 National Standards (UNE, DIN, etc.)

- 3.4.3 Asia Pacific

- 3.4.3.1 China GB (Guobiao) Standards

- 3.4.3.2 Japan JIS Requirements

- 3.4.3.3 Korea KS Certification

- 3.4.3.4 Indian BIS Standards

- 3.4.3.5 Thai Industrial Standards Institute (TISI)

- 3.4.4 Latin America

- 3.4.4.1 INMETRO (National Institute of Metrology)

- 3.4.4.2 INTI certification (Instituto Nacional de Tecnologia Industrial)

- 3.4.4.3 NOM standards (Norma Oficial Mexicana)

- 3.4.5 Middle East & Africa

- 3.4.5.1 ESMA / Emirates Conformity Assessment Scheme (ECAS)

- 3.4.5.2 GCC technical regulations

- 3.4.5.3 SABS certification

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 EV-Specific Tire Economics & Design Trade-offs

- 3.13.1 Rolling resistance vs durability trade-offs

- 3.13.2 Acoustic foam cost premium

- 3.13.3 Impact on ASP and margins

- 3.13.4 EV vs ICE replacement economics

- 3.14 Raw Material Risk & Cost Sensitivity Analysis

- 3.15 Channel-Level Margin & Pricing Analysis

- 3.16 Consumer Behavior & Premium Adoption Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Tire, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Summer tires

- 5.3 Winter tires

- 5.4 All-season tires

- 5.5 All terrain tires

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Tire Construction, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Radial

- 6.3 Bias

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV (Light commercial vehicle)

- 7.3.2 MCV (Medium commercial vehicle)

- 7.3.3 HCV (Heavy commercial vehicle)

Chapter 8 Market Estimates & Forecast, By Rim Size, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Below 15 inches

- 8.3 15-20 inches

- 8.4 Above 20 inches

Chapter 9 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Run-flat technology

- 9.3 Self-sealing tires

- 9.4 Eco-friendly tires

- 9.5 Noise reduction technology

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Poland

- 11.3.9 Romania

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Apollo Tyres

- 12.1.2 Bridgestone

- 12.1.3 Continental

- 12.1.4 Cooper Tire & Rubber Company

- 12.1.5 Goodyear Tire & Rubber Company

- 12.1.6 Hankook Tire & Technology

- 12.1.7 Kumho Tire

- 12.1.8 Michelin

- 12.1.9 Pirelli

- 12.1.10 Sumitomo Rubber Industries

- 12.1.11 Toyo Tire

- 12.1.12 Yokohama Rubber Company

- 12.2 Regional players

- 12.2.1 CEAT

- 12.2.2 Giti Tire

- 12.2.3 JK Tyre & Industries

- 12.2.4 Linglong Tire

- 12.2.5 Maxxis International

- 12.2.6 MRF Tyres

- 12.2.7 Nexen Tire

- 12.2.8 Nokian Tyres

- 12.2.9 Sailun

- 12.3 Emerging players

- 12.3.1 Double Coin

- 12.3.2 Laufenn

- 12.3.3 Petlas

- 12.3.4 Radar Tires

- 12.3.5 Triangle Tyre

- 12.3.6 ZC Rubber