|

시장보고서

상품코드

1959565

자동차용 NFC 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive NFC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

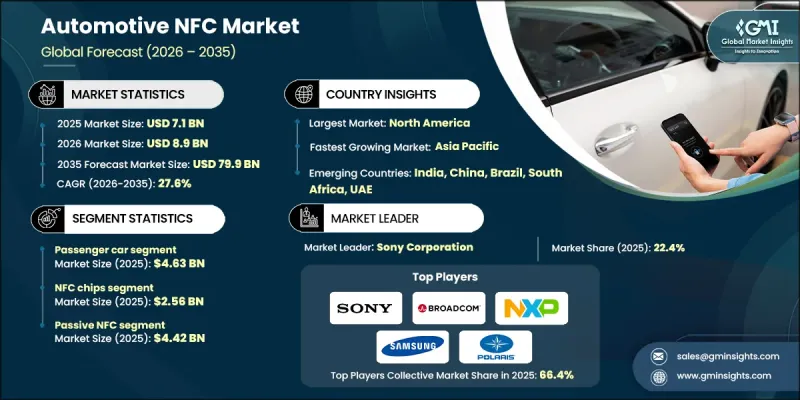

세계의 자동차용 NFC 시장은 2025년에 71억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 27.6%로 성장하여 799억 달러에 이를 것으로 예측되고 있습니다.

시장 확대의 배경에는 커넥티드카 및 소프트웨어 정의 차량으로의 빠른 전환과 주요 디지털 액세스 도구로서 스마트폰에 대한 소비자의 의존도가 높아진 것이 있습니다. 자동차 제조업체들은 기존의 기계식 키를 NFC 지원 디지털 키로 대체하는 움직임을 가속화하여 차량 접근을 보다 안전하고 유연하며 사용자 중심의 경험으로 전환하고 있습니다. NFC 기반 액세스를 통해 운전자는 인증된 스마트 기기를 사용하여 차량의 잠금 해제, 시동 및 관리를 할 수 있으며, 보안을 손상시키지 않으면서도 액세스 권한 공유를 제어할 수 있습니다. NFC 칩, 보안 요소, 암호화 기술의 발전으로 인증 기준이 강화되어 더욱 엄격한 자동차 안전 규정과 도난 방지 규정을 준수하고 있습니다. 디지털 관리형 모빌리티의 매력과 일상적인 디지털 라이프 스타일에 대한 완벽한 통합이 결합되면서 NFC는 차세대 차량 출입 및 ID 관리의 핵심 기술로서 그 중요성이 더욱 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 71억 달러 |

| 예측 금액 | 799억 달러 |

| CAGR | 27.6% |

디지털 차량 액세스는 진화하는 모빌리티 모델을 지원하고, 승용차 및 상용차의 사용자 경험을 향상시킵니다. 스마트폰 기반 액세스는 편의성과 중앙 집중식 디지털 제어에 대한 소비자의 기대에 따라 추가 하드웨어에 대한 의존도를 줄이면서 현대의 커넥티드 서비스를 지원합니다. 차량이 디지털 생태계의 연장선상에 있는 만큼, NFC 기반 액세스 솔루션은 ID 관리, 권한 관리, 개인화를 위한 최적의 선택이 되고 있습니다.

승용차 부문은 2025년 46억 3,000만 달러에 달했습니다. 이 부문 수요는 다중 사용자 환경을 지원하는 안전하고 편리한 액세스 솔루션에 대한 소비자의 선호에 의해 주도되고 있습니다. NFC 지원 디지털 키는 개인화를 강화하고, 암호화 인증을 통해 보안을 강화하며, 표준화가 진행됨에 따라 자동차 제조업체의 폭넓은 채택을 촉진하고 있습니다.

NFC 칩 부문은 2025년 25억 6,000만 달러 시장 규모를 기록했습니다. 이 부품들은 비교적 저렴한 비용으로 근접 접근과 안전한 시스템 페어링을 실현하며, 양산차부터 고급차까지 다양한 차량에 통합될 수 있도록 지원합니다. 칩의 효율성, 호환성, 성능의 지속적인 향상으로 도입 기회가 확대되고 있으며, 자동차 등급 보안 표준 준수는 공급업체에게 중요한 차별화 요소로 작용하고 있습니다.

북미 자동차 NFC 시장은 2025년 38.5%의 점유율을 차지할 것으로 예측됩니다. 이 지역은 높은 커넥티드카 보급률, 첨단 디지털 인프라, 스마트폰 기반 액세스 기술에 대한 소비자의 높은 수용성이라는 이점을 가지고 있습니다. 기존의 자동차 생태계와 안전하고 편리한 차량 기능에 대한 수요가 결합되어 모든 차종에서 NFC의 빠른 통합을 지속적으로 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 차종별, 2022-2035

제6장 시장 추산 및 예측 : 유형별, 2022-2035

제7장 시장 추산 및 예측 : 기술별, 2022-2035

제8장 시장 추산 및 예측 : 접속 방식별, 2022-2035

제9장 시장 추산 및 예측 : 용도별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

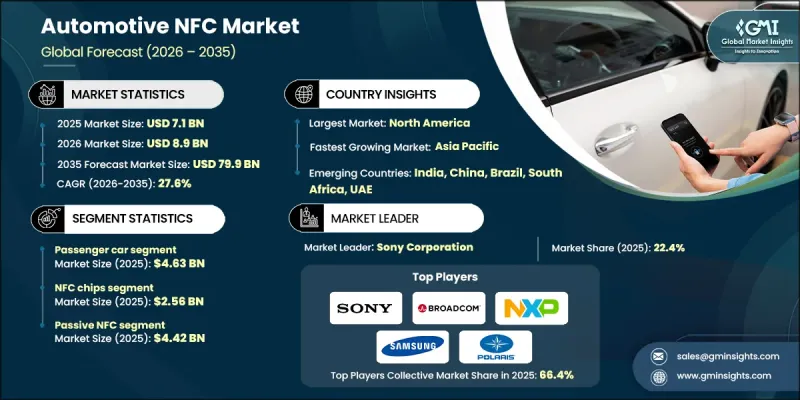

LSH 26.03.18The Global Automotive NFC Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 27.6% to reach USD 79.9 billion by 2035.

Market expansion is driven by the rapid shift toward connected and software-defined vehicles, alongside growing consumer reliance on smartphones as primary digital access tools. Automakers are increasingly replacing conventional mechanical keys with NFC-enabled digital keys, transforming vehicle access into a more secure, flexible, and user-controlled experience. NFC-based access allows drivers to unlock, start, and manage vehicles using authorized smart devices, while also enabling controlled sharing of access without compromising security. Advances in NFC chips, secure elements, and encryption technologies are strengthening authentication standards and aligning with stricter automotive safety and anti-theft regulations. The growing appeal of digitally managed mobility, combined with seamless integration into everyday digital lifestyles, is reinforcing NFC as a core enabler of next-generation vehicle access and identity management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $79.9 Billion |

| CAGR | 27.6% |

Digital vehicle access also supports evolving mobility models and enhances the user experience across passenger and commercial vehicles. Smartphone-based access aligns with consumer expectations for convenience and centralized digital control, reducing dependence on additional hardware while supporting modern connected services. As vehicles increasingly function as extensions of digital ecosystems, NFC-based access solutions are becoming a natural fit for managing identity, permissions, and personalization.

The passenger car segment reached USD 4.63 billion in 2025. Demand in this segment is fueled by consumer preference for secure and convenient access solutions that support multi-user environments. NFC-enabled digital keys enhance personalization, improve security through encrypted authentication, and are increasingly standardized, which encourages wider adoption by vehicle manufacturers.

The NFC chips segment generated USD 2.56 billion in 2025. These components enable proximity-based access and secure system pairing at a relatively low cost, supporting integration across both mass-market and premium vehicles. Continuous improvements in chip efficiency, compatibility, and performance are expanding deployment opportunities, while compliance with automotive-grade security standards remains a key differentiator for suppliers.

North America Automotive NFC Market held 38.5% share in 2025. The region benefits from strong adoption of connected vehicles, advanced digital infrastructure, and high consumer acceptance of smartphone-based access technologies. A well-established automotive ecosystem, combined with demand for secure and convenient vehicle features, continues to support rapid NFC integration across vehicle categories.

Key players operating in the Global Automotive NFC Market include NXP Semiconductors N.V., Qualcomm Inc., Infineon Technologies AG, Samsung Electronics Co. Ltd., Sony Corporation, STMicroelectronics N.V., Texas Instruments, Renesas, Murata Manufacturing Co., Intel Corporation, Broadcom, MediaTek Inc., Panasonic Corporation, Robert Bosch GmbH, Marvell Technology Inc., Verimatrix, Nordic Semiconductor, MagTek Inc., Polaris, and FeliCa Networks, Inc. Companies in the Automotive NFC Market are strengthening their competitive position by investing heavily in secure hardware design, encryption technologies, and compliance with automotive-grade safety standards. Strategic collaborations with automakers, Tier-1 suppliers, and software platform providers help accelerate integration into next-generation vehicle architectures. Firms also focus on standardization initiatives to ensure interoperability across devices and ecosystems. Expanding product portfolios to support digital keys, in-vehicle payments, and personalized user profiles enables revenue diversification.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Vehicle type trends

- 2.2.2 Type trends

- 2.2.3 Technology trends

- 2.2.4 Connectivity trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million & Units)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of digital car keys

- 3.2.1.2 Increasing demand for connected and software-defined vehicles

- 3.2.1.3 Growing consumer preference for smartphone-based vehicle access

- 3.2.1.4 Advancements in NFC chip and secure element technology

- 3.2.1.5 Stringent automotive security and anti-theft regulations

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High implementation cost for OEMs

- 3.2.2.2 Compatibility issues across devices and platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Economy

- 5.2.2 Mid-range

- 5.2.3 Luxury

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles (LCVs)

- 5.3.2 Heavy commercial vehicles (HCVs)

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 NFC tags

- 6.3 NFC readers

- 6.4 NFC chips

- 6.5 NFC controllers

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Active NFC

- 7.3 Passive NFC

Chapter 8 Market Estimates and Forecast, By Connectivity, 2022 - 2035 (USD Million & Units)

- 8.1 Key Trends

- 8.2 Active NFC

- 8.3 Passive NFC

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Keyless Entry

- 9.3 Infotainment Systems

- 9.4 Payment Systems

- 9.5 Access Control

- 9.6 Bluetooth Pairing

- 9.7 Vehicle Communication

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 NXP Semiconductors N.V.

- 11.1.2 Broadcom

- 11.1.3 Qualcomm Inc.

- 11.1.4 Intel Corporation

- 11.1.5 Infineon Technologies AG

- 11.1.6 STMicroelectronics N.V.

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Texas Instruments

- 11.2.1.2 Polaris

- 11.2.1.3 Marvell Technology Inc.

- 11.2.1.4 MagTek Inc.

- 11.2.2 Europe

- 11.2.2.1 Robert Bosch GmbH

- 11.2.2.2 Verimatrix

- 11.2.2.3 Nordic Semiconductor

- 11.2.3 Asia Pacific

- 11.2.3.1 Sony Corporation

- 11.2.3.2 Samsung Electronics Co. Ltd.

- 11.2.3.3 Panasonic Corporation

- 11.2.3.4 MediaTek Inc.

- 11.2.3.5 Reneses

- 11.2.3.6 Murata Manufacturing Co.

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 FeliCa Networks, Inc