|

시장보고서

상품코드

1959318

항공우주용 고성능 열가소성 플라스틱 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)High-Performance Thermoplastics in Aerospace Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

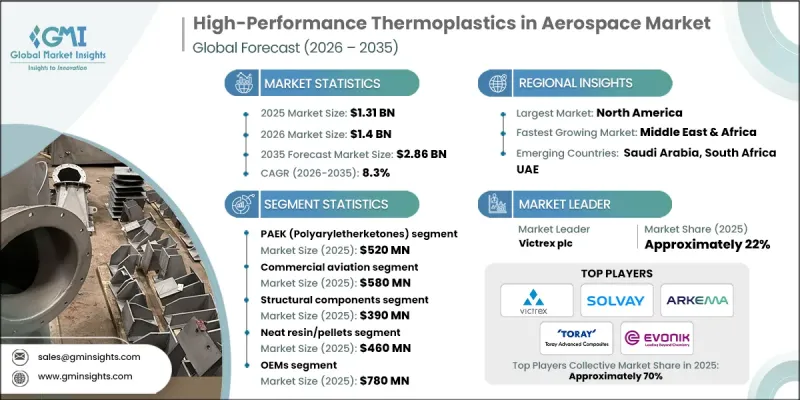

세계의 항공우주용 고성능 열가소성 플라스틱 시장은 2025년에 13억 1,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR)8.3%로 성장하여 28억 6,000만 달러에 이를 것으로 예측되고 있습니다.

시장 성장의 배경에는 항공우주 산업에서 경량 및 고강도 소재에 대한 수요 증가가 있습니다. 이러한 재료는 연료 효율을 높이고 운영 비용을 절감하는 데 기여합니다. 항공우주 제조업체들은 기존의 금속 및 열경화성 플라스틱에서 고성능 열가소성 플라스틱으로의 전환을 추진하고 있습니다. 이 폴리머는 우수한 열 안정성, 기계적 강도, 내식성을 제공함과 동시에 항공기 전체 무게를 줄일 수 있습니다. 첨단 고분자 과학의 발전으로 이러한 재료의 내구성과 성능이 향상되어 중요한 구조 부품에 적용될 수 있게 되었습니다. 또한, 지속가능성에 대한 관심과 배출 규제 강화로 인해 환경 부하가 적은 재생 가능한 열가소성 플라스틱의 채택이 촉진되고 있습니다. 이 소재들은 극한의 온도와 가혹한 화학적 환경에도 견딜 수 있는 능력을 가지고 있어 민간항공, 국방, 비즈니스 항공 분야에서 더 긴 수명, 유지보수 주기 감소, 신뢰성 향상을 실현합니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 13억 1,000만 달러 |

| 예측 금액 | 28억 6,000만 달러 |

| CAGR | 8.3% |

PAEK(폴리알릴 에테르 케톤) 부문은 2025년 5억 2,000만 달러 시장 규모를 기록할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.8%를 나타낼 것으로 예측됩니다. PAEK 소재는 높은 내열성과 까다로운 기계적 성능이 요구되는 항공우주 분야에서 점점 더 선호되고 있습니다. 내화학성 및 내열성으로 인해 구조 부품 및 반구조 부품에 이상적입니다. 마찬가지로, 폴리이미드는 엔진 주변이나 기타 고온 영역과 같이 극한의 열에 노출되는 영역에서 뛰어난 치수 안정성과 내열성으로 인해 주목받고 있습니다. 이러한 소재의 고유한 특성으로 인해 항공우주 엔지니어들은 가혹한 운항 조건을 견딜 수 있는 더 가볍고 효율적인 항공기를 설계할 수 있게 되었습니다.

민간 항공 분야는 2025년 5억 8,000만 달러 규모에 달할 것으로 예상되며, 2026년부터 2035년까지 연평균 7.9%의 성장률을 보일 것으로 전망됩니다. 항공기 제조 증가, 기체 현대화 및 효율성 향상으로 인해 항공기 구조, 인테리어 및 탑재 시스템용 고성능 열가소성 수지에 대한 수요가 증가하고 있습니다. 군용 및 국방 항공 분야도 성장에 기여하고 있으며, 이들 분야에서는 가혹한 운용 환경을 견디면서 긴 수명을 구현하는 소재가 요구되고 있습니다. 비즈니스 항공 및 일반 항공 플랫폼은 기존 항공우주 소재의 복잡성과 비용 문제를 해결하기 위해 성능 향상과 제조 공정 간소화를 위한 첨단 열가소성 수지의 사용이 증가하고 있습니다.

북미 항공우주용 고성능 열가소성 수지 시장은 2025년 4억 9,000만 달러 규모에 달할 것으로 예측됩니다. 이 지역 시장 확대는 첨단 항공기 생산, 연구개발을 통한 지속적인 소재 혁신, 자동화 제조 기술의 조기 도입에 의해 촉진되고 있습니다. 북미는 항공우주 공급망과 차세대 항공기 프로그램에 대한 지속적인 투자의 혜택을 누리고 있습니다. 미국은 민간 항공기 납품 증가, 군사 현대화 프로그램, 구조 및 시스템 부품에 경량 고성능 열가소성 플라스틱의 통합으로 이 지역의 성장을 주도하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 소재 유형별, 2022-2035

제6장 시장 추산 및 예측 : 항공기 플랫폼별, 2022-2035

제7장 시장 추산 및 예측 : 부품 유형별, 2022-2035

제8장 시장 추산 및 예측 : 제품 유형별, 2022-2035

제9장 시장 추산 및 예측 : 제조 공정별, 2022-2035

제10장 시장 추산 및 예측 : 최종사용자별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.03.18The Global High-Performance Thermoplastics in Aerospace Market was valued at USD 1.31 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 2.86 billion by 2035.

Market growth is driven by the aerospace industry's increasing need for lightweight, high-strength materials that can improve fuel efficiency and reduce operational costs. Aerospace manufacturers are progressively replacing traditional metals and thermosets with high-performance thermoplastics, as these polymers offer superior thermal stability, mechanical strength, and corrosion resistance while reducing overall aircraft weight. The development of advanced polymer science has enhanced the durability and performance of these materials, making them suitable for critical structural components. Sustainability concerns and stricter emissions regulations are also pushing the adoption of recyclable thermoplastics with lower environmental impact. Their ability to endure extreme temperatures and harsh chemical environments ensures longer service life, fewer maintenance cycles, and increased reliability across commercial, defense, and business aviation applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.31 Billion |

| Forecast Value | $2.86 Billion |

| CAGR | 8.3% |

The PAEK (Polyaryletherketones) segment generated USD 0.52 billion in 2025 and is estimated to grow at a CAGR of 7.8% between 2026 and 2035. PAEK materials are increasingly preferred for aerospace applications requiring high thermal tolerance and demanding mechanical performance. Their chemical and thermal resilience make them ideal for structural and semi-structural components. Similarly, polyimides are gaining traction in regions exposed to extreme heat, such as areas near engines or other high-temperature zones, due to their exceptional dimensional stability and heat resistance. The unique properties of these materials enable aerospace engineers to design lighter and more efficient aircraft capable of withstanding rigorous operating conditions.

The commercial aviation segment reached USD 0.58 billion in 2025 and is expected to grow at a CAGR of 7.9% from 2026 to 2035. The rise in aircraft manufacturing, fleet modernization, and the push for improved efficiency are driving demand for high-performance thermoplastics in airframes, interiors, and onboard systems. Military and defense aviation is also contributing to growth, as these sectors demand materials capable of enduring harsh operational conditions while offering long service life. Business and general aviation platforms are increasingly utilizing advanced thermoplastics to enhance performance and simplify manufacturing processes, addressing the complexity and cost of traditional aerospace materials.

North America High-Performance Thermoplastics in Aerospace Market accounted for USD 0.49 billion in 2025. Market expansion in the region is fueled by advanced aircraft production, continuous material innovation through research and development, and early adoption of automated manufacturing technologies. North America benefits from a well-established aerospace supply chain and ongoing investment in next-generation aircraft programs. The U.S. is leading regional growth due to rising commercial aircraft deliveries, military modernization programs, and the integration of lightweight, high-performance thermoplastics in both structural and system components.

Key players operating in the Global High-Performance Thermoplastics in Aerospace Market include Solvay Special Chemicals, Victrex plc, Toray Advanced Composites, Evonik Industries AG, Arkema S.A., and several others. Companies in the high-performance thermoplastics in the aerospace market are focusing on strategic growth initiatives to strengthen their market foothold. They are investing heavily in research and development to create advanced thermoplastic materials with higher thermal tolerance, mechanical strength, and chemical resistance to meet evolving aerospace demands. Expanding production capabilities and forming partnerships with aerospace OEMs allow companies to integrate their solutions into cutting-edge aircraft designs. Firms are also emphasizing sustainability by developing recyclable materials with lower environmental impact, improving lifecycle performance, and reducing maintenance needs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Aircraft Platform

- 2.2.4 Component Type

- 2.2.5 Product Type

- 2.2.6 Manufacturing Process

- 2.2.7 End-User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 PAEK (Polyaryletherketones)

- 5.2.1 PEEK (Polyetheretherketone)

- 5.2.2 PEKK (Polyetherketoneketone)

- 5.2.3 LM-PAEK (Low-Melt PAEK)

- 5.3 Polyimides

- 5.3.1 PEI (Polyetherimide/Ultem)

- 5.3.2 PAI (Polyamideimide)

- 5.4 Polysulfones

- 5.5 PPS (Polyphenylene Sulfide)

- 5.6 Other High-Performance Thermoplastics

Chapter 6 Market Estimates and Forecast, By Aircraft Platform, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Commercial Aviation

- 6.2.1 Narrow-Body Aircraft

- 6.2.2 Wide-Body Aircraft

- 6.3 Military & Defense Aviation

- 6.3.1 Fighter Aircraft

- 6.3.2 Military Transport Aircraft

- 6.3.3 Military Helicopters

- 6.4 Business & General Aviation

- 6.5 Space Applications

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Structural Components

- 7.2.1 Primary Structures

- 7.2.2 Secondary Structures

- 7.3 Interior Components

- 7.3.1 Seats & Seat Frames

- 7.3.2 Galleys & Lavatories

- 7.3.3 Overhead Stow Bins

- 7.3.4 Sidewall & Ceiling Panels

- 7.3.5 Window Reveals & Trim

- 7.4 Engine & Propulsion Components

- 7.4.1 Nacelles & Engine Cowlings

- 7.4.2 Thrust Reversers

- 7.4.3 Ducts & Air Management Systems

- 7.4.4 Fan Blades & Acoustic Liners

- 7.5 Electrical & Electronic Housings

- 7.5.1 Radomes & Antenna Housings

- 7.5.2 Avionics Enclosures

- 7.5.3 Cable Management Systems

- 7.5.4 EMI/RFI Shielding Requirements

- 7.6 Transparencies & Windows

- 7.6.1 Aircraft Windows & Windshields

- 7.6.2 Canopies (Military Applications)

- 7.6.3 Polycarbonate vs. Acrylic Analysis

- 7.7 Leading Edges & Aerodynamic Surfaces

- 7.7.1 Wing Leading Edges

- 7.7.2 Control Surfaces

- 7.7.3 Aerodynamic Fairings

Chapter 8 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Neat Resin/Pellets

- 8.3 Prepregs

- 8.3.1 Unidirectional (UD) Tape

- 8.3.2 Woven Fabric Prepregs

- 8.4 Semi-Finished Products

- 8.4.1 Sheets & Laminates

- 8.4.2 Films & Membranes

- 8.4.3 Profiles & Extruded Shapes

- 8.5 Finished Parts/Components

Chapter 9 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Automated Fiber Placement (AFP) & Automated Tape Placement (ATP)

- 9.3 Compression Molding & Stamp Forming

- 9.4 Thermoforming

- 9.5 Injection Molding

- 9.6 Additive Manufacturing (AM)

- 9.7 Welding & Joining Technologies

- 9.7.1 Resistance Welding

- 9.7.2 Induction Welding

- 9.7.3 Ultrasonic Welding

- 9.7.4 Laser Welding

- 9.8 Continuous Compression Molding (CCM)

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 OEMs (Original Equipment Manufacturers)

- 10.3 MRO (Maintenance, Repair & Overhaul) Providers

- 10.4 Research Institutions & Academia

- 10.5 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East & Africa

Chapter 12 Company Profiles

- 12.1 Victrex plc

- 12.2 Solvay Special Chemicals

- 12.3 Arkema S.A.

- 12.4 Evonik Industries AG

- 12.5 SABIC

- 12.6 BASF SE

- 12.7 Envalior

- 12.8 Toray Advanced Composites

- 12.9 Teijin Limited

- 12.10 Celanese Corporation

- 12.11 Mitsubishi Chemical Group

- 12.12 Rochling Group

- 12.13 Syensqo

- 12.14 Ensinger GmbH